Sample Category Title

Yen Steady at 112 as Japanese Inflation Matches Expectations

USD/JPY is showing little movement in the Wednesday session. In the North American session, the pair is trading at the 112 line, up 0.07% on the day. On the release front, the Japanese Services Producer Price Index edged up to 0.8%, matching the forecast. In the US, New Home Sales remained steady at 610 thousand, short of the estimate of 615 thousand. Later in the day, the Federal Reserve releases its rate statement and is expected to maintain the benchmark at 1.25%. On Thursday, the US will release two key indicators – Unemployment Claims and Core Durable Goods Orders. Japan will release a host of inflation indicators, led by Tokyo Core CPI. The indicator is expected to post a small gain of 0.1%.

The Bank of Japan minutes from the June meeting revealed a split among members as to how much information the bank should disclose regarding a potential withdrawal from its quantitative easing program. Some policymakers were in favor of full disclosure about the bank's plans, while others said that publicizing information about an exit too soon could lead to market volatility. As expected, the BoJ maintained its ultra-loose policy, but there was an unexpected development, as the bank revised upwards its forecast for consumer consumption, for the first time in six months. An additional complication for policymakers is that the BoJ is now trailing other central banks with regard to tightening monetary policy – the Federal Reserve and Bank of Canada recently raised rates, and the ECB and BoE are contemplating tighter policy. If the BoJ continues to lag behind the other central banks, the yen could lose ground against other currencies.

All eyes are on the Federal Reserve, which concludes its monthly policy meeting later on Wednesday. The Fed is not expected to alter its interest rate policy, but the rate statement could still be a market-mover. The rate statement will be under careful scrutiny, as analysts will be looking for any references to the "I" word. Inflation continues to hover around 1.4% (based on the Fed's calculations), well below the Fed target of 2%. In June, Janet Yellen described low inflation as "transitory", but recent comments from Yellen and other policymakers have shifted in tone, an apparent acknowledgment that inflation may remain stuck at low levels. This has raised doubts as to whether the Fed will indeed raise rates one more time this year. No move is expected before December, and the odds of a December hike have fallen to just 37%, according to the CME Group. If today's rate statement fails to reassure the markets that a December hike is planned, investors could respond by selling dollar-denominated assets in favor of other currencies or gold.

Aside from interest rates, Fed members will be discussing when to commence tapering the Fed's $4.2 trillion bond portfolio. The bloated balance sheet is a result of the aggressive quantitative easing program which was put in place after the financial crisis in 2008. In June, the Fed outlined plans to taper purchases, with experts circling September as the start date of the reduction. This would involve the Fed tapering the purchases of Treasury bonds and mortgage securities, with an initial taper likely of $10 billion/month. Analysts expect the taper to begin in September, so we could see the Fed make reference to this in the July statement.

Forex Market Awaits FOMC Statement; Pound Helped by UK GDP

It was a relatively quiet day in forex markets as traders were mostly looking forward to the Fed statement later in the US session and as UK second quarter GDP figures were in line with estimates.

In the day's main economic news, the preliminary estimate of UK second quarter GDP came in line with expectations at 0.3% quarter-on-quarter and 1.7% year-on-year. This was on the one hand a slowdown from the previous quarter's 2% year-on-year growth rate but the quarterly rate improved slightly from 0.2% in the first quarter. The UK Chancellor acknowledged that uncertainty about Brexit was a burden for the country's economy as he said more clarity on that front would help. The pound managed to broadly hold the 1.30 level against the US dollar and rose to as high as 1.3061. Euro/pound was relatively soft at 0.8922.

The euro was comfortably holding the 1.16 handle against the US dollar following the upbeat German Ifo business survey released the previous day, while the US dollar received a short-term boost from the surprisingly strong consumer confidence numbers which were also out on Tuesday. A rise in German 10-year yields on Tuesday was also supporting the single currency. German 10-year paper was yielding 0.55% on Wednesday from around 0.49% on Monday.

The US dollar stayed within relatively narrow ranges against both the euro and the yen in anticipation of the statement from the Federal Reserve's rate-setting committee later in the US session. The Fed could comment either on the pace of its future interest rate hikes or on when it would commence to slowly shrink its massive $4.5 trillion balance sheet. Some economists also thought that the Fed could reveal little and choose to give more clues during its annual Jackson Hole Symposium which is held every August. Euro/dollar was last at 1.1627 and dollar/yen was 111.94.

In US data, new home sales for June came in close to expectations at 610 thousand units and also close to the previous month's starts of 605 thousand (seasonally adjusted, annual rate). As such, the upbeat starts did not impact the dollar much.

Gold managed to recover some of the losses it made the previous day and during today's Asian session to climb back to $1248 an ounce. In the oil market, weekly crude oil inventory figures showed a much larger-than-expected reduction of 7.2 million barrels compared with analysts' forecast of a 2.62 million barrels drawdown. Consequently, WTI oil rose to around $48.45 a barrel and was trying to break through the previous day's high of $48.63.

Looking ahead, traders will of course focus on the FOMC statement later in the day. Thursday is looking relatively quiet for forex markets, with the exception of June durable goods in the US.

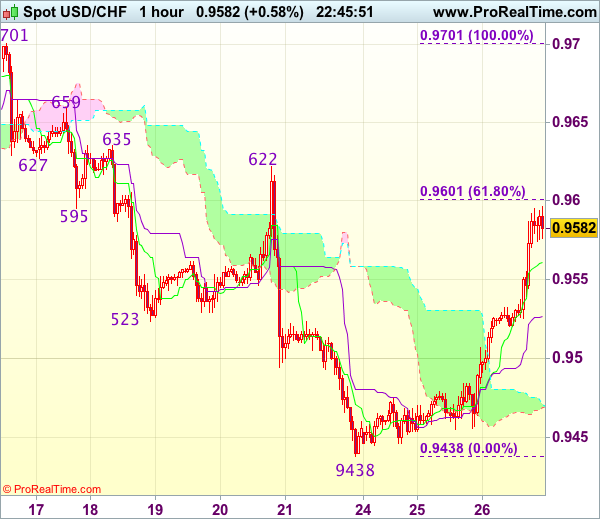

Trade Idea Wrap-up: USD/CHF – Hold short entered at 0.9570

USD/CHF - 0.9588

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9561

Kijun-Sen level : 0.9527

Ichimoku cloud top : 0.9471

Ichimoku cloud bottom : 0.9469

Original strategy :

Sold at 0.9570, target: 0.9470, Stop: 0.9605

Position : - Short at 0.9570

Target : - 0.9470

Stop : - 0.9605

New strategy :

Hold short entered at 0.9570, target: 0.9470, Stop: 0.9605

Position : - Short at 0.9570

Target : - 0.9470

Stop : - 0.9605

As the greenback has maintained a firm undertone after staging a strong rebound from 0.9438 late last week, suggesting near term upside risks remains for this corrective bounce to extend marginal gain from here, however, reckon upside would be capped at 0.9600-05 (61.8% Fibonacci retracement of 0.9701-0.9438) and bring retreat later, below 0.9520 would suggest an intra-day top is possibly formed but break of 0.9450-55 is needed to signal the rebound from 0.9438 has ended, bring retest of this level first.

In view of this, we are holding on to our short position entered at 0.9570. Above 0.9600-05 (61.8% Fibonacci retracement of 0.9701-0.9438) would suggest a temporary low is formed instead, bring a stronger rebound towards resistance area at 0.9622-35.

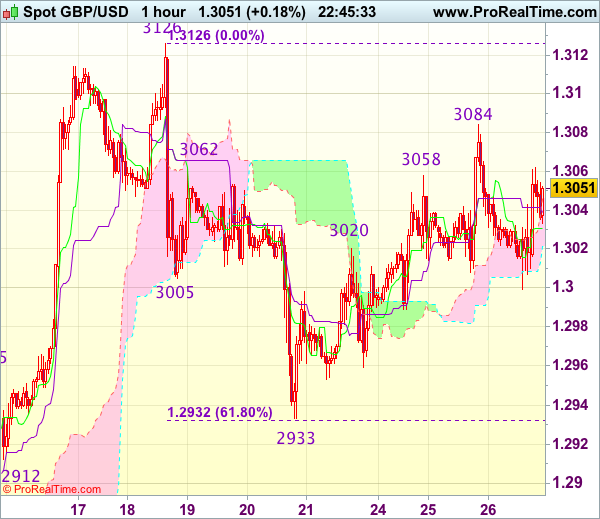

Trade Idea Wrap-up: GBP/USD – Sell at 1.3100

GBP/USD - 1.3048

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3031

Kijun-Sen level : 1.3039

Ichimoku cloud top : 1.3046

Ichimoku cloud bottom : 1.3022

Original strategy :

Sell at 1.3100, Target: 1.2980, Stop: 1.3135

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3100, Target: 1.2980, Stop: 1.3135

Position : -

Target : -

Stop : -

Although cable retreated after rising to 1.3084 yesterday, break of 1.2980-85 is needed to signal top is formed, bring further fall to 1.2950-55 but only below there would confirm the rebound from 1.2933 has ended, then another test of this support would follow, once this level is penetrated, this would add credence to our view that early fall from 1.3126 top has resumed for further weakness to previous support at 1.2912 which is likely to hold on first testing.

In view of this, would not chase this fall here and we are looking to sell cable on subsequent recovery as 1.3100-10 should limit upside. A firm break above 1.3100 would abort and suggest the fall from 1.3127 has ended instead, bring retest of this level but only break there would shift risk back to upside for further gain to 1.3150-60.

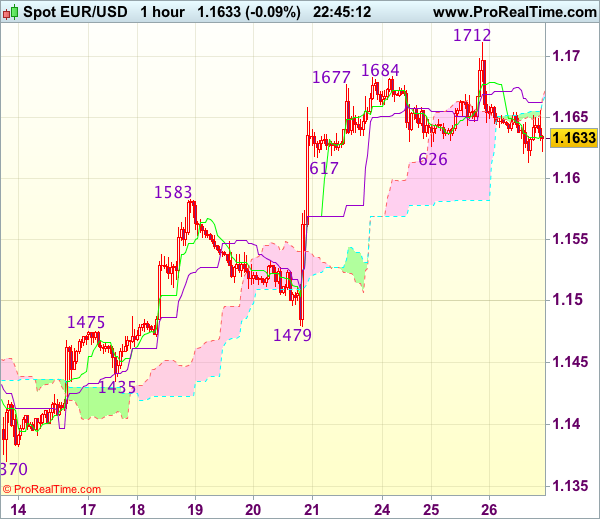

Trade Idea Wrap-up: EUR/USD – Sell at 1.1680

EUR/USD - 1.1637

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1635

Kijun-Sen level : 1.1663

Ichimoku cloud top : 1.1667

Ichimoku cloud bottom : 1.1663

Original strategy :

Sell at 1.1680, Target: 1.1580, Stop: 1.1715

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1680, Target: 1.1580, Stop: 1.1715

Position : -

Target : -

Stop : -

Although the single currency moved higher to 1.1712 yesterday, the subsequent retreat suggests consolidation below this level would be seen and as long as 1.1712 holds, mild downside bias is seen for test of 1.1617-20 support, break there would signal a temporary top is formed, bring retracement of recent rise towards previous resistance at 1.1583 but price should stay above 1.1550, bring another rally later.

In view of this, we are looking to turn short on recovery but one should exit on such fall. Above said resistance at 1.1712-14 would signal the rise from 1.0340 low is still in progress and may extend headway towards 1.1750, then 1.1775-80.

Trade Idea Wrap-up: USD/JPY – Exit short entered at 112.00

USD/JPY - 111.90

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.85

Kijun-Sen level : 111.73

Ichimoku cloud top : 111.17

Ichimoku cloud bottom : 111.12

Original strategy :

Sold at 112.00, Target: 111.00, Stop: 112.35

Position : - Short at 112.00

Target : - 111.00

Stop : - 112.35

New strategy :

Exit short entered at 112.00

Position : - Short at 112.00

Target : -

Stop : -

As the greenback has maintained a firm undertone, suggesting near term upside risk remains for the rise from 110.62 (this week’s low) to extend gain to 112.08-10 (previous resistance and 50% Fibonacci retracement of 113.58-110.62), break there would bring headway towards 112.42-45 (previous resistance and 61.8% Fibonacci retracement), however, reckon upside would be limited and price should falter well below resistance at 112.87, bring retreat later.

In view of this, would be prudent to exit short and look to sell dollar again on subsequent rally. Below 111.55-60 would suggest top is possibly formed but break of previous resistance at 111.34 (now support) is needed to add credence to this view, bring weakness to 111.10-15, below there would suggest the rebound from 110.62 has ended, bring test of 110.83 support first.

Elliott Wave Analysis: USDJPY Breaking Higher; More Bullish Moves Expected

USDJPY can also be trading within wave A, as part of a bigger three wave recovery as USDCHF. Well, if that is the case, the more upside may come in sessions ahead. At the moment we see blue sub-wave iv in the making, that can see limited downside near the 111.5/111.70 region. Once sub-wave iv unfolds, a new push higher into the following leg v can come in play, with potential limited upside near the previous swing high of wave B at the 112.43 level.

USDJPY, 1H

Copper Regained Strong Momentum on Very Positive Sentiment

July copper rose further on Wednesday, extending strong rally on Tuesday when the metal was up 3.75% for the day. Copper hit fresh over two-year high at $2.9040, after generating strong bullish signal on Tuesday's close above strong resistance at 2.8215 (13 Feb former top) one-year recovery rally from $1.9360 (2016 low). Further upside is seen likely as the metal regained strong momentum on very positive sentiment, boosted rising demand from the biggest copper consumer China, as well as tight supply. Bulls could extend towards Fibo 138.2% projection at 2.9550, with psychological $3.0000 barrier also coming in sight. The price so far did not show more significant reaction on strongly overbought daily studies, but technical pullback on profit-taking after strong rally could be expected. Limited correction should ideally find footstep at 2.8250/15 zone (Fibo 38.2% of 2.6975/2.9040 upleg/former high) with extension towards 2.8000 (50% retracement) which would keep larger bulls intact. Otherwise, loss of 2.8000 handle would initial signal of deeper pullback.

Res: 2.8885; 2.9040; 2.9310; 2.9550

Sup: 2.8555; 2.8305; 2.8215; 2.8000

USDCAD in Consolidation Mode after Repeated Unsuccessful Probes Below 1.2500 Support

The USDCAD pair is in consolidation mode after repeated unsuccessful probes below 1.2500 support. Tuesday's close in tight Doji signaled hesitation at 1.2500 hurdle (that I anticipated in my previous report), following dips to 1.2483/80 lows on Mon/Tue, but close above 1.2500 on both days. Reaction was so far mild as daily technical studies remain firmly bearish and lacking firmer positive signals, despite strongly oversold conditions. Limited upside attempts stay so far under Tuesday's high at 1.2532, short of the initial pivot at 1.2545 (hourly cloud top) and more significant barriers at 1.2595 (falling 10SMA) and 1.2613 (daily Tenkan-sen) regain of which is needed to generate stronger reversal signal. Overall bearish structure suggests limited correction ahead of final push towards target at 1.2459 (03 May 2016 low). The pair may stay within narrow consolidation, awaiting FOMC statement for firmer signals.

Res: 1.2532; 1.2545; 1.2595; 1.2613

Sup: 1.2500; 1.2480; 1.2459; 1.2400

Fed to Decide on Next USD-Move?

- Gains in commodities from oil to copper lent momentum to European stocks as positive corporate results continued to feed into markets.

- GDP-growth in the UK edged up in Q2, in line with expectations. The ONS estimates the economy expanded by 0.3% Q/Q, up from 0.2% Q/Q in Q1. The year on year growth slowed to 1.7% from 2%.

- The INSEE office released figures showing French consumer confidence fell from 108 in June (a 2007 high) to 104 in July while a stabilisation was expected. The survey also revealed concerns over rising unemployment while inflation expectations also leapt among consumers.

- Copper prices have jumped to the highest level in two years following reports China could move to ban imports of scrap metal by the end of next year, a move that would likely boost demand for refined metals in China.

- The UK government says it will ban sales of fossil-fuelled vehicles by 2040, two weeks after France announced a similar plan.

- Poland, Hungary and the Czech Republic suffered a double blow as the EU mounted a legal fightback to force them to comply with EU refugee quotas. The EU forged ahead to enforce the law, as it prepared to sign-off legal suits against hold-out countries and separately won a favourable opinion at Europe's top court.

- The European Commission stands ready to trigger fresh legal action against the Polish government despite the country's president vetoing two out of four controversial reforms to the Polish judiciary. The EC vice president said the approval of the remaining measures still undermined the independence of the country's judges.

Rates

Core bonds move sideways ahead of FOMC decision

Global core bonds took a breather today following yesterday's sell-off and ahead of the FOMC decision later this evening. Equities traded with a positive bias, while oil moved sideways keeping yesterday's steep gains intact. No firm directional moves either on the main FX crosses. None of these other market had a noticeable impact on bond trading. The eco calendar was thin with UK Q2 GDP weak, but as expected at 0.3% Q/Q and French consumer confidence disappointing. The bond movements were also technically irrelevant. Needless to say that bond volumes traded were very light. Summarizing, dull trading across the board during the Summer holidays before the FOMC decision.

At the time of writing, US yields fell between 0.3 bps (30-yr) and 1.2 bps (5-10yr), the belly marginally outperforming the wings. Changes on the German yield curve were slightly bigger (-1.4 to -1.8 bps). On intra-EMU bond markets, 10-yr yield spread changes versus Germany varied between -2 bps (Italy) and +2 bps (Greece). Dull trading continued. The Italian small IL and zero coupon auctions went well.Later today, the Treasury holds its 5-year T-Note auction and the FOMC concludes its meeting. The FOMC has little incentive to inject volatility in these thin Summer markets and may wait for the September meeting to take some decisions. At that time, new eco and rate projections will be available and chair Yellen will hold a press conference to explain eventual new decisions. Two items nevertheless need to be watched in the FOMC statement this evening. First, will the FOMC announce the start of the tapering of its balance sheet? September is the more likely announcement date, but there is a small chance it will be announced today (to start in October?). It would underline that the Fed considers this tapering as a background event that will continue independent of temporary developments in the economy, for which its main tool, the FF rate, will be used. Second, will the Fed show more concerns about the low inflation readings of the past four month? Depending on the outcome of these questions, there might be some moves in the US Treasury market. Overall though, these should be subdued and temporary.

Currencies

Fed to decide on next USD-move?

Today, trading in the major USD cross rates was somewhat paralysed as investors kept side-lined ahead of this evening's Fed policy statement. The dollar tried to extend yesterday's rebound during European trading, but the bid faded later in the session. EUR/USD trades in the 1.1635 area. USD/JPY is changing hands in the 111.80/0 area. The Fed holds the key to unlock this stalemate.

Asian equities traded mixed to slightly lower. Japan and Australia outperformed on a decline of their currencies. USD/JPY maintained yesterday's gain and traded just below 112 going into European trading. The dollar also held its gains against the euro with EUR/USD trading in the 1.1635 area.

There were no important data in Europe. Trading in the major dollar cross rates was order-driven as investors awaited the Fed policy statement. The dollar initially kept a slightly positive bias. Especially EUR/USD lost a few more ticks and filled bids in the 1.1615 area mid-morning. USD/JPY didn't go anywhere. Changes in interest rate differentials were insignificant and no driver for USD trading. Sentiment on the dollar turned a bit softer going into the start of US dealings. EUR/USD returned to the mid 1.16 area. USD/JPY lost a few ticks to the 111.75 area. US investors didn't place big USD bets ahead of the Fed policy statement. EUR/USD trades in the 1.1640 area and USD/JPY is changing hands in the 111.80 area.

We expect the Fed to be more concerned on inflation but to keep the door open for a December rate hike. The market implied probability of a December rate hike is less than 50%. We don't expect the Fed to be so soft that markets reduce their expectations further. With US interest rates already at very low levels, one could assume that there is quite some negative news discounted for the dollar. US eco news has to be very good before it can trigger a sustained USD rebound. However, assuming that the Fed statement won't be overly soft, we expect no sustained break of the key 1.1714/35 resistance for now.

Sterling doesn't react to soft UK Q2 growth

Today's UK Q2 GDP estimate was one of the last important data series ahead of next week's BoE policy decision. UK Q2 GDP growth printed at 0.3% Q/Q and 1.7% Y/Y, exactly as expected. EUR/GBP was under slight pressure going into the GDP report, but this was euro softness rather than GBP strength. EUR/GBP temporarily dropped to the 0.8915 area, but rebounded slightly after the data. T The sterling correction didn't go far as global markets were in some kind of lethargy ahead of the Fed policy decision. The market implied probability of a BoE rate hike was and remains low (about 10 %). There probably is additional negative news (or spill-overs from other cross rates) needed to trigger additional sterling losses. EUR/GBP trades in the 0.8920 area. Cable trades near 1.3050.