Sample Category Title

BoE’s Breeden: Pace of rate cut uncertain, gradual easing expected

BoE Deputy Governor Sarah Breeden today reinforced expectations for gradual easing of monetary policy, citing the abating effects of past economic shocks.

"I expect to continue to remove restrictiveness gradually over time," she added.

However, she cautioned against prescriptive timelines, remarking that it is "difficult to know" how quickly rates should fall.

Fed’s Harker: To maintain easing bias but pause briefly to assess impact

Philadelphia Fed President Patrick Harker reaffirmed his view today that Fed remains on a “downward policy rate path,” but emphasized flexibility based on future data.

“Looking at everything before me now, I am not about to walk off this path or turn around,” he stated at an event.

However, Harker suggested that the current stage of the policy cycle calls for some patience. “I think it’s appropriate for us to take a bit of a pause right now and see how things shake out,” he said, hinting at a temporary hold in rate adjustments to assess the economic impact of past cuts.

While advocating for a short pause, Harker added that Fed likely won’t remain in this holding pattern for long.

Fed’s Collins advocates gradual and patient approach on rate cuts

Boston Fed President Susan Collins noted in a speech today that the economy is overall in a "good place" and inflation steadily retreating from its 2022 peak. She added that current monetary policy is already closer to a neutral stance, allowing Fed to proceed with a "gradual and patient approach" as it evaluates further steps.

Collins acknowledged the significant progress in lowering inflation, describing it as moving "gradually, if unevenly," toward Fed’s 2% target. Importantly, this progress has been achieved alongside a "healthy overall" labor market that has shown signs of rebalancing from previously overheated conditions.

Reflecting on Fed’s decision to cut rates last month, Collins her support as a “close call,” as the move provided "some additional insurance" to support the labor market while maintaining a restrictive stance necessary to restore price stability.

Sunset Market Commentary

Markets

The spotlights remain squarely focused on the UK. Gilts yields gapped another 12 bps higher across the curve at the open this morning before calm returned somewhat. While net daily changes are close to zero today, the sharp uptick over the previous days and increased media attention did force the UK government to respond to urgent questions in parliament today. Treasury’s number two, Darren Jones, said the bond market is functioning in an orderly way and stressed that “There should be no doubt of the government’s commitment to economic stability and sound public finances. This is why meeting the fiscal rules is non-negotiable.” The material yield increase is eroding the limited fiscal headroom Chancellor Reeves has to comply with her self-imposed rule to fund day-to-day public spending with tax receipts by 2029-30. People familiar already told Bloomberg that if updated OBR forecasts end March would indeed show fiscal headroom has been absorbed by risen debt costs, Reeves would resort to spending cuts instead of higher taxes or even worse: change the rules of the game once again as she did back in October. Sterling is headed for back-to-back losses with EUR/GBP briefly topping the 0.84 big figure. The pair is currently trading around 0.838. Cable slipped to the lowest level since November 2023 to hit an intraday low around 1.224 but then paring losses to 1.23.

Moves in other core areas remain very limited. German rates barely budge and US yields ease a few basis points. Yesterday’s successful 30-yr auction underscored solid demand, especially at such attractive yields. That offered some respite for bonds on a day that had little to offer otherwise. The eco calendar is empty and US markets have either a shortened (bond markets) or no trading session at all (stocks) on this national day of mourning for ex-president Carter. USD changes are confined to tight ranges. JPY outperforms in one of the “bigger” moves today.

News & Views

UK CFOs in December assumed a slight rise in inflations expectations, the Bank of England Decision Maker Panel survey revealed. Year ahead own price inflation was expected to be 3.8% up from 3.7% in November. 3.8% was also the reported level of realized annual output price inflation in the three months to December of last year. A similar trend was seen in CFO’s CPI inflation expectations. Perceived CPI was 2.5% in the three months to December, down 0.1% from 2.6% but the one year ahead expectations rose from 2.7% to 2.8% in the three months to December. The corresponding measure for three-year ahead CPI inflation expectations was 2.7% from 2.6% in November. Reported annual wage growth eased 0.1% to 5.4%. Expected year-ahead wage growth remained unchanged at 4.0%. Asked about their reaction to the increase in employer national insurance contributions in the Autumn Budget, on average over the November and December surveys, 61% of firms expect to lower profit margins, 54% expect to raise prices, 53% expect lower employment and 39% expect to pay lower wages than they otherwise would have done.

Eco data in Hungary published today showed a mixed picture. Industrial production in November declined 1.9% M/M (SA) resulting in a 2.9% contraction compared to the same month last year. The statistical office reported falling production volumes in November 2024 in the great majority of the manufacturing subsections, with growth seen only in three subsections including the manufacture of coke and refined petroleum products. In the first 11 months of the year production was 3.9% lower than in the same period last year. Retail sales showed a slightly better picture rising 0.6% M/M and 4.1% Y/Y. YTD November sales growth was reported at 2.9%. The finance Ministry today also indicated that the 2024 budget shortfall probably came out at 4.8%, missing the deficit target of 4.5%. Despite the 2024 overshoot, the government still intends to reduce the budget deficit to 3.7% this year. This budget target however is based on an assumption of 3.4% 2025 GDP growth and 3.2% Inflation, which might be challenging to realize. After being under pressure due to global market sentiment, the forint regains modest ground trading near EUR/HUF 415 compared to reaching weakest levels since end 2022 (416.6 area) earlier this week.

Aussie Lower as Retail Sales Misses Estimate

The Australian dollar has edged lower on Thursday. In the North American session, AUD/USD is trading at 0.6198, down 0.28% on the day.

Australian retail sales point to cautious consumers

Australian retail sales rose 0.8% m/m in November 2024, higher than the downwardly revised 0.5% gain in October but shy of the market estimate of 1%. This was the strongest pace since January but there was some disappointment that pre-Christmas and Black Friday discounts didn’t result in stronger sales. Despite retailer incentives, consumers remained cautious, as high inflation and elevated interest rates have squeezed households and dampened consumer spending.

The Australian economy is struggling and today’s weaker-than-expected retail sales report along with the drop in underlying inflation in December is bolstering the case for a February rate cut. The Reserve Bank of Australia has highlighted household spending and inflation as key factors in its rate decisions and the central bank hasn’t budged from a cash rate of 4.35% for over a year. The RBA is sounding less hawkish but hasn’t hinted at the timeline for a rate cut, saying rate decisions will be data-dependent. The RBA hold its first meeting of the year on Feb. 18 and the money markets have priced in a rate cut at over 70%.

Fed minutes: Concern about Trump

The minutes of the Federal Reserve’s December meeting indicated that members were concerned about the upside risks of inflation due to President-elect Trump’s policies. Members stated that inflation could rise to “the likely effects of potential changes in trade and immigration policy”. Trump has pledged to slap tariffs on China and other US trading partners and has threatened the mass deportation of illegal immigrants.

The minutes also indicated that the Fed plans to “go slow” with further rate cuts in 2025, after starting the easing cycle last September with an oversized 50-basis point cut. The Fed’s December rate projection calls for only two rate cuts in 2025, down from four in the September forecast.

AUD/USD Technical

- AUD/USD tested support at 0.6189 earlier. Below, there is support at 0.6161

- 0.6215 and 0.6243 are the next resistance lines

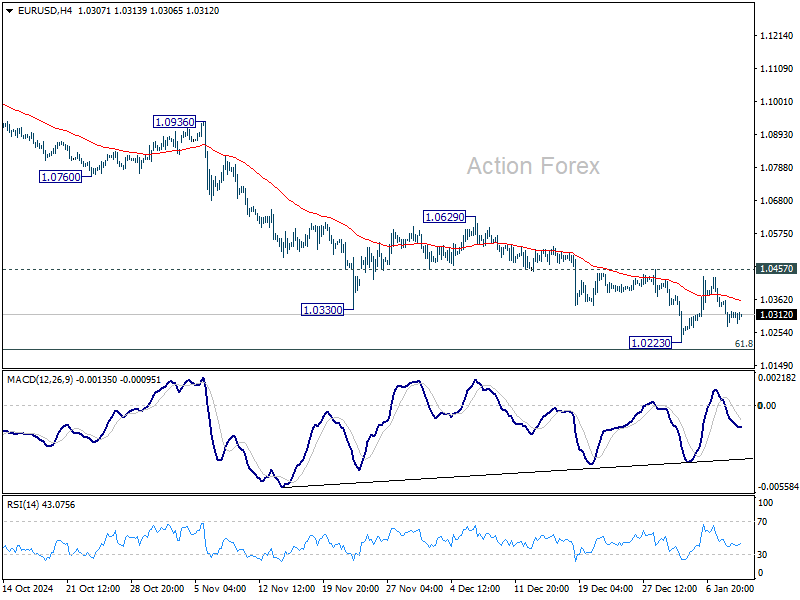

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0276; (P) 1.0317; (R1) 1.0361; More...

Sideway trading continues in EUR/USD and intraday bias remains neutral. Outlook also stays bearish with 1.0457 resistance intact. Firm break of 1.0223 will resume the fall from 1.1213. However, sustained break of 1.0457 will confirm short term bottoming, and turn bias to the upside for 55 D EMA (now at 1.0542).

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

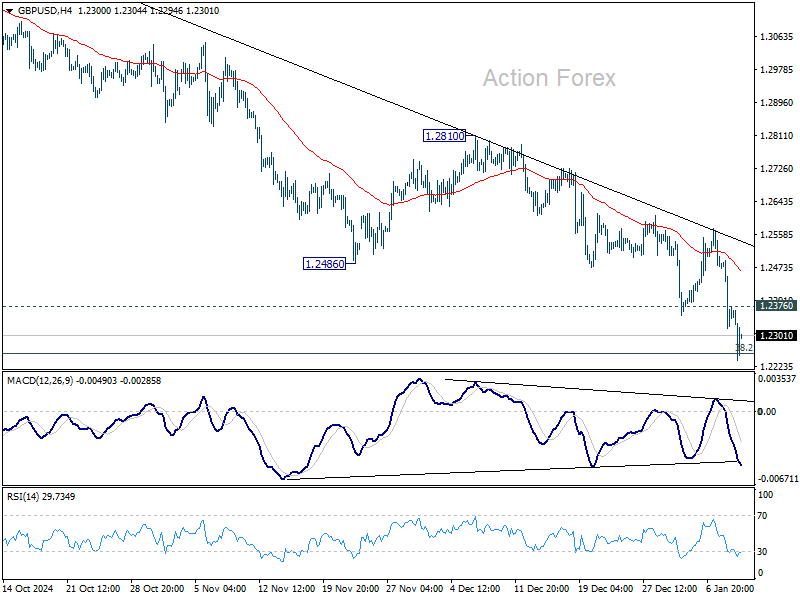

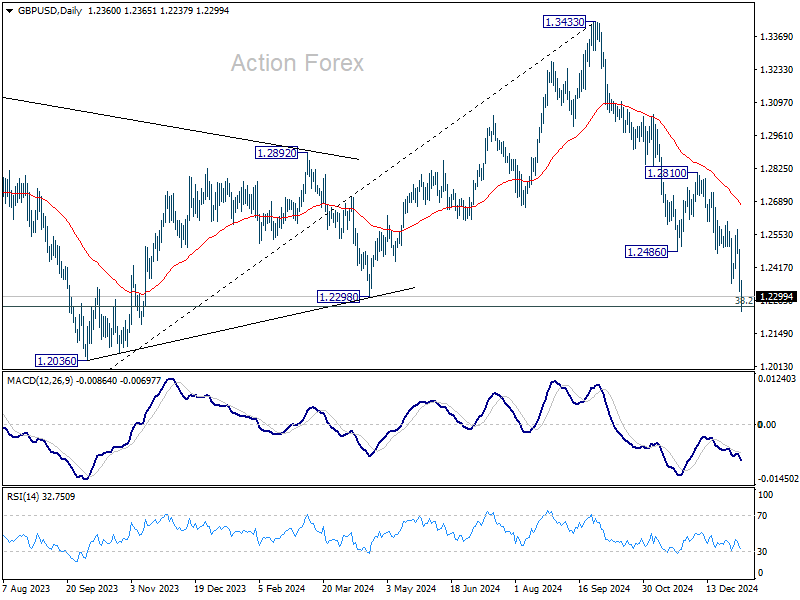

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2292; (P) 1.2393; (R1) 1.2465; More...

Intraday bias in GBP/USD remains on the downside for the moment. There is no clear sign of bottoming yet. Sustained trading below 1.2256 fibonacci level will carry larger bearish implications. On the upside, break of 1.2376 will turn intraday bias neutral first. Further break of 1.2486 support turned resistance should confirm short term bottoming.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Strong support is still expected from 38.2% retracement of 1.0351 to 1.3433 at 1.2256 to bring rebound to extend the corrective pattern. However, firm break of 1.2256 will argue that the trend has reversed and target 61.8% retracement at 1.1528.

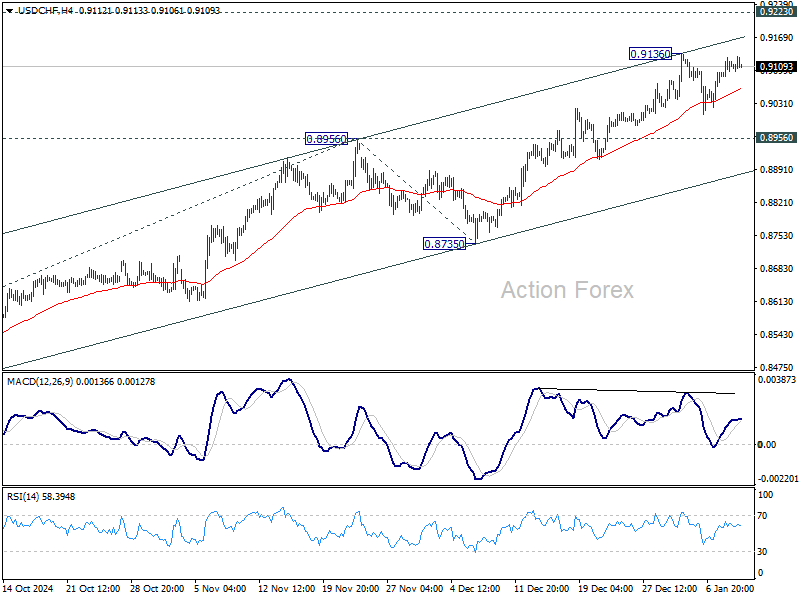

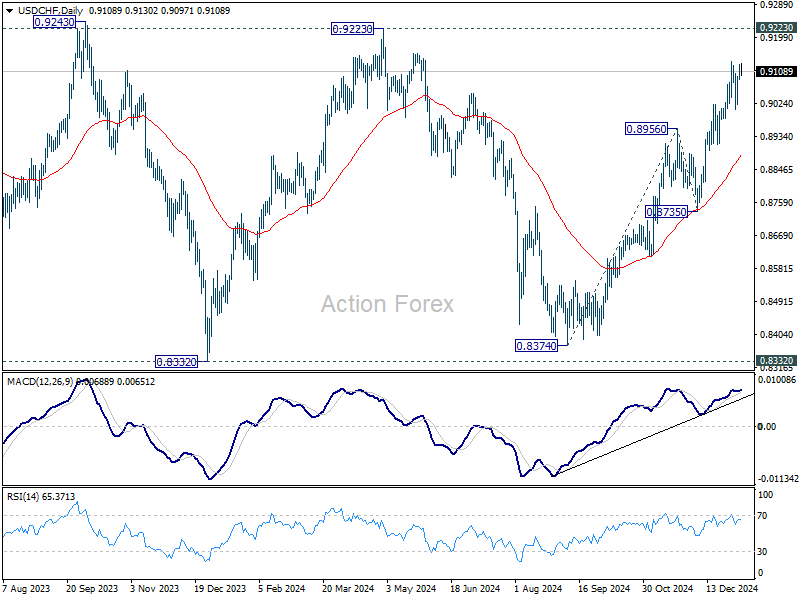

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9082; (P) 0.9106; (R1) 0.9134; More…

No change in USD/CHF's outlook as range trading continues. Intraday bias remains neutral for the moment, and more consolidations could be seen below 0.9136 resistance. Further rally is expected as long as 0.8956 resistance turned support holds. Above 0.9136 will resume the rally from 0.8374 to 0.9223 key resistance next. However, firm break of 0.8956 will turn bias back to the downside for 55 D EMA (now at 0.8888).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

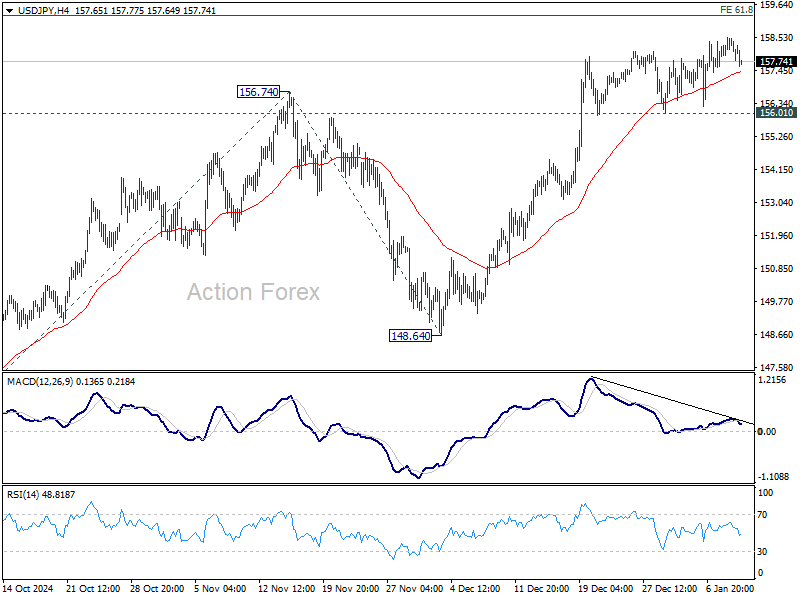

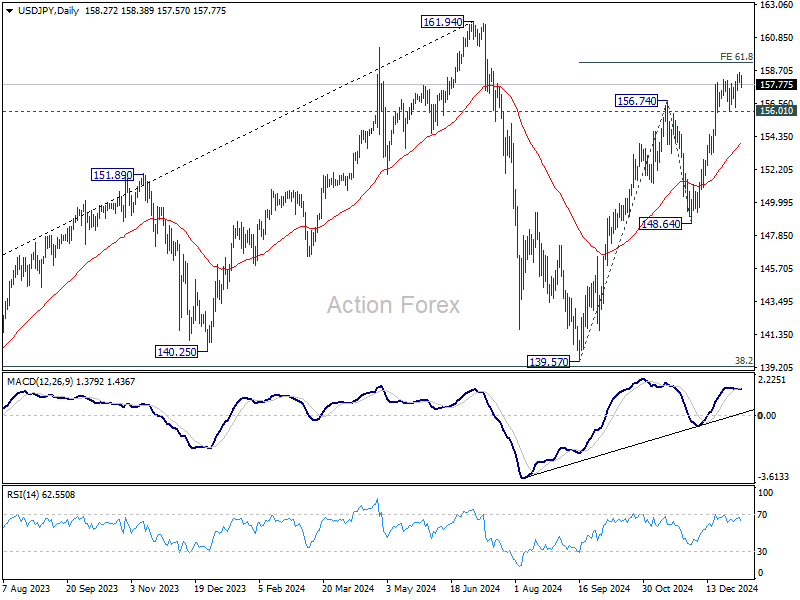

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.99; (P) 158.27; (R1) 158.64; More...

Intraday bias in USD/JPY is turned neutral first with current retreat. But further rally will remain in favor as long as 156.01 support holds. Break of 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 will extend the rally from 139.57 to retest 161.94 high. However, considering bearish divergence condition in 4H MACD, firm break of 156.01 support will indicate short term topping. Intraday bias will then be back on the downside for 55 D EMA (now at 153.98) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Yen Outperforms as Investors Turn Defensive, Sterling’s Downward Spiral Persists

While Sterling continues to be the market's primary focus as it faces heavy losses, Japanese Yen is quietly staging a modest, but broad-based recovery. However, Yen’s rally appears driven more by position adjustments ahead of tomorrow’s US non-farm payrolls report, as risk sentiment has across markets has turned more cautious. Meanwhile, there little support for Yen from increasingly dovish expectations surrounding BoJ policy.

The probability of a BoJ rate hike this month is waning. Although Japan's wage growth has shown strong improvement, economic uncertainty is casting doubt on immediate action. March is now starting to appear to be a more plausible timeline for further policy normalization.

Former BoJ Governor Haruhiko Kuroda noted in a recent research paper that while gradual rate hikes are anticipated, estimating the neutral interest rate remains challenging, making the path for monetary policy less clear.

Separately, ex-BoJ board member Makoto Sakurai expressed skepticism about a January hike, attributing it to the uncertainties surrounding global economic trends and the incoming US Trump administration. Sakurai suggested a 70% likelihood of a March hike, indicating that BoJ might prefer to wait for more clarity.

In the UK, government officials attempted to downplay concerns over the recent financial market volatility. Chief Secretary to the Treasury Darren Jones dismissed calls for emergency intervention, stating there was “no need” for such measures despite the sharp drop in Sterling and government bond prices. Jones attributed the movements to broader global financial dynamics and emphasized the government’s firm stance on borrowing only for investment purposes. However, these reassurances did little to lift the Pound, which remains near multi-month lows.

Overall for the day so far, Yen leads gains, followed by Dollar and Swiss Franc. Sterling is the day’s worst performer, followed by Aussie and Kiwi. These rankings reflect a tilt toward risk aversion. Euro and Canadian Dollar hover in the middle. Nevertheless, the global equities have yet to reflect significant negativity.

Technically, Copper's strong rally this week and break of 4.2831 resistance suggests that fall from 4.6904 has completed at 3.9667. Rise from there is now seen as the third leg of the corrective pattern from 3.9127 low, and could extend further towards 4.6904.

However, the fundamental backdrop for Copper raises questions about sustainability. China’s economic sluggishness, coupled with the looming threat of new US tariffs under the incoming administration, could temper the optimism in commodity markets. Yet, extended rally in Copper could help AUD/USD bounces off 0.6169 key support level.+

Eurozone retail sales marginally rise 0.1% mom in Nov, lag expectations

Eurozone retail sales edged up by 0.1% mom in November, falling short of expectations for 0.3% mom increase. Within the retail sectors, volume of sales rose slightly for food, drinks, and tobacco by 0.1%, while non-food product sales, excluding automotive fuel, contracted by -0.6%. Meanwhile, sales of automotive fuel increased by 0.8%, providing a modest lift to the overall figure.

At the EU level, retail sales grew by 0.2% mom. Among member states, Cyprus posted the strongest retail performance with a 2.3% increase, followed by Bulgaria at 1.3%, and Denmark and Latvia, both recording a 1.1% rise. Conversely, Belgium faced the sharpest contraction at -2.4%, with Germany and Spain both reporting a -0.6% decline. Poland and Finland also recorded slight decreases of -0.2%.

BoJ regional report highlights broadening price hikes

BoJ, in its latest Regional Economic Report, upgraded its economic outlook for two of Japan’s nine regions—Tohoku and Hokuriku—citing signs of moderate recovery.

The assessment for the remaining seven regions was left unchanged, with all areas described as either “picking up” or “recovering moderately.”

The report highlighted an increasingly widespread trend of price hikes by firms aiming to accommodate rising wages. While some companies, particularly larger ones, are already deliberating the scale of wage increases, smaller firms remain cautious. Concerns about the impact of higher costs on profit margins have slowed their willingness to commit to pay raises.

Japan's nominal wage gains hit 3% in Nov, but inflation erodes real earnings

Japan’s real wages fell by -0.3% yoy in November, marking the fourth consecutive monthly decline as wage growth failed to outpace inflation again.

While nominal wages rose by a robust 3.0% yoy—beating expectations of 2.7% yoy and extending a 35-month streak of growth—consumer prices grew at an even faster pace of 3.4% yoy during the same period, up from 2.6% yoy in October.

A notable highlight in the data was the sharp rise in special cash earnings, including bonuses, which surged by 7.9% yoy. Excluding bonuses and nonscheduled payments, average wages increased by 2.7% yoy, the fastest rate in 32 years, suggesting some underlying improvement in base wages.

Australia's retail sales growth misses expectations at 0.8% mom in Nov

Australia's retail sales increased by 0.8% mom in November, falling short of market expectations for 1.1% mom rise. Despite the miss, all retail industries recorded growth during the month, reflecting the ongoing impact of Black Friday.

This marks the third consecutive month of retail sales growth, following gains of 0.5% mom October and 0.4% mom in September. The steady trend highlights a degree of resilience in consumer spending, though the pace remains moderate.

Robert Ewing, head of business statistics at the Australian Bureau of Statistics, noted “Black Friday sales events proved once again to be a big hit”. He also pointed out that the sales promotions now extend beyond the traditional weekend, influencing spending patterns across the entire month of November.

China's inflation stalls at 0.1% in Dec, factory prices remain deflationary

China’s inflation decelerated again in December, with the CPI rising only 0.1% yoy, matching expectations and marking the slowest pace since April.

This brings full-year inflation for 2024 to 0.2%, far below the official target of around 3%, extending a 13-year streak of missing the annual inflation goal.

Core inflation, which strips out volatile food and energy prices, offered a slight reprieve, ticking up from 0.3% yoy to 0.4% yoy, the highest in five months.

PPI data showed a marginal improvement, with factory-gate prices contracting by -2.3% yoy compared to -2.5% yoy in November, slightly better than market expectations of -2.4% yoy. However, PPI has now stayed in deflationary territory for an extended 27 months.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.99; (P) 158.27; (R1) 158.64; More...

Intraday bias in USD/JPY is turned neutral first with current retreat. But further rally will remain in favor as long as 156.01 support holds. Break of 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 will extend the rally from 139.57 to retest 161.94 high. However, considering bearish divergence condition in 4H MACD, firm break of 156.01 support will indicate short term topping. Intraday bias will then be back on the downside for 55 D EMA (now at 153.98) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.