Sample Category Title

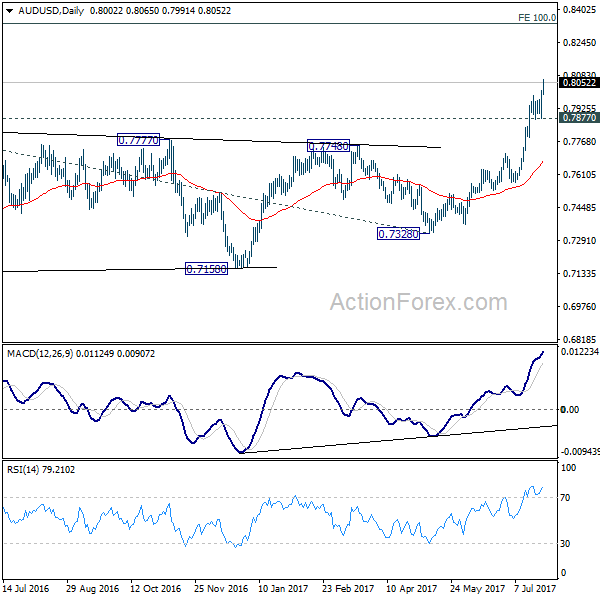

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7917; (P) 0.7965; (R1) 0.8053; More...

AUD/USD's rally resumed by taking out 0.7988 and reaches as high as 0.8065 so far. Intraday bias is back on the upside. Current rise from 0.7328 is now targeting next key projection level at 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335. On the downside, break of 0.7877 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, current development suggests that rebound from 0.6826 is developing into a medium term rise. There is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, further rise is now expected to 55 month EMA (now at 0.8100) or even further to 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now expected.

Dollar Selloff Resumed after FOMC, Commodity Currencies the Best Performers

Dollar's broad based selloff resumed overnight after Fed kept monetary policies unchanged. The move was seen as reaction to Fed's slight tweak in description of inflation. Also, Fed's indication that balance sheet normalization would start very soon suggest that it will push another rate hike, if any to December. While the greenback is weak, it's still slightly better than the Swiss Franc. The Franc dived yesterday in catch up to recent developments in the financial markets and there is no sign of halting yet. Commodity currencies are the best performer this week as markets are on full risk-on mode.

Fed to start balance sheet normalization "relatively soon"

Fed left its monetary policy unchanged, maintaining the federal funds rate target at 1-1.25%. The Fed made two tweak in the statement, though. First, it noted that balance sheet reduction would begin 'relatively soon', signaling that the official announcement would come in September. Second, policymakers revised lower the outlook on core inflation. US dollar plunged, with the weighted index falling to a 13-month low as the market interpreted the inflation assessment as dovish.

More on FOMC:

- FOMC Signaled To Begin Balance Sheet Normalization 'Relatively Soon', Downgraded Core Inflation Assessment

- Dollar Resumes The Unwind As Fed Fail To Impress

- FOMC Review: Smidgen Dovish But It Does Not Alter The Overall Picture

- FOMC: Steady As She Goes

- Little-Changed FOMC Statement Maintains Dovish Uncertainty, Weighs Further On Dollar

- Fed Stands Pat as Expected, Signals Coming Balance Sheet Normalization

- Fed Acknowledges the Inflation Miss, But Sticks to Balance Sheet Plans

DOW at record thanks to Boeing, not Fed

DOW surged 97.58 pts, or 0.45% to close at record high at 97.58 overnight. But it should be noted that the index has gapped up at 21690.38 at open already and barely moved after FOMC announcement. The surge was mainly driven by Boeing upgrading its forecast for the year after posting strong earnings. The 9.9% gain in Boeing has indeed added 144 pts to DOW. Overall, in spite of weak momentum, the index is still on course for 61.8% projection of 17883.56 to 21169.11 from 20379.55 at 22410.01.

RBA Lowe warned of prolonged weak wage growth

In Australia, RBA governor Philip Lowe warned that prolonged weakness in wage growth could hurt the economy. He said that "if workers are getting no real wage increase year after year after year that's insidious." And, he emphasized that high wage growth "would help get inflation back to target and I think people would feel a bit better as well, and the fact that many of us have lowered our expectations of future income growth means we're less inclined to spend."

Regarding monetary policy, Lowe noted that "the main effect of lower interest rates is that more people have jobs". And "that's why I'm very comfortable with the current setting of monetary policy, it's helped people get jobs." Regarding the exchange rate, Lowe said that "it would be better if the exchange rate were a bit lower than it currently is. It would help generate more jobs, push inflation a bit closer to our target -- so that's the solution to a competitiveness problem."

On the data front

Australia import price index dropped -0.1% qoq in Q2. German Gfk consumer sentiment and Eurozone M3 will be featured in European session. UK will also release CBI realized sales. US will release durable goods orders, trade balance and jobless claims.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7917; (P) 0.7965; (R1) 0.8053; More...

AUD/USD's rally resumed by taking out 0.7988 and reaches as high as 0.8065 so far. Intraday bias is back on the upside. Current rise from 0.7328 is now targeting next key projection level at 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335. On the downside, break of 0.7877 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, current development suggests that rebound from 0.6826 is developing into a medium term rise. There is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, further rise is now expected to 55 month EMA (now at 0.8100) or even further to 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now expected.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | Import Price Index Q/Q Q2 | -0.10% | 0.70% | 1.20% | |

| 6:00 | EUR | German GfK Consumer Confidence AUG | 10.6 | 10.6 | ||

| 8:00 | EUR | Eurozone M3 Y/Y Jun | 5.00% | 5.00% | ||

| 10:00 | GBP | CBI Realized Sales Jul | 10 | 12 | ||

| 12:30 | USD | Initial Jobless Claims (Jul 22) | 240k | 233k | ||

| 12:30 | USD | Durable Goods Orders Jun P | 3.50% | -0.80% | ||

| 12:30 | USD | Durables Ex Transportation Jun P | 0.40% | 0.30% | ||

| 12:30 | USD | Advance Goods Trade Balance Jun | -65.0B | -65.9B | ||

| 12:30 | USD | Wholesale Inventories Jun P | 0.30% | 0.40% | ||

| 14:30 | USD | Natural Gas Storage | 28B |

Market Morning Briefing: Further Strength In Euro To 1.1744

STOCKS

Dow (21711.01, +0.45%) rose above 21700 yesterday indicating resumption of the long term uptrend and has enough room on the upside towards 21800 for the coming sessions. Near term is likely to remain bullish.

Dax (1235.11, +0.33%) could test 12400-12450 in the coming sessions before seeing another down leg.

Shanghai (3221.92, -0.79%) came off sharply as expected and could fall further towards 3200 before again rising towards 3240-3260 levels.

Nikkei (20093.41, +0.22%) has been stable in the past 6-7 weeks and could continue to trade within 19705-20000 region for the next couple of weeks.

Nifty (10020.65, +0.56%) moved up yesterday to close above 10000. Immediate resistance is visible near 10050-10100 from where a sharp correction is possible in the medium term.

COMMODITIES

The support of 1245 held for Gold (1260) due to fresh weakness in Dollar index (93.22). Immediate trading range for Gold is 1258-1270. Gold is overbought in near term time frame and we are not confident about the sustainability beyond 1270 regions. Similarly Silver (16.69) is also trading within 16.69-17, well supported by the bullish momentum in Copper. Both Gold and Silver are out of their short term bearish channel but the supports of 1245 and 16.20 should hold to keep the bullish momentum intact.

Copper (2.86) looks on a firm footing while it is trading above 2.78 levels. Midterm resistance comes at 3.12 regions from where we may see some correction due to profit taking.

Both Brent (50.88) and WTI (48.66) moved upward as U.S weekly crude inventory data (actual -7.2M B) was highly supportive for the entire energy pack. This is the 5th consecutive week of shortage in weekly U.S crude inventory. We will remain bullish while Brent and WTI are trading above 47.70 and 45.50 on a weekly closing basis. Immediate trading range for Brent and WTI could be 48-51.50 and 46-49.70 respectively and a weekly close above51.50 and 49.70 levels might confirm the end of the midterm bearish trend too.

FOREX

Further strength in Euro to 1.1744, breaking above the earlier crucial resistance at 1.1712. This surge opens up targets of 1.18-20.

Dollar-Yen has come down again all the way to 110.98, giving back almost all the gains up to 112. Supports seen at 110.50 and deeper at 110.00.

The Euro-Yen (130.26) looks poised to climb further towards 132, possibly led by Euro. Dips likely to be bought.

Strong surge in Pound (1.3144) and Aussie (0.8044). f the Pound sustains above 1.31 today, look for a test of 1.32, beyond which 1.34 will come into the picture. Medium term Support at 1.29-28. The Aussie has no near term Resistance till 0.81 at least and might be able to rise beyond that as well given the surge in Copper.

Dollar-Rupee quotes 64.31/36 on NDF.

INTEREST RATES

The US yields have dipped slightly from long term resistance levels and could remain stable in the coming sessions before moving down sharply later on. Overall long term trend is likely to remain down.

The UK-US 10YR (-1.05%) can rise towards resistance near-0.98% in the near term. the surge in Pound could continue for a few more sessions. Near term looks bullish.

The German-US 10Yr (-1.72%) and the German-Us 2Yr (-2.03%) both have bounced slightly from immediate supports and could move up in the near term again boosted by the strength in Euro. The rise in Euro and the yield spreads may continue for the next few sessions.

Dollar Resumes The Unwind As Fed Fail To Impress

Despite the mention of balance sheet reduction beginning 'relatively soon' markets sent the Dollar to fresh lows as they continue to doubt fed's ability to raise once more this year.

Summary of the July meeting (read full statement)

- The labour market has continued to strengthen and that economic activity has been rising moderately

- Market-based measures of inflation compensation remain low

- Inflation on a 12-month basis is expected to remain somewhat below 2 percent in the near term

- but to stabilize around the Committee's 2 percent objective over the medium term.

- Near-term risks to the economic outlook appear roughly balanced

- The stance of monetary policy remains accommodative

- the federal funds rate is likely to remain

The Committee expects to begin implementing its balance sheet normalization program relatively soon

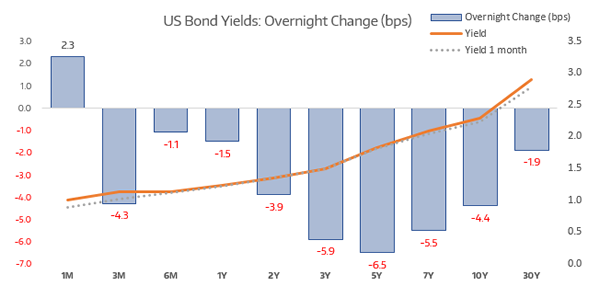

The US Dollar extended declines as the potential for a hike seemed diminished. We thought that was the case going into the meeting anyway as inflation has continued to soften and data overall has been soft. The biggest change to the statement was the point of normalising the balance sheet 'relatively soon' which puts the September meeting in full focus for the implementation to take place. Previously it was thought they would reveal plans for the tapering in September, yet they now speak of action. It is therefore possible we'll hear more details at the Jackson Hole symposium at the end of this month. It remains widely debated as to what effect this will have on markets, although we see it as a form of tightening. Therefor we may see yields move higher if bonds do sell-off although the Fed learned their lesson with the taper tantrum so lots of forward guidance is expected on this subject.

The dovish meeting saw money flow back into bonds which pressured yields from 3 months right through to 30 years decline. It was the centre of the curve which attracted the heaviest flow back into bonds as the 3, 5 and 7-year yields dropped by -5.9, -6.5 and -5.5 bps respectively. With policy remaining accommodative little hope of a raise or even balance sheet reduction soon, yield may continue to come under pressure as bonds remain supported. It is the threat of tightening which weakens bonds as the act is done to fend off inflation (which erodes the value of bonds). If there is no inflation, there is less need to hike and bond markets flourish. With inflation and inflation expectations all pointing lower, yields may indeed come under pressure and the stock market is more likely to continue its bullish trajectory.

The US Dollar Index printed a bearish outside day which provides a prominent swing high at 94.28. We are now firmly below the monthly S2 and the prior low to assume a resumption of the bearish trend. We only expect minor pullbacks from here so we'd consider fading into rallied below monthly S2. This only adds yet further support for EUR, AUD, NZD and the like which continue to rise against their central banks wishes. Unfortunately for the smaller, latter two, they have less sway in the direction of their currency if USD is in freefall.

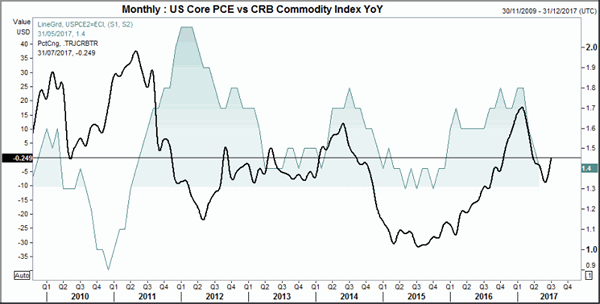

Next week the US release personal consumption expenditures. Whilst it looks at the consumption side of the economy, therefor a measure of consumer confidence and spending, it is the preferred inflationary measure of the Fed. It shares a relationship with commodity prices too, although the correlation between commodities YoY and inflation does vary and go out of syn. Yet since 2012 the correlation has been decent enough to call turning points, which is why we're highlighting the uplift of the CRB commodity index YoY. This does not necessarily mean we will see an uptick next week but it is possible we'll see one in the next couple of months or so if the gains on commodities are at least sustained or extended. This seems to be a viable outcome given the extended drop in the US Dollar.

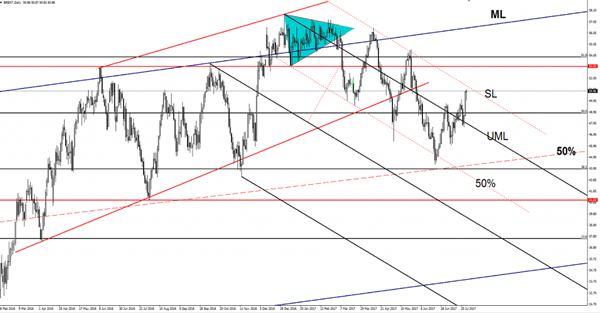

Brent Oil At New Highs

Price is strongly bullish and could take out the resistance from the sliding line (SL) in the upcoming days, a valid breakout from the descending channel will drive the rate towards the next upside target from $53.03 per barrel. Brent could take advantage of the weaker dollar to reach new highs in the upcoming period.

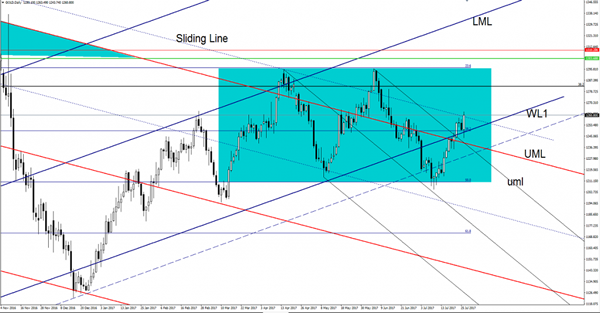

Gold Rallied As Expected

The Gold edges higher and resumes the upside movement, is trading right above the $1260 per ounce and most likely will target the 1295 level.

Has broken above the outside sliding line (descending dotted line) of the major descending pitchfork, we may have a buying opportunity if will close above this level. I’ve said in the previous report that the Gold is located in the buyer’s territory after the breakout from the descending pitchfork’s body and from the minor descending pitchfork’s body, has come only to retest the 38.2% retracement level and the warning line (WL1) before has jumped higher.

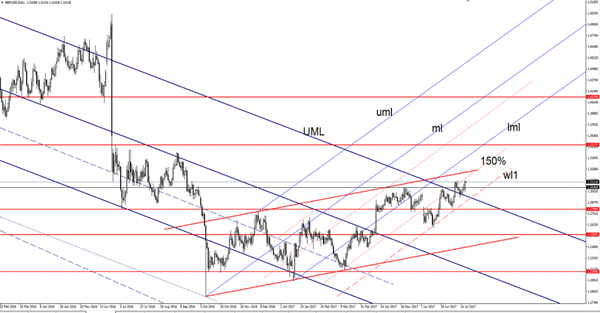

GBP/USD Further Increase Expected

Price has increased in the second part of the day and has managed to resume the minor upside momentum. The greenback was ruined by the FOMC and now could drop much deeper versus all its rivals.

GBP/USD moves within an ascending channel, maintains a bullish perspective in the upcoming period, even if we'll have a minor consolidation in the upcoming weeks.

As you already know, the Federal Reserve has maintained the monetary policy unchanged, the Federal Funds Rate remains steady at 1.25%, matching expectations, but unfortunately these decisions have demolished the USD.

USDX plunged after the FOMC Statement and now is located below the 93.50 psychological level, should drop much deeper after the retest of a strong dynamic resistance. The dollar index is very heavy right now and looks unstoppable, could approach the 92.49 major static support.

Price rallied in the last few hours and is very close to jump above the 1.3125 previous high, could touch also the first upside obstacle from the 150% Fibonacci line (ascending dotted line). Technically should increase further after the retest of the upper median line (UML) of the major descending pitchfork. I've said in the previous articles that the sentiment will change drastically if the rate will stabilize outside the major descending pitchfork.

I've also said that we'll have a buying opportunity if will come to retest also the warning line (wl1), this scenario is still possible, it was too risky to buy the retest of the UML has shown some exhaustion signs.

You can see that GBP/USD is trapped within an ascending channel, could still reach the upside line of this pattern if the USDX will slide further, the next major upside targets ar at the lower median line (lml) of the ascending pitchfork and at the 1.3527 level.

FOMC Signaled To Begin Balance Sheet Normalization ‘Relatively Soon’, Downgraded Core Inflation Assessment

The July FOMC meeting came in as widely anticipated. The Fed left its monetary policy unchanged, maintaining the federal funds rate target at 1-1.25%. The Fed made two tweak in the statement, though. First, it noted that balance sheet reduction would begin 'relatively soon', signaling that the official announcement would come in September. Second, policymakers revised lower the outlook on core inflation. US dollar plunged, with the weighted index falling to a 13-month low as the market interpreted the inflation assessment as dovish.

As indicated in the concluding paragraph of the accompanying statement, the Fed is maintaining, 'for the time being', the reinvestment of principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. It expects to begin implementing its balance sheet normalization program 'relatively soon', given that 'the economy evolves broadly as anticipated'.

Policymakers acknowledged that the overall inflation and the measure excluding food and energy prices (core inflation) have 'declined' and are 'running below 2%'. The removal of the word 'somewhat' signaled the weakness in inflation is more than the Fed had anticipated. They noted that 'market-based measures of inflation compensation remain low' while 'survey-based measures of longer-term inflation expectations are little changed, on balance'. Yet, the Fed retained that the long-term inflation would have 'a sustained return to 2%'.

For now, we believe the Fed would make an official announcement of the balance sheet reduction process in as soon as September. We continue to expect the Fed would deliver one more rate hike this year, likely in December, unless the economic growth and inflation prints decline dramatically.

FOMC Review: Smidgen Dovish But It Does Not Alter The Overall Picture

As expected, the Fed maintained the target rate at 1.00%-1.25%. As this was a small meeting without updated projections and a press conference, focus was solely on the statement. However, the statement was without any big changes as per usual.

One change in the statement was that it now says that the process of unwinding the balance sheet may start 'relatively soon' instead of 'this year', but in reality this was not new as it just reflects the words Fed Chair Yellen used during the press conference in June. We think this supports our call that the Fed will make an announcement on quantitative tightening at the next meeting in September.

Another change was that it now says that inflation runs below 2% instead of 'somewhat below', which was a smidgen dovish. It is difficult to say whether it is something we should pay a lot of attention to, as we know, based on Janet Yellen's recent testimony to US congress, that the Fed still has faith in the Phillips curve, i.e. the tighter labour market will push wage growth and thus underlying inflation higher eventually. Due to the Fed's strong belief in the Phillips curve and given we expect a further tightening of the labour market, we think the Fed will hike one more time this year in December. Consensus is for another hike this year, while markets price in a 40% probability.

However, in our view, the jobs report for June highlighted the Fed's dilemma and we still think risks are skewed towards the Fed pausing its hiking cycle due to low inflation, which may not be just 'transitory' given the low inflation expectations. In our view, the problem is that the tightness of the labour market is not the only factor determining wage growth, as second-round effects after many years with low inflation have hit wage growth. When employees expect inflation to remain low, they can live with low wage growth, as real wage growth may still be solid, making it less likely inflation will reach the target (see also Strategy: Central banks consider leaving the party, 30 June). In this regard, it is interesting that four FOMC members indicated that they do not expect the Fed to hike more this year in the June projections.

EUR/USD initially bounced back above 1.17 and yields on US government bonds fell 3-4bp across the curve after the minor dovish twist in the FOMC statement. Over the past month, EUR/USD has indeed witnessed a kind of perfect storm with ECB communication and the balance of political risks shifting in favour of the euro, and with today´s FOMC statement, relative monetary policy should also be less of a downside risk factor for EUR/USD in the near term. On 25 July, we revised our EUR/USD forecast higher and here we pencilled in even more upside to the cross longer term. In the near term, we target EUR/USD at 1.17 in 1-3M, reflecting that we expect the recent level shift higher in EUR/USD to persist, while momentum is expected to ease near term amid stretched technicals, short-term valuations and positioning (IMM). Longer term, we still expect EUR/USD to trade higher targeting 1.22 in 12 months driven by fundamentals and less Fed-ECB divergence. See FX Strategy: more upside for EUR/USD in store, 25 July, for more details.

FOMC: Steady As She Goes

- FOMC keeps target range policy rate unchanged at 1 to 1.25%year

- Risks to economic outlook roughly balanced; No change in assessment inflation

- FOMC confirms its desire to gradual tighten policy, if situation evolves as expected

- Tapering balance sheet to start 'relatively soon' (instead of this year)

- No noticeable other changes in statement and no dissenters

- US Treasuries rally, dollar is sold and equity stabilize

FOMC keeps policy unchanged

The FOMC statement met market expectations that its policy setting would remain unchanged. The Fed prefers to take decisions at meetings where new forecasts are available and a press conference is scheduled. This means March, June, September and December. Given thin markets, especially the July meeting isn't an appropriate time to surprise markets or implement new measures.

Balance sheet tapering to start soon

The July statement was almost identical with the June one (when rates were increased). The only change worth mentioning concerned the start of the tapering of its balance sheet. In June, the FOMC said it would do so in 2017 provided the economy evolved broadly as expected. Now, it stated: ' The Committee expects to begin implementing its balance sheet normalization program relatively soon, provided that the economy evolves broadly as anticipated. We think that the official announcement will be made at the September meeting and the implementation to start on October 1.

No particular concern about inflation

Following four months of slowing inflations, markets looked closely to eventual changes in the statement about the inflation outlook. Some time ago, Yellen said it was largely due to temporary factors. That assessment is very much open to debate and a few governors already expressed concerns about it and said they preferred to take a pause in the tightening cycle to see how inflation would evolve.

The changes in the statement on inflation were marginal though. In its description of recent developments (first paragraph), the statement mentioned that headline and core inflation had declined and are running below 2%. In June, the statement mentioned that they were running somewhat below 2%. On the outlook, there was no change: 'Inflation on a 12-month basis is expected to remain somewhat below 2 percent in the near term but to stabilize around the Committee's 2 percent objective over the medium term.' and ' The Committee is monitoring inflation developments closely'.

FOMC expects further gradual tightening

'The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate' but is watching inflation developments carefully. 'The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal.' 'The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate.'

Summarizing, we expect the Fed to start implementing its balance sheet tapering after the September meeting. That gives them the opportunity to keep rates unchanged in September and defer an eventual rate hike to the December meeting, if economic conditions remain good and especially if inflation doubts subside. A potential hurdle to start tapering might be the stand-off in Congress over raising the debt ceiling that may reach its zenith end September-half October.

Market reactions not so subdued

Despite the lack of much new info, the Treasury and FX markets reacted substantially in a dovish fashion. US Treasuries went up and erased Tuesday's sell-off losses, while the dollar was sold. The T Note future rose from about 125-21 to 126-02. The curve sifted lower by 3 (30-yr) to 7 bps (5-yr). The outperformance of the 5-yr suggests that the market considered the statement as relevant for the outlook of monetary policy. EUR/USD rose from 1.1640 to 1.1735, setting a new cycle high and threatening key resistance at 1.1736 (38% retracement). USD/JPY fell to 111.20 from 1.1190. Equities couldn't choose a distinct direction