Sample Category Title

GBP/USD Bearish Breakout

GBP/USD has broken bullish trend . Hourly resistance is given at 1.3267 (03/08/2017 high). Hourly support is given at 1.2933 (20/07/2017 low) while support can be found at 1.2933 (20/07/2017 low). Expected to show growing bearish pressures.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Bullish Momentum Is Going To Continue

EUR/USD bullish pressures are still on despite ongoing consolidation. Hourly resistance is given at 1.1910 (02/08/2017 high). Hourly support can be found at 1.1728 (04/08/2017 high). Stronger support lies at 1.1613 (26/07/2017 low). Expected to show continued bullish pressures.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance holding at 1.1871 (24/08/2015 high) has been broken while strong support lies at 1.0341 (03/01/2017 low).

USD Reverses Gains, CNY Loses Ground

FX market is treading water as Fed members talk the US dollar down

It has been a slow start into the week so far with most currency pairs trading sideways. With the exception of the New Zealand dollar, which experienced a sell-off on Monday amid a drop in inflation expectations, most G10 currencies reversed Friday’s losses. The single currency bounced back to 1.1824 on Tuesday after dipping as low as 1.1728 last Friday. USD/JPY trimmed gains and stabilised at around 110.50, unable to gain upside momentum.

The dovish comments from two Fed members prevented the dollar to initiate a recovery. Both Bullard and Kashkari emphasized that the weak inflationary pressures were still a problem that cannot be solved by an improving job market. St. Louis Fed President Bullard declared that “the current level of the policy rate is likely to remain appropriate over the near term," and added that the weak inflation reading were concerning because it suggests this setback is not due to temporary factors.

The July inflation report is due for release on Friday. After the publication of a rather mixed personal expenditure indicator for June on August 1st, investors are impatiently awaiting for the July’s CPI figures. Economists have turned slightly more optimist with the headline gauge expected to come in at 1.8%y/y from 1.6% in June, while the core gauge should have remained flat at 1.7%.

Beside the July’s inflation report, it is going to be a slow week in term of economic data. It is however important to remember that the RBNZ is holding its August meeting tomorrow. A downside move in NZD/USD can therefore not be ruled out.

China: Exports suffered in July

China continues its transition from an economy driven mostly from manufacturing to an economy based on its domestic market. China’s economy is also a great barometer of the global economy and today’s China’s exports are a good illustration of it. The data have shown a decline in July way below consensus printing at 7.2% y/y versus 11% y/y expected. It is worth noting that there exists a strong seasonality of China’s exports which tend to slow down just after the summer before bouncing back towards the end of the year. This year, it seems that the slow down happens sooner than the years before.

Trade balance has increased in July above markets expectations at $46.7 billion vs $45 expected. This is mostly due to imports that keeps growing at a higher pace than exports. Imports came in at a strong 11% y/y in July, even though below expectations. Imports growth decelerates and we may believe that domestic demand is also cooling – slightly at the moment.

Currency-wise the USDCNH is now trading at its lowest levels since October 2016 at 6.7 Yuan against a single dollar note. China’s falling exports are also the sign that the global outlook does not seem so promising and this validates the China’s transition. USDCNH is set to weaken again.

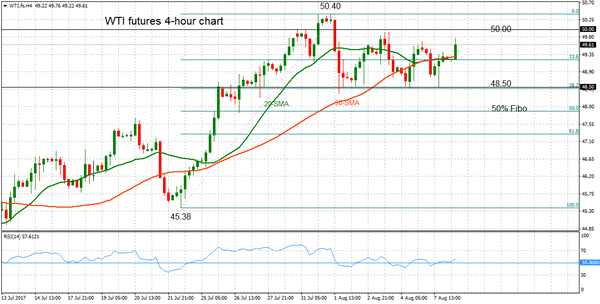

WTI Oil Futures Neutral In Near-Term After Recent Rally, Market Consolidates Below Key 50 Level

WTI oil futures maintain a neutral bias on the 4-hour chart after a strong rally that took place between the July 24 low of 45.38 to the August 1 high of 50.40. Prices have been moving sideways in a range between 48.50 and 50.00 during the past one week as upside momentum faded when the market became overextended. This was indicated by the RSI which rose above 70 into overbought territory.

The RSI has not shown any clear sense of direction lately and has been pivoting around the 50 level, which separates bullish from bearish territory. The 20-period simple moving average (SMA) is converging with the 50-period SMA which is also an indication of a lack of trend.

Immediate resistance is at the key psychological level at 50.00. Breaking it could increase bullish momentum to target the 50.40 high with scope to rise further towards the 60.00 area. The next major peak is the May 25 high of 51.97.

Alternatively, if support at 48.50 fails to hold, an accelerated decline could follow since this is an important level. It is the 38.2% Fibonacci retracement of the most recent rally from 45.38 to 50.40. Below this, the near-term trend would shift out of neutral to a more bearish one. The next support level comes into view at 47.88, at the 50% Fibonacci. A deeper decline would see prices enter the 47.00 area before reaching 45.38.

There are no clear signs of a trend in the near-term and the consolidation phase is expected to hold between 48.50 and 50.00 until there is a shift in momentum and prices break out of either side of the range. In the bigger picture, the uptrend from 45.38 to 50.40 remains intact and the market is now consolidating this move.

Daily Technical Analysis: GBP/CAD Inverted Head And Shoulders Pattern On Intraday Time Frame

In the lack of any major driver today, the GBP/CAD is still bullish ,after the retracement from the weekly H4 camarilla pivot. At this point, we can see a bullish SHS (inverted head and shoulders pattern) that cues for an uptrend continuation. 1.6493-1.6506 (bullish shs, trend line, 2 hammers, historical buyers, 61.8, D3) is the POC zone and the price might reject. Above 1.6520 we might see a continuation towards 1.6540, 1.6565 and 1.6602. D L4 -1.6477 should hold for the bullish SHS pattern to succeed. Below 1.6475 we might see the pattern invalidation, leading to 1.6440.

Fed’s Bullard Supports B/S Normalization In September|

In an otherwise quiet day in terms of market developments yesterday, two of the Fed's most dovish policymakers, St. Louis Fed President James Bullard and Minneapolis Fed President Neel Kashkari stepped up to the rostrum. Both expressed their concerns regarding the recent low inflation readings. Given that Kashkari did not speak about policy much, we will focus on Bullard, who said he is unlikely to support any rate hikes in the near-term, as inflation is unlikely to rise much, even despite the tight US labor market. However, he pointed out that he is still ready “to get going” with a normalization of the Fed's balance sheet (B/S) in September. Bullard is not a voter this year, but considering that he is usually ultra-dovish on policy, his comments suggest that even the most cautious FOMC officials may support a B/S action as early as September.

The dollar did not react much to these comments, possibly due to Bullard's non-voting status. Even though we are not calling for a reversal in USD yet, we should point out that the short-USD trade is looking increasingly crowded to us. Fed rate expectations are already quite pessimistic, with markets pricing less than a 50% probability for another hike this year. Meanwhile, economic data have consistently surprised to the downside recently, while political developments (especially ones surrounding the White House) probably contributed to the USD's underperformance as well. As such, we believe that further negative US news are likely to have a diminishing negative impact on the dollar, while any positive surprises could result in strong upside reactions. Leaving politics aside, a potential pick up in inflation over the coming months could lead to a significant repricing of Fed rate-hike expectations, and may thereby ignite a recovery in the dollar. Thus, we will pay close attention to the nation's CPI data due out on Friday, for any signs as to whether the greenback's fortune is likely to change anytime soon.

EUR/USD continued trading north on Monday and during the Asian morning Tuesday it tested the 1.1830 (R1) line as a resistance. The rate continues to trade above the short-term uptrend line taken from the low of the 22nd of June, which keeps the near-term picture positive, in our view. If the bulls manage to break the 1.1830 (R1) barrier, we expect them to target once again the 1.1900 (R2) hurdle. Nevertheless, a break above that obstacle is needed to confirm a higher high, something that could set the stage for more bullish extensions, perhaps towards our next resistance of 1.1980 (R3).

USD/JPY slid somewhat during the Asian morning Tuesday after it hit once again resistance slightly below the 111.00 (R1) zone on Monday. On the 28th of July, the pair has entered a sideways range between that barrier and the support of 109.90 (S2). As such, given that the latest retreat came after testing the upper bound of the aforementioned range, we would expect the slide to continue, at least within the range. A clear dip below the support of 110.50 (S1) may confirm the case and is possible to pave the way for the lower end of the range, at 109.90 (S2).

The economic calendar is light today as well:

The only indicators worth mentioning are Germany's trade balance for June, and the US JOLTS job openings survey for June.

EUR/USD

Support: 1.1725 (S1), 1.1655 (S2), 1.1615 (S3)

Resistance: 1.1830 (R1), 1.1900 (R2), 1.1980 (R3)

USD/JPY

Support: 110.50 (S1), 109.90 (S2), 109.45 (S3)

Resistance: 111.00 (R1), 111.30 (R2), 111.70 (R3)

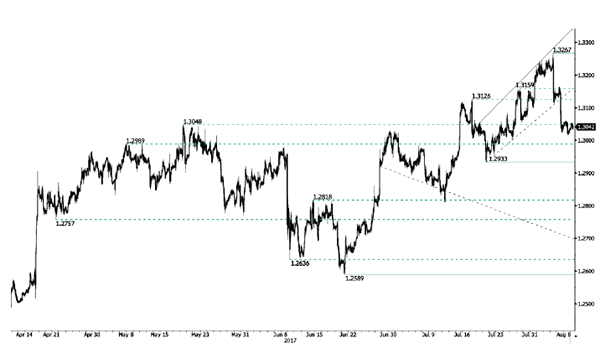

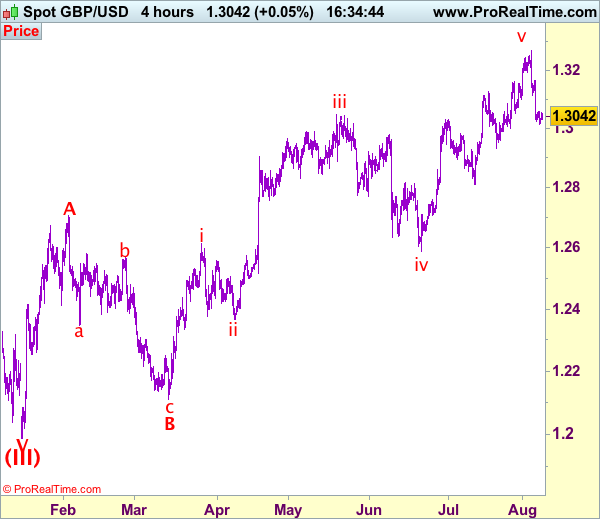

Trade Idea: GBP/USD – Sell at 1.3150

GBP/USD – 1.3040

Recent wave: Wave V of larger degree wave (III) has ended at 1.1986 and major correction has commenced from there for gain to 1.3000 and 1.3140-50

Trend: Near term up

Original strategy :

Sell at 1.3150, Target: 1.2980, Stop: 1.3210

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.3150, Target: 1.2980, Stop: 1.3210

Position: -

Target: -

Stop:-

As cable has remained under pressure after recent selloff from 1.3269 top (last week’s high), adding credence to our view that top has been formed at 1.3269 and downside bias remains for this move to bring retracement of recent upmove, hence further weakness to support at 1.2999 is likely, break there would provide confirmation, bring further fall to 1.2955-60, however, near term oversold condition should limit downside and reckon support at 1.2933 would hold on first testing.

In view of this, would be prudent to sell cable on recovery as said resistance at 1.3165 should cap upside, bring another decline. A firm break above this level would defer and suggest first leg of decline from 1.3269 has ended instead, risk a strong rebound to 1.3200, however, price should falter well below said resistance and bring another decline later.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

Chinese Data Fails Forecast | Dollar And Oil Weakness Continues | Gold Edges Higher

Chinese Trade balance shows global growth improving

Fed will focus on PPI and CPI data for a rate hike

US NFP tail wind for the dollar stops

Oil traders focus on compliance

Gold changes gear

The Chinese trade balance data is weighing on the sentiment over in Europe and this is going to keep investors on the side-lines. Although, the recent data out of China has shown improvement and it confirms that both the internal and external factors are becoming stronger. However, China's export engine went down a gear and this is what investors do not like. The trade surplus also inflated to $46.7 billion.

Over all, you can say that the numbers have painted a dull picture to start the third quarter of this year. It is important that global demand improves because that would imply that the world economy is healthy.

St Louis Fed president James Bullard and Minneapolis Neil Khaskari both think that inflation is the key to increase the interest rate further because the evidence is not supporting for another hike this year. William Dudley, the New York Fed will also share his thought later this week. Dudley is known for his hawkish stance and investors will be looking at that how far he can stretch the support for a rate hike.

The tail wind from the US NFP data which helped the dollar index did not last for long. It is your downward trend which has more strength and we do think that the dollar index could be pushed all the way to the 91 mark. This means that the EURUSD, GBPUSD, AUDUSD and USDJPY pairs will not only recoup their losses from Friday but they will also score more gains. In terms of economic data, it is going to be a very boring day and there isn't anything strong enough which could pause the dollar weakness against these pairs.

A lot of dollar weakness is mainly due to the disappointment around Trump's ability to deliver on his promises. Realistically speaking, we have not seen anything yet on the tax reform or on the fiscal front. That is keeping the pressure on the inflation and the Fed just can't take the chance to make a mistake and therefore they cannot be overly hawkish. Although this week, we will get a more updated picture on the US producer price index and consumer price index. Both are essential to make any conclusion about the overall inflation.

The black gold is struggling to make any major upward move as the chief focus during the OPEC meeting was on the compliance in their meeting yesterday. It appears that the technicals are supporting that we may move lower and retrace more. We need to break above the 50.50 mark and that would involve fresh money joining the rally. If the compliance issue among the cartel improves, speculators would try to push the price higher. However, even then the upside is limited due to the lack of any meaningful demand. Investors would look closely at the export numbers from Saudi Arabia and if the country obeys its own rules and limits the export to 6.6 m barrels a day, we could see the price breaking the current consolidation zone.

The yellow precious metal has seen some life on the back of the dollar weakness. Usually, when the equity market is this strong, investors become a little oblivious and they forget to hedge. Basically, who wants to invest in gold when they see the equity markets making all-time highs? The yellow metal may continue to recoup its losses but the upside is capped by the resistance of 1270. North Korea is the wild card right now after the US along with UN which slammed more sanction. This would prompt for more missile tests and sparks more geopolitical pensions. The support is at 1245 mark and if there is any interest we may see the price taking another steb towards the 1270 mark

Euro Shrugs Off Strong German Trade Surplus

EUR/USD continues to have a quiet week. Currently, the pair is trading at 1.1806, up 0.11% on the day. On the release front, Germany's trade surplus improved to EUR 21.2 billion, above the estimate of EUR 20.8 billion. In the US, today's major event is US JOLTS Jobs Openings, which is expected to improve to 5.74 million. On Wednesday, the US releases two employment indicators – Preliminary Nonfarm Productivity and US Preliminary Unit Labor Costs.

The euro has been on a roll over the past few months, as EUR/USD has soared 10.7% since April 1. Last week, the euro briefly pushed across the 1.19 line, its highest level since January 2015. Although the US economy is in better shape than the eurozone, investors have snapped up the continental currency, as expectations remain high that the ECB is not far away from starting to wind down its ultra-easy monetary policy. The cautious ECB has not provided any dates for a change in policy, but in June, ECB President Mario Draghi spoke about a “strengthening and broadening recovery” in the eurozone, and this sent the euro soaring. Clearly, any hints from the ECB about tightening policy could send the euro higher. In contrast, the dollar has taken a beating, as Donald Trump's antics and inability to pass healthcare legislation has increased political risk in the US. As well, the Federal Reserve's monetary policy remains unclear. Earlier this year the Fed strongly hinted that it planned to raise rates three times in 2017, but has only pressed the rate trigger twice. In June, Fed Chair Janet Yellen shrugged off low inflation, saying that it was due to “transient” factors, leaving the impression that the Fed still planned one final hike. However, inflation has not improved and the Fed has changed its tune. Last week, St. Louis Federal Reserve President James Bullard said he opposed further Fed hikes, warning that another hike would actually delay inflation from hitting the Fed's target of 2%. The markets have become more skeptical about a rate hike in December, as the odds have fallen to 33%, compared to 43% a week ago.

A strong US economy continues to grapple with weak inflation, which is also apparent in the labor market. Although the nonfarm payrolls report in July easily beat expectations and the unemployment rate dropped from 4.4% to 4.3%, wage growth remains a sore point. In July, Average Hourly Earnings remained unchanged at 0.3%, and the indicator has failed to break above 0.3% in 2017. The weakness in earnings growth has puzzled economists, as a red-hot labor market should translate into higher wages. In fact, wage growth has actually slowed in 2107, and this could have significant economic repercussions, as consumers are responding by holding tight on the purse strings and reducing spending.

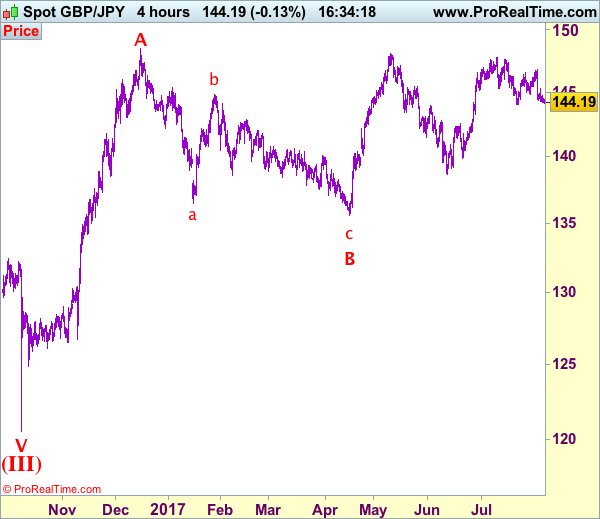

Trade Idea: GBP/JPY – Sell at 145.50

GBP/JPY - 144.20

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term up

Original strategy:

Sell at 145.50, Target: 143.50, Stop: 146.10

Position: -

Target: -

Stop: -

New strategy :

Sell at 145.50, Target: 143.50, Stop: 146.10

Position: -

Target: -

Stop:-

Sterling has remained under pressure after recent selloff from 146.80 (last week’s high), adding credence to our view that the rebound from 144.05 has ended there, hence downside bias remains for another fall to said support, however, break there is needed to retain bearishness and signal another leg of corrective decline from 147.75 top is underway, then further fall to 143.50 and later test of support at 143.30 would follow.

In view of this, would not chase this fall here and would be prudent to sell cable on subsequent recovery as 145.60-70 should limit upside. Above 146.00-10 would dampen this bearish scenario and risk a strong rebound to 146.50 but only break of said resistance at 146.80 would revive bullishness and signal correction from 147.75 has ended instead, bring further gain to 147.30-35 later.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.