Sample Category Title

Trade Idea : USD/JPY – Buy at 110.30

USD/JPY - 110.59

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 110.68

Kijun-Sen level : 110.73

Ichimoku cloud top : 110.64

Ichimoku cloud bottom : 110.45

Original strategy :

Buy at 110.45, Target: 111.45, Stop: 110.10

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.30, Target: 111.30, Stop: 109.95

Position : -

Target : -

Stop : -

As the greenback has retreated again today, suggesting near term downside risk remains for marginal weakness to 110.30-40, however, if our view that a temporary low formed at 109.85 last week is correct, downside should be limited and 110.00 should hold, bring another rebound later, above 110.90-95 would extend the rebound from 109.85 for retracement of recent decline towards 111.29-30 (previous resistance and 61.8% Fibonacci retracement of 112.20-109.85), having said that, break there is needed to add credence to this view, bring a stronger rebound to 111.50 but price should falter below another previous resistance at 111.71.

In view of this, we are looking to buy dollar on dips as 110.30-40 should limit downside and bring another rise later. Below 110.000 would signal the rebound from 109.85 has ended, bring retest of this level, below there would extend recent decline to 109.70 and later towards 109.50.

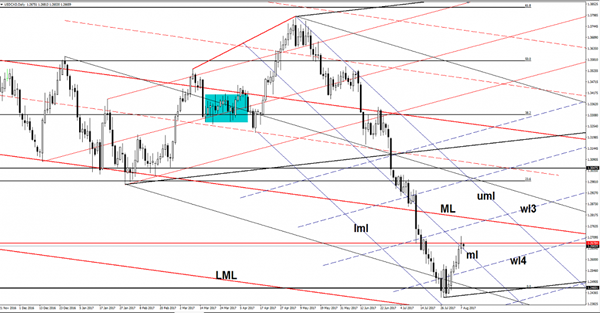

USD/CAD False Breakout?

Price failed to close above the 1.2678 static resistance and now is retesting the broken median line (ml) of the minor descending pitchfork. Will slip lower if the mentioned upside obstacle will hold, could come down to retest the fourth warning line (wl4) before will climb higher again.

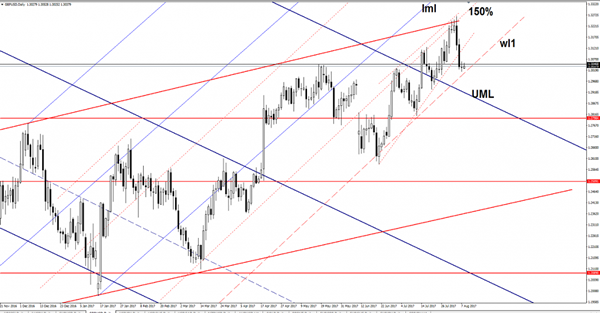

GBP/USD Downside Paused

The GBP/USD posted humble gains today, is fighting hard to stay in the green zone, but remains to see if the buyers will be strong enough to keep the price higher. Is trading within an ascending channel, between the warning line (wl1) and the 150% Fibonacci line (ascending dotted line).

Is expected to retest the warning line (wl1), we'll see how will react because a rejection will bring us a great buying opportunity, but I want to remind that a breakdown will open the door for more declines.

AUD/USD Accumulation Or Distribution?

Price moves sideways on the short term, is consolidating the latest gains and should climb much higher because the uptrend line remains intact. USD could slip lower again as the USDX could decrease a little as well in the upcoming days.

Right now is trying to recover after the last day's drop, the Aussie received a helping hand from the Chinese economic data, which have come in better than expected. The Trade Balance climbed from 294B to 321B in July, beating the 294B estimate, while the USD-Denominated Trade Balance increased from 42.8B to 46.7B, exceeding the 45.4B estimate. Moreover, the Australian NAB Business Confidence increased from 8 to 12 points.

The US is to release economic numbers as well today, but I don't believe that will have any impact on the AUD/USD price action.

Price increased after the failure to reach the 0.7874 static support and now could pressure the median line (ml) of the minor descending pitchfork. A valid breakout above the median line (ml) will confirm an increase towards the upper median line (UML) of the ascending pitchfork and towards the upper median line (uml).

Continues to move between the 0.8065 and the 0.7874 levels, a breakout from this range will bring us a great trading opportunity. It could drop again, only if the US dollar index will have enough energy to climb much higher in the upcoming period.

USDX decreased a little after the Friday's impressive rally, could move sideways till will recapture enough directional energy to really start another leg higher.

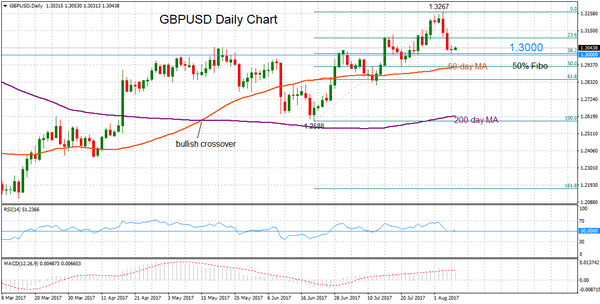

GBPUSD Retreats From 11-Month High, Recent Uptrend Intact Above 1.30

GBPUSD hit an 11-month high of 1.3267 last week before losing upside momentum and reversing back towards the key psychological level of 1.3000. The overall market structure on the daily chart remains bullish and the current move lower is viewed as a corrective phase as long as the price remains above 1.3000.

Support at 1.3000 is considered strong as it also happens to be close to the 38.2% Fibonacci retracement of the recent rally from 1.2588 to 1.3267. This level appears to be holding so far and if it continues to be respected then a bounce higher would open the way towards 1.3100 with scope to re-test the 1.3267 high. Clearing this peak would strengthen the uptrend from June for a continuation of higher highs and higher lows. The next major high is at 1.3480.

Should support at 1.3000 fail to hold, then this would turn the bias back to the downside. The next target would be at 1.2926. This is the 50% Fibonacci retracement level and also where the 50-day moving average (MA) is converging. This level is also close to the July 20 low. A breakdown below would start to change the trend and increase bearish momentum towards the 1.2800 area before reaching the June 21 low at 1.2588.

In the near-term a consolidation phase is expected just above the 1.3000 level. RSI is holding above but close to the 50 line which separates bullish from bearish territory. There are no clear signs of a reversal from the recent uptrend – the bullish crossover on May15 when the 50-day MA moved above the 200-day one is supporting a bullish market structure. The MACD though is not clearly giving a bullish picture – the indicator is hand positive but below the red signal line.

USDJPY Intraday Analysis

USDJPY (110.65): The US dollar continues to struggle to break out above 110.80 resistance level. Price action has once again failed to make any inroads above this resistance level. In the near term, any reversals could be limited within the inside bar range that was formed on Friday. The breakout from Friday's high or low of 111.05 an 110.67 will signal further direction in the near term. To the upside, 111.77 will be the next target where resistance sits, while to the downside, below 110.67 low, the support at 109.58 will be tested for support.

GBPUSD Intraday Analysis

GBPUSD (1.3044): The British pound was seen trading rather subdued yesterday about price action was seen hitting the support at 1.3025. A confirmed break down below this level could suggest further downside in prices. The next main technical support in GBPUSD is at 1.2818 - 1.2800. However, watch for any potential reversal above this support. Unless resistance is clearly formed at 1.3025, further gains cannot be ruled out in GBPUSD.

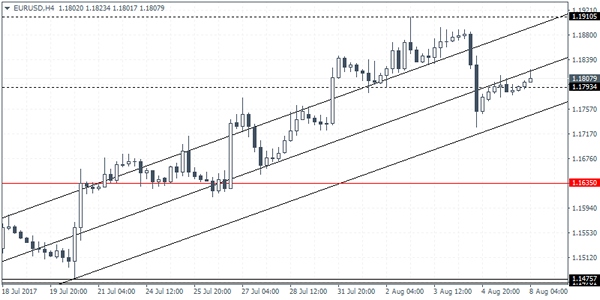

EURUSD Intraday Analysis

EURUSD (1.1807): Following the brief retracement to 1.7934 resistance level, EURUSD has turned lower. This could potentially suggest a near-term decline in prices in the short term. There is also scope for a bearish flag pattern that could be forming as a result of this reversal. If EURUSD manages to break down below the previous low on Friday at 1.1728, then expect to see further declines. A measured move of this potential bearish flag pattern will see EURUSD targeting 1.1635. This also coincides with the support level that is formed here.

US Dollar Holds Gains But Broadly Subdued

The greenback managed to hold on to the gains made from Friday on Monday's session. Price action was however rather subdued with thelack of any clear economic data on Monday.

Fed speeches included that from Neel Kashkari and Bullard. Bullard said that the Fed does not need to raise interest rates in the near term amid a surprisingly stubborn low inflation. The US consumer prices data will be released this Friday. Expectations are high that inflation has managed to increase in July.

Looking ahead, the economic data today will include the German trade balance followed by the NFIB small business index in the US Later in the evening, RBA assistant governor Kent will be speaking.

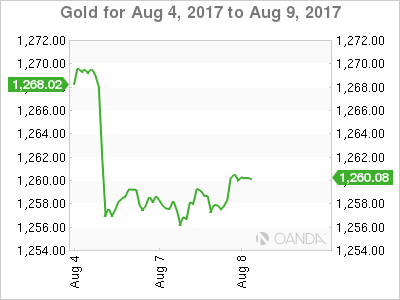

Oil And Gold Take A Chill Pill And Becalm Down

Oil and gold remain becalmed ahead of various data points with only some Fed speeches and Noth Korea rhetoric stirring the otherwise placid waters.

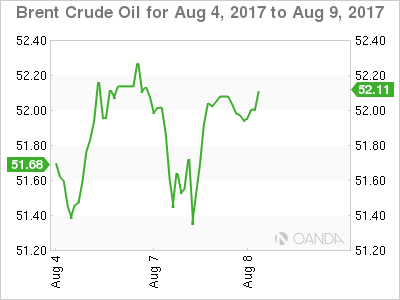

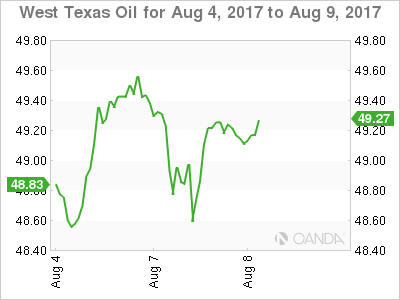

Oil remained locked into choppy range trading overnight as the market awaits the first of the crude inventory numbers of the week from the American Petroleum Institute. Both Brent and WTI spot fell some two percent as Libya announced its biggest oil field was resuming full production. Both contracts however shrugged of this new to make back almost all their losses and close virtually unchanged at 52.05 and 49.25 respectively.

Bulls can take heart from the comeback, but both Brent and WTI's ranges continue to contract in a quiet news environment, suggesting a breakout is imminent. Assuming that nothing comes from OPEC/Non-OPEC's technical meeting in Abu Dhabi today, oils near term fate will most likely be determined by the official U.S. Department of Energy inventory data tomorrow evening Asia time.

OIL

Brent spot is trading at 52.075 with its triple top resistance at 52.70 still untested. Some congestion below appears at 51.20 ahead of key support at 50.50, the 1st August low and the 100-day moving average.

WTI spot trades at 49.20, well below its double top at 50.30. Interestingly a triple bottom has formed over the last four sessions around 48.40 providing initial support ahead of 48.00 and then the key 47.70 level, the 100-day moving average.

GOLD

Gold consolidated near the bottom of its recent trading range overnight with a lack of new to provide any new price direction. Like many other markets this week, gold appears to be in a holding pattern with the increasing risk that stale long positioning may see traders head for the door until some directional clarity is restored.

Gold traded in a 1255/1260 range overnight and opened at a sleepy 1258.50 level this morning in Asia. Some dovish comments from Fed Governors Kashkari and Bullard along with the day's daily dose of sabre rattling from North Korea has seen gold drift higher to 1260.00. However, initial daily resistance still lies distantly at 1274.20 with the near term support much closer and likely to be of more concern to traders.

The Friday low and also the 100-day moving average is just below current levels at the 1253.00 regions, followed by the 50% Fibonacci retracement at 1249.20. A daily close below these levels would be a concerning development for gold bulls, suggesting a further test to the 1243 regions and possibly a deeper retracement to the 200-day moving average at 1230.00.