Sample Category Title

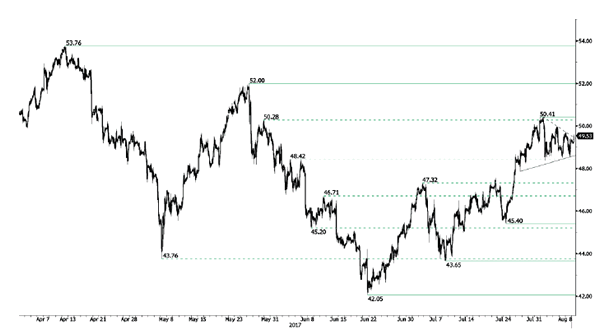

Crude Oil Strengthening

Crude oil is trading higher. Hourly support is given at 47.86 (26/07/2017 low). Strong resistance can be found at 50.41 (31/07/2017). Expected to monitor resistance at 50.41(31/07/2017 high).

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

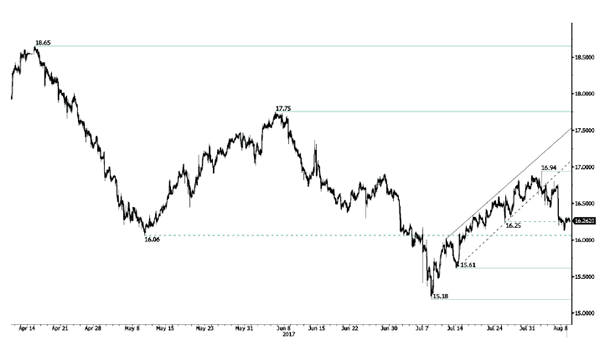

Silver Going lower

Silver's bullish pressures have faded after the commodity reached hourly resistance at 16.94 (02/08/2017 high). The commodity has broken hourly support at 16.25 (25/07/2017 low). Expected to continue pushing lower.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

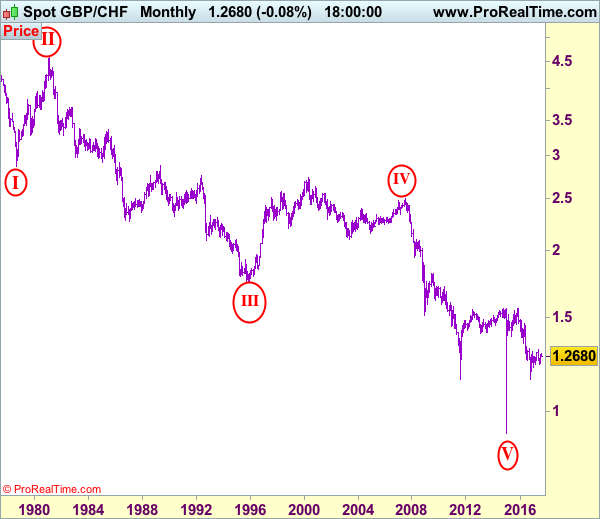

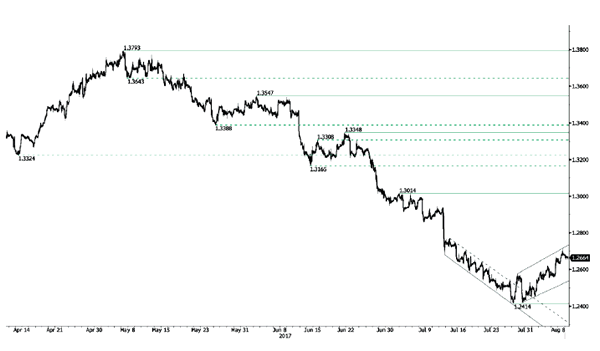

GBP/CHF Elliott Wave Analysis

GBP/CHF – 1.2675

GBP/CHF – Circle wave v ended at 0.9106 and major correction has commenced for subsequent gain to 1.5547.

Despite falling to 1.2270 late last month, as sterling found decent demand there and has staged a much stronger-than-expected rebound, suggesting early fall from 1.3069 top has ended at 1.2241 (June low) and consolidation with upside bias would be seen for another test of this month’s high at 1.2854, however, break there is needed to retain bullishness and extend the rebound from 1.2241 to 1.2900, then 1.2950, having said that, as broad outlook remains consolidative, reckon upside would be limited to 1.3000 and price should falter well below said resistance at 1.3069.

To recap the larger degree count, the selloff from 2.4965 (July 2007) is the beginning of wave V with circle and is labeled as 1: 2.3760, 2: 2.4425, wave 3 extension ended at 1.1470, followed by wave 4 at 1.5547, the quick rebound from 0.9106 suggests wave 5 as well as entire circle wave V could have ended there, hence consolidation with mild upside bias is seen for major correction to take place, bring initial test of 1.5547 (previous 4th of a lesser degree).

On the downside, although current retreat from 1.2854 suggests initial downside risk is for pullback to 1.2600-10, reckon downside would be limited to 1.2550 and 1.2525-30 should hold, bring another rise later. Below 1.2470-75 would abort and suggest top is formed instead, risk weakness to 1.2400-10 and then 1.2350 but price should stay above said support at 1.2270, bring another rebound later.

Recommendation: Stand aside for this week.

On the Monthly chart, the longer-term count is that major downtrend is under way with circle wave I at 2.8645 (Sep 1.978), then wave II with circle at 4.6175 (Feb 1981), the wave III with circle ended at 1.7425 (Nov 1995) and followed by wave IV with circle at 2.4965 (July 2007 with a short wave C) and wave V with circle has possibly ended at 0.9106. A monthly close above 1.5547 would add credence to this view, bring major correction to 1.7000, then towards psychological level at 2.0000.

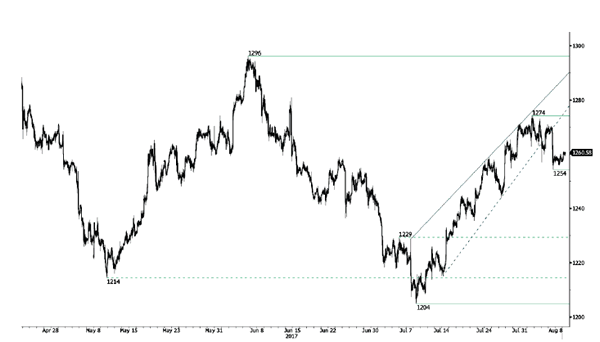

Gold Consolidation Phase

Gold is consolidating. Hourly support is given at 1254 (04/0782017 low). Strong support is given at 1204 (10/07/2017 high). Hourly resistance is given at 1274 (01/08/2017 high). Expected to see further consolidation.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low)

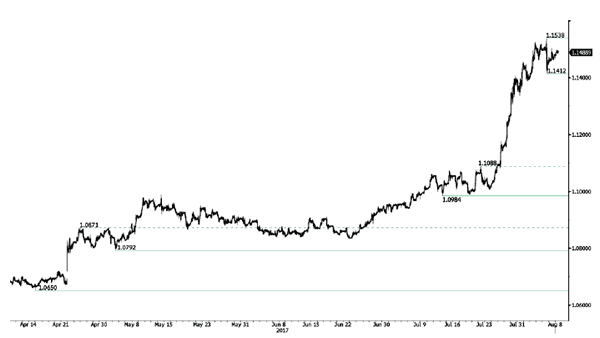

EUR/CHF Ready For Another Leg Higher

EUR/CHF has consolidated and short-term buying pressures are back. Hourly support is located at 1.1412 (04/08/2017 low). Expected to show another leg higher.

In the longer term, the technical structure has reversed. Strong resistance at 1.1200 (04/02/2015 high) has been broken. Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Bullish Pressures Persist

EUR/GBP is trading around its highest levels of the year. The pair keeps on pushing higher. Hourly resistance lies at 0.9054 (04/08/2017 high). Hourly support is given at a distance at 0.8742 (16/06/2017 low). Downside risks are nonetheless important.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

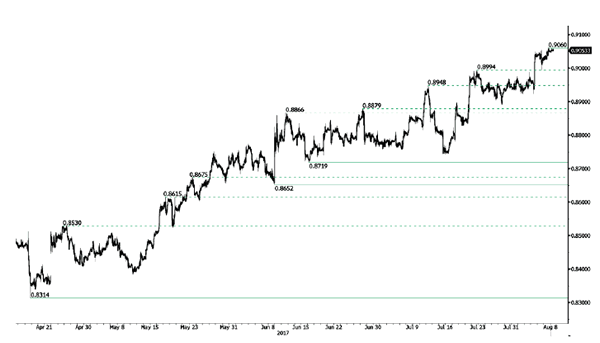

AUD/USD Growing Selling Pressures

AUD/USD's short-term technical structure is bearish. Hourly resistance is given at 0.8066 (27/07/2017 high) while hourly support can be found at 0.7875 (21/07/2017 low). Expected to show further consolidation.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

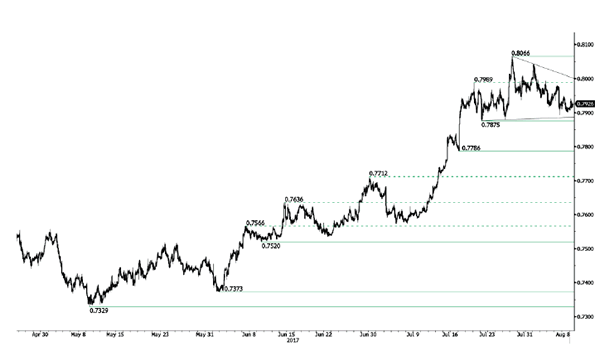

USD/CAD Short-Term Bullish Momentum Continues

USD/CAD's short-term bullish momentum continues. Hourly resistance is given at 1.2619 (03/08/2017) while support can be found at 1.2414 (27/07/2017 low). Expected to show continued consolidation above 1.2400.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low) before bouncing back. Strong resistance is given at 1.4690 (22/01/2016 high). The pair should head further lower.

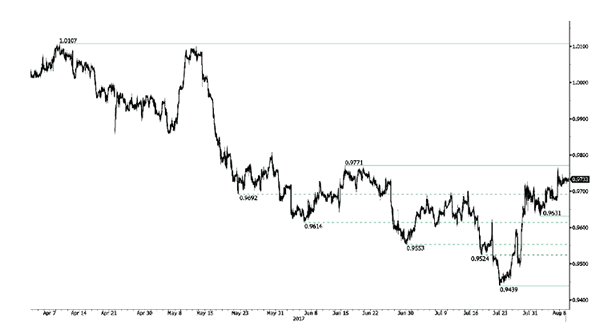

USD/CHF Testing Strong Resistance

USD/CHF's bullish momentum continues. Hourly support can be found at 0.9631 (01/08/2017 low). Strong resistance is given at 0.9771 (15/06/2017 high) is on target. Expected to to show further strengthening.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

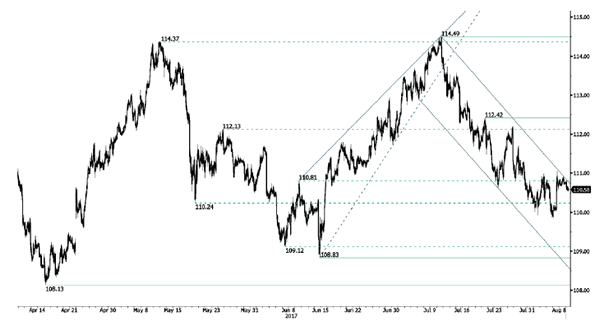

USD/JPY Riding Downtrend Channel

USD/JPY's bearish momentum continues. Yet, the pair is monitoring resistance implied by the upper bound of the downtrend channel. Hourly support is given at 109.85 (04/08/2017 low). Stronger support is located at a distance at 108.83 (17/04/2017 low). Expected to show further downside pressures.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).