Sample Category Title

Trade Idea: GBP/JPY – Sell at 145.50

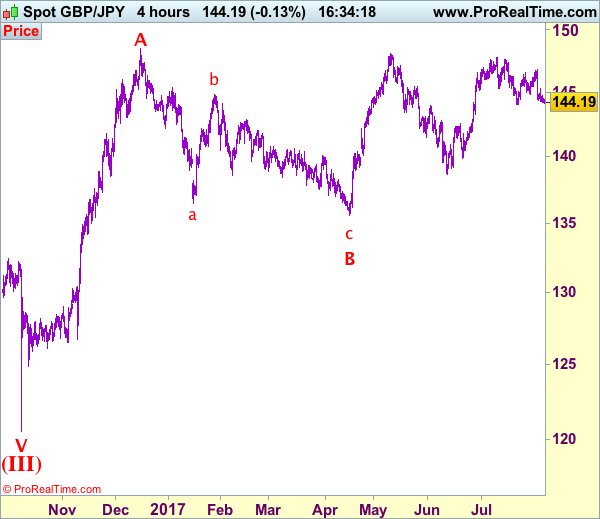

GBP/JPY - 144.20

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term up

Original strategy:

Sell at 145.50, Target: 143.50, Stop: 146.10

Position: -

Target: -

Stop: -

New strategy :

Sell at 145.50, Target: 143.50, Stop: 146.10

Position: -

Target: -

Stop:-

Sterling has remained under pressure after recent selloff from 146.80 (last week’s high), adding credence to our view that the rebound from 144.05 has ended there, hence downside bias remains for another fall to said support, however, break there is needed to retain bearishness and signal another leg of corrective decline from 147.75 top is underway, then further fall to 143.50 and later test of support at 143.30 would follow.

In view of this, would not chase this fall here and would be prudent to sell cable on subsequent recovery as 145.60-70 should limit upside. Above 146.00-10 would dampen this bearish scenario and risk a strong rebound to 146.50 but only break of said resistance at 146.80 would revive bullishness and signal correction from 147.75 has ended instead, bring further gain to 147.30-35 later.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

Market See Light Release Schedule On Tuesday

The financial markets will experience a light release schedule on Tuesday, giving investors time to absorb recent data releases while looking ahead to a more active second half of the week.

The European data wire begins at 05:45 GMT with a report on Swiss unemployment. Switzerland’s jobless rate is expected to hold steady at 3.2% in July.

Just 15 minutes later, Germany’s Federal Statistics Office will report on the June trade balance. Berlin’s trade surplus is forecast to widen to €21 billion in June from €20.3 billion the month before. Exports are projected to drop 0.1% after rising 1.4% the previous month. Imports, meanwhile, are forecast to climb 0.2% after gaining 1.2% in May.

France will also release its latest trade figures on Monday. Paris’ trade deficit is forecast to widen to €5.1 billion in June from €4.9 billion the previous month.

There are no major data releases scheduled in North America. The National Federation of Independent Business (NFIB) will release its monthly business optimism index at 10:00 GMT. The July report is expected to show no change from the previous month.

Oil traders will be keeping a close eye on the weekly US crude inventory report from the American Petroleum Institute (API) at 17:00 GMT. Crude prices declined on Monday, as investors evaluated recent data pointing to a broad pickup in crude output from the Organization of the Petroleum Exporting Countries (OPEC).

Investors will also be evaluating Chinese trade data throughout the day. China’s dollar-denominated trade surplus widened to $46.74 billion in July from $42.77 billion in June, the General Administration of Customs reported Tuesday. Exports rose at an annualized 7.2%, following a gain of 11.3% the month before. Imports spiked 14.7% year-over-year, following a gain of 23.1%.

When measured in Chinese yuan, the trade surplus rose to 321.2 billion yuan from 294.3 billion, official data showed.

EUR/USD

After climbing above 1.1900 on Friday, the EUR/USD has broken to the downside, with traders increasing their short positions on the pair. The EUR/USD is currently holding just above the 1.18 level, with prices vulnerable to a bigger reversal now that the month-long uptrend has been disrupted.

GBP/USD

The British pound stemmed its decline on Monday following heavy losses during the previous two sessions. The GBP/USD exchange rate approached the mid-1.32 region ahead of the Bank of England rate decision last Thursday. Cable declined some 200 pips following the rate announcement on account of only two MPC members voting to raise interest rates.

WTI OIL

Oil prices were down in overnight trade, with US crude futures hovering around $49.24 a barrel. Crude prices remain in a firm uptrend, but have faced significant resistance around the $50 a barrel mark. Fundamentals continue to drive the market, as investors evaluate OPEC’s efforts to rein in supplies.

Trade Idea: EUR/JPY – Stand aside

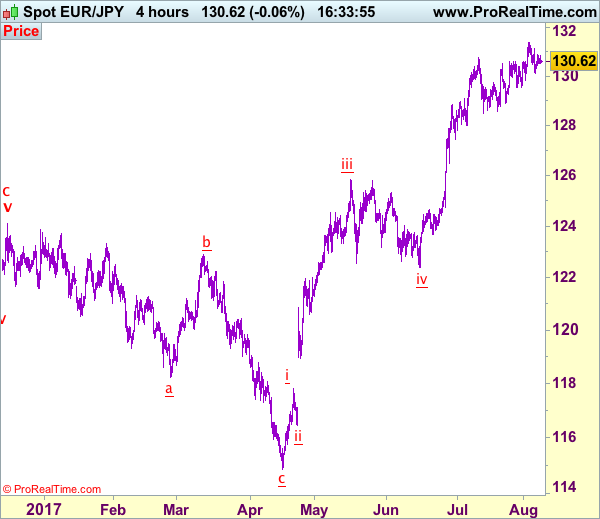

EUR/JPY - 130.56

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term up

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Although euro found support at 130.09 late last week and recovered, reckon resistance at 131.12 would limit upside and bring further consolidation below last week’s high at 131.40, hence downside risk remains for the retreat from there bring weakness to 130.09, then support at 129.84, break there would suggest a temporary top has been formed at 131.12, bring retracement of recent rise to 129.54 and later towards 129.00.

In view of this, would be prudent to stand aside in the meantime. Above said resistance at 131.12 would signal the retreat from 131.40 has ended, bring retest o this level later. Once this resistance is penetrated, this would confirm recent upmove has resumed and extend gain to 131.60, then 132.00-10, however, loss of upward momentum should prevent sharp move beyond 132.50-60 and reckon 132.90-00 would hold from here.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

British Pound Turned Bearish Vs US Dollar

Key Highlights

- The British Pound made a medium-term top at 1.3298 against the US Dollar and moved down.

- There was a break below two important bullish trend lines at 1.3150 on the 4-hours chart of GBP/USD.

- Recently, the UK's BRC Like-For-Like Retail Sales for July 2017 (YoY) was released, which posted an increase of 0.9%.

- Today in the US, the NFIB Business Optimism Index for July 2017 will be released, which is forecasted to remain at 103.6.

GBPUSD Technical Analysis

The British Pound seems like completed an uptrend near 1.3260 against the US Dollar. The GBP/USD pair is now below 1.3100 and trading with a negative bias.

Looking at the 4-hour chart, there was a break below two important bullish trend lines at 1.3150. The pair also moved below the 100 simple moving average to trade as low as 1.3012.

The pair seems to be forming a short-term bottom above 1.3000 and might recover. On the upside, an initial resistance is near the 23.6% Fib retracement level of the last decline from the 1.3268 high to 1.3013 low at 1.3073.

Above 1.3073, the 100 simple moving average (H4) is positioned at 1.3085. So, if the pair continues to move higher, the 1.3080-1.3100 zone is likely to act as a major resistance for buyers.

On the downside, the 1.3000 handle holds a lot of importance and remains a key pivot for GBP/USD.

UK's BRC Like-For-Like Retail Sales

Recently, the UK's BRC Like-For-Like Retail Sales for July 2017 was released by the British Retail Consortium. The market was aligned for an increase of 0.6% compared with the same month a year ago.

However, the actual result was better, as the BRC Like-For-Like Retail Sales grew by 0.9%. However, it was less than the last increase of 1.2%. The increase in sales was mostly driven by food sales. On the other hand, non- food sales moved into negative territory.

Commenting on the same, the Chief Executive at BRC, Helen Dickinson OBE, stated:

Sales growth slowed in July from June. That said, given the strong performance of the same month the previous year, the figures are fairly solid. Closer inspection of the headlines however unveils some familiar challenges. While online sales continue to outpace in-store growth, it is not one at the expense of the other.

Overall, the GBP/USD pair may correct a few pips higher in the near term towards 1.3080-1.3100. However, the pair is most likely to face sellers near 1.3100 and the 100 SMA (H4).

Trade Idea: AUD/USD – Hold short entered at 0.8030

AUD/USD – 0.7928

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term up

Original strategy :

Sold at 0.8030, Target: 0.7880, Stop: 0.7985

Position: - Short at 0.8030

Target: - 0.7880

Stop: - 0.7985

New strategy :

Hold short entered at 0.8030, Target: 0.7880, Stop: 0.7985

Position: - Short at 0.8030

Target: - 0.7880

Stop:- 0.7985

Aussie’s recovery after falling to 0.7891 has retained our view that consolidation above this level would be seen, however, as long as resistance at 0.7980 holds, mild downside bias remains for another retreat, below said support at 0.7891 would add credence to our view that wave iii top is possibly formed at 0.8066, bring correction in wave iv to 0.7875-80 (previous support) but break there is needed to retain bearishness, bring retracement of recent upmove to 0.7839 (previous resistance tuned support), however, downside should be limited to 0.7786 and price should stay well above wave i top at 0.7712.

In view of this, we are holding on to our short position entered at 0.8030. A sustained breach above said resistance at 0.7980 would abort and suggest low is possibly formed, bring a stronger rebound to 0.8000, then towards 0.8043 resistance, break there would signal the pullback from 0.8066 top has ended instead, bring retest of this level first, then 0.8100 and possibly 0.8140-50. We are keeping our latest bullish count that recent impulsive waves is unfolding as (1 2, (i)(ii), i ii) and may extend headway to aforesaid upside targets.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

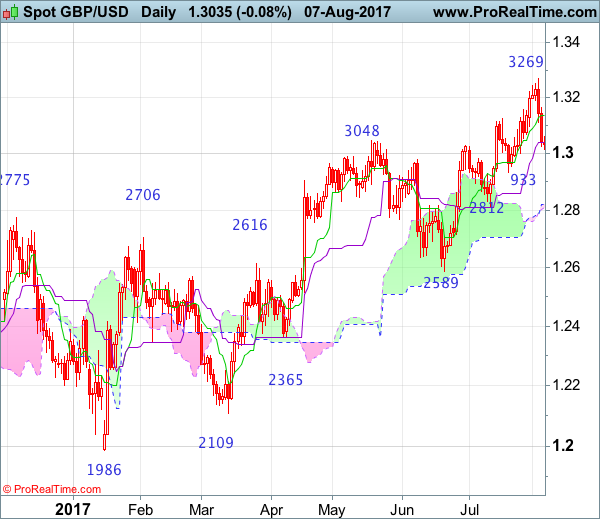

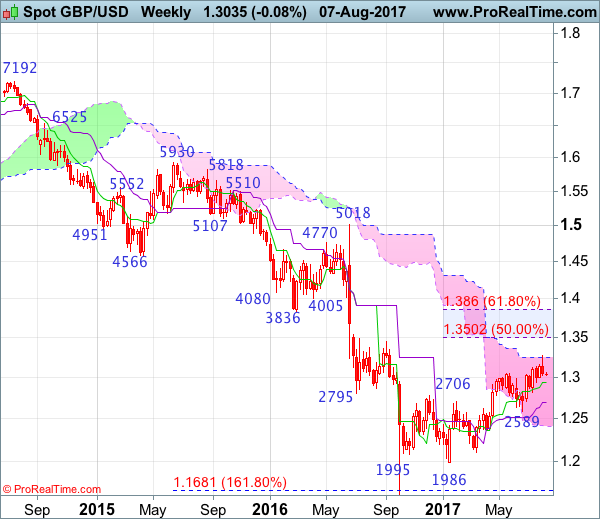

GBP/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 16 Jan 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 18 Apr 2017

• Trend bias: Near term up

GBP/USD – 1.3193

Although cable extended recent upmove to 1.3269 last week, the subsequent sharp retreat suggests a temporary top is possibly formed there and consolidation with mild downside bias is seen for test of support at 1.2999, break there would add credence to this view, bring retracement of recent upmove to another previous support at 1.2933. Once this level is penetrated, this would signal recent upmove is over, bring further fall to 1.2890, then towards previous support at 1.2812 which is expected to contain downside.

On the upside, whilst recovery to 1.3060-70 cannot be ruled out, if our view that a temporary top formed at 1.3269 is correct, upside should be limited to the Tenkan-Sen (now at 1.3134) and bring another retreat later. Above 1.3200 would risk another test of said resistance at 1.3269 but break there is needed to confirm recent upmove has resumed and extend gain to 1.3300-10, however, loss of upward momentum should prevent sharp move beyond resistance at 1.3425 and price should falter well below 1.3500-05 (50% Fibonacci retracement of 1.5018-1.1986), risk from there is seen for a retreat later.

Recommendation: Sell at 1.3100 for 1.2900 with stop above 1.3200.

On the weekly chart, the British pound has retreated after last week’s brief rise to 1.3269, a black candlestick with a long upper shadow (shooting star alike) was formed, suggesting a temporary top is possibly formed there and consolidation with mild downside bias is seen and if this week ends with a black candlestick, this would add credence to this view, bring test of the Tenkan-Sen (now at 1.2929), a weekly close below this level would bring correction of recent rise to 1.2860-65, then test of 1.2812 support, however, downside would be limited to 1.2700-10 and price should stay well above support at 1.2589, bring a rebound later.

On the downside, although initial pullback to 1.3095-00 is likely, reckon downside would be limited to 1.3050-55 and said support at 1.2999 should hold, bring another rise later. A weekly close below 1.2999 would suggest a temporary top is possibly formed, bring test of 1.2933 support, break there would add credence to this view, then retracement of recent rise to the Tenkan-Sen (now at 1.2895) and later 1.2812 support would follow, however, downside would be limited to 1.2700-10 and price should stay well above support at 1.2589, bring a rebound later.

EUR/USD Analysis: Reveals Descending Pattern

On Tuesday morning a classic pattern was spotted on the hourly chart for the EUR/USD currency exchange rate. Namely, a junior descending channel pattern was spotted in the borders of the dominant ascending channel. In accordance with both of the patterns, various scenarios can occur during the next two trading sessions. Moreover, the close proximity of the simple moving averages of the hourly chart makes the situation more complex. However, in general the currency pair is most likely going to surge up to the upper trend line of the junior pattern, and it will be propelled higher by the 200-hour simple moving average. Afterwards the rate should decline down to the support line of the dominant channel.

GBP/USD Analysis: Flat On Tuesday

In line with expectations, GBP/USD was relatively still on Tuesday, as no major fundamental events that could shake the market were scheduled for the given session. As a result, the Pound formed a flat short-term channel down and tested its upper boundary this morning. Meanwhile, the rate remains stranded between the bounds of the 55-hour SMA and the weekly and monthly S1s at 1.3065 and 1.2950, respectively. The Pound may appreciate against the Greenback in this session, testing a resistance set by the aforementioned 55-hour SMA and the monthly PP at 1.3085. Nevertheless, it is likely that yesterday's lack of momentum may likewise repeat today, thus making no significant changes to the overall price level by Wednesday morning.

USD/JPY Analysis: Moves Along Channel Line

On Monday, the US Dollar was driven by neither bears nor bulls, thus resulting in a movement sideways. This stillness was broken this morning when the rate fell down to the 110.60 mark and crossed the 200-hour SMA from above. Thus, it remained stranded in a very narrow range between the 200-, 100– and 55-hour SMAs and the monthly PP in the 110.65/55 area. The previously drawn channel down was shifted to the upside, demonstrating that the Greenback has been quite sticky to the upper channel boundary. This implies that the given currency may eventually breach to the upside. However, it is not yet clear if this move will occur today. For now, the rate is likely to either move sideways near the weekly PP or trade lower along the upper channel line.

XAU/USD Analysis: Reaches Long Term Support

On Tuesday morning the yellow metal's price was trading just above the lower trend line of the long term ascending channel pattern. However, the commodity price was about to face various levels of resistance. First of all the 55, 100 and 200-hour simple moving averages will attempt to keep the bullion lower. The resistance levels are located, respectively, at 1,260.83, 1,263.25 and 1,264.01 levels. Moreover, there is a weekly pivot level located near the 1,260 mark. Due to these reasons market participants should watch, whether the metal's price breaks through the combined strong resistance or not. As the result of the face off will show the future medium term direction of the commodity price.