Sample Category Title

Aussie Dollar Riding Downtrend Channel Vs US Dollar

Key Highlights

- The Aussie Dollar failed to hold the 0.8000 level against the US Dollar and moved down.

- The AUD/USD pair is currently following a descending channel with resistance at 0.7900 on the 4-hours chart.

- Australia's Home Loans in June 2017 increased by 0.5%, less than the forecast of 1.5%.

- Australia's Westpac Consumer Confidence for August 2017 declined 1.2%, compared with the last +0.4%.

AUDUSD Technical Analysis

The Aussie Dollar after an impressive run towards 0.8060 against the US Dollar formed a medium-term top. The AUD/USD pair declined lately and currently riding a downtrend channel with support at 0.7850.

Looking at the 4-hour chart, there is a descending channel with resistance at 0.7900. The pair is trading well below the 0.8000 handle the 100 simple moving average (H4), which is a bearish sign.

On the upside, the channel resistance is near the 50% Fib retracement level of the last decline from the 0.7942 high to 0.7853. Therefore, the 0.7890-0.7900 area is a major hurdle an upside move.

On the downside, the pair is trading near a crucial pivot of 0.7870-0.7850. The mentioned levels are key supports, but buyers need to take the pair above 0.7900 for a bounce back.

Overall, the pair may correct higher, but it won't be easy for AUD/USD to close above 0.7900.

Australia's Home Loans

Recently in Australia, the Home Loans figure for June 2017 was released by the Australian Bureau of Statistics. The market was aligned for an increase of 1.5% compared with the previous month.

However, the actual result was disappointing, as the increase in loans was 0.5%. On the other hand, the last reading was revised up from +1% to +1.1%. The worst part was a decline of 0.9% in investment housing commitments.

The report added that:

In trend terms, the number of commitments for the construction of dwellings rose 1.9% and the number of commitments for the purchase of new dwellings rose 1.3%, while the number of commitments for the purchase of established dwellings fell 0.5%.

The AUD/USD pair recovered a few pips during the past two sessions, but faces a major hurdle on the upside at 0.7900-0.7910.

Today's NY session will see the release of the Non-farm Productivity (Q2 2017) (Prelim) by the Bureau of Labor Statistics of the US Department of Labor. The forecast is +0.7% compared with the last 0%. The Unit Labor Cost is forecasted to increase by 1.2% in Q2 2017 (Prelim), less than the last +2.2%.

Trade Idea: AUD/USD – Target met and stand aside

AUD/USD – 0.7873

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term up

Original strategy :

Sold at 0.8030, met target at 0.7880

Position: - Short at 0.8030

Target: - 0.7880

Stop: -

New strategy :

Stand aside

Position: -

Target: -

Stop:-

As aussie has fallen again after brief recovery to 0.7943, adding credence to our bearishness and our short position entered at 0.8030 finally met our downside target at 0.7880 (with 150 points profit), outlook remains mildly bearish for the erratic fall from 0.8066 top to bring retracement of recent rise in wave iv, hence weakness to 0.7839 (previous resistance tuned support) is likely, however, downside should be limited to 0.7786 and price should stay well above wave i top at 0.7712.

As we have taken profit on our short position entered at 0.8030, would not chase this fall here and would be prudent to stand aside for now. On the upside, expect recovery to be limited to 0.7940-45 and bring another decline later. Only break of indicated resistance at 0.7980 would suggest low is formed, bring a stronger rebound to 0.8000, then towards 0.8043 resistance, break there would signal the pullback from 0.8066 top has ended instead, bring retest of this level first. We are keeping our latest bullish count that recent impulsive waves is unfolding as (1 2, (i)(ii), i ii) and may extend headway towards 0.8150.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

After a dull start to the day, the greenback gather upward momentum against all of its major rivals after Wall Street's opening, with EUR/USD's decline extending down to 1.1714 before bouncing to settle around 1.1760. The US released some minor macroeconomic figures, all of them encouraging. The NFIB Index of Small Business Optimism rose 1.6 points to 105.2 in July, above June's 103.6, whilst the IBD/TIPP Economic Optimism for August climbed to 52.2 above previous 50.2, also above the 12-month average of 51. Additionally, the number of jobs´ openings increased to 6.163 million in June, beating expectations and at an all time high. Dollar's gains were exacerbated by thin trading conditions, with the currency ending the day mixed across the board.

The EUR/USD pair has bounced from a critical static support the 2015 yearly high which was set at 1.1713, and the 4 hours chart shows that it stands now well below a bearish 20 SMA, after the indicator contained advanced all through the day. Technical indicators in the mentioned time frame have bounced with different strength with the Momentum heading higher around its mid-line, but the RSI indicator holding near oversold levels, indicating that the risk remains towards the downside, particularly if the mentioned support gives up. A break below the mentioned level will open doors for a steeper correction, although seems unable that the dollar could advance much more ahead of Friday's inflation release in the US.

Support levels: 1.1715 1.1680 1.1630

Resistance levels: 1.1785 1.1820 1.1860

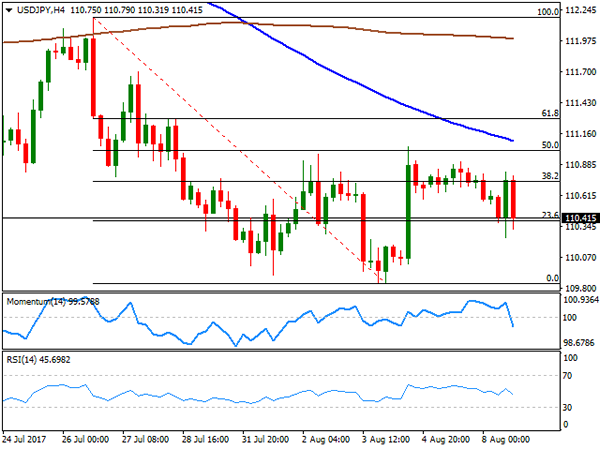

USD/JPY

The USD/JPY pair ended the day in the red around 110.40, having quickly reverted an advance up to 110.82, this last triggered by strong US employment data, as the number of open jobs reached a record high of 6.16 million at the end of June, up 461,000 from May and exceeding the expected 5.6 million. Anyway, the pair resumed its decline afterwards, retaining the bearish bias seen over the last few weeks. The pair keeps trading within Fibonacci levels, trapped most of this Tuesday between the 23.6% and the 38.2% retracement of the latest daily decline between 112.18 and 109.84, with scope to test this last on a break below the daily low of 110.24. Technical readings in the 4 hours chart support such decline as the 100 SMA extended its slide above the current level, now around 111.10, while the Momentum indicator entered bearish territory with a strong bearish slope and the RSI indicator resumed its slide after failing to surpass its mid-line, currently at 46.

Support levels: 110.25 109.85 109.50

Resistance levels: 110.70 111.05 111.40

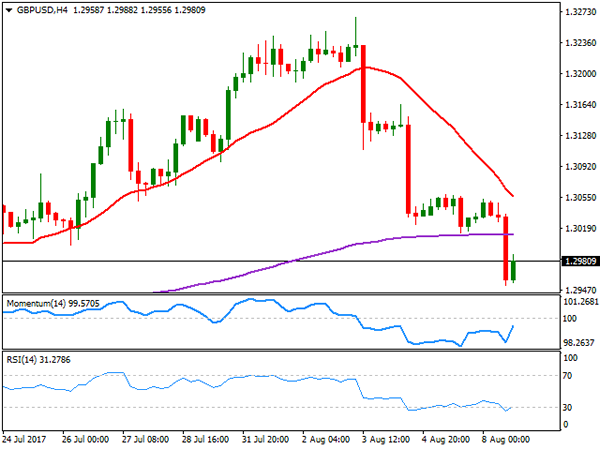

GBP/USD

The GBP/USD pair plunged to 1.2952, as a bout of dollar's buying affected the most a weakened Pound, further extending after the pair broke the critical 1.3000 support. There were no macroeconomic releases in the UK, but the Sterling became vulnerable by the end of last week, when the BOE decided to remain on-hold, and somehow suggested that a rate hike for this year is out of the table. Adding to the bearish case of the British currency is the uncertainty surrounding Brexit, with negotiations being slow and painful, and with no signs of progress. From a technical point of view, the pair has scope to fall further as long as it holds now below the mentioned psychological level, and as long as news coming from the US don't result disappointing. In the 4 hours chart, the price settled below its 200 EMA for the first time in almost a month, while the 20 SMA accelerated its decline above the current level, now reinforcing the static resistance area around 1.3060. Technical indicators in the mentioned chart have managed to bounce from oversold readings, rather reflecting the late recovery than suggesting downward exhaustion, still holding within negative territory, limiting therefore chances of a recovery.

Support levels: 1.2965 1.2920 1.2880

Resistance levels: 1.3005 1.3030 1.3060

GOLD

Spot gold settled at $1,255.79 a troy ounce, the lowest in two weeks, as the market decided to give the greenback a vote of confidence after another solid local employment report, as the number of jobs' opening hit a record high in June. The figure came after a solid US employment report for July, and should keep the Fed in the tightening path, although no rate move is expected for September. The daily chart for gold indicates and increasing bearish potential, although further confirmations are required, as technical indicators are now hovering around their mid-lines, with diminished downward strength, whilst the price settled around its 20 DMA after briefly falling below the 100 DMA. In the 4 hours chart, the price settled below both, the 20 and 100 SMAs, with the shortest gaining bearish traction, in line with further declines, whilst technical indicators have managed to bounce within negative territory, still unable to re-enter bullish ground.

Support levels: 1,251.46 1,243.75 1,235.22

Resistance levels: 1,260.10 1,267.60 1,274.05

WTI CRUDE OIL

West Texas Intermediate crude futures settled at $49.10 a barrel, down for a second consecutive day, reverting early gains on news indicating that some OPEC producers increased their output in July, with crude oil exports from the OPEC reaching a record high in July mostly due to Nigeria and Libya exports, both exempt from the agreement to limit production. Further weighing on the commodity were news showing that Libya's biggest oil field, Sharara, came back online after a short interruption on Monday. Ahead of the release of US stockpiles data, the commodity remains within a consolidative phase below the key 50.00 level, with the daily chart showing that technical indicators are retreating within positive territory, as the price remains trapped between its 100 and 200 SMAs. In the shorter term, and according to the 4 hours chart, the technical stance is neutral-to-bearish with the price a few pips below a directionless 20 SMA and technical indicators heading modestly lower within neutral territory.

Support levels: 48.50 47.90 47.20

Resistance levels: 49.65 50.20 50.85

DJIA

Having struggled around their opening levels for most of the day, US indexes finally turned south and closed in the red, amid a stronger dollar, and with healthcare and material stocks leading the way lower. The Dow Jones Industrial Average turned red after nine record closes, settling at 22,85.34, down by 33 points, while the Nasdaq Composite shed 13 points to 6,370.46. The S&P closed 6 points lower, at 2,474.92. Within the Dow, Apple was the best performer, adding 0.86%, followed by Chevron that added 0.61%. Leading decliners was El du Pont, down 0.84%, followed by Merck that shed 0.82.%. From a technical point of view, the daily chart shows that the index remains far above all of its moving averages that remain bullish, while technical indicators began correcting lower, still within overbought territory. In the 4 hours chart, the index settled a few points below its 20 SMA, whilst technical indicators have extended their declines within positive territory, now about to enter negative territory, supporting a bearish extension for this Wednesday that anyway will be seen as corrective after the latest record rally.

Support levels: 22,055 22,001 21,967

Resistance levels: 22,055 22,080 22,137

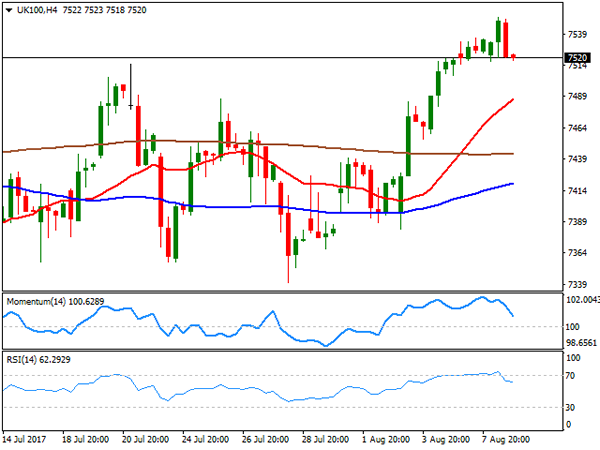

FTSE100

The FTSE 100 continued advancing this Tuesday, up 10 points to end at 7,542.73, not far below its previous record close of 7,547. A weaker Pound kept mood high among local investors, even despite earnings reports were not that encouraging. Paddy Power Betfair led decliners for a second consecutive day, down 4.11% after the bookmaker said it had suffered from "adverse sports results" in recent months, followed by InterContinental Hotels Group, down 3.99% on the day after reporting a slowdown in revenue growth. Taylor Wimpey, on the other hand, was the best performer, adding 1.93%. The index retreated in after hours trading following a late decline in US equities, heading into the Asian opening around 7,514, and with the daily chart showing that technical indicators turned lower within positive territory, as the index remains above its moving averages, these lasts, limiting chances of a steeper decline. In the 4 hours chart the index is also holding above all of its moving averages, with the 20 SMA retaining a strong bullish slope, yet technical indicators have turned sharply lower from overbought levels and are currently approaching their mid-lines, suggesting the index may extend its decline this Wednesday.

Support levels: 7,487 7,440 7,392

Resistance levels: 7,540 7,572 7,600

DAX

European equities trade mostly in the red, but the German DAX managed to shrug off the negative tone and settled at 12,292.05, up 35 points or 0.28%. Mood was undermined by poor Chinese and German trade data, as despite both economies presented wider-than-expected surplus, a decline in exports and imports triggered an alert. Helping European indexes to recover ground was EUR's weakness at the end of the session. Within the DAX, Continental was the best performer, adding 2.12%, followed by E.ON, still on the positive track and up by 1.91%. Banks gave back their Monday's gains, with Commerzbank leading decliners, down 1.29% and Deutsche Bank ending the day 0.58% lower. The index retains a negative tone according to the daily chart, as a bearish 20 DMA keeps capping advances, whilst technical indicators remain within negative territory, although lacking directional strength. In the 4 hours chart, the index settled above a horizontal 20 SMA but still below bearish 100 and 200 SMAs, whilst technical indicators also lack directional strength, but stand above their mid-lines.

Support levels: 12,210 12,174 12,128

Resistance levels: 12,275 12,323 12,381

Euro Subdued As Investors Look For Cues

EUR/USD continues to have a quiet week. Currently, the pair is trading at 1.1751, down 0.01% on the day. On the release front, there are no German or European indicators on the schedule. In the US, the focus is on employment numbers, with the release of Preliminary Nonfarm Productivity and Preliminary Unit Labor Costs. On Thursday, there are two key events – PPI and unemployment claims.

With the eurozone continuing to show solid growth in 2017, the ECB's quantitative easing program (QE) is coming under closer scrutiny. The scheme is scheduled to end in December, although this is not a drop-dead date – the ECB has been careful to state that QE could be extended “if necessary”. The ECB hold its next policy meeting in September 7, and there is a strong possibility that the bank will make an announcement regarding tapering QE, which could start in early 2018. The problem facing policymakers is that despite a stronger labor market and improved growth, inflation levels remain stubbornly low, as the ECB's inflation target of 2% has proven overly optimistic. The ECB is well aware that any talk of tighter policy could send the euro higher, as was the case in June, when investors snapped up euros after Mario Draghi made some hawkish comments at a meeting of central bankers. As far as interest rate moves, the ECB is unlikely to raise rates until its tapering process is well under way, meaning we're unlikely to see any rate moves before the second half of 2018.

While the euro is enjoying a revival, it's been the opposite story for the US dollar. Paralysis in Washington is weighing on the greenback, as Donald Trump's antics and inability to pass healthcare legislation has increased political risk in the US. As well, the Federal Reserve's monetary policy remains unclear. Earlier this year the Fed strongly hinted that it planned to raise rates three times in 2017, but has only pressed the rate trigger twice. In June, Fed Chair Janet Yellen shrugged off low inflation, saying that it was due to “transient” factors, leaving the impression that the Fed still planned one final hike. However, inflation has not improved and the Fed has changed its tune. Last week, St. Louis Federal Reserve President James Bullard said he opposed further Fed hikes, warning that another hike would actually delay inflation from hitting the Fed's target of 2%. The markets have become more skeptical about a rate hike in December, as the odds have fallen to 33%, compared to 43% a week ago.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

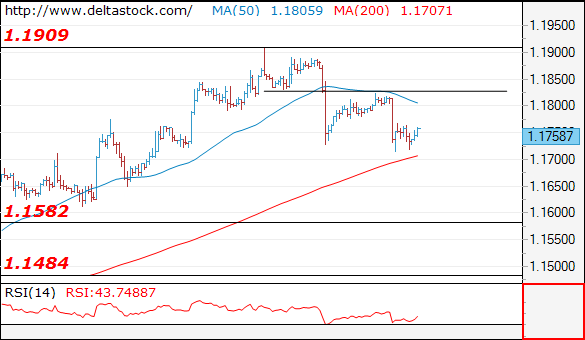

EUR/USD

Current level - 1.1758

The test at 1.1825 has failed and the pair reached a new low at 1.1713. The outlook remains negative, for an attack of 1.1650-1580 area. Minor intraday resistance lies at 1.1780.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.1780 |

1.1909 |

1.1650 |

1.1580 |

|

1.1825 |

1.2000 |

1.1580 |

1.1480 |

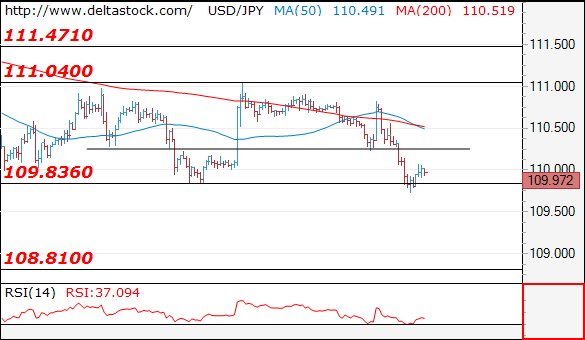

USD/JPY

Current level - 109.97

The slide through 110.25 signals a renewal of the general downtrend and the outlook is bearish, for a depreciation towards 108.80. Initial intraday resistance lies at 110.25.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

110.25 |

112.20 |

109.80 |

109.80 |

|

111.04 |

114.50 |

108.80 |

108.10 |

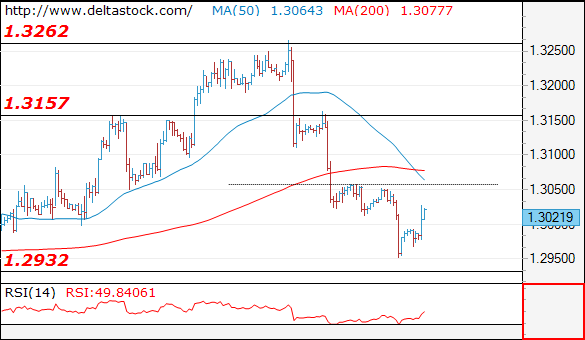

GBP/USD

Current level - 1.3021

The recent low at 1.2950 should be enough for a completion of the downtrend from 1.2360 and the intraday bias is positive above 1.3000, for a break through 1.3050, towards 1.3160.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.3050 |

1.3260 |

1.3000 |

1.2930 |

|

1.3100 |

1.3500 |

1.2930 |

1.2810 |

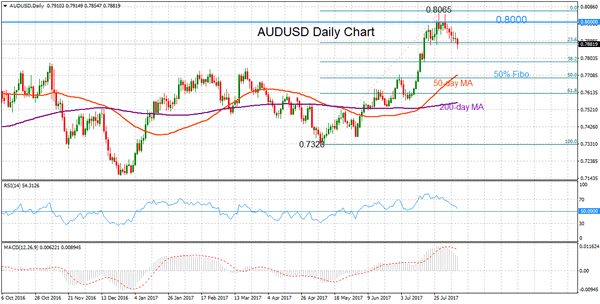

AUDUSD Retreats From Multi-Year Highs Below Key 0.80 Level, Downside Risk Increases

AUDUSD declined after testing a fresh multi-year high of 0.8065 on July 27. The pair struggled to sustain gains above the key 0.8000 psychological level. The market was overextended on the daily chart as indicated by the RSI which rose above 70 into overbought territory.

Momentum signals have shifted to the downside – RSI and MACD are sloping down, suggesting that AUDUSD will most likely have trouble progressing significantly higher at this point. Major resistance is now at 0.8000. Clearing the 0.8065 peak would see a resumption of the recent uptrend.

The level at 0.7888 held as support for the past three weeks and is currently being tested. It is the 23.6% Fibonacci retracement level of the rise from 0.7328 to 0.8065. A daily close below it would likely mean further slippage towards 0.7781 – the 38.2% Fibonacci and July 18 low. From here, the 50% Fibonacci at 0.7695 is expected to provide support. Reaching this level would bring the longer-term market structure to neutral from the current bullish picture.

The overall technical landscape remains bullish. The crossover of the 50-day with the 200-day moving average on July 14 gave a bullish signal. RSI and MACD are in bullish territory. Meanwhile, the short-term bias is neutral to bearish. While downward momentum is increasing (as the RSI and MACD indicators decline), clearer signals are needed to determine the outlook for AUDUSD.

Safe-Haven Assets Gain On Escalating US-North Korea Geopolitical Turmoil

Geopolitical woes between the US and North Korea escalated overnight following announcements by the presidents of both countries. In response, safe-haven assets such as the yen, Swiss franc and gold strengthened overnight. The dollar index was moderately down ahead of European trading. The escalating situation commanded the news flow during the Asian session, overshadowing other economic developments of significance for forex markets.

North Korea announced that its leader Kim Jong Un was weighing a possibility to strike the US Pacific territory of Guam as a response to Donald Trump’s earlier comments that any threats made by North Korea will be met 'with fire and fury like the world has never seen'. Trump’s remarks were provoked by Pyongyang’s threats of 'physical' retaliation for new sanctions imposed by the United Nations and vocally supported by the US and South Korea. In the wake of new developments, the dollar index weakened, giving up on some of the strong gains following an upbeat JOLTS report yesterday. US job vacancies increased by 6.163 million in June instead of 5.775 million expected, exceeding the previous mark of 5.702 million and recording a multi-year high. The dollar index soared to 93.88 in yesterday’s late session but retreated to 93.62 this morning.

During the Asian session, the yen, considered a safe-haven, strengthened against the greenback, with the dollar/yen pair last trading at 110.03. The Swiss franc, another currency that has the same safe-haven appeal as the yen in times of geopolitical anxiety, strengthened with the dollar falling to 0.9688 francs. For the same reason, gold rose to $1,265.55 an ounce during late Asian session trading.

The Australian dollar weakened against its US counterpart. Aussie/dollar was last trading at 0.7891. The kiwi weakened as well under additional pressure ahead of the Reserve Bank of New Zealand meeting tomorrow. The bank is expected to be dovish about its monetary policy outlook. Kiwi/dollar was last trading at 0.7315.

The euro was slightly up against the US dollar to last trade at 1.1754, though the single currency has plunged from the highs of 1.1909 achieved last week following reports showing a strong labor market in the US.

Sterling recovered from yesterday’s low of $1.2952 to trade at $1.3018 ahead of the European session. The pound has been negatively impacted by tepid consumer spending. UK retail sales rose 0.9% annually in July, down from 1.2% the prior month. While the figure came in above expectations of 0.6% gain, it still got investors worried as UK consumers cut back on discretionary spending and budgeted for a more pricey food basket.

Weakness in oil prices continued for the third day as concerns persist over OPEC cuts. The Energy Information Administration (EIA) is due to report its crude oil inventories later in the session. WTI was last trading at $49.10 a barrel while Brent was at $52.00.

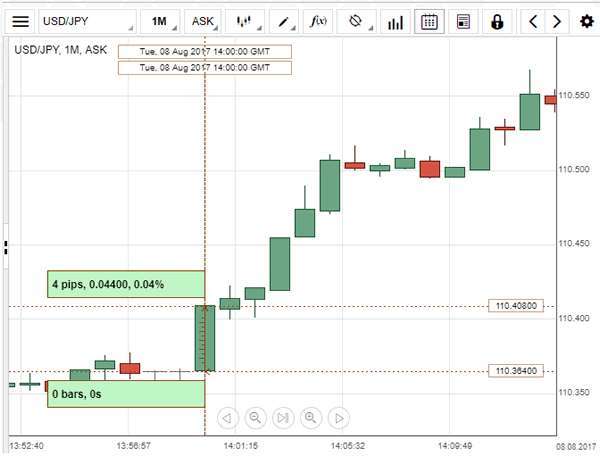

USD/JPY: JOLTS Job Openings

The US job openings report showed a record-high figure, which resulted in the instant advance of the USD/JPY currency pair. Strong figures supported the appreciation of the Greenback against the Yen, which marked a 0.04% increase to be seen trading above the 110.40 level. The Labour Department released its Job Openings and Labour Turnover Survey, or JOLTS, which revealed that the number of job openings jumped 461K to a seasonally adjusted 6.16M, following the preceding month's upwardly revised figure of 5.70M. The better-than-expected data bolstered optimism over the future of the labour market, as the gap between hiring and job openings indicated qualified workers' shortages, which would sustain upward pressure on pay growth.

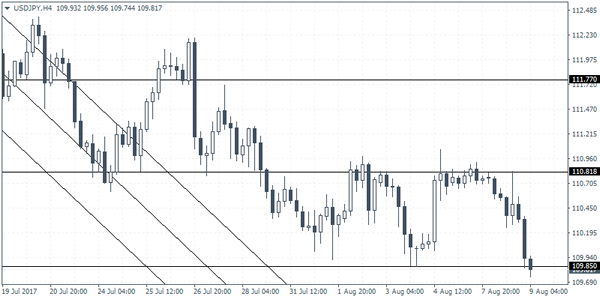

USDJPY Intraday Analysis

USDJPY (109.81): The USDJPY failed to breakout past the 110.80 resistance level. This resulted in some downside in prices. Currently, USDJPY is seen retesting the previous lows formed near 109.85 levels. This is a support level that was previously tested. We could, therefore, expect to see some reversal at this support level followed by an upside move in prices. However, in the near term, USDJPY could remain range bound within 110.81 and 109.85 levels of resistance and support.

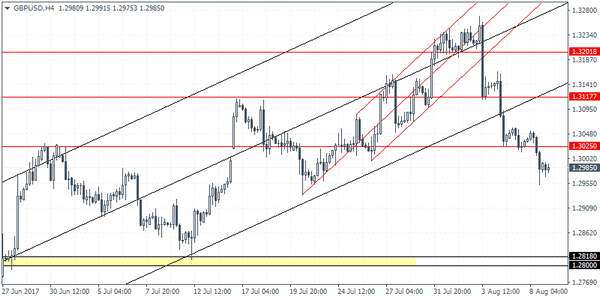

GBPUSD Intraday Analysis

GBPUSD (1.2985): The British pound closed on a bearish note below 1.3025 level of support yesterday. This would suggest further downside in the cable. In the near term, we can expect to see price action consolidate near the resistance level at 1.3025 which could be tested. The next main support for GBPUSD comes in at 1.2818 - 1.2800. This would mark a strong decline in the currency pair. So far, price action in GBPUSD has been falling in a step fashion. Resistance levels are seen at 1.3025 and 1.3177.