Sample Category Title

(RBA) Statement by Philip Lowe, Governor: Monetary Policy Decision

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

Conditions in the global economy are continuing to improve. Labour markets have tightened further and above-trend growth is expected in a number of advanced economies, although uncertainties remain. Growth in the Chinese economy has picked up a little and is being supported by increased spending on infrastructure and property construction, with the high level of debt continuing to present a medium-term risk. Commodity prices have generally risen recently, although Australia's terms of trade are still expected to decline over the period ahead.

Wage growth remains subdued in most countries, as does core inflation. Headline inflation rates have declined recently, largely reflecting the earlier decline in oil prices. In the United States, the Federal Reserve expects to increase interest rates further and there is no longer an expectation of additional monetary easing in other major economies. Financial markets have been functioning effectively and volatility remains low.

The Bank's forecasts for the Australian economy are largely unchanged. Over the next couple of years, the central forecast is for the economy to grow at an annual rate of around 3 per cent. The transition to lower levels of mining investment following the mining investment boom is almost complete, with some large LNG projects now close to completion. Business conditions have improved and capacity utilisation has increased. Some pick-up in non-mining business investment is expected. The current high level of residential construction is forecast to be maintained for some time, before gradually easing. One source of uncertainty for the domestic economy is the outlook for consumption. Retail sales have picked up recently, but slow growth in real wages and high levels of household debt are likely to constrain growth in spending.

Employment growth has been stronger over recent months, and has increased in all states. The various forward-looking indicators point to continued growth in employment over the period ahead. The unemployment rate is expected to decline a little over the next couple of years. Against this, however, wage growth remains low and this is likely to continue for a while yet.

The recent inflation data were broadly as the Bank expected. Both CPI inflation and measures of underlying inflation are running at a little under 2 per cent. Inflation is expected to pick up gradually as the economy strengthens. Higher prices for electricity and tobacco are expected to boost CPI inflation. A factor working in the other direction is increased competition from new entrants in the retail industry.

The Australian dollar has appreciated recently, partly reflecting a lower US dollar. The higher exchange rate is expected to contribute to subdued price pressures in the economy. It is also weighing on the outlook for output and employment. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

Conditions in the housing market vary considerably around the country. Housing prices have been rising briskly in some markets, although there are some signs that these conditions are starting to ease. In some other markets, prices are declining. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. Rent increases remain low in most cities. Investors in residential property are facing higher interest rates. There has also been some tightening of credit conditions following recent supervisory measures to address the risks associated with high and rising levels of household indebtedness. Growth in housing debt has been outpacing the slow growth in household incomes.

The low level of interest rates is continuing to support the Australian economy. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

Gold Looks To Trade Higher

The Yellow metal increased significantly in the last days and aims the 1282 level in the upcoming days. Should climb further as the USDX is under selling pressure and could slip lower to reach the 92.49 long term static support. Moves in range, but maintains a bullish perspective, is targeting the 23.6% retracement level and the $1295 per ounce.

EUR/JPY In The Buyer’s Territory

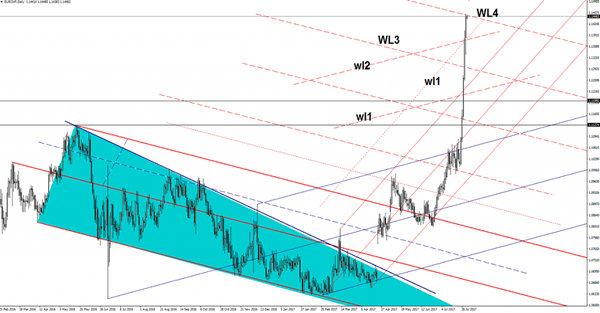

Price increased in the last two days and looks determined to reach the 130.76 previous high, it could climb much higher as long as is trading above the median line (ml) of the ascending pitchfork and above the upper median line (UML). Has retested the mentioned levels and now should climb higher, a further increase will be confirmed if will close above the previous high. The next upside target will be at the 150% retracement level

EUR/USD Jumped Above Another Upside Target

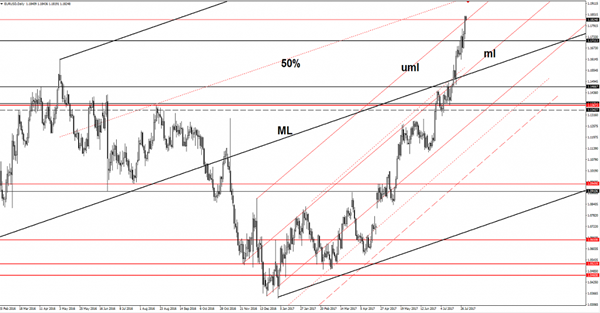

Price rallied aggressively in the yesterday's session and has managed to climb above another upside target. The breakout needs confirmation because this could be a false breakout if the dollar index will find strong support and will bounce back.

EUR/USD is trading in the red right now as the USD is trying to recover after the yesterday's massive sell-off. The greenback dropped further on the mixed United States data, has taken a hit from the Chicago PMI, which has decreased more than expected.

The minor decrease could be only temporary if the Euro-zone data will come in better later, the economic calendar is filled with high impact data. Price will be driven by the fundamental factors again, so remains to see the direction.

Price is testing the broken upper median line (uml) of the minor ascending pitchfork, will increase further if will manage to stabilize above this dynamic resistance. Only a false breakout above the upper median line (uml) will signal an exhaustion and a potential minor decrease.

Has jumped much above the 1.1712 long term static resistance, personally I'm still expecting to see a retest of this broken obstacle. We may have a buying opportunity if the rate will consolidate above this level.

The next upside target will be at the 50% Fibonacci line (ascending dotted line) of the major ascending pitchfork, it will reach this level if the United States data will disappoint again in the afternoon. You should be careful today because we may have a high volatility caused by the US reports.

The greenback needs a strong bullish spark to be able to shine again, it will turn to the upside if the US data will impress in the US session.

Elliott Wave View: DAX More Downside

Short term DAX Elliott Wave view suggests the decline from 5/15 high is unfolding as a double three Elliott wave structure. Down from 5/15 peak, Primary wave ((W)) ended at 12303 as a Flat and Primary wave ((X)) bounce ended at 12672. Primary wave ((Y)) is currently in progress and unfolding as a triple three Elliott wave structure. Down from 12672 peak, Intermediate wave (W) ended at 12373.5, Intermediate wave (X) ended at 12567, Intermediate wave (Y) ended at 12180.5 and Intermediate second wave (X) ended at 12339.48. Near term, while bounces stay below 12339.48, expect the Index to resume lower towards 11878.65 – 12030.11 area to end cycle from 5/15 high. Afterwards, from that area, expect the Index to at least bounce in 3 waves to correct cycle from 5/15 high.

DAX 1 Hour Elliott Wave Chart

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

We typically search for lower-timeframe confirmation between the M15 and H1 timeframes, since most of our higher-timeframe areas begin with the H4. Stops are usually placed 1-3 pips beyond confirming structures.

EUR/USD

In recent trading, the single currency climbed to a high of 1.1845. The 1.18 handle was, as you can see, taken out with relative ease, allowing daily price to gravitate higher into the walls of supply coming in at 1.1870-1.1786. While this daily supply zone is considered strong, we are a tad anxious at the moment. Weekly price recently crossed above resistance at 1.1759, which could, if the bulls remain in a dominant position, further encourage buying up to a weekly resistance planted at 1.2044.

Our suggestions: For those who have shorted this market, with stops conservatively placed above the current daily supply zone, there's still a chance the bears may make an appearance, despite the strong weekly push above weekly resistance. We decided to pass here and focus our efforts more on the GBP/USD, as you'll see below.

Data points to consider: US ISM manufacturing PMI at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

GBP/USD

Of late, we can see that the GBP/USD extended higher, reaching fresh highs of 1.3223 in the process. As a result of this, weekly price is now seen trading beyond the walls of supply at 1.3120-1.2957. However, technically speaking, it is far too early in the week to tell if this move north suggests further upside to the Quasimodo resistance planted at 1.3371.

Down on the daily picture, yesterday's move brought the unit into contact with supply drawn from 1.3278-1.3179, which as we mentioned in Monday's analysis, is overflowing with confluence. We have a trendline resistance taken from the high 1.3477, a channel resistance drawn from the high 1.2903 and two converging AB=CD (green/orange arrows) 127.2 Fib extensions at 1.3222/1.3223 (taken from the lows 1.2811/1.2365). Also, for you RSI fans, there is daily divergence in play, as well.

Moving across to the H4 timeframe, price recently tested an AB=CD bearish pattern (black arrows) that completes a few pips above the 1.32 handle at 1.3207 (the 127.2% Fib ext.). This – coupled with the daily structures mentioned above – forms incredibly attractive confluence.

Our suggestions: In light of the above, our team is now short from 1.3209, with conservative stops planted at 1.3280 (two pips above the top edge of daily supply). Ultimately, we're now looking for H4 price to cross back below the 1.32 handle, and touch gloves with the mid-level number 1.3150. It will be here that we'll consider reducing risk to breakeven.

Data points to consider: UK manufacturing data at 9.30am. US ISM manufacturing PMI at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.3209 ([live] stop loss: 1.3280).

AUD/USD:

Since Thursday, the commodity currency has been seen consolidating between the 0.80 handle and a H4 support at 0.7963 (converges with a H4 trendline support taken from the high 0.7987, a nearby H4 mid-level support at 0.7950 and also a H4 61.8% Fib support at 0.7950 drawn from the low 0.7877). As can be seen from the H4 window, the bears are beginning to make an appearance around 0.80 which could signal a downside move to the 0.7963 neighborhood.

On the weekly timeframe, the pair came within touching distance of a weekly resistance pegged at 0.8075 last week. Should this encourage sellers into the market, we could see price trade as low as the weekly support area marked at 0.7849-0.7752. In conjunction with the weekly timeframe, the daily Quasimodo resistance at 0.8030 managed to cap upside on Thursday, which could lead to a move being seen down to daily demand located nearby at 0.7874-0.7922. A break below this area, nonetheless, would almost immediately bring one into close contact with the top edge of the said weekly support area, which, as you can see, also holds a daily broken Quasimodo line at 0.7819 within.

Our suggestions: Ultimately, we do believe the Aussie is heading lower and will eventually close below this current H4 range. Usually, this would signal a potential sell trade, but with top edge of the current daily demand sited at 0.7922, we will likely pass. Therefore, for now at least, our team has decided to remain on the sidelines.

Data points to consider: RBA Rate statement at 5.30am. US ISM manufacturing PMI at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

USD/JPY:

For those who read Monday's report, you may recall us underscoring the H4 demand area at 110.21-110.40 as a high-probability buy zone. As you can see, price did respond nicely to this area, but fell short ten pips of the overall take-profit target: June's opening level at 110.83. The demand itself, although appears to be under pressure at the moment, remains intact for the time being. For how long though is difficult to judge.

From the weekly timeframe, the market looks as though it could continue to press lower until we reach the small demand base seen at 108.13-108.95.Zooming in and looking at the daily picture shows us that price concluded Monday's segment closing beyond support at 110.76. In theory, this move could have potentially cleared the river south down to a Quasimodo support logged at 109.11, which happens to unite closely with a trendline support etched from the low 108.13.

Our suggestions: With the higher-timeframe picture suggesting that further selling could be on the cards, we would not advise buying this market right now. Selling is also challenging given that the 110 handle is lurking just below the current H4 demand base.

Data points to consider: US ISM manufacturing PMI at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

USD/CAD:

Kicking this morning's report off from the weekly timeframe, we can see that the pair is hovering beneath resistance at 1.2538 at the moment. Assuming that this level remains firm, we do not see a whole lot of support on this scale until the demand base registered at 1.2127-1.2309. Despite this, a closer look at price action reveals that daily price is currently supported by demand coming in at 1.2303-1.2423, which happens to be glued to the top edge of the weekly demand mentioned above.

Crossing over to the H4 chart, we see price toying with the 1.25 handle. The next upside target beyond this number is seen nearby at 1.2532 (resistance), followed closely by a mid-level resistance at 1.2550. Therefore, buying this market is likely going to be difficult, despite daily price coming from demand. Along the same vein, selling from weekly resistance at 1.2538 will also be just as difficult given the current daily demand in play.

Our suggestions: At the time of writing, we do not see much to hang our hat on. Therefore, we have decided to hold fire for the time being and remain on the sidelines.

Data points to consider: US ISM manufacturing PMI at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (Stop loss: N/A).

- Sells: Flat (Stop loss: N/A).

USD/CHF

On the whole, weekly, daily and H4 structure collectively implies that shorting this market is the way to go.

What's interesting from the weekly timeframe is that the Swissy recently interacted with a trendline resistance extended from the low 0.9257, which remains firm as we write. Turning over a page to the daily timeframe, price connected with supply logged at 0.9738-0.9691that happens to converge with a channel resistance extended from the high 0.9808 and a 38.2% Fib resistance at 0.9693 taken from the high 1.0099. And finally, across on the H4 timeframe, we can see that the candles are now trading below June's opening level at 0.9680. As we mentioned in Monday's report, a close below here would likely clear the path south down to the 0.96 handle, followed closely by July's opening level at 0.9580 and then daily support positioned at 0.9546.

Our suggestions: For us to pull the trigger here, however, we would like to see the H4 candles retest June's opening level at 0.9680 and form a full, or near-full-bodied candle. This would, in our humble opinion, be enough evidence to enter short, targeting 0.96 as an initial take-profit zone.

Data points to consider: US ISM manufacturing PMI at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 0.9680 region ([waiting for a full or near-full-bodied bearish candle to emerge is advised] stop loss: ideally beyond the candle wick).

DOW 30:

For five consecutive sessions, the US equity market has advanced north. This places the index at record highs and also within striking distance of a H4 channel resistance extended from the high 21493. However, selling at this angle, in our humble opinion, is a chancy move given the strength of the bulls and lack of higher-timeframe resistances.

Our suggestions: Personally, we have very little else to comment on this market at the moment, as there are unfortunately no supports seen nearby for a buy trade.

Data points to consider: US ISM manufacturing PMI at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

GOLD

As of current price, the H4 chart shows the unit spent yesterday clinging to the underside of resistance at 1269.8. As we highlighted in yesterday's report, the H4 supply at 1281.1-1275.4 seen above this line is interesting. Encased within the area is a H4 AB=CD (blue arrows) 161.8% Fib ext. at 1278.4 drawn from the low 1243.6, and a H4 78.6% Fib resistance (blue line) at 1276.5 taken from the high 1296.0. The question is, will this H4 supply be enough to halt further buying?

As can be seen from the weekly timeframe the gold market remained strongly bid last week, placing the metal within striking distance of an area comprised of two Fibonacci extensions 161.8/127.2% at 1312.2/1284.3 taken from the low 1188.1 (green zone). Already capping upside on two occasions, will we see history repeat itself from the green area this week? A closer look at price action on the daily timeframe shows price used support at 1258.9 to trade higher on Friday. Should the bulls remain in position, the next upside hurdle in the firing range will likely be the trendline resistance extended from the high 1337.3.

Our suggestions: So, taking into account that both the weekly and daily charts show room to extend north, we are going to refrain taking shorts from the said H4 supply. The feeling of going against higher-timeframe buyers from the H4 area just doesn't sit right with us.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

European Open Briefing: AUDUSD Is Well Bid Ahead Of The RBA Rate Decision

Global Markets:

- Asian stock markets: Nikkei up 0.20%, Shanghai Composite gained 0.65%, Hang Seng rose 0.55%, ASX 200 rallied 0.75%

- Commodities: Gold at $1269 (+0.20%), Silver at $16.83 (+0.30%), WTI Oil at $50.30 (+0.20%), Brent Oil at $52.80 (+0.15%)

- Rates: US 10 year yield at 2.30, UK 10 year at 1.23, German 10 year yield at 0.55

News & Data:

- China Caixin Manufacturing PMI Ju: 51.1 (Est 50.4, Prev 50.4)

- Japan Nikkei Manufacturing PMI Jul F: 52.1 (Prev 52.2)

- South Korea Nikkei Manufacturing PMI Jul: 49.1(Prev 50.1)

- Australia AIG Perf of MFG Index Jul: 56 (Prev 55)

- PBoC Fixes USDCNY Reference Rate At 6.7148 (Prev 6.7283)

Markets Update:

The US Dollar came under renewed pressure overnight as concerns about the political situation in Washington weighed on the currency. EURUSD broke above 1.18 and there is little resistance now until 1.20.

GBPUSD cleared resistance at 1.32, which suggests the rally could extend to 1.35 in the near-term. While the outlook for GBP is mixed, the broad USD weakness could keep the pair supported for a while.

USDJPY has bounced off 110 on the first test, but the support level looks very fragile. A break below is likely to trigger more momentum selling and eventually push the pair in the direction of 108 – the next major support level.

AUDUSD is well bid ahead of the RBA rate decision. The market is not expecting any changes, so the highlight will be the RBA statement. The tone in the recent minutes were slightly more hawkish, so the market has hopes that this will be confirmed in today's release.

Upcoming Events:

- 08:45 BST – Italian Manufacturing PMI

- 08:50 BST – French Manufacturing PMI

- 08:55 BST – German Manufacturing PMI

- 08:55 BST – German Unemployment Rate

- 09:00 BST – Euro Zone Manufacturing PMI

- 09:30 BST – UK Manufacturing PMI

- 10:00 BST – Euro Zone GDP

- 13:30 BST – US Personal Spending

- 15:00 BST – US Manufacturing PMI

Market Morning Briefing: Aussie Is Seeing Strength Ahead Of The RBA Meet Today

STOCKS

Dow (21891.12, +0.28%) is inching up every session to move up bit by bit. While the near term uptrend remains intact, there could be more room on the upside towards 22000-22100 levels in the medium term.

Dax (12118.25, -0.37%) is almost stable and continues to trade above the near term weekly support at 12060. A bounce from here is necessary to take it higher towards 12300-12400 in the medium term.

Shanghai (3283.67, +0.33%) has been moving up firmly since the last 3-months and has come up to test medium term resistance near 3300. While that holds, the index could come off towards 3250 or maybe consolidate for a few sessions to gather more momentum to resume the uptrend in the longer term. A corrective dip from 3300 is expected in the coming sessions.

Nikkei (19959.41, +0.17%) is almost stable and is likely to consolidate within 19700-20280 in the medium term. Only on a break on either side of the range would we get some more clarity on further direction.

Nifty (10077.10, +0.63%) could head towards 10100-10132 before again seeing a slight dip back to 10000 in the next 2-3 sessions. Near term likely to remain within 10200-9900 with the uptrend intact.

COMMODITIES

Gold (1272) is struggling to close above the 1273-75 regions and only a close above those levels may open up the higher targets of 1298 and 1307. Crucial supports are poised at 1258 and 1245 levels. We are not confident about the sustainability beyond 1270-75 regions due to short term overbought condition. In case the Support at 1245 breaks, there will be a further dip to 1230 and 1210 levels respectively.

Silver (16.84) stands comparatively strong due to the recent strength in copper prices. Immediate resistance poised at 17 levels. Only a close below 16.50 could open up lower levels of 16.20 and 15.90 levels respectively.

Copper (2.90) moved higher in line with our expectation. Midterm resistance comes at 3.12 regions from where we may see some correction due to profit taking. Gold-Copper ratio (437) is trading below of its long term trend line support, could be beneficial for overall growth of world economy.

Brent (52.81) is out of its midterm bearish channel as it is trading above 51.30 regions. Immediate resistance comes at 53 levels and a close above that could open up 56 as well. WTI (50.28) is also moved higher and a close above 51 could be the end of midterm bearish trend in WTI too. Both Brent and WTI are approaching towards near term overbought condition thus we might see profit taking at 53 and 51 levels respectively.

FOREX

Lack of stability and major shakeups in the White House are inviting fresh selloff in Dollar, which in turn pushes the majors up.

Dollar Index (92.88) is on its way towards 92.00 as expected after achieving our initial target of 93.00. The 5th consecutive negative monthly closing is its longest monthly losing streak since 2011 and its difficult to see any chance of short covering before 92.00 is met.

Euro (1.1827) has overshot our initial target of 1.18 and now rising towards our next target of 1.20 in line with our expectations. The highly overbought state hasn’t affected the currency yet but we follow the trend cautiously.

Dollar-Yen (110.13) has broken below the support of 110.30 and opened up the downside target/support of 109.50. Resistance comes at 110.50-80.

Pound (1.3215) has finally managed a break above the major resistance of 1.32 and now if it can sustain above the level, the downside risk will be much reduced. In that case, higher targets of 1.3330 and 1.3420 come into consideration.

Aussie (0.8032) is seeing strength ahead of the RBA meet today. The central is widely expected to hold rates but it remains to be seen what steps it consider to weaken the currency. Our targets of 0.8100-70 remain unchanged with immediate support coming at 0.7970.

Dollar Rupee (64.18) closed almost flat with a gain of only 3 paisa. The resistance of 64.25-30 may hold till the RBI meet conclusion coming on Wednesday with the downside open.

INTEREST RATES

The UK-US 10YR (-1.06%) has bounced back from near term support in line with a sharp surge in the Pound to 1.3215. While the Pound continues to move up further against the US Dollar, the yield spread could rise further in the near term towards -1.02% or even higher.

The UK 10-5Yr (0.64%) has broken above the immediate resistance and could move up towards 0.70% in the near term. the differential looks bullish for the near term.

The Us yields are almost stable and could remain so for the coming sessions. The 5Yr, 10YR and the 30YR are trading at 1.83%, 2.29% and 2.90% respectively.

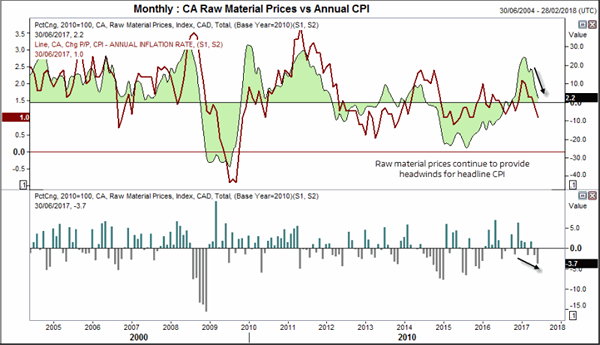

Soft Data Brings CAD’s Rally Into Question

Technically, some of the CAD crosses appear to be over-extended from their bullish run which leaves them vulnerable to data which undermines the BoC's tightening cycle. With raw materials and industrials yanking overnight, it may only take weak trade or employment on Friday to bring more of a correction.

Raw material prices softened further in July by contracting -3.7%, its fastest ate since Dec '15. This makes it the third contraction over four months and have dragged the annual rate to 2.2%, its lowest rate of expansion since October 2015.

Oil prices have played a large part here as the annual rate of material prices and WTI track very well. As there has been a rebound in oil prices, we expect the decline to provide a trough and perhaps even move higher in the next couple of months. Yet further out we cannot rule out an extension of softer prices as the rally with Oil has been largely due to short-covering over increased bullish interest, which suggests a limit to how high oil can rebound from here.

Industrial production also threw a curve ball into the mix by contracting by 1%, its heaviest decline since Dec '14. Annually it expanded by 3.3%, its lowest in 5 months yet we'll have to wait until next month to see if this is merely an outlier or the beginning of something more sinister.

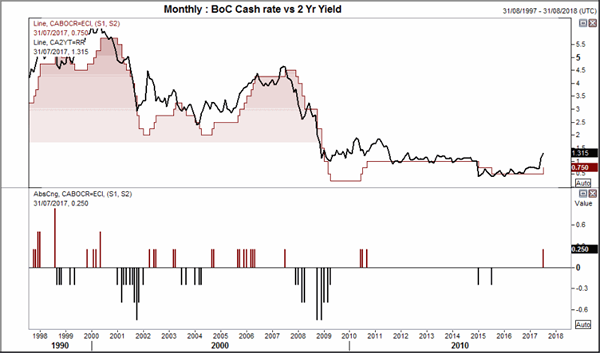

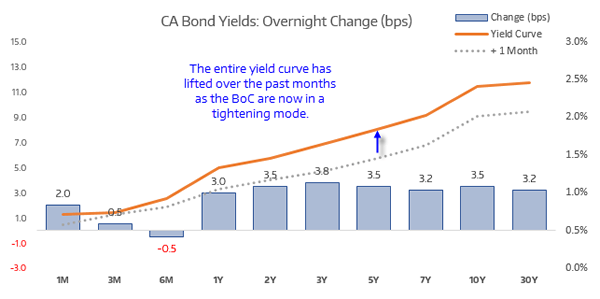

Data overnight throws another spanner in the works for traders. The Canadian economy has been making headway in recent months, at least by just enough to warrant a hike for the first time in 9 years. Bond yields have been moving higher in anticipation of a continued pickup in data, yet mixed signals from inflation reads may deter some the bullish bets. As data since their hawkish hike has been a little on the soft side and CAD crosses appear to be technically over-extended, we may be setting up for some counter-trend moves.

Bond markets suspect another hike or two may be on the way, judging from the acceleration of the 2yr yield. As inflation erodes the value of a bond, the fear of inflation (or a hike which is associated it) can send bond prices lower and yields higher. It is this added sensitivity to inflation which can make bond prices a leading indicator for policy changes and, whilst not perfect, can lead turning point between policy shifts. It is worth pointing out that they're not so great at predicting the level of central bank rates but it can help with the general direction. For now, markets remain convinced BoC are in tightening mode and we now need hard data to justify the rise in yields over the coming months, or bonds will regain their lure and send yields lower.

EURCAD rallied overnight and has tested the upper channel. This area also coincides with the monthly pivot and weekly R2 which makes it an idea zone to monitor for both bullish and bearish signals; a break of such a level makes a decent bullish case, whereas a rejection form here could entice bearish swing traders.

As price respected and accelerated away from the weekly pivot, we favour an eventual upside break. Only a firm rejection of the monthly pivot would deter us from that bias, as a mild retracement from here could also be expected before a bullish break.

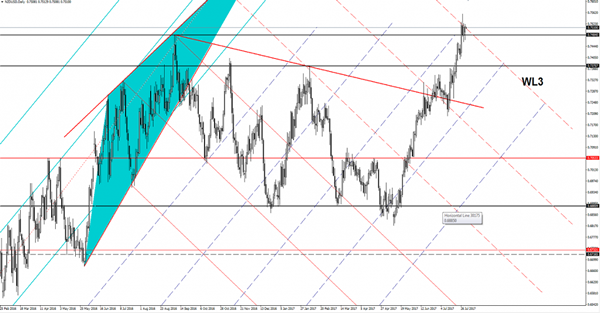

NZD/USD Breakout In Play

NZD/USD is trading in the green and tries to perforate the fourth warning line (WL4) of the major descending pitchfork. We may have a buying opportunity if will close above the WL4 and if will come to retest the 0.7484 support (resistance turned into support).