Sample Category Title

GBP/JPY On A Declining Path

The downside momentum was paused by the median line (ml) of the minor descending pitchfork. Now could come back to retest the upper median line (uml) before will drop much deeper. We may have a selling opportunity if will retest the broken 150% Fibonacci line (ascending dotted line), the next downside target will be at the uptrend line.

EUR/CHF Stabilized In The Green Zone

EUR/CHF increased on Monday and continues to stay in the buyer’s area. The rebound invalidated the Friday’s breakdown below the fourth warning line (WL4). However, the rate could still come down to test and retest the WL4 and the second warning line (wl2) of the minor ascending pitchfork.

The current drop was natural after the failure to reach the confluence are formed by the third warning line (WL3) of the major ascending pitchfork with the second warning line (wl2).

EUR/JPY Changed Little

Price posted some gains on Monday and maintains a bullish perspective because is located above some important dynamic support levels. Could come down to retest the support lines before will try to climb much higher.

EUR/JPY shows some exhaustion signs on the daily chart, but right now we don't have a reversal sign. We have a bearish divergence on the Daily chart, but is premature to say that we'll have another leg lower. Price could decrease again if the Nikkei stock index will decrease, today has jumped higher and is trading near the 20058 major static resistance.

JP225 is narrowing on the short term, a further increase towards the 20320 previous high will force the Yen to depreciate versus its rivals.

The Yen needs a bullish spark to be able to take the lead again, the Japanese Current Account could increase from 1.40T to 1.51T in June, while the Bank Lending could increase by 3.3%, matching the 3.3% growth in the former reading period. The Economy Watchers Sentiment could drop in the pessimism territory if will decrease from 50.0 points to 49.8 points.

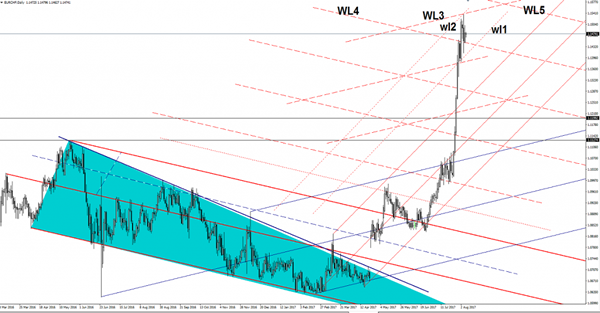

You can see that has failed to stay much above the 130.76 previous high and now has come back down and could retest the median line (ml) of the minor ascending pitchfork. We have a bullish bias as long as it is trading above the median line (ml) and above the upper median line (UML) of the major ascending pitchfork, only a valid breakdown below these obstacles will open the door for a broader decrease.

Don’t Get Too Complacent, It’s Only Tuesday

Don't get too complacent; it's only Tuesday

The markets took Monday off after a frenzied NFP Friday. There remains a bit of confusion regarding Friday's dollar price action.However with EUR struggling to gain any momentum above 1.1800 overnight, it would suggest traders are still expecting a deeper USD correction, so the dollar bears are holding off for now.

The dollar remains tentatively bid post-NFP as dealers are likely more concerned with overcrowded dollar shorts that appear more brittle now than in anytime during the past 4-6 weeks

The data void overnight has certainly dampened enthusiasm in Forex markets. However, all eyes are looking towards Friday's US CPI print.Given the enormity of inflation metrics in the Fed's rates outlook, I suspect traders will be reluctant to commit big views before the event and even more so given August's sparse liquidity conditions

Equities continue to enjoy the 'Goldilocks Markets' as the Dow recorded its ninth straight record close. Certainly, investors are showing little concern for ' irrational exuberance.' but provided the Feds keep the money tap open, the party will rave on.

Fed Bullard rolled out this usual dovish rhetoric anguishing over the low-inflation environment while crediting the USD weakness entirely on EU economic growth and a hawkish ECB. Fed's Kashkari predictably waxed dovish on the low inflation low wage growth narrative. But investors could turn circumspect as the market prepares for the numerous possibilities around the US debt ceiling showdown.

Euro

No significant data to hang one's hat on today but dealers are setting sights on Draghi's highly anticipated speech at Jackson Hole. But given the two way USD risk due to a combination of thin August liquidity and crowded dollar short positioning makes for dangerous trading conditions. That said, I think the market is in agreement EUR strength should run further' which suggests that the EURO will remain bid on dips, little momentum in the markets which is clouding trader views.

That said, I think the market is in agreement EUR strength should run further implying the EURO will remain bid on dips, but little momentum in the market's traders views are clouded.

Australian and New Zealand Dollars

Both AUD and NZD are trading on the soft side following US NFP

The Kiwi has remained under pressure after New Zealand lowered their 2y Inflation expectations. But of course, the focus this week is on the RBNZ OCR on Wednesday. No policy shift is expected, but given the run of weak domestic data and a stronger local unit driven by a weaker US dollar, there is room for a dovish lean from the RBNZ in an attempt to influence the currency. The Kiwi's underperformance on the crosses would suggest this view also.

As for the Aussie, it's a very sparsely populated domestic macro calendar, so the market remains in wait and sees mode. But Low oil prices and a looming OPEC meeting continues to weigh massively on the Energy sector, and by proxy the commodity bloc.

Regional focus shifts to China trade figures due out later today

Japanese Yen

Extremely quiet trade and has barely budged over night. A sign that dealers are unwilling to engage and waiting for clearer signals.

EUR/USD is Consolidating after Recent Volatility

The market has shown low volatility level after confident growth of the US dollar on the background of positive news from the labor market. The unemployment rate in the US fell by 0.1% to 4.3% and non-farm payrolls increased by 209.000 in July against the expected 182.000. These statistics slightly increased the probability of another rate hike by the Fed before the end of the year. Investors may keep fixing positions after a strong rally during the previous weeks.

Additional pressure on EUR/USD quotes came from Germany where the industrial production level in June declined by 1.1% against predicted growth of 0.2%. The Sentix investor confidence index also declined to 27.7 in August which is 0.6 less than in July.

The British pound is losing positions amid speculations about negotiations on the Brexit terms that may last until 2022. Lack of significant progress in the talks on this key issue will put pressure on the pound that is currently influenced by the slowing pace of GDP growth in the UK. The stronger than expected data from the Halifax house price index in the UK for July which showed an increase by 0.4% after declining by 0.9% in June was not able to change the market mood regarding the sterling.

The USD/JPY is consolidating after an increase on Friday and ahead of the report on the current account balance at 23:50 GMT. Considering the growth of the US dollar the resumption of a fall for the guppy is less likely in the coming days.

EUR/USD

The common currency quotes corrected upwards after a strong decline at the end of the previous week. In case of a further increase and overcoming the 1.1800 mark, we are likely to see growth up to 1.1900. On the other hand, recent price fixing below 1.1800 may be a strong sell signal with the stop above 1.1900 and potential targets at 1.1700 and 1.1620.

GBP/USD

The GBP/USD price is moving below the angled resistance line. Recently the price was consolidating near the important 1.3050 level and afterwards resumed dropping. On one hand, it may be judged a signal for a further decline to 1.2950 and lower but the RSI on the15-minute chart points to a possible rising correction in the coming hours.

USD/JPY

The USD/JPY is consolidating near 110.70. In case of overcoming the resistance at 111.00 on the 15-minute chart, we may see the double bottom formation that is a reversal pattern. In this case, the immediate objectives will be placed at 113.00 and 114.70. The decline is likely to be limited by support at 110.00.

Gold Stabilizes After Friday Slide

Gold is almost unchanged in the Monday session, after strong losses on Friday. In North American trade, spot gold is trading at $1259.10, down 0.03% on the day. On the release front, there are no major events on the schedule. On Tuesday, the US releases JOLTS Jobs Openings, which is expected to edge lower to 5.66 million.

The Federal Reserve is sounding less sure about a final rate hike in 2017, and the markets remain skeptical, with the odds of a December move below 50%. Investors have now shifted their attention to the Fed's balance sheet, which stands at $4.2 trillion. Fed policymakers have broadly hinted at reducing purchases of bonds and securities starting in September, but San Francisco Fed President John Williams was more forthcoming about the Fed's plans, likely aimed at giving notice to the markets. In a speech on Wednesday, Williams said that the economy had "fully recovered" from the 2008 financial crisis and called on the Fed to start trimming the balance sheet "this fall". Williams added that the process would be gradual and would take four years to reduce the balance sheet to a "reasonable size". Other FOMC members have also come out in favor of the Fed starting to wind up its portfolio this fall. A reduction in the Fed portfolio would likely push gold prices lower, with the Institute of International Finance estimating that a reduction of $200 billion in the balance sheet would be equivalent to three normal interest hikes. Gold prices move inversely to rate hikes, so as the Fed trims down its portfolio, the dollar could move higher against gold.

Pound Dips Close to 1.30 as NFP Boosts Greenback

GBP/USD has posted small losses in the Monday session. In North American trade, the pair is trading at 1.3030, down 0.13% on the day. On the release front, it's a quiet start to the week, with no major events on the schedule. On Tuesday, the US releases JOLTS Jobs Openings, which is expected to edge lower to 5.66 million.

The British pound had a rough week, as GBP/USD slipped 0.09%. The dollar posted broad gains on Friday, as the July nonfarm payrolls report was better than expected. The indicator came in at 209 thousand, easily beating the estimate of 182 thousand. The unemployment rate edged lower to 4.3%, but the positive news was dampened somewhat by wage growth, which remained unchanged at 0.3%. This underscores weak inflation levels, which has left investors skeptical as to whether the Federal Reserve will raise rates one final time in 2017. On Thursday, the pound reacted negatively as the BoE cut its growth forecasts for 2017, from 1.9% in May to 1.7%, and for 2018, from 1.7% to 1.6%. As well, the bank sharply cut lowered its wage growth forecast for 2018, from 3.5% to 3.0%. The BoE held rates at 0.25%, but the minutes from the policy meeting were dovish, with MPC members warning that "GDP growth had been sluggish and was expected to remain so in the near term." The BoE's pessimistic message has dashed hopes of a rate hike before the end of the year, although the bank suggested that a slight improvement in growth could lead to a rate hike in 2018. BoE policymakers have publicly argued about monetary policy, and the vote at Thursday's meeting, 6 members favored holding rates, while only 2 members voted to raise rates. The British economy has slowed down, but the bank is reluctant to raise rates when inflation is running at 2.6%, well above the bank's target of 2%. To complicate matters, the Brexit talks have made little progress, raising fears of a messy exit from the EU, which could take a serious toll on the British economy. The City of London, a key European financial center, stands to lose thousands of financial jobs due to Brexit. Deutsche Bank announced that it will move at least 2,000 jobs from its London office to Frankfurt, and RBS has announced that it will relocate its London office to Amsterdam.

With the odds of a December rate hike at less than 50%, investor attention has shifted to the Fed's balance sheet, which stands at $4.2 trillion. Fed policymakers have broadly hinted at reducing purchases of bonds and securities starting in September, but San Francisco Fed President John Williams was more forthcoming about the Fed's plans, likely aimed at giving notice to the markets. In a speech on Wednesday, Williams said that the economy had "fully recovered" from the 2008 financial crisis and called on the Fed to start trimming the balance sheet "this fall". Williams added that the process would be gradual and would take four years to reduce the balance sheet to a "reasonable size". Other FOMC members have also come out in favor of the Fed starting to wind up its portfolio this fall.

Euro Struggles to Rise after German Industrial Production; Oil Bounces as Libya’s Largest Oilfield is Disrupted

As the economic calendar was lacking important data, the European session was quiet with the markets digesting the release of the German industrial production and the Halifax house price index, the only closely watched indicators of the day. Moreover, while investors were focused to catch any hints from the two-day OPEC/non-OPEC meeting launched today, energy prices initially edged higher before backtracking later in the day.

The dollar was more or less steady against its rivals during European trading, with the dollar index moving sideways around 93.30. Earlier, the dollar fell below its one-week high of 93.61 reached on Friday when better than expected non-farm payrolls pushed the dollar higher. Now, investors who continue being cautious about the political developments in the US, expect CPI and PPI data, to be released at the end of the week, in order to get more evidence on the subdued inflation. Based on forecasts, analysts anticipate the core CPI to grow flat at 1.7% in July year-on-year and the PPI to increase by 2.2% from the 2% estimated in June. Any improvements in inflation would motivate Fed policymakers to hike rates for the third time this year and reduce the Fed's overloaded balance sheet sooner.

The euro struggled to hold onto its intraday gains after German industrial production for the month of June disappointed forecasts. German industrial output surprisingly plummeted for the first time this year by 1.1% in June month-on-month from a positive 1.2% observed in May, while analysts anticipated output to rise moderately by 0.2%. This weighed on Germany's benchmark 10-year government bond yield which scaled back on Monday by one basis point to 0.46 percent from 0.47 percent seen on Friday amid concerns that the ECB will unwind its ultra-easy monetary policy later rather than sooner.

Euro/dollar was last eyeing the 1.18 handle, while euro/yen was up by 0.26% at 130.68. Meanwhile, euro/pound hit a fresh 11-month high of 0.9060 during today's trading.

Sterling followed a downward path after not so optimistic comments from a former top diplomat pushed the currency down by 0.20% to $1.3024. Simon Fraser, who was the senior civil servant at Britain's Foreign Office and the head of the UK Diplomatic Service until 2015 said on Monday that Brexit negotiations have not started "promisingly, frankly on the British side", attributing the outcome to disagreements between May and her team on the type of deal they want to conclude with the EU. Despite May's spokesman expressing his opposition to this as well as to Sunday's news of Britain agreeing to pay a £40 billion EU exit bill, the pound could not bounce back. Moreover, the Halifax house price index which was released earlier in the day and which rose slightly above expectations, could not support sterling either. The index which is estimated by the Halifax Bank of Scotland, one of the largest mortgage lenders in the UK, increased by 2.1% in July year-on-year, below June's reading of 2.6% but above the mark of 2% forecasted by analysts. On a monthly basis, the index improved from a negative 0.9% in June to a positive 0.4%. Expectations were set at a growth of 0.2%.

Regarding energy markets, WTI and Brent were last down 1.8% and 1.7%, trading at $48.66 and $51.50 per barrel respectively. OPEC and non-OPEC members are gathering in Abu Dhabi on Monday and Tuesday to discuss their compliance regarding output cuts. Meanwhile, other news out of the industry were that Libya's largest oilfield, Sharara, is getting ready to shut down according to an engineer working in the field, as the field is said to have been attacked by an army group. This development provided some short-term boost to oil prices during afternoon European trading hours.

Yen Quiet, Markets Eye Japanese Current Account

USD/JPY is almost unchanged in the Monday session. In North American trade, the pair is trading at 110.80, up 0.11% on the day. On the release front, it's a quiet start to the week, with no US releases on the calendar. Later in the day, Japan releases Current Account, with the surplus expected to climb to JPY 1.51 trillion. On Tuesday, the US publishes releases JOLTS Jobs Openings, which is expected to edge lower to 5.66 million.

The US dollar pushed the yen lower on Friday, courtesy of a solid nonfarm payrolls report. The indicator came in at 209 thousand, easily beating the estimate of 182 thousand. The unemployment rate edged lower to 4.3%, but the positive news was dampened somewhat by wage growth, which remained unchanged at 0.3%. This underscores weak inflation levels, which has left investors skeptical as to whether the Federal Reserve will raise rates one final time in 2017.

Last week's strong US payrolls report boosted the US dollar and raised the odds of a December rate hike, which are currently at 47%, up from 43% one week ago. With the Federal Reserve unlikely to raise rates before December, investor attention has shifted to the Fed's balance sheet, which stands at $4.2 trillion. Fed policymakers have broadly hinted at reducing purchases of bonds and securities starting in September, but San Francisco Fed President John Williams was more forthcoming about the Fed's plans, likely aimed at giving notice to the markets. In a speech on Wednesday, Williams said that the economy had "fully recovered" from the 2008 financial crisis and called on the Fed to start trimming the balance sheet "this fall". Williams added that the process would be gradual and would take four years to reduce the balance sheet to a "reasonable size". Other FOMC members have also come out in favor of the Fed starting to wind up its portfolio this fall.

Japan's economy has shown improvement, but the Japanese consumer remains pessimistic about economic conditions. Consumer Confidence moved higher in July, with a reading of 43.8 points. This marked a 4-month high. The lack of confidence in the economy has resulted in soft borrowing and spending levels. At the same time, manufacturing and housing indicators looked sharp earlier this week. Preliminary Industrial Production rebounded with a strong gain of 1.6%, after a decline of 3.3% a month earlier. As well, Housing Starts gained 1.7%, compared to a reading of -0.3% in May. These numbers underscore a stronger Japanese economy, buoyed by stronger demand for Japanese exports. However, weak inflation levels remain a serious concern. The BoJ's ultra-loose monetary policy has failed to coax inflation upward. At its recent policy meeting, the BoJ again extended its time-frame for reaching its inflation target of 2%. The bank is reluctant to scale back its asset-purchase program, which means that it will likely lag behind other central banks, such as the ECB, in reducing its stimulus program.

Elliott Wave Trade Ideas Performance Update

5 positions were entered last week with total profit of 65 points and the positions are listed below.

1 Aug : AUD/USD - Short at 0.8030,

1 Aug : EUR/GBP - Long at 0.8925, exited at 0.9025 (+ 100 points)

2 Aug : GBP/JPY - Long at 145.55, exited at 145.35 (- 20 points)

4 Aug : EUR/JPY - Long at 130.70, exited at 130.40 (- 30 points)

4 Aug : GBP/USD - Long at 1.3145, exited at 1.3160 (+ 15 points)

| AUD EUR/JPY EUR/GBP CAD GBP GBPJPY

Jan - 15 -275 - 35 -120

Feb + 140 -17 - 40 +11

Mar - 20 +115 +132 - 19

Apr + 30 - 40 +120 + 45

May - 55 +100 - 6 -65 -60

Jun + 81 +150 - 10 +185 -120 +205

Jul - 40 - 60

Aug - 30 + 100 +15 - 20

Sep

Oct

Nov

Dec

Y-T-D + 216 -112 +167 +463 -170 +110