Sample Category Title

GBP Rises Ahead Of BoE Meeting

Is the dollar sell-off over?

This is no news that the US dollar has had a tough year so far but the question is whether further USD weakness is sustainable. On a trade weighted basis, the greenback fell more than 8.5% since the beginning of the year. The sharp appreciation of the single currency is responsible for most of move as it rose more than 12.60% against the USD, followed by the Swedish krona and the Australian dollar, up 12.25% and 9.90% respectively.

Nevertheless, since the beginning of the week, it seems that downside pressures on the USD are fading away as market participants reassess the dollar outlook. Given the rapid pace and the scale of the greenback debasement, we think it is time to consider the possibility of a bounce back. Not because the US fundamentals have changed drastically recently - even though yesterday dovish comments from Mester and Williams do not support my point - but because the market has a strong bearish bias. It is true that the latest US economic data does not allow for excess optimism; however the situation abroad is not much brighter.

More specifically, there are some interest opportunities, especially in the commodity currency complex. Both the Aussie and the Kiwi have benefited from the flight to higher yielding currencies as investors discounted the Fed’s hawkish bias. In addition, recently released economic data suggests that both of those countries are suffering from temporary setbacks, meaning that a downward adjustment of their respective currency is more than likely.

Window of opportunity for the Bank of England

Early this afternoon, the BoE will announce its key rate that should remain unchanged at 0.25%. Markets estimate that rates should only increase by early 2018.

For the time being, the British Central Bank is largely enjoying a weak pound in the wake of the Brexit vote. The economic collapse predicted after the referendum has not materialised and fundamental data are correct. Inflation is at 2.6%, growth at 1.7% (annualized) and unemployment rate keeps on declining, now at 4.5%.

The pound is getting stronger against the greenback but is weakening against the single currency. Indeed, Trump was unable to deliver what he promised and the Fed fears to increase rates. On the ECB side, markets estimate that the monetary policy divergence between the US and the Eurozone should now narrow down and that European policymakers should increase rates in the late part of this year. Current pounds levels are still providing the BoE with a window of opportunity to raise rates and drive growth.

In addition, the BoE is still targeting £435 billion in its asset purchase program and it may soon be the time to reduce the flow of liquidity the BoE injects in the market. By now, the amount injected has been of £375 billion – around 25% of the annual UK GDP -. Current economic development may definitely be a great moment for the British institution to act towards a monetary policy normalization.

Dollar Softness Drives DOW To 22K | BOE May Lower Growth Forecast

The Dow index touched the level of 22K thanks to the dollar weakness

BOE under constant pressure to change its monetary policy

The softness in the dollar and rally in the US stock market is something which cannot be overlooked. Traders do know that the key reason for the dollar weakness is largely due to the fact that there may be no more rate hikes for this reason. However, the question which puzzles many is why is the dollar weak when the Fed has already increased the interest rate so many times this year? The answer is simply because the market expectations were utterly out of whack. It was anticipated that the Fed would be hawkish with respect to their monetary policy despite the fact that it was clearly communicated that the interest rate hikes would be gradual.

A non-voting member of the Federal Reserve, St Louis Fed Chief James Bullard's comment further ruined the confidence for the bulls when he said he opposed any further rate hikes for this year as that would hinder the Fed's inflation target of 2 percent. If he is the only one with that mind frame or if he has other pals who think the same, would matter a lot for the dollar index.

A meagre jobs number tomorrow could put the final nail in the coffin for any rate hike for this year. Therefore, the importance of this economic reading cannot be undermined. The wage growth would also provide another signal if the job conditions have improved or not.

While the decline in the dollar has pushed the Dow Jones index to reach another record high of 22K, the strength in the euro is creating major headwinds for the Dax index. The index is feeling the heat, and the CAC 40 has also given away all its gain since Macron's victory.

Back in the UK, it has been a very long time since the Bank of England has increased its interest rate. The last surprise from the BOE was in 2016 when it lowered its interest to ward off Brexit woes. With Brexit looming, it is highly likely that the BOE will let the economy run hot rather than risking all their hard work by increasing the interest rate. The pound was trading near 1.33 before the BOE cut the interest rate and surprised the market which pushed the Sterling dollar price to 1.19. The selloff in the Sterling increased the pressure on the consumer income and their spending.

In today's decision, there is enough rift among policy members who would like to reverse the bank's decision which it made last year. But what the members cannot ignore is that the UK's economy is slowing down and the construction numbers released yesterday were miserable and the services data has also displayed a much softer side.

Later today, we have the services PMI number due and an improvement is expected. What can support the case for a hawkish outcome today is an improvement in the wages and strength in the Sterling. So it would be important how the bank would manage the expectations, especially its growth forecast which is lowered by the IMF to 1.7%. We expect the bank to lower its growth forecast as well, and if it does that, the chances for a rate hike are pushed further away. If the growth forecast is changed then the inflation forecast would also have an equal importance in the bank's view.

Technical Outlook: Cable Higher After UK PMI Data, BOE Super Thursday In Focus

Cable jumped after better than expected UK Service PMI (53.8 in July vs 53.6 f/c and 53.4 in June) and broke above yesterday's fresh high at 1.3250.

Bulls are looking for extension towards 1.3300 (round-figure resistance) and 1.3330 (Fibo 161.8% projection of bull-leg from 1.2588.

BoE's super Thursday is in focus, with the central bank expected to keep unchanged but focus is on votes for rate hike. Expectations are for 6-2 vote which would signal interest rates may stay on hold for some, while surprise 5-3 vote (seen in June) would turn BoE's outlook more hawkish and further boost sterling.

Key barrier at 1.3473 (weekly cloud top) could be tested on stronger acceleration higher.

On the downside, higher base at 1.3190 marks initial support, followed by rising Tenkan-sen / former high at 1.3125) violation of which would generate negative signal.

Res: 1.3268, 1.3300, 1.3330, 1.3346

Sup: 1.3210, 1.3190, 1.3125, 1.3100

Bitcoin Sideways Price Action

Bitcoin's volatility has declined despite the fork. Strong resistance can be found at 3000 (12/06/2017 high) and hourly support lies at 2403 (26/07/2017 low). Further retracement are expected. For the time being, the cryptocurrency keeps on trading between 2700 and 2800

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will consolidate above $1500. Long-term support is given at $1464 (04/05/2017 low).

Crude Oil Consolidating Below 50

Crude oil is consolidating lower on profit taking. Hourly support is given at 45.40 (24/07/2017 low). Strong resistance can be found at 50.28 (29/05/2017). Expected to show further consolidation before another leg higher.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

Silver Bullish Pressures Are Fading

Silver's bullish pressures are fading after the bounce from hourly support given at 15.18 (10/07/2017 low). Hourly resistance is given at 16.94 (02/08/2017 high). The commodity is set to further consolidate.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

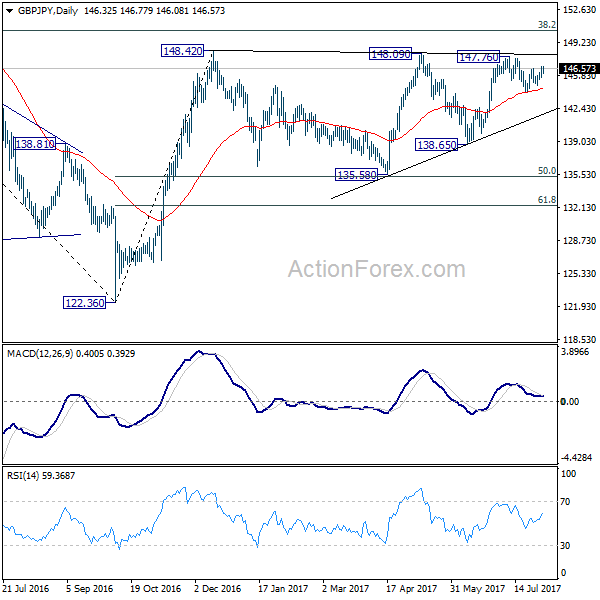

GBP/JPY Daily Outlook

Daily Pivots: (S1) 145.71; (P) 146.23; (R1) 146.94; More

GBP/JPY's recovery from 144.01 extends today but it's still bounded in range of 144.01/147.76. Intraday bias remains neutral for the moment. On the upside, break of 147.76/148.42 key resistance zone will resume larger rebound from 122.36. On the downside, break of 144.01 will extend the sideway pattern from 148.20 with another fall back to 135.58/65 support zone.

In the bigger picture, rise from medium term bottom at 122.36 is expected to continue to 38.2% retracement of 196.85 to 122.36 at 150.43. Decisive break there will carry long term bullish implications and pave the way to 61.8% retracement at 167.78. In case the sideway pattern from 148.42 extends, we'd be looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside.

Gold Consolidating

Gold is consolidating lower. Strong support is given at 1204 10/07/2017 high). Hourly resistance is given at 1274 (01/08/2017 high). Expected to show continued another leg higher.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low)

EUR/CHF Growing Until 1.15

EUR/CHF's buying pressures are very important and is trading below 1.15. Hourly support is located at a distance at 1.0984 (13/07/2017 low). Road is wide-open for further strengthening.

In the longer term, the technical structure has reversed. Resistance at 1.1200 (04/02/2015 high) has been broken. Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Edging Higher

EUR/GBP is trading around its highest levels of the year. The pair is consolidating. Hourly support is given at a distance at 0.8742 (16/06/2017 low). Downside risks are nonetheless important.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.