Sample Category Title

Trade Idea : USD/JPY – Stand aside

USD/JPY - 110.01

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 110.03

Kijun-Sen level : 110.29

Ichimoku cloud top : 110.70

Ichimoku cloud bottom : 110.53

Original strategy :

Bought at 110.30, stopped at 110.25

Position : - Long at 110.30

Target : -

Stop : - 110.25

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s brief bounce to 110.83, the subsequent selloff dampened our near term bullishness and the breach of previous support at 109.85 signals recent decline has resumed, hence downside risk remains for weakness to 109.70, then 109.50, however, loss of near term downward momentum should prevent sharp fall below 109.20-25 and price should stay above 109.00.

In view of this, would not chase this fall here and would be prudent to stand aside for now. Above the Kijun-Sen (now at 110.29) would suggest an intra-day low is possibly formed, bring rebound to 110.55-60 but break there is needed to add credence to this view, then test of 110.83 and later 111.05 would follow.

USD Bulls Retreat With Trumps ‘Fire & Fury’ Threat

The latest Chinese economic data points to steady global demand. The world’s second-largest economy trade surplus grew for a 5th consecutive month in July, as demand for Chinese goods held up in the face of growing tensions with the US.

Another set of unexpectedly positive data out of the US saw USD gain against many of its peers on Tuesday. The US Bureau of Labor Statistics JOLTS Job Openings (Jun) release of 6.163 million was 388K better than the expected release of 5.775 million, resulting in a record number of job openings in the US.

Further USD buying resulted from the IBD/TIPP Economic Optimism (MoM) (Aug) that was released with a 52.2 reading besting the consensus of 50.6, indicating US consumer’s improved optimism towards current economic conditions. Typically, these US indicators are not 'market impactful' however, with somewhat lackluster markets of late, any news, whether positive or negative, is having an exaggerated effect on the markets.

The latest tensions between the US and North Korea caused President Trump to react with the comment that further threats from North Korea would be met with 'Fire & Fury'. The markets reacted with a slight risk off sentiment with typical safe havens, such as JPY and Gold, in demand.

EURUSD gave up 0.5% on Tuesday, hitting a low of 1.17147 on the back of positive US data. Currently, EURUSD is trading around 1.1740.

USDJPY was subdued on Tuesday, trading in a sub 60 pip range. Currently, USDJPY is trading around 110.00 after reaching a 2-month low in early trading of 109.738, following Trumps reaction to North Korea.

GBPUSD, after holding above 1.30, broke lower to 1.29521 on Tuesday due to overall USD bullishness. GBPUSD is currently trading around 1.2990.

Gold dropped 0.4% on Tuesday to trade as low as $1,251.41, before rebounding higher overnight as markets bought 'safe havens'. Gold is currently trading around $1,265.

WTI edged 0.35% lower on Tuesday, as Saudi Arabia said it would pressure other OPEC members to improve their compliance rate, but there is still the question of Libya and Nigeria, both exempt from the cuts, which are ramping up their oil output at a respectable rate. WTI is currently trading around $49.18pb.

At 11:00 BST the UK Treasury Committee will hold its Inflation Report Hearings.

At 13:30, the US Bureau of Labor Statistics will release Unit Labor Costs and Nonfarm Productivity (Q2). A mixed result is expected with Unit Labor Costs expected to be 1.2% (prev. 2.2%) and Nonfarm Productivity expected at 0.7% (prev. 0.0%).

At 15:30 BST, EIA Crude Oil Stocks change (Aug 4) will be released, with a consensus drawdown of -2.800 Million. With successive recent drawdowns, the market will be evaluating the release in respect to overall US supply/demand.

At 22:00 BST, The Reserve Bank of New Zealand will publish its Interest Rate decision and its Monetary Policy statement. Consensus is for the RBNZ to hold interest rates at 1.75%, but markets will be wary for any change in the 'tone' of monetary policy.

Australia’s Westpac Consumer Confidence Declined In August

For the 24 hours to 23:00 GMT, the AUD rose 0.06% against the USD and closed at 0.7915.

LME Copper prices rose 0.5% or $31.0/MT to $6364.0/MT. Aluminium prices rose 3.2% or $61.0/MT to $1981.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7873, with the AUD trading 0.53% lower against the USD from yesterday's close.

Early morning data showed that Australia's Westpac consumer confidence index fell to a level of 95.5 in August. The index had recorded a reading of 96.6 in the prior month. Also, the nation's seasonally adjusted home loan approvals increased less-than-anticipated by 0.5% in June, compared to a revised rise of 1.1% in the previous month.

Elsewhere in China, Australia's largest trading partner, the consumer price index (CPI) registered a rise of 1.4% on an annual basis in July, underscoring market expectations for a rise of 1.5%. The CPI had climbed 1.5% in the prior month. Moreover, the nation's producer price index (PPI) advanced less-than-expected by 5.5% in July, compared to market expectations for a rise of 5.6%. In the previous month, the PPI had registered a similar rise.

The pair is expected to find support at 0.7838, and a fall through could take it to the next support level of 0.7802. The pair is expected to find its first resistance at 0.7926, and a rise through could take it to the next resistance level of 0.7978.

Moving ahead, investors will focus on Australia's consumer inflation expectation for August, slated to release in the early hours of tomorrow.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

German Trade Surplus At A 10-Month High In June

For the 24 hours to 23:00 GMT, the EUR declined 0.26% against the USD and closed at 1.1763.

On the macro front, Germany’s seasonally adjusted trade surplus widened to a ten-month high level of €21.2 billion in June, as a fall in imports outstripped that of exports. The nation registered a trade surplus of €20.3 billion in the prior month, while investors had anticipated it to widen to €21.0 billion.

On the other hand, the nation’s seasonally adjusted exports recorded an unexpected drop of 2.8% MoM in June, rising at its weakest pace in nearly two years. Market participants had expected exports to rise 0.2%, after recording a revised advance of 1.5% in the prior month. Also, the nation’s seasonally adjusted imports surprisingly dropped 4.5% on a monthly basis in June, posting its sharpest decline since January 2009. In the prior month, imports had recorded a revised rise of 1.3%, while markets were anticipating for a gain of 0.2%.

The greenback lost ground against most of its key peers, after the US President, Donald Trump warned North Korea that any threats to the US will be “met with fire and fury.”

Earlier in the session, the US Dollar strengthened, following robust US labour market report.

Data showed that JOLTs job openings in US surged to a record high level of 6163.0K in June, topping market consensus for a rise to a level of 5750.0K. In the prior month, JOLTs job openings had recorded a revised reading of 5702.0K. Moreover, the nation’s NFIB small business optimism index unexpectedly climbed to a level of 105.2 in July, notching a five-month high, thus indicating that small business firms are feeling optimistic about the economy’s growth prospects. The index had registered a reading of 103.6 in the previous month, while markets anticipated it to ease to a level of 103.5.

In the Asian session, at GMT0300, the pair is trading at 1.1734, with the EUR trading 0.25% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.1693, and a fall through could take it to the next support level of 1.1653. The pair is expected to find its first resistance at 1.1796, and a rise through could take it to the next resistance level of 1.1859.

With no major macroeconomic releases in the Euro-zone today, investors will look forward to the US MBA mortgage applications data, slated to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Pound Trading Marginally Lower In The Asian Session

For the 24 hours to 23:00 GMT, the GBP declined 0.31% against the USD and closed at 1.2994.

In the Asian session, at GMT0300, the pair is trading at 1.2987, with the GBP trading a tad lower against the USD from yesterday’s close.

The pair is expected to find support at 1.2943, and a fall through could take it to the next support level of 1.2898. The pair is expected to find its first resistance at 1.3042, and a rise through could take it to the next resistance level of 1.3096.

Moving ahead, traders will keep a close watch on UK’s inflation report hearings, due to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Japanese Yen Trading On A Stronger Footing In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.57% against the JPY and closed at 110.12.

The Japanese Yen gained ground, amid increased risk aversion among investors after the US President, Donald Trump promised a reprisal of fire and fury if North Korea threatens to attack the US.

On the data front, Japan's Eco-Watchers Survey for the current situation unexpectedly dropped to a level of 49.7 in July, defying market expectations for a rise to a level of 50.2. In the previous month, the index had recorded a reading of 50.0. Further, the nation's Eco-Watchers Survey for the future outlook surprisingly eased to a level of 50.3 in July, compared to a reading of 50.5 in the previous month, while market participants expected the index to rise to a level of 51.0.

In the Asian session, at GMT0300, the pair is trading at 109.90, with the USD trading 0.2% lower against the JPY from yesterday's close.

The pair is expected to find support at 109.48, and a fall through could take it to the next support level of 109.07. The pair is expected to find its first resistance at 110.57, and a rise through could take it to the next resistance level of 111.25.

Ahead in the day, traders will closely monitor Japan's flash machine tool orders for July.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Switzerland’s Unemployment Rate Remained Steady In July

For the 24 hours to 23:00 GMT, the USD declined 0.07% against the CHF and closed at 0.9727.

Macroeconomic data revealed that Switzerland's seasonally adjusted unemployment rate remained steady at 3.2% in July, at par with market expectations.

In the Asian session, at GMT0300, the pair is trading at 0.97, with the USD trading 0.28% lower against the CHF from yesterday's close.

The pair is expected to find support at 0.9676, and a fall through could take it to the next support level of 0.9651. The pair is expected to find its first resistance at 0.9749, and a rise through could take it to the next resistance level of 0.9797.

With no macroeconomic releases in Switzerland today, investor sentiment will be governed by global macroeconomic events.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Reverses Its Gains In The Asian Session, Ahead Of Canada’s Housing Starts And Building Permits Data

For the 24 hours to 23:00 GMT, the USD declined 0.1% against the CAD and closed at 1.2667.

In the Asian session, at GMT0300, the pair is trading at 1.2689, with the USD trading 0.17% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2658, and a fall through could take it to the next support level of 1.2628. The pair is expected to find its first resistance at 1.2712, and a rise through could take it to the next resistance level of 1.2736.

Looking ahead, Canada's housing starts for July and building permits for June, set to release later in the day, will garner a lot of market attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

EURUSD Saw A Notable Drop Below The 1.18 Level

Market movers today

Today is set to be another quiet day in terms of data releases.

The Reserve Bank of New Zealand (RBNZ) will announce its Official Cash Rate (OCR) decision today. We expect the rate to remain at 1.75%, in accordance with consensus.

In the US, preliminary unit labour cost figures and crude Oil inventories data are released.

Danish foreign trade data is out today. Imports and exports rose strongly in May and there was some reversal in June but the underlying out look is good, as growth continues to be strong in Europe and it is hoped that business investments are rising in Denmark.

Selected market news

The Washington-Pyongyang confrontation continued yesterday with US president Trump threating the North Korean regime with ‘fire and fury' amid reports the latter is continuing its missile programme unabatedly amid the recently agreed UN sanctions with North Korea's Kim Jung Unasking his military to examine how to do a strike on the US Guam base. The continued rise in tensions drove gains in safe haven assets with USD/JPY breaking below 110 and EUR/CHF below 1.1350. As a result of souring risk sentiment and yenstrength , equities were generally lower in the Asian session with the Nikkei down more than 1.5%. Slightly weaker than- expected Chinese price indices showing growth in producer prices at 5.5% y/y in July (vs 5.6 expected) and consumer prices at 1.4% y/y (vs 1.5% expected) were less of a driver amid growing geopolitical concerns.

Yesterday afternoon EUR/USD saw a notable drop below the 1.18 level following the strong JOLTS job figures out of the US which added another second-tier data contribution to reversing the US economic surprise index. The US CPI data out on Friday will be instrumental for whether there is a repricing of the Fed in a more hawkish direction ahead of the September meeting: we look for core CPI to be unchanged at 1.7% which should keep the Fed on a 'cautious path'.

In South Africa, president Zuma survived the no-confidence vote which was cast in the national assembly last night. The rand fell by about 1.6% against the USD in the immediate aftermath of the results, but has since regained some ground. In our view, ZAR may stay under a bit of pressure in the coming months, but the currency has shown itself to be relatively resilient to adverse political developments before as investors eye possible leadership change at the ANC conference in December, a modest economic recovery and the sharp improvement in the external balance over the past year.

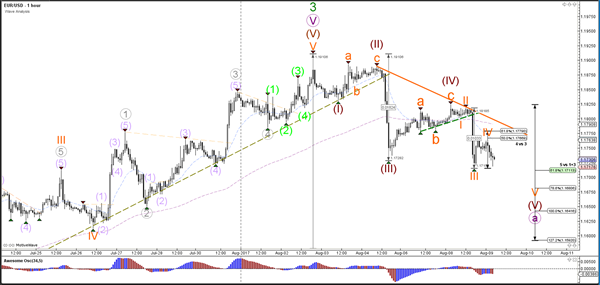

Daily Technical Analysis: EUR/USD Bearish Break Below 1.18 Within Wave 5

.

Currency pair EUR/USD

The EUR/USD bearish retracement is indeed continuing lower, as expected in the wave analysis earlier this week. Price is now approaching two strong support trend lines, which could act as a bounce or break zone. A bullish bounce indicates the completion of wave A (purple) whereas a bearish breakout could see price fall towards the 23.6% Fibonacci level of wave 4 (green).

The EUR/USD broke below the support trend line (dotted green) and could be extending the 5th wave (brown) with 5 waves (orange) if price stays below the Fibonacci levels of wave 4 vs 3.

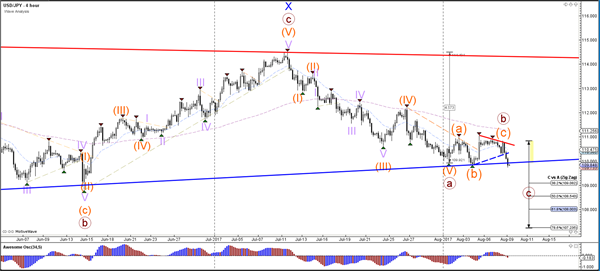

Currency pair USD/JPY

The USD/JPY completed an ABC (orange) zigzag within a larger ABC correction (brown) and seems to be starting a wave C correction now.

The USD/JPY seems to have completed a potential wave 4 and truncated wave 5 (purple) which does not break the top of wave 3.

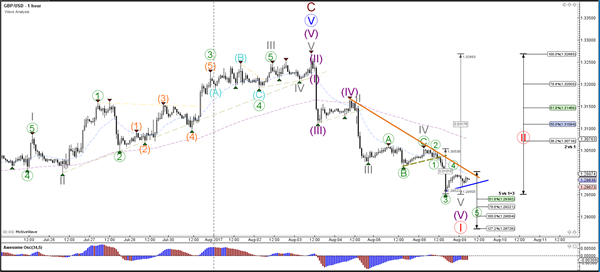

Currency pair GBP/USD

The GBP/USD continued with its downtrend and is building 5 waves (grey) within wave 1 (red).

The GBP/USD could be extending the 5th waves with 5 more waves (green), which could see a bearish breakout below the support trend line (blue). The other scenario is that price will bounce and complete wave 1 and start wave 2 (red). In this case price will probably break above the resistance trend line (orange).