Sample Category Title

Oil And Gold Take A Chill Pill And Becalm Down

Oil and gold remain becalmed ahead of various data points with only some Fed speeches and Noth Korea rhetoric stirring the otherwise placid waters.

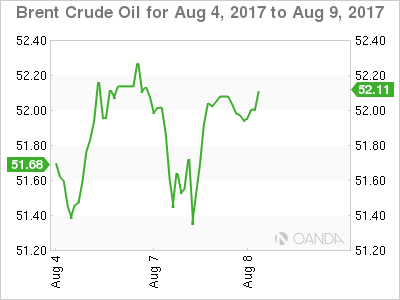

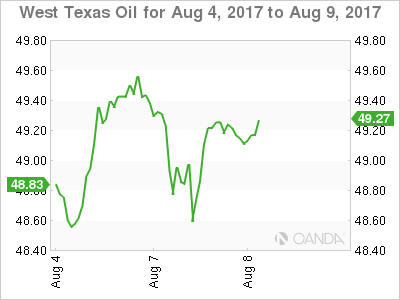

Oil remained locked into choppy range trading overnight as the market awaits the first of the crude inventory numbers of the week from the American Petroleum Institute. Both Brent and WTI spot fell some two percent as Libya announced its biggest oil field was resuming full production. Both contracts however shrugged of this new to make back almost all their losses and close virtually unchanged at 52.05 and 49.25 respectively.

Bulls can take heart from the comeback, but both Brent and WTI's ranges continue to contract in a quiet news environment, suggesting a breakout is imminent. Assuming that nothing comes from OPEC/Non-OPEC's technical meeting in Abu Dhabi today, oils near term fate will most likely be determined by the official U.S. Department of Energy inventory data tomorrow evening Asia time.

OIL

Brent spot is trading at 52.075 with its triple top resistance at 52.70 still untested. Some congestion below appears at 51.20 ahead of key support at 50.50, the 1st August low and the 100-day moving average.

WTI spot trades at 49.20, well below its double top at 50.30. Interestingly a triple bottom has formed over the last four sessions around 48.40 providing initial support ahead of 48.00 and then the key 47.70 level, the 100-day moving average.

GOLD

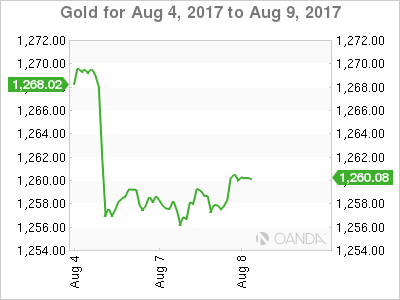

Gold consolidated near the bottom of its recent trading range overnight with a lack of new to provide any new price direction. Like many other markets this week, gold appears to be in a holding pattern with the increasing risk that stale long positioning may see traders head for the door until some directional clarity is restored.

Gold traded in a 1255/1260 range overnight and opened at a sleepy 1258.50 level this morning in Asia. Some dovish comments from Fed Governors Kashkari and Bullard along with the day's daily dose of sabre rattling from North Korea has seen gold drift higher to 1260.00. However, initial daily resistance still lies distantly at 1274.20 with the near term support much closer and likely to be of more concern to traders.

The Friday low and also the 100-day moving average is just below current levels at the 1253.00 regions, followed by the 50% Fibonacci retracement at 1249.20. A daily close below these levels would be a concerning development for gold bulls, suggesting a further test to the 1243 regions and possibly a deeper retracement to the 200-day moving average at 1230.00.

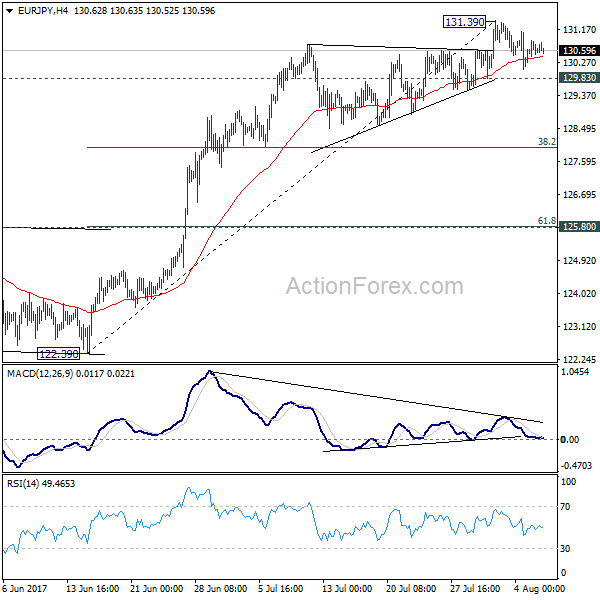

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.31; (P) 130.59; (R1) 130.87; More...

Intraday bias in EUR/JPY remains neutral for the moment. A short term top is in place at 131.39 on bearish divergence condition in 4 hour MACD. Break of 129.83 will confirm and turn bias to the downside for 38.2% retracement of 122.39 to 131.39 at 127.95. But we'd expect strong support from there to contain downside and bring rebound. On the upside, break of 131.39 is needed to confirm rise resumption. Otherwise, more consolidative trading is expected with risk of another fall.

In the bigger picture, the down trend from 149.76 (2014 high) is completed at 109.03 (2016 low). Current rally from 109.03 should be at the same degree as the fall from 149.76 to 109.03. Further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. Medium term outlook will remain bullish as long as 124.08 resistance turned support holds.

Markets Look To OPEC

As OPEC began its 2-day meeting in Abu Dhabi on Monday, to align its members to adherence to output reductions, data from S & P Platts revealed that Libya and Nigeria pushed OPEC’s crude oil output in July to the highest level this year at 32.82 million barrels a day. Per Platts; Libya and Nigeria (both exempt from the cuts agreed last year) oil production went up 210K barrels per day in July, 210K bpd and 1.81 million bpd respectively. If the data from Platts is correct then OPEC’s output in July was 920K bpd above the ceiling of 31.9 million bpd OPEC set last year. It is evident that compliance with the cuts is not being made, thus leading to an oversupply that has kept WTI below $50. The markets will be waiting to see if OPEC makes further demands of its members to reduce production and, more importantly, that its members abide by such demands.

In currencies, USD edged lower on Monday, giving back some of its gains from Friday, as the markets became cautious ahead of inflation data this week that may signal a reversal in USD weakness. Finally, the latest economic data out of China pointed to steady global demand. While exports missed market estimates, rising 11.2% in July in yuan terms, demand for Chinese goods held up in the face of escalating tensions with the US.

EURUSD trading was relatively light on Monday, trading in a narrow 43.7 pip range as it made some gains from Fridays sell-off. Currently, EURUSD is trading around 1.1805.

USDJPY was also trading in a narrow range of less than 28 pips on Monday. Currently, USDJPY is trading around 110.60.

GBPUSD appears to have found some support just above 1.30 on Monday in relatively light trading. Currently, GBPUSD is trading around 1.3045.

Gold edged lower on Monday, failing to gain support from a weaker USD, as the markets digested sharp losses in the previous session and worried about further U.S. rate hikes. Currently, Gold is trading around $1,260.00.

WTI lost 1.2% on the day, as Oil failed to recover from recent USD strength. WTI currently trades around $49.40pb.

Economic data releases on Tuesday are, somewhat, second tier – with little expected impact on the markets.

Day 2 of the OPEC meeting in Abu Dhabi ends. The main focus being members’ compliance to the output pact the cartel inked with 10 other oil suppliers, including Russia, in late 2016. The deal so far has not produced meaningful effects to reduce global output or inventories.

Market Update – Asian Session: Japan And N. Korea Hold Short Meeting

Asia Summary

Asian markets opened mixed, with USD weakening during the session. China reported its July trade balance data, exports slowed for the 5th consecutive month. The yuan rose 0.25% against the USD, after trade data, to 6.7044. Notably steel product exports were down ~29% y/y at a 2013 low. AUD/USD rose after July business confidence and conditions rose. Fresh talks recirculated that the yuan trading band could be expanded later this year. Japan and Korea markets were little moved on the report that Japan and North Korea foreign ministers briefly met yesterday. No further details were given on the meeting.

Key economic data

(CN) CHINA JULY TRADE BALANCE (CNY): 321.2B V 297.4BE; Exports Y/Y: 11.2% v +15.2%e, Imports Y/Y: 14.7% v 22.6%e

(CN) CHINA JULY TRADE BALANCE: $46.7B V $45.0BE; Exports Y/Y: 7.2% v +11.0%e; Imports Y/Y: 11.0% v +18.0%e

(JP) JAPAN JUN TOTAL CURRENT ACCOUNT: ¥934.6B V ¥860.5BE; ADJ TOTAL CURRENT ACCOUNT: ¥1.52T V ¥1.50TE; TRADE BALANCE BOP BASIS: ¥518.5B V ¥571.5BE

(JP) JAPAN JUL BANK LENDING (INC TRUSTS) Y/Y: 3.3% V 3.3% PRIOR; BANK LENDING (EX-TRUSTS) Y/Y: 3.4% V 3.3%E

(AU) Australia July NAB Business Confidence: 12 v 8 prior; Conditions: 15 v 14 prior

Speakers and Press

China

(CN) Trump delays intellectual property investigation into China by at least 1-week after China backed UN sanctions against North Korea

Australia

(AU) Australia Trade Min Ciobo: Stronger A$ is making exports less competitive

(AU) Australia July Port Hedland Iron Ore Exports: 37.9Mt v 43.1M tons prior; Iron ore exports to China 32.0Mt v 36.6M tons prior

Korea

(KR) North Korea Foreign Min Yong Ho: Will not give up its nuclear weapons under any circumstances

Japan

(JP) Japan Chief Cabinet Sec Suga: Japan and North Korea Foreign Mins met briefly yesterday

(JP) Former BOJ Deputy Gov Iwata: BOJ should proceed with current slowdown in JGB buying so annual pace of buying eventually falling to ¥40T from ¥80T

Asian Equity Indices/Futures (00:00ET)

Nikkei -0.3%, Hang Seng +0.1%, Shanghai Composite -0.2%, ASX200 -0.7%, Kospi -0.1%

Equity Futures: S&P500 -0.1%; Nasdaq100 -0.1%, Dax -0.2%, FTSE100 -0.2%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1824-1.1791; JPY 110.81-110.57; AUD 0.7939-0.7906; NZD 0.7369-0.7351

Dec Gold +0.1% at 1,265/oz; Sept Crude Oil -0.3% at $49.23/brl; Sept Copper -0.3% at $2.90/lb

(AU) Australia sells A$150M in 2030 bonds; avg yield 0.8959%; bid-to-cover 7.04x

(CN) China PBOC OMO injects CNY140B in 7 and 14-day reverse repos v CNY250B prior; Drains net CN0Y v CNY60B prior

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT: 6.7184 V 6.7228 PRIOR

JGB (JP) Japan MoF sells ¥647B v ¥800B indicated in 0.8% (0.8% prior) 30-yr bonds; Avg yield: 0.8760% v 0.8780% prior; Bid to cover: 3.90x v 3.62x prior (highest bid-to-cover since March 2016)

Equities notable movers

Hong Kong/China

Geely, 175.HK Reports July Vehicle sales 91.1K units +88% y; +3.8%

Japan

Suntory Beverage, 2587.JP Reports Q1 Net ¥20.5B v ¥17.9B y/y; Op ¥43.0B v ¥39.9B y/y; Rev ¥689.6B v ¥679.1B y/y; -4.5%

Korea

Kia, 000270.KR Seoul Court to rule on base pay case on Aug 17th - South Korean press; -4.5%

Australia

Mobile Embrace, MBE.AU Reports FY17 EBITDA A$5.3M v A$5-6M guided; Rev A$52.1M v A$52M guided: Names Neil Wiles new CEO; +18.7%

Cudeco,CDU.AU Reports July Rocklands shipment of 8,620 WMT, valued at A$17.4M; +10%

James Hardie, JHX.AU Reports Q1 Net $57.4M v $87.1M y/y; Rev $507.7M v $477.7M y/y; -5.3%

CBA.AU Says CEO Narev retains 'full confidence of the board'; Narev short-term variable pay to be cut to zero; -1.2%

Other

Shin Kong Financial, 2888.TW Reports July Net NT$6.84B v NT$2.07B m/m; +10%

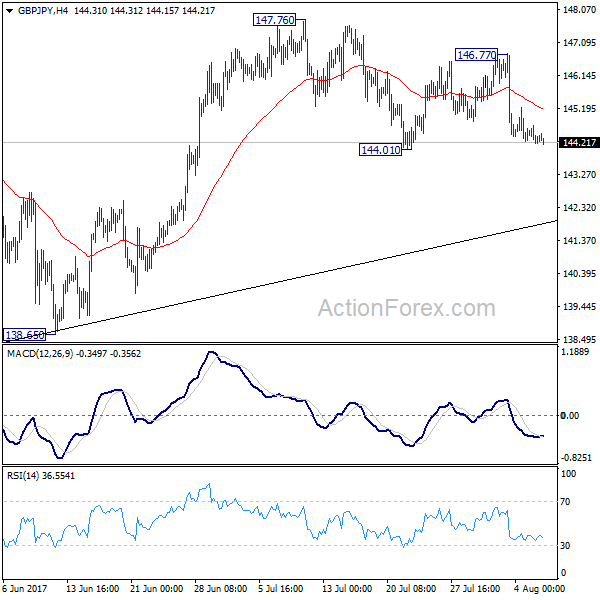

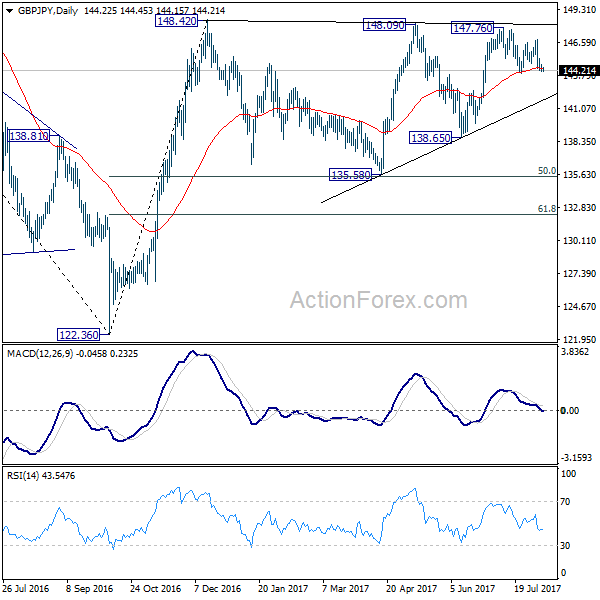

GBP/JPY Daily Outlook

Daily Pivots: (S1) 144.08; (P) 144.40; (R1) 144.62; More

GBP/JPY is staying in range and intraday bias remains with focus on 144.01 support. Break will turn bias to the downside for trend line support (now at 141.87). Further break there will target 135.58/138.65 support zone. However, above 146.77 will turn bias to the upside. Further break of 147.76/148.42 key resistance zone will resume larger rebound from 122.36.

In the bigger picture, rise from medium term bottom at 122.36 is expected to continue to 38.2% retracement of 196.85 to 122.36 at 150.43. Decisive break there will carry long term bullish implications and pave the way to 61.8% retracement at 167.78. In case the sideway pattern from 148.42 extends, we'd be looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside.

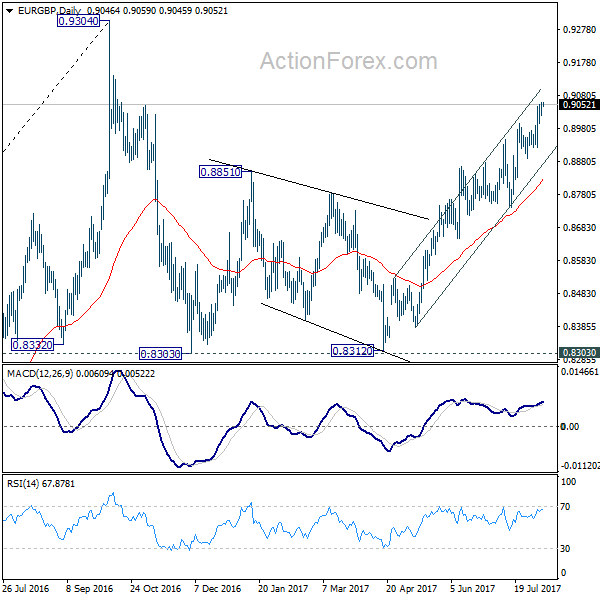

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.9027; (P) 0.9043; (R1) 0.9066; More

Intraday bias in EUR/GBP remains on the upside for the moment. Current rise from 0.8312 should extend towards 0.9304 key high. At this point, there is no clear sign of up trend resumption yet. Hence, we'll be cautious on strong resistance from 0.9304 to limit upside and bring another fall. Meanwhile break of 0.8922 support will indicate short term topping and turn bias to the downside for 0.8742 support.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

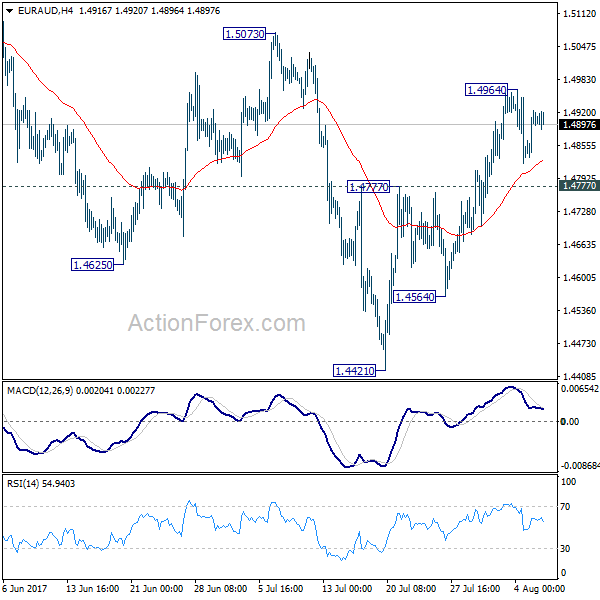

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4849; (P) 1.4887; (R1) 1.4939; More...

Intraday bias in EUR/AUD stays neutral at this point. Near term outlook remains bullish with 1.4777 support intact and further rally is expected. As noted before, correction from 1.5226 should have completed with three waves down to 1.4421 already. Above 1.4964 will target 1.5073 resistance first. Break of 1.5073 will likely resume the rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4421 at 1.5411 next. However, firm break of 1.4777 will dampen this bullish view and turn bias to the downside for 1.4564 support. Break will extend the correction from 1.5226 through 1.4421.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to resume to retest 1.6587. The corrective structure of the fall from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, another decline will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

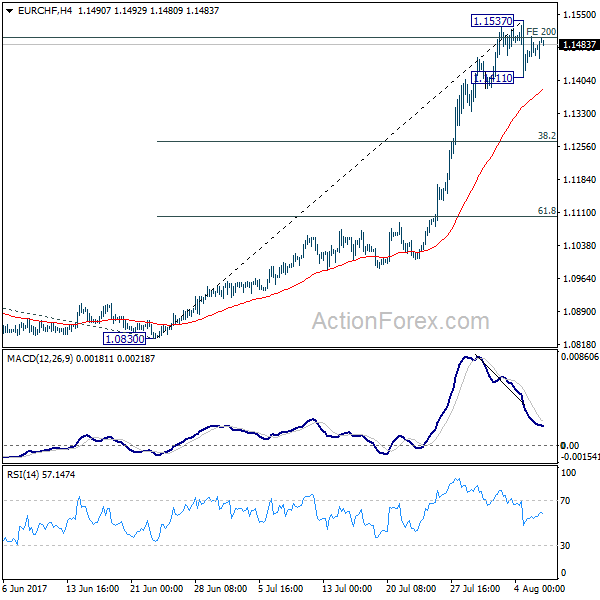

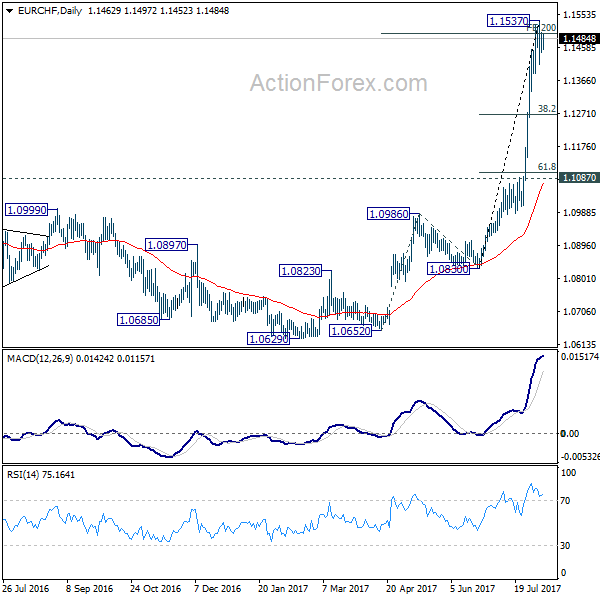

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1451; (P) 1.1476; (R1) 1.1505; More...

Intraday bias in EUR/CHF remains neutral for the moment. A short term top should be formed at 1.1537 on bearish divergence condition in 4 hour MACD, after hitting a key projection level. More corrective trading and deeper fall is expected in near term. Below 1.1411 will target 4 hour 55 EMA (now at 1.1385) and below. But downside should be contained by 38.2% retracement of 1.0830 to 1.1537 at 1.1267 and bring rebound.

In the bigger picture, sustained break of 1.1198 key resistance confirms resumption of the long term rise from SNB spike low back in 2015. In this case, EUR/CHF would eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

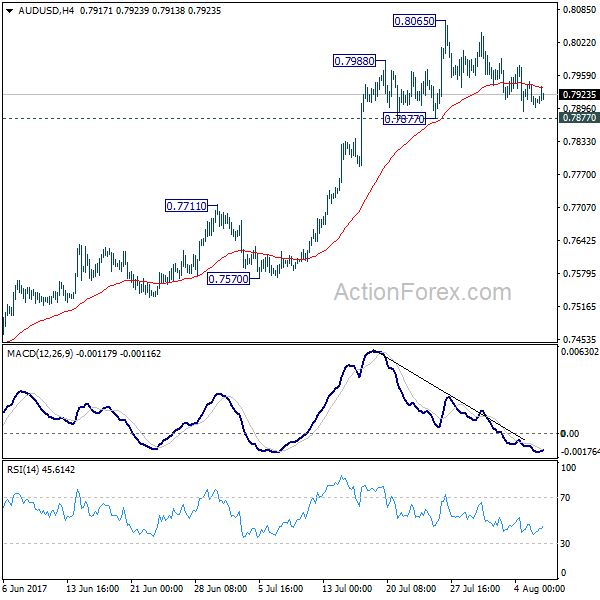

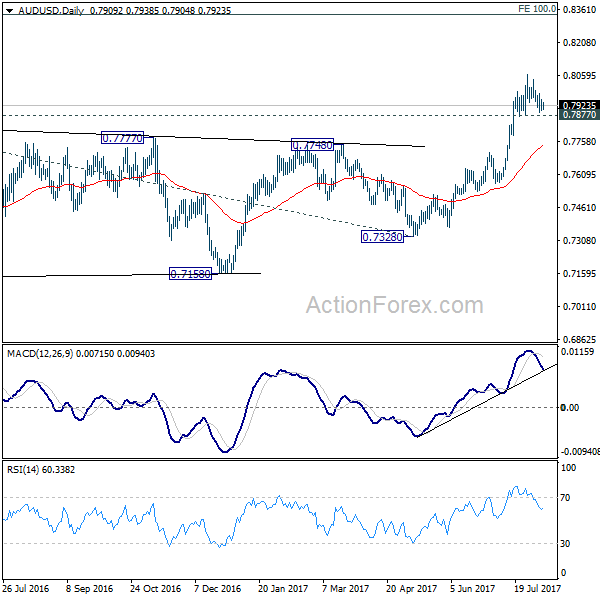

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7893; (P) 0.7920; (R1) 0.7942; More...

AUD/USD is staying in consolidation from 0.8065 and intraday bias remains neutral. As long as 0.7877 support holds, another rise remains mildly in favor. Break of 0.8065 will target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335. Nonetheless, break of 0.7877 will indicate short term topping, with bearish divergence condition in 4 hour MACD. In such case, intraday bias will be turned back to the downside for 0.7711 resistance turned support.

In the bigger picture, current development suggests that rebound from 0.6826 is developing into a medium term rise. There is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8100) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now expected.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2633; (P) 1.2673; (R1) 1.2719; More....

Intraday bias in USD/CAD remains on the upside as rebound from 1.2412 short term bottom continues. Such rebound should be corrective whole fall from 1.3793. Further rise would be seen back to 38.2% retracement of 1.3793 to 1.2412 at 1.2940. On the downside, break of 1.2552 minor support will indicate completion of the rebound. In such case, intraday bias will be turned back to the downside for 1.2412 low.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. A short term bottom is formed at 1.2412 after hitting 61.8% projection of 1.4689 to 1.2460 from 1.3793 at 1.2415. But there is no sign of completion of the correction yet. Break of 1.2412 will target 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Meanwhile, sustained break of 1.2968, 38.2% retracement of 1.3793 to 1.2412 at 1.2940 will be the first sign of completion of the correction and will turn focus back to 1.3793 key resistance.