Sample Category Title

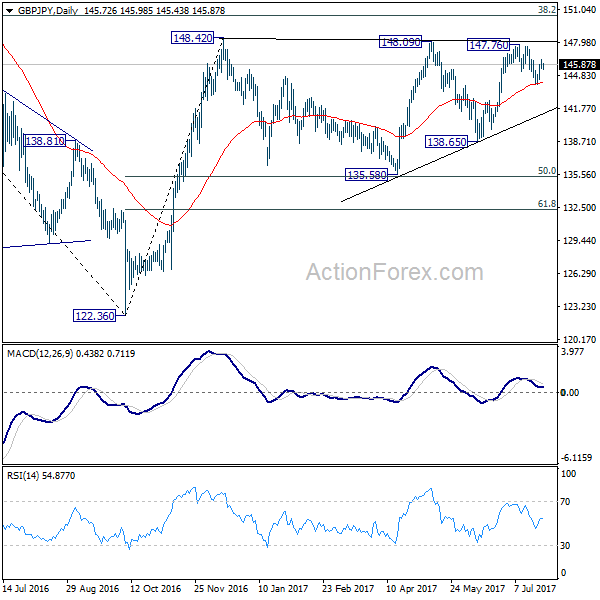

GBP/JPY Daily Outlook

Daily Pivots: (S1) 145.42; (P) 145.91; (R1) 146.35; More

The breach of 146.42 minor resistance argues that pull back from 147.76 has completed at 144.01, after being supported by 55 day EMA. Intraday bias is now mildly on the upside for 147.76/148.42 key resistance zone. Break there will resume larger rebound from 122.36. ON the downside, break of 144.01 will extend the sideway pattern from 148.20 with another fall back to 135.58/65 support zone.

In the bigger picture, rise from medium term bottom at 122.36 is expected to continue to 38.2% retracement of 196.85 to 122.36 at 150.43. Decisive break there will carry long term bullish implications and pave the way to 61.8% retracement at 167.78. In case the sideway pattern from 148.42 extends, we'd be looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside.

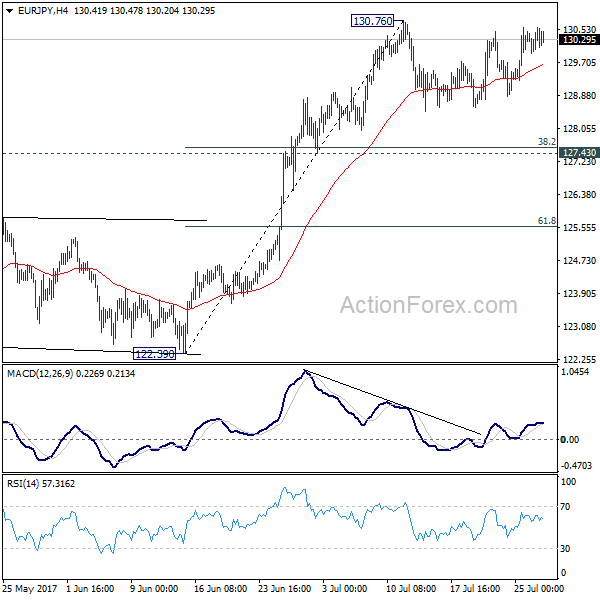

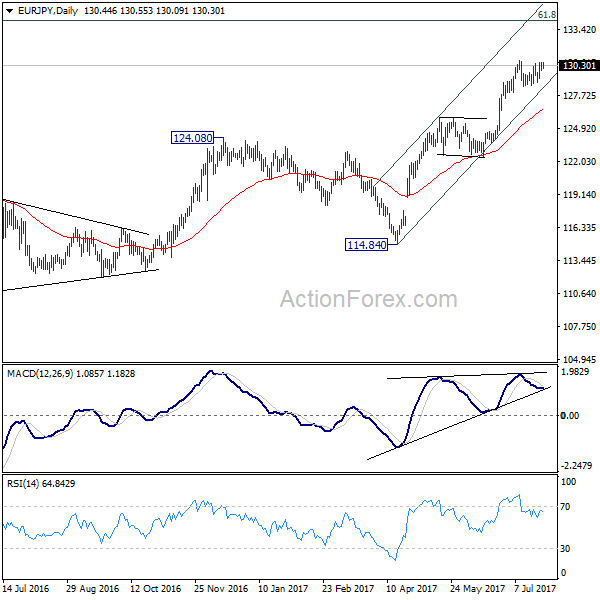

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.51; (P) 130.04; (R1) 130.84; More...

Intraday bias in EUR/JPY remains neutral as consolidation from 130.76 is still in progress. In case of another fall, downside should be contained by 127.43 cluster support (38.2% retracement of 122.39 to 130.76 at 127.56) and bring rebound. Above 130.76 will extend the larger rally to next key fibonacci level at 134.20.

In the bigger picture, the down trend from 149.76 (2014 high) is completed at 109.03 (2016 low). Current rally from 109.03 should be at the same degree as the fall from 149.76 to 109.03. Further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. Medium term outlook will remain bullish as long as 124.08 resistance turned support holds.

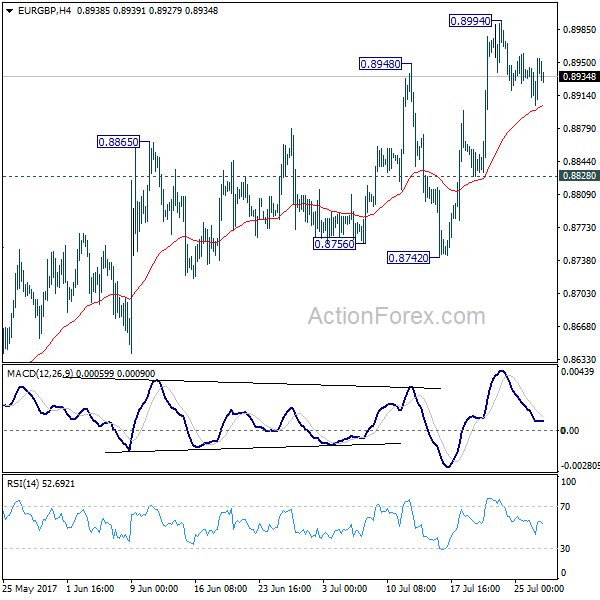

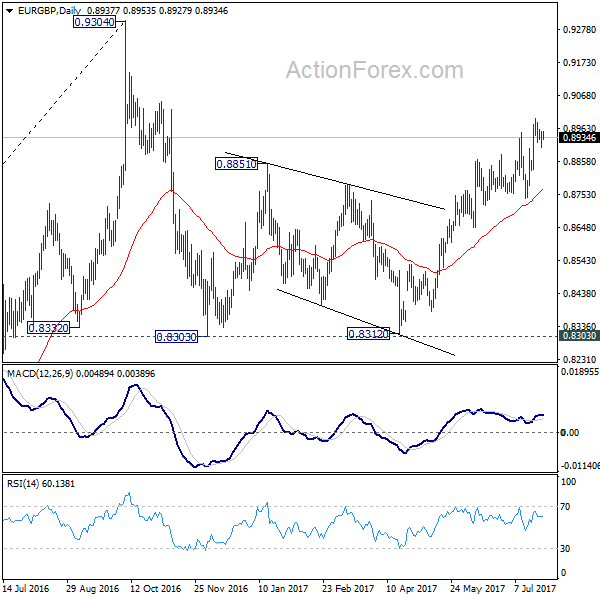

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8913; (P) 0.8934; (R1) 0.8963; More

EUR/GBP is staying in consolidation below 0.8994 temporary top and intraday bias remains neutral first. Downside of retreat should be contained by 0.8828 minor support to bring another rally. Break of 0.8994 will extend the whole rise from 0.8312 towards 0.9304 high. here is no clear sign of up trend resumption yet. Hence, we'll be cautious on strong resistance from 0.9304 to limit upside and bring another fall.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

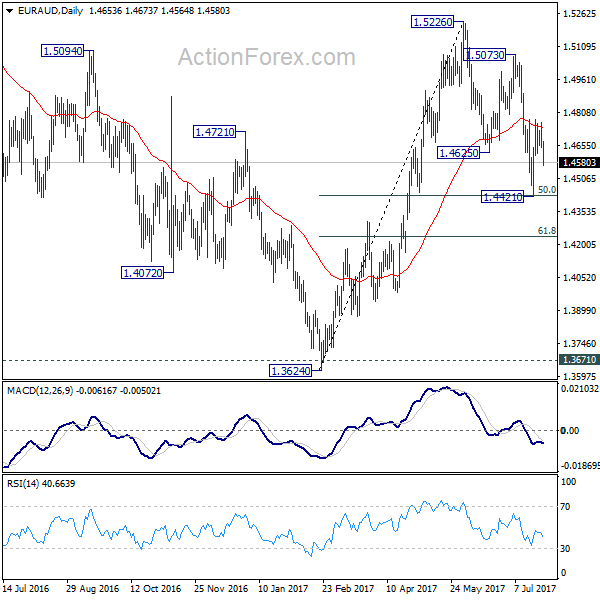

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4612; (P) 1.4688; (R1) 1.4730; More...

Intraday bias in EUR/AUD remains neutral as it's bounded in range of 1.4421/4777. At this point, we're still favoring the case that correction from 1.5226 could have completed with three waves down to 1.4421 already. Therefore, another rally is expected in the cross. Break of 1.4777 will turn bias to the upside for 1.5073 resistance first. Break there will indicate resumption of whole rise from 1.3624. However, break of 1.4221 will invalidate our view and extend the decline from 1.5226 to 61.8% retracement of 1.3624 to 1.5226 at 1.4236.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to resume to retest 1.6587. The corrective structure of the fall from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, further downside acceleration will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

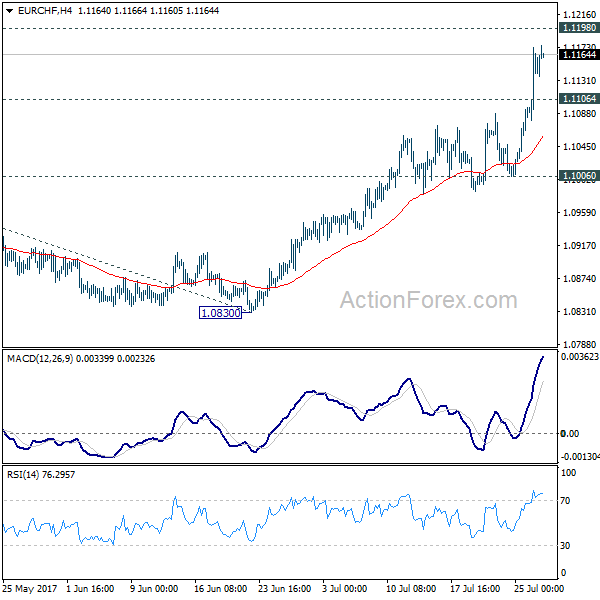

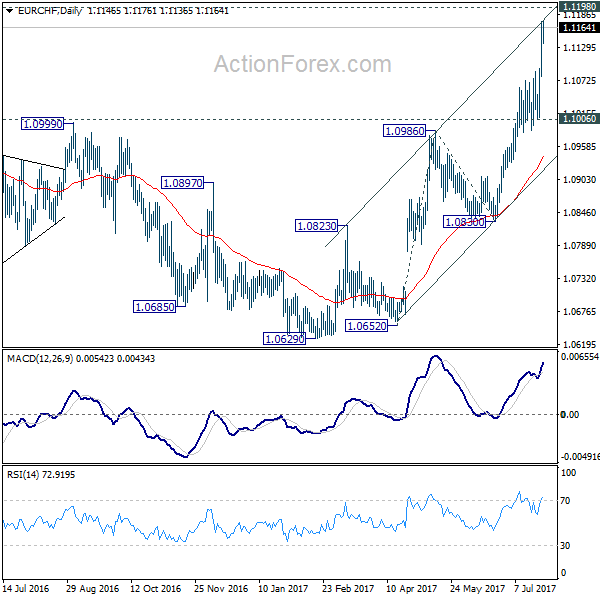

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1099; (P) 1.1136; (R1) 1.1194; More...

Intraday bias in EUR/CHF remains on the upside as current rally is in progress for 1.1198 key resistance level. Sustained break there will carry larger bullish implication. In such case, next near term target will be 161.8% projection of 1.0652 to 1.0986 from 1.0830 at 1.1370. On the downside, below 1.1106 minor support will turn intraday bias neutral first. But retreat should be contained by 1.1006 to bring rise resumption.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Such correction could have completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.1198 will resume the long term rise from SNB spike low back in 2015. In such case, EUR/CHF could eventually head back to prior SNB imposed floor at 1.2000. We'll favor this bullish case as long as 1.0830 support holds. However, rejection from 1.1198 will extend the multi-year range trading with another fall.

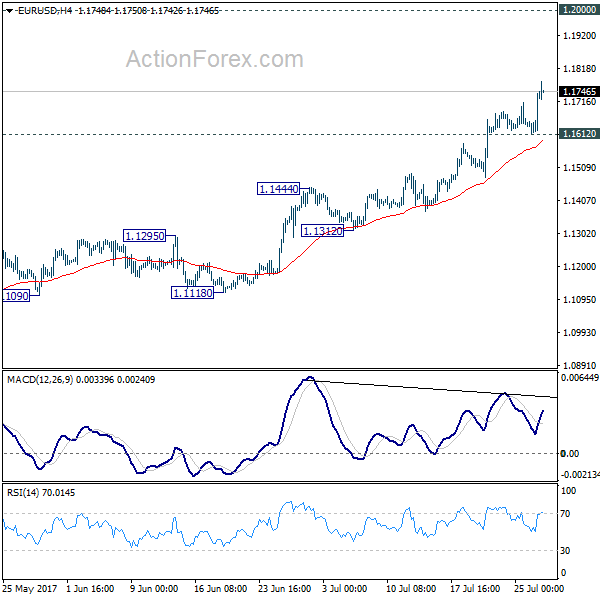

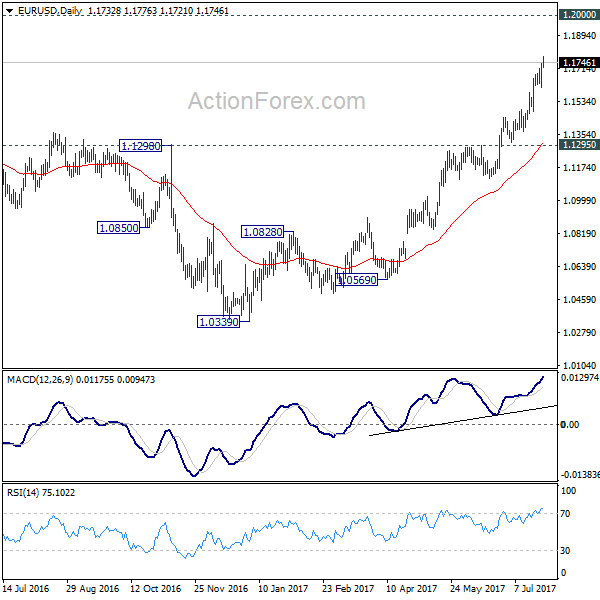

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1649; (P) 1.1695 (R1) 1.1777; More...

EUR/USD's rise resumed after brief consolidation and intraday bias is back on the upside. Current rally is expected to target 1.2 handle next. On the downside, break of 1.1612 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained break of 55 month EMA (now at 1.1760) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

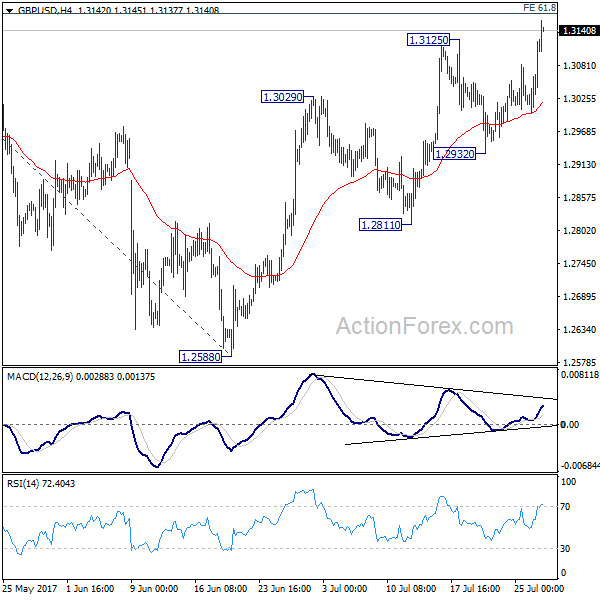

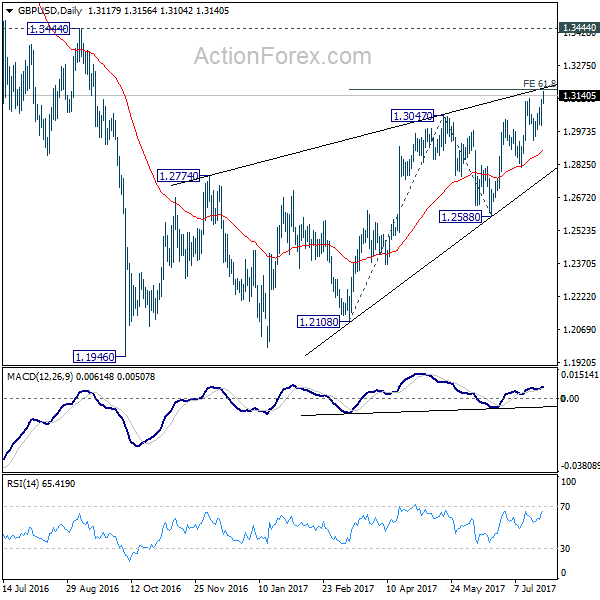

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3037; (P) 1.3080; (R1) 1.3161; More...

GBP/USD's rise resumed by taking out 1.3125 and intraday bias is back on the upside. At this point, we'll stay cautious on strong resistance from 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 to limit upside. However, sustained break there could extend recent rebound towards 1.3444 key resistance. But still, price actions from 1.1946 is seen as a corrective pattern and GBP/USD should feel heavy approaching 1.3444. On the downside, break of 1.2932 support will be the first sign of reversal and will turn bias to the downside to target 1.2588 key support next.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

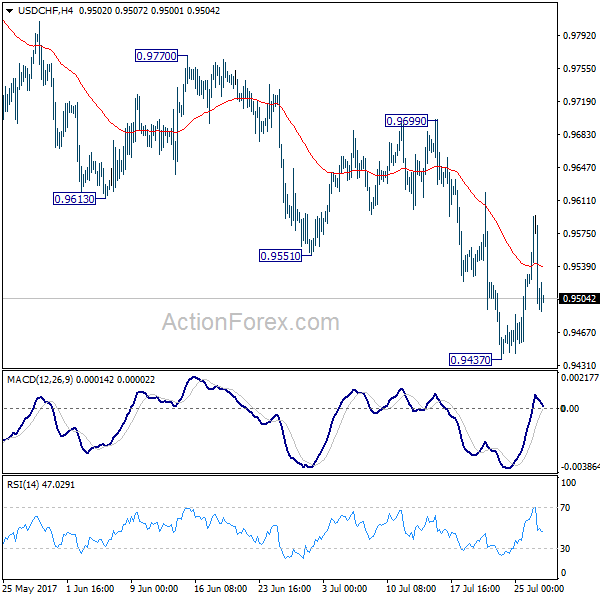

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9472; (P) 0.9533; (R1) 0.9569; More...

Intraday bias in USD/CHF remains neutral as it's staying in range of 0.9437/9699. At this point, we remain cautious on strong support from 0.9443 key support to bring reversal. Decisive break of 0.9699 will confirm and turn outlook bullish. Meanwhile, sustained trading below 0.9443 will extend the down trend from 1.0342 to 161.8% projection of 1.0342 to 0.9860 from 1.0099 at 0.9319.

In the bigger picture, focus is now back 0.9443 key support level. Sustained break there indicate underlying bearish momentum and would target 0.9 handle and possibly below. Meanwhile, strong rebound from current level and break 0.9699 resistance will extend long term range trading between 0.9443/1.0342.

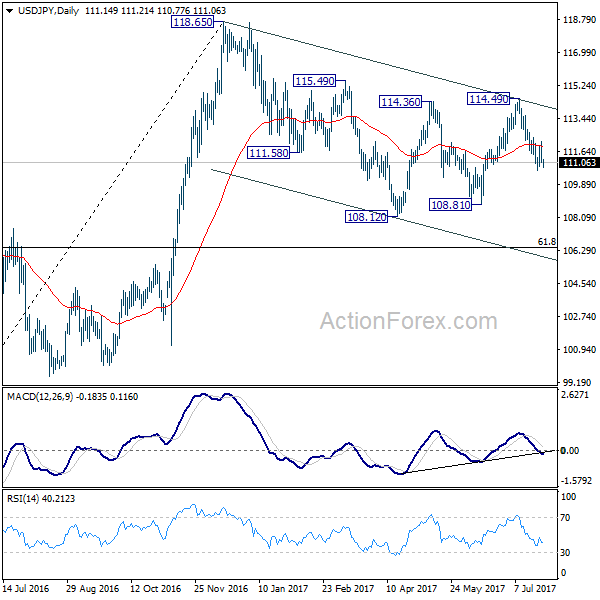

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.76; (P) 111.47; (R1) 111.89; More...

At this point, USD/JPY is staying in range of 110.61/112.41 and intraday bias remains neutral. With 112.41 intact, further decline is expected. Below 110.61 will target 108.81. Break there will resume whole correction from 118.65 and target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, break of 112.41 will dampen this bearish view and turn focus back to 114.49 resistance instead.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2391; (P) 1.2467; (R1) 1.2521; More....

USD/CAD's decline is still in progress and took out 1.2460 key support level. We'd stay cautious on rebound on bullish convergence condition in 4 hour MACD, as well as deep oversold condition in daily RSI. But for the moment, further fall is expected as long as 1.2543 minor resistance holds. Sustained trading below 1.2460 will target next key fibonacci level at 1.2048. On the upside, break of 1.2543 will indicate short term bottoming and bring rebound.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Fall from 1.3793 is seen as the third leg and should target 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. However, firm break there will target 100% projection of 1.4689 to 1.2460 from 1.3793 at 1.1564.