Sample Category Title

The Political Headline Cup Runneth Over

The Political headline cup runneth over

There's never a dull moment in the Foggy Bottom these days as the market's conviction was dented overnight by uncertain monetary policy and the constant stream of US Special Prosecutor Mueller's Russia-Gate headlines which explain the overnight dollar swoon. Special Counsel Mueller has reportedly empanelled a grand jury to investigate Russia's alleged interference in the 2016 national elections. The grand jury is a sign that the investigation is growing in intensity over the Trump campaign's possible collusion with Russia. Another toxic elixir for the Greenback is brewing.

The Old Lady of Threadneedle Street ( Bank of England) kept policy on hold by a 6-2 vote, but the BOE statement views were very balanced and a complete departure from recent hawkish overtones that some MPC members have been expressing. On cue, the pound tanked 100 pips on the initial decision with EURGBP ripping higher through the .90, levels we have not seen since Nov 2016. With the BOE 2017 rate hike window likely nailed shut we should expect GBP to underperform G-10 particularly against the crosses. ( EURGBP and GBPAUD)

The US 10 years yield dipped on the BOE dovish tones which now has currency markets shifting their view to a similar dovish tack by the Federal Reserve Boards due to the incessant political fracas in Washington. US yields remained heavy all NY session weighing on the Greenback which received little help from economic data when US Non-manufacturing business grew slower than expected in July. Markets continue to re evaluate the likely impact of Fed policy in the wake of the political headlines and soft US data. The 10-year yield dropped five bps to 2.22%, while 30-year yield lost six bps, reaching 2.79%.

However, it was the Trump Russia -Gate headlines in late NY that has seen the psychologically key 110 level taken out in USDJPY.The Russia headlines are coming out fast and furious sending a shiver down investors spines. Where there is smoke, there may be fire so look for headlines risk to be front and centre as this inquisition expands.

And of course, we have the NFP later today as the all-important wage data will come under the markets glare. Crystal ball assumptions aside, one thing current price action is suggesting, this month's headline is unlikely to affect current market Fed view and that only much keener than expected rise in hourly earnings could provide any support to the beleaguered Buck. Given the elusiveness of wage growth in the current economic climate, a top side beat is highly unlikely. Even in an unlikely USD dollar rally post-NFP scenario, traders will be more inclined to fade dollar strength so look for any dollar rallies to be sold.

Blue chips continue to hit the higher ground, with the Dow posting a new all-time high again at 22,040 before trading lower towards day end. Apple and Amazon both lost nearly 1%, putting the most pressure on the S&P

Euro

The Euro is doing what the Euro has been doing for the past month, a buy in the dip but on an eventual clean break of 1.1900, we are likely in for some serious profit taking ahead of the magnetic 1.200 levels.The reason is the Drahi risk which is speaking at Jackson Hole later this month. While President Draghi did not sound any alarm bell about the Euros surge after last month's ECB, there are some concerns that the speed of the Euro rise will trigger a Jackson Hole response for the ECB president.

Japanese Yen

Abe's cabinet reshuffle overnight came and went without much ado but the US political headline risk, which is again rearing its ugly head, has sent a tremor across all asset classes as the USDJPY tracks in risk averse mode. We had been basing just below 110 in recent days so that the 109.75-85 area will be critical. However, with NFP later today it's unlikely we'll see any aggressive dollar moves until after the US jobs print.

Australian Dollar

The Australian Dollar traded heavy overnight only to get a reprieve from the general USD malaise.The focus will now be on Retail sales and the RBA's quarterly Monetary policy report later this morning.

Overnight RBA Harper told the Wall Street Journal that AUD strength was due to a disarticulate USD “The real economy in the U.S. is staging a quite remarkable recovery. You would expect that would lead to a stronger U.S. dollar.”

USD/CAD Canadian Dollar Lower Ahead Of US Jobs Data

The Canadian dollar has fallen versus the US dollar on Thursday with little help from energy prices that are softer after OPEC compliance concerns and awaiting the U.S. non farm payrolls (NFP) to be published on Friday, August 4 at 8:30 am EDT.

Canadian employment data will also be published on Friday. The jobs data has crushed expectations this year, with an outlier in the report published in May. While the forecast remains close to the past two month's estimate of 11,000 jobs the Canadian economy added 54,500 and 43,300. The US NFP report will get most of the spotlight as the USD will trade based on the indicator release, Canadian dollar investors will be on the lookout for confirmation of a strong recovery north of the border.

NAFTA renegotiations talks will begin in two weeks. Mexico and the US have said they favour a quick resolution to avoid further politicizing the negotiations with upcoming elections in 2018. Today the Mexican Minister of the Economy Idelfonso Guajardo has said that under a best case scenario the NAFTA would not be implemented before the end of 2018.

The USD/CAD gained 0.227 percent in the last 24 hours. The currency pair is trading at 1.2619 awaiting the US and Canadian employment reports from July. The loonie is near a two week low after having rallied for most of 2017 against the USD on the back of rising Trump uncertainty and a sudden change in monetary policy rhetoric for the Bank of Canada (BoC).

The central bank cut rates twice in 2015 to soften the blow to the economy from a drop in oil prices, but as crude has stabilized thanks to the efforts of the Organization of the Petroleum Exporting Countries (OPEC) the central bank had a quick turnaround in June and is now expected follow the July interest rate hike with another in October. The timing of the decision makes sense if the Canadian central bank wants to see if the Fed decides to start reducing stimulus in September and a Canadian rate rise could preempt a rate hike by the Fed in December

Housing prices in Canada, specially in Toronto seem to have come down following a change in regulation and the 25 basis rate hike in June. A second rate hike in October would further cool rising house prices as mortgage prices would climb. Toronto home sales have dropped 40 percent compared to a year ago, but higher prices prevail gaining 5 percent over the same period.

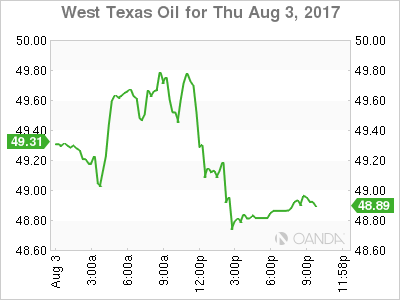

Energy prices fell 1.519 percent on Thursday. West Texas Intermediate is trading at $48.74 after yesterday's US crude inventories in particular the larger than expected rise in gasoline demand but the rise in Organization of the Petroleum Exporting Countries (OPEC) exports has reversed the trend.

The OPEC and other major producer agreement to limit crude production has stabilized prices but it enters into uncertain territory ahead of a meeting to discuss tighter compliance of members. There have been several voices of dissent and Iraq and the United Arab Emirates (UAE) are seen as wavering as their compliance numbers have slipped. The meeting on August 7 and 8 follows through the meeting in Russia last month where the same topics were discussed.

Market events to watch this week:

Friday, August 4

8:30 am CAD Employment Change

8:30 am CAD Trade Balance

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

Dollar Mixed Ahead Of Jobs Report

Wage Growth to Trump Number of Jobs Added

The US dollar is mixed on the Thursday session against the major currencies awaiting the release of the U.S. non farm payrolls (NFP) due Friday, August 4 at 8:30 am EDT. The US economy is anticipated to have gained 181,000 jobs in July but more importantly the average hourly earning to have risen 0.3 percent. The U.S. Federal Reserve could pause its monetary policy tightening if there is no clear evidence that inflation is moving closer to the 2 percent target.

US employment has been the most reliable pillar of the economy, but as headline job additions have kept a strong record, wage growth and labour participation have stagnated. The Fed is hoping the jobs recovery forces employers to offer more competitive salaries and gets people back on the hunt for jobs to keep on the path of more future rate hikes and the start of its balance sheet reduction program.

Canadian employment data will also be published on Friday. The jobs data has crushed expectations this year, with an outlier in the report published in May. While the forecast remains close to the past two month’s estimate of 11,000 jobs the Canadian economy added 54,500 and 43,300. The US NFP report will get most of the spotlight as the USD will trade based on the indicator release, Canadian dollar investors will be on the lookout for confirmation of a strong recovery north of the border.

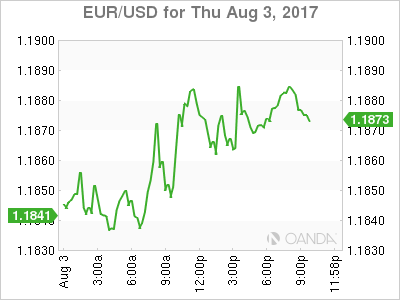

The EUR/USD lost 0.156 percent on Thursday. The single currency is trading at 1.1866 after breaking briefly above the 1.19 price level on Wednesday. The EUR has gained against the dollar after the turmoil in Washington has impaired the American currency. Employment data yesterday was not as strong as expected and put serious question marks on the NFP jobs report due Friday.

The ADP private payrolls report came in lower than expected at 178,000 jobs but there was some positive news with the upward revision to the already strong numbers from June. Wage growth was stuck at 2.5 percent which puts the emphasis on the NFP report to really move the needle for the USD.

The market is now unsure if the Fed will hike rates for the remainder of the year. The CME FedWatch tool is showing a 98.6 percent probability of the Fed funds rate staying at 100-125 in September but the December Federal Open Market Committee (FOMC) meeting is now 50/50 to end with rates going to 125-150 basis points. The Fed moved away from the patient mode it had displayed in the previous two years and has already hiked twice in 2017 and has signalled it will start to reduce the balance sheet it accumulated starting this fall.

The Trump administration has lost credibility after squandering important political capital by failing to push through health care reform and various changes in its first six months in power. The market was pricing in tax reform and infrastructure spending in what was called the Trump trade, but as those policies kept being pushed back the USD depreciated. Tax reform is back on the agenda, but there are serious questions on how optimistic the Administration is when it talks about an obstacle free path for the policy.

August will have very little economic events to guide the currency markets, leaving a lot in the hands of political uncertainty as the US relations with China and North Korea, and the upcoming start of NAFTA renegotiations talks could prove to be tough issues for the Trump administration, but with the benefit of less oversight from elected representatives in start contrast of the healthcare reform attempt.

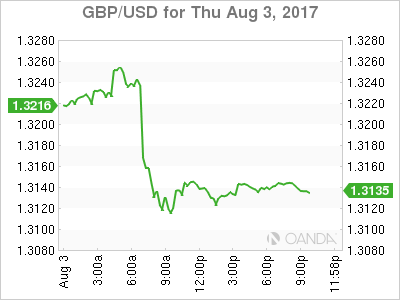

The GBP/USD lost 0.853 percent in the last 24 hours. The pair is trading at 1.3128 after the Bank of England (BoE) kept interest rates unchanged at 0.25 percent. The MPC voted 6-2 to keep rates at current levels. No surprise after last month the vote of 5-3, with a prominent hawk set to leave the committee. The pound dropped even after the BoE mentioned that rates could be higher after a year on the back of a strong jobs market and a global recovery but the ghost of Brexit kept the pound from gaining too much on those comments.

The BoE disclosed that Brexit uncertainty has discouraged employers from offering higher wages and with rising inflation that will continue to hit British pocket books. Updated forecasts on the UK economy were downgraded with higher inflation estimated did not leave the pound other option but to drop.

Market events to watch this week:

Wednesday, August 2

4:30 am GBP Construction PMI

8:15 am USD ADP Non-Farm Employment Change

10:30 am USD Crude Oil Inventories

9:30pm AUD Trade Balance

Thursday, August 3

4:30 am GBP Services PMI

7:00 am GBP BOE Inflation Report

7:00 am GBP MPC Official Bank Rate Votes

7:00 am GBP Monetary Policy Summary

7:00 am GBP Official Bank Rate

7:30 am GBP BOE Gov Carney Speaks

8:30 am USD Unemployment Claims

10:00 am USD ISM Non-Manufacturing PMI

9:30 pm AUD RBA Monetary Policy Statement

9:30 pm AUD Retail Sales m/m

Friday, August 4

8:30 am CAD Employment Change

8:30 am CAD Trade Balance

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

Dollar Digs Its Own Grave

Yesterday we wrote about potentially negative consequences of trade disputes on the US dollar, today it was soft economic data and more Russia drama hurting USD. The pound was the laggard on the day while yen led the way. US and Canadian jobs reports are up next. After closing out of the Premium cable long at 170-pip gain just ahead of the BoE decision, we opened a long above the prevailing price, which was not filled. The trade was cancelled and a new one was issued.

It's rarely one thing that sinks a currency. All the reasons to sell the US dollar would evaporate if growth was at 3%. Through the first half of the year, it's been at a 2% pace and the remainder of the year is a question mark.

One forward-looking indicator is the ISM non-manufacturing index but it stumbled on Thursday to 53.9 compared to 56.9. That set off another round of US dollar selling. Still, USD/JPY buyers made a stand at the weekly low and it bounced… at least until a few hours later when reports revealed Russia special prosecutor Robert Mueller had gathered a grand jury.

The last thing that's really propping up the dollar is the Fed. Despite a slightly more cautious tone at the Fed, the core of the FOMC is close to Williams who on Wednesday said he expects another hike this year and three more in 2018. If that happens the dollar will easily erase the last few months of losses.

The easy path to make that happen via tax reform and infrastructure spending. The problem now is that time is running out on the debt ceiling, and that will eat up more political capital, while the Russia story continues to eat up the remainder.

Still, the US economy has showed remarkable resilience despite Washington's best efforts for years and could do it again. A big signal will come Friday in the non-farm payrolls report. The consensus is 180K new jobs but the market will be almost-entirely focused on average hourly earnings, which are forecast up 0.3% and 2.4%. If those miss, the Fed and markets may begin to lose patience.

A central bank on the opposite side of the spectrum is the Bank of Canada. Canadian jobs data is also due Friday and expected at +10K. The consensus has consistently been too cautious and the numbers have beaten expectations in 10 of the past 11 months, often by a large margin. Another strong report could light another fire under CAD.

Has Swissie Bid Goodbye to its Highs for Good?

After two years of relative stability, the safe-haven swiss franc came into the spotlight again when it came under pressure against the euro last week and broke out of its long-term range. The much-desired weakness will likely be welcome by the Swiss National Bank which longs for a more export-competitive currency. However, the swissie remains "overvalued" as the level of risk aversion in the markets remains quite high despite investors' rising appetite for riskier assets. The question arising now is for how long the recent retreat will persist.

It was back in 2011 when the Swiss National Bank (SNB) decided to introduce a currency ceiling in a period when an extremely high level of uncertainty in the financial markets increased dramatically the demand for safe-haven assets and therefore strengthened the Swiss franc against other major currencies. The SNB in an attempt to protect domestic exporters from an overvalued currency set a limit of 1.20 francs to the euro, but after four years the SNB scrapped its ceiling, as the bank's foreign reserves reached almost 80% of Swiss GDP. On January 15, 2015, the swissie jumped by 20%, soaring to an all-time high of 0.8588 francs per euro. The euro managed to climb above parity only after the SNB applied an even looser monetary policy by reducing interest rates (three-month LIBOR) from -0.25% to -0.75%.

However, the swissie started showing signs of weakening recently, after the French elections this spring declared Eurozone supporter, Emanuel Macron, as the next president, removing a layer of uncertainty in the European political environment. Then, a few months later, the currency experienced further correction to the downside, when major central banks and particularly the European Central Bank (ECB) signalled to scale back their ultra-easy monetary policy soon as Eurozone economic indicators were seen to be gathering positive momentum. In addition, traders attributed the recent weakness in the safe-haven franc to decreasing spreads between European government bond yields, reflecting reduced risks for the Eurozone's periphery economies. For instance, the spread between the 10-year Italian and German bond yields narrowed by 50 basis points to 150 basis points in the last two months.

Despite the swissie having already entered a downward path, with euro/franc climbing for the first time above the 200-weekly moving average since 2008 and peaking at a 29-month high of 1.1453 on Monday, the SNB chief, Thomas Jordan, reiterated last week that the currency is still "significantly overvalued". Even though the improving economic climate in the eurozone is driving investors to reallocate their investment portfolio by switching safe-haven assets into riskier ones, political turmoil in the US, Brexit, and tension between the US, China, Russia, and North Korea is preventing traders from fully unwinding their low-risk assets that were accumulated after the financial crisis. Besides that, if inflation, which is a key determinant of monetary policy, fails to approach the target rates then major central banks will likely abandon their current hawkish stance and consequently postpone exiting from their stimulus programs.

Under these adverse scenarios, the Swiss franc will likely find renewed demand from safe-haven flows and reverse higher, harming the Swiss economy by weighing on the already feeble inflation rate (0.2% in July) and hurting exports (the Eurozone is Switzerland's biggest trading partner). The Swiss franc appreciated by around 21% against other currencies between 2007 and 2016. In comparison, its gains versus its Eurozone counterpart were more pronounced, rising by around 34%.

In the best scenario, the threat of global political uncertainty will recede and accelerating economic growth will generate inflationary pressures, giving way to monetary tightening. In this case, the tiny yet wealthy economy of Switzerland, wishing to see her European neighbours adopt a more euro-supportive monetary policy, would see the franc's strength wane, demand for its goods pick up and prices moving towards the central bank's goal. Currently, the swissie is looking bearish versus its major peers, while Swiss economic indicators are gradually recovering. GDP growth in the March 2017 quarter rose slightly to 0.3% quarter-on-quarter from 0.2%, which was upwardly revised from 0.1%. The unemployment rate edged down to 3% in July from 3.1%, whereas the KOF barometer, a closely watched measure which predicts the outlook for the next six months, jumped unexpectedly by 1 point to 106.8 in July. Taking the above into account, SNB board members in their last meeting projected the economy will continue expanding moderately in the second quarter. Nevertheless, they lowered their inflation forecasts for the next two years and pledged to continue intervening in the foreign exchange markets, as global political risks around the world have not yet faded, with Brexit talks and the dark cloud around the Trump White House remaining in the background and more elections coming up in Europe in 2018 (Italy).

Bank of England Review – More Dovish But Still Too Optimistic on Growth

6-2 vote count was interpreted dovishly

- As expected, the Bank of England maintained the Bank Rate at 0.25% and kept the targets for the government bond purchases and corporate bond purchases at GBP435bn and GBP10bn, respectively. In line with our call (but against the view of some houses), the vote count for the Bank Rate was 6-2 against 5-3 last time, as Kristin Forbes, a known hawk voting for a hike, has left the committee and it was too early for Andy Haldane to jump camp already despite a more hawkish tone in his latest speech.

- We still view the core of the Monetary Policy Committee (including governor Mark Carney) as being tilted to the dovish side.That said, since the unemployment rate has declined to NAIRU and inflation is above target, it may not take much for BoE to become more hawkish. Higher wage growth (and thus higher underlying inflation) is one trigger.

- We still expect the BoE to remain on hold until the Brexit negotiations are concluded in Spring 2019. The main reasons are that we think the BoE is still too optimistic on both wage growth and GDP growth and political uncertainty remains high due to Brexit.

- As expected, the BoE announced that it is ending the so-called Term Funding Scheme (TFS) in February 2018, as the BoE has been more worried about credit growth recently.

We lift our EUR/GBP targets to 0.91 in 1-3M

- EUR/GBP rose sharply and broke above 0.90 on the announcement as expected given the dovish twist from the BoE. UK yields traded some 4-5bp higher across the 2-10Y segment of curve, while the very front end of the UK money market curve was little changed. The market now implicitly indicates around 35% probability (8.5bp priced) of a November rate hike compared to 9.5bp priced prior to the BoE announcement.

- Over the coming 1-3 months, we expect EUR/GBP to test higher levels on the back of a strong EUR and BoE repricing. A 5bp decline in 2Y UK yields due to a further postponement of market expectations for the first BoE rate hike, will (everything else being equal) push EUR/GBP 0.1-0.25% higher, according to our models. We lift our 1M and 3M EUR/GBP targets to 0.91 (previously 0.88) expecting the cross trade within a narrow range of 0.90-0.92.

- Over 3-12M, we continue to see some stabilisation in GBP, expecting EUR/GBP to drift back below 0.90 on the back of potential for some clarification regarding Brexit negotiations and valuations.However, as relative growth and relative monetary policy is expected to remain EUR/GBP supportive in the medium term, we see only modest downside potential in the year ahead. We target 0.90 in 6M (previously 0.88) and 0.88 in 12M.

- Given the high political uncertainty due to the British government's weak parliamentary majority, we expect EUR/GBP to remain volatile and we generally recommend investors and corporates hedging GBP assets/income to maintain a high hedge ratio.

35% probability of a BoE hike this year, according to market pricing

BoE still too optimistic on growth

BoE expects growth to pick-up again next year

- The Bank of England has lowered its GDP forecast both because it overestimated growth in H1 17 and because it has become more pessimistic in the short term. However, the BoE still expects growth to pick up next year, as business investments pick up and consumption recovers due to higher wage growth.

- We still think the Bank of England is too optimistic on growth, as we do not think wage growth will pick up as fast as the BoE projects and think business investment growth will remain subdued.

- We expect GDP growth to continue around 0.3% q/q in coming years, slightly below trend growth of 0.4%.

- As we are more pessimistic on growth, we still expect the BoE to remain on hold until the Brexit negotiations are concluded in Spring 2019.

Inflation projection unchanged

- As expected, the CPI inflation forecast was broadly unchanged. CPI inflation is expected to stay above 2% in coming years, as it takes time for the weaker GBP and higher import prices to pass-through to consumer prices and because the Bank of England expects wage growth to pick up.

- We think the BoE is still too optimistic on wage growth and hence underlying inflation, which is one of the reasons why we do not think the BoE will hike soon.

- That said, higher wage growth remains one of the triggers for a more hawkish BoE.

Unemployment rate to stabilise around current NAIRU

- The Bank of England projects that the unemployment rate will stabilise around 4.5% (which is also the BoE's NAIRU estimate). The combination of higher inflation and lower unemployment was one of the reasons why the BoE turned more hawkish in June/July.

- Still, the tight labour market has not translated into higher wage growth yet and given that NAIRU is unobservable, the BoE may revise down its NAIRU estimate further at some point.

Macro charts: slowest UK growth since the European debt crisis

GDP growth in H1 17 the weakest since the European debt crisis

PMIs indicate GDP growth continued around current pace at the beginning of Q3

Weaker GBP => higher import prices => higher inflation => eroding purchasing power

Higher commodity prices have contributed to higher inflation

Inflation expectations have stabilised at a higher level

Copper Has Retraced Some of its Move Up in Recent Days, Silver Lower after a Marginal Break of Key...

- Copper has retraced some of its move up in recent days

- Silver lower after a marginal break of key resistance

COPPER Technicals

In our last note we commented on how the move up had some room to continue, as there was still some distance to be covered before the market reached the February 2017 highs.

This level of the February highs, around 2.82, has now been eclipsed and the move has continued to prices last seen in Q2 2015. The February 2017 highs could now be looked for as a potential support level in a move lower.

A second ascending trend-line shows how the most recent upswing has gathered pace, while the market has retraced some of its move up in recent days.

China data

Earlier this week the Caixin China manufacturing PMI, a private survey of China's factory activity, rose to four-month high of 51.1 in July, from 50.4 in June. However, the country's official manufacturing PMI fell to 51.4 in July from 51.7 in June.

In a release last Monday the IMF raised its 2017 growth forecast for China to 6.7%, a 0.1% increase from its April forecast. This comes after the previous week's Q2 GDP print, which beat expectations with growth at 6.9%.

Warehouse data

LME copper stocks recorded a net outflow for a third consecutive week, ending with inventory levels down 3% for the week ending 28 July from the close of the previous week.

SILVER Technicals

The market has traded lower after a marginal break above the key resistance of the June 29th high around 16.90. A move higher than this level will show a higher high after the market has put in a series of lower highs and lower lows in recent months and could potentially indicate a change in the trend.

In a move down, support might be found around the June 21 low near 16.34, while below that the 8 May comes in at around 16.05

Silver Coin Sales

American Eagle 1oz silver coin sales in July rose to 2,270,000 ounces from 986,000 ounces in June and up from 1,370,000 ounces sold in July 2016, according to data released by the US mint. This data suggests that investment demand in the form of physical bullion coins has recovered from the low levels seen in June 2017 and is also higher than during the same period in 2016.

Lower Forecast on the British GDP Growth Hit the Pound

The EUR/USD rolled back after it renewed the 2.5-year maximums and currently is consolidating in anticipation of tomorrow's release of labor market data in the US. Better figures on non-farm payrolls and the unemployment rate tomorrow may become a trigger for a massive selloff due to profit taking. Today support for the common currency came from retail sales in the Eurozone that in June expanded by 0.5% against the expected zero change. Traders ignored the flash manufacturing PMI in the euro area that remained at 55.4 for June.

The GBP came under pressure today following the Bank of England's decision to keep the interest rate unchanged at 0.25%. Leading up to the event, investors were going long on the pound as they anticipated a similar vote of confidence for a rate hike of 5-3 vote. However, Bank of England members voted 6-2 to keep the rate at its current level. Disappointed investors received more dovish news from the BOE as it reduced its forecasted growth for the UK for this year by 0.2% to 1.7%. The central bank noted that Brexit is weighing in on the economy as consumers are feeling the pinch of a lower pound.

The AUD/USD is consolidating after a sharp fall caused by the weak Australian trade balance data according to which the surplus in June was only 0.86 billion compared to the expected 1.78 billion. The pair is getting support from positive growth in the commodities markets, but we do not rule out a correction in the near future. The focus for traders tomorrow will be the retail sales report in Australia and the RBA's monetary policy statement which will be released at 01:30 GMT.

EUR/USD

The euro price renewed positive dynamics after some consolidation during the day. Quotes previously tested the resistance at 1.1900 and in case of its overcoming the next objective will be the psychologically important level of 1.2000. On the other side, fixing below the lower limit of the current rising channel and the support at 1.1800 may lead to the trend change to negative with targets at 1.1700 and 1.1620.

GBP/USD

The GBP/USD price has shown a rapid descending movement as a result of which the quotes broke through the lower limit of the ascending channel and the important level of 1.3250. This fact may be the basis for a continued decline with potential targets at 1.3050 and 1.2950. The RSI on the 15-minute chart approached the oversold zone, indicating a possible rebound. The growth potential is likely to be limited by resistance at 1.3250.

AUD/USD

The aussie quotations are trying to restore some positions after they left the limits of the local rising channel. Fixing beyond its borders will be the basis for continued decline to 0.7875 after which the negative dynamics may continue to 0.7800 and 0.7740. There is strong resistance at 0.8000 and its overcoming is less likely today. Volatility is likely to rise tomorrow due to a number of important events in Australia and the US.

Gold Ticks Higher Ahead of Nonfarm Payrolls

Gold continues to have an uneventful week and has posted small gains in the Thursday session. In North American trade, spot gold is trading at $1269.20, up 0.20% on the day. On the release front, unemployment claims edged lower to 240 thousand in July, beating the estimate of 242 thousand. ISM Non-Manufacturing slowed down to 53.9, compared to the estimate of 57.4 points. This reading was well below the forecast of 56.9 points. On Friday, the US releases wage growth and non-farm payrolls, so we could see some movement in gold prices.

The US economy is in good shape, underscored by a strong Advance GDP of 2.5% in the second quarter. This strong reading came after weak growth in the first quarter, which clocked in at just 1.4%. Still, investors are skeptical about a third interest rate hike in 2017, with current odds of a December hike at just 42%. Investor appetite for risk has waned and this has been good news for gold, which touched 6-week highs earlier this week. The pessimism on the part of markets is chiefly due to inflation, which has remained stubbornly low despite a strong labor market. In June, Fed Chair Janet Yellen said that factors causing weak inflation were "transient", but there are no signs that inflation will pick up anytime soon.

With the Federal Reserve unlikely to raise rates before December, investor attention has shifted to the Fed's balance sheet, which stands at $4.2 trillion. Fed policymakers have broadly hinted at reducing purchases of bonds and securities starting in September, but San Francisco Fed President John Williams was more forthcoming about the Fed's plans, likely aimed at giving notice to the markets. In a speech on Wednesday, Williams said that the economy had "fully recovered" from the 2008 financial crisis and called on the Fed to start trimming the balance sheet "this fall". Williams added that the process would be gradual and would take four years to reduce the balance sheet to a "reasonable size". On Wednesday, two other FOMC members also came out in support of starting to taper the balance sheet – St. Louis Fed President James Bullard and Cleveland Fed President Loretta Mester.

USDJPY Retests 110.00 Support after Downbeat US PMI Data

The dollar fell back below 110.00 handle against Japanese yen after US ISM Non-Manufacturing PMI dropped to 53.9 in July, well below forecast at 57.0 and June's release at 57.4.

On the other side, US Factory orders jumped to 3.0% in June, posting the biggest gain in eight months, but positive impact on upbeat results was diminished by expectations for modest pace of growth in manufacturing sector, due to fading support from energy sector.

Fresh acceleration lower and retest of strong supports at 110.00 zone signaled an end of corrective phase which stalled under strong 111.00 resistance.

Close below 110.14 (Fibo 76.4% of 108.80/114.49 rally remains as minimum requirement for generating firmer bearish signal, with sustained break below 110.00/109.91 pivots to confirm bearish continuation.

Conversely, repeated failure at 110.00 support may keep the pair within near-term 110.00/111.00 range.

Res: 110.51; 110.82; 111.00; 111.34

Sup: 109.91; 109.62; 109.26; 109.00