Sample Category Title

EUR/JPY Continues Higher

After blowing through double top resistance, EUR/JPY has continued higher on fundamentally driven Euro strength.

I don't normally go as wide as the weekly chart, but higher time frame levels are the same no matter what time frame you view them on and this one is no different. Take a look at the weekly EUR/JPY chart below:

EUR/JPY Weekly:

As you can see, the price of EUR/JPY has returned to quite the significant zone. Just take a look at all the markers that I've placed on the chart.

Literally years and years of touches on both sides of the line. Also significant is the fact that each of the breakouts have been swift. Look at the full candle bodies when the line has been broken. This means that it takes something to make the level snap.

Now zoom into the intraday chart and let's take a look at the price action that we're now seeing:

EUR/JPY 4 Hourly:

Price is respecting the level on an intraday basis too, but those higher highs mean that price is coiling for a possible break higher.

Just keep in mind that EUR/USD is breaking out of higher time frame resistance and momentum is strong.

FOMC Fallout

FOMC Fallout

The Fed has articulated its concerns about the low level of inflation in the US, which lessens the likelihood of a December rate hike. The US dollar then dropped against the other major currencies in a lively afternoon New York session on Wednesday.

As expected, The Feds tipped their hat to the widely telegraphed September balance sheet reduction timing, but it was the subtle downgrade in inflation language which the markets pounced on leaving the December rate hike camp perched precariously. But realistically, after four consecutive misses on US CPI, the writing was on the wall.

Now traders are left mulling over how to deal with the greenback going forward knowing there’s a lot of important data to deal with between now and December. Some are resisting the temptation to not to over react to a Fed that was not supposed to be this dovish, but this price action is too hard to ignore.

EURO

The Euro sprang to life taking out the key 1.0715 Euro’s strength continues to be the market focus, and while we’ve stalled out a bit in Asia unless there’s some re-inflationary signal from Friday’s GDP/PCE, it’s hard to envision any support for the greenback near term. Which would suggest the path of least resistance is higher EURUSD From the 1.4 move, down to 1.0341). Where to from here?

G-10 Complex

Everything else has reacted as expected with the both the KIWI and Aussie taking flight

Outside for the FOMC

The US Senate vote to repeal Obamacare failed. So back to headline watching to see whats next.

WTI nearly hit $49.0 on the back of inventory data providing an underpin to the commodity complex.

USD/CAD Canadian Dollar Higher After Fed Inaction And Oil Inventory Drawdown

The Canadian dollar rose on Wednesday after the Federal Open Market Committee (FOMC) statement kept interest rates unchanged as expected. The biggest highlight of the Fed’s communication was the addition of “relatively soon” to the timing for the start of the central bank’s balance sheet reduction. The September FOMC meeting is seen as a likely candidate to begin trimming the portfolio of assets accumulated during the quantitive easing program.

Weekly US Inventories Fall More than Expected

Oil prices jumped close to 2 percent after the release by the Energy Information Administration (EIA) of the weekly US crude inventories. Oil stocks fell by 7.2 millions barrels, gasoline by 1 million barrels and distillates by 1.9 millions barrels. The larger than expected drawdown pushed oil prices higher as US production is starting to slowdown and the Organization of the Petroleum Exporting Countries (OPEC) and Russia are not backing down in their plans to extend production cuts to reduce the global oil glut.

Fed Remains Optimistic But Concerned About Inflation

The U.S. Federal Reserve tweaked the language on its July FOMC statement from the one published last month regarding inflation. A slight downgrade was evident as the Fed removed the “somewhat” when talking about inflation declining. The other major change was a big signal toward the balance sheet reduction to start in September. Overall there was nothing new for the market and the downgrade on inflation was seen as dovish which is the main reason the USD is on the back foot across the board. Political uncertainty in Washington is not doing the dollar any favors as the healthcare reform debate continues with low probability of a definite outcome.

The USD/CAD lost 0.241 percent in the last 24 hours. The currency is trading at 1.2482 after a dovish FOMC statement was delivered earlier today. The July FOMC meeting did not include a press conference which meant that the document at the end of the meeting was all the central bank would share with the market. The language remained almost unchanged, adding very little to the already known and well telegraphed plans of balance sheet reduction and a potential rate hike later in the year.

The loonie rose against the US dollar as economic indicators in Canada have proven the economy is on a solid path of growth, while the US fundamentals continue to be mixed while also adding the political turmoil surrounding the Trump administration. The Fed has been the biggest supporter of the dollar ever since the market has priced out a Trump bump this year as pro-growth policies promised after the President’s victory are yet to arrive.

The Canadian currency is at a two year high versus the dollar ahead of Friday’s monthly GDP numbers for Canada and the US first estimate of second quarter growth. The loonie rally faces few obstacles unless economic indicators start to soften and the US shakes off the cloud of political uncertainty along with a better than expected GDP.

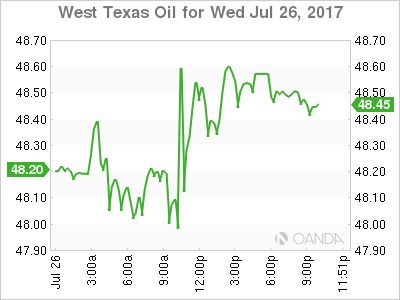

The price of oil gained 1.838 percent on Wednesday. West Texas Intermediate is trading at $48.54 after the USD retreated following an uneventful Federal Open Market Committee (FOMC) statement published by the U.S. Federal Reserve and a larger than expected drawdown in US weekly crude stocks.

The 7.2 drawdown in weekly inventories was higher than analyst expected with the API report a day earlier also showing a fall of 10.2 million barrels. The comments from US producers about the lack of revenue at current price levels forcing them to cut capital expenses has also driven prices higher as US output is not expected to keep pace against the OPEC led agreement cut in supply.

The price of WTI is near an 8 week high after the OPEC and the other producers who joined the production cut agreement appear to have more stamina than US producers. Risks remain in particular around compliance levels as deeper cuts or even maintaining the current output might be unsustainable for members of the agreement. Already Ecuador and Venezuela have pleaded their case to OPEC. Libya and Nigeria are still exempt from the deal given their latest disruptions caused by geopolitical issues.

Relations within the OPEC are also fragile with Iran and Saudi Arabia on opposite sides of an ideological dispute with other producers taking sides or being forced to like Qatar. Iraq has also hinted that they could increase production but no more details have been shared after the meeting in Russia. Saudi Arabia promised a more stringent compliance regime to assure output limits are enforced.

Market events to watch this week:

Thursday, July 27

8:30 am USD Core Durable Goods Orders m/m

8:30 am USD Unemployment Claims

Friday, July 28

8:30 am CAD GDP m/m

8:30 am USD Advance GDP q/q

Fed Stands Pat as Expected, Signals Coming Balance Sheet Normalization

Highlights:

- The target range for the fed funds rate was left unchanged at 1.00-1.25% as expected.

- The Fed's characterization of the economy was almost entirely unchanged: growth has been moderate with household spending and business investment continuing to expand.

- The recent decline in both all items and core inflation was noted and inflation is expected to continue running below 2 percent in the near term. Chair Yellen has previously attributed some of the slowing to transitory factors.

- Near-term risks to the outlook were again characterized as "roughly balanced."

Our Take:

Expectations for this week's meeting were low and the Fed delivered on that with no rate change and a policy statement that was very similar to June's. The sole development was a change in language on balance sheet normalization though that was not a surprise. The Fed is now indicating that the planned change in their reinvestment policy, which was outlined in June, will begin "relatively soon." We think today's guidance sets up for tapering to be announced in September and implemented in October. The pace of tapering laid out by policymakers is gradual but nonetheless we think the Fed will want to see how the market reacts. As such, we look for interest rates to be held steady once again in September, breaking the recent trend of one hike per quarter. Holding off on further rate increases until later this year will also give the Fed some time to evaluate inflation developments. We think the Fed will want to see some evidence that tight economic and labour market conditions are actually feeding through to higher prices before going too far toward normalizing interest rates.

Fed Acknowledges the Inflation Miss, But Sticks to Balance Sheet Plans

As widely expected, the Federal Open Market Committee (FOMC) held the target range for the federal funds rate unchanged between 1 and 1-1/4 percent.

The Fed's views appear to have changed very little from the mid-June meeting round, with only minor wording changes in the policy statement.

The Committee upgraded its view of the labor market, removing the previous reference to a moderation in hiring, instead highlighting that job gains have been "solid." Household spending and business investment were also viewed as having expanded.

The Fed had previously communicated that overall inflation declined and the core metric was running "somewhat below" 2%.This wording was changed, with both the overall and core metrics viewed as having declined in today's statement. Moreover, the FOMC removed the "somewhat" qualifier, suggesting that the magnitude of the divergence from target is greater.

The Fed changed its forward guidance on policy, indicating that it will keep reinvesting MBS and rolling over Treasuries "for the time being," expecting the normalization program to start "relatively soon." No new details on this were provided above and beyond what was communicated in the Addendum in June.

This was a unanimous decision, with Kashkari (FRB Minneapolis) voting with the Committee once again, after dissenting in June.

Key Implications

There was not much here to work with as far as clues to Fed thinking with the Committee only tinkering with the words a bit.

The Fed's take on the economy appears relatively sanguine, with the current momentum seen as improved after some moderation earlier in the year. However, the Committee's views of inflation took a dovish turn, with the Fed acknowledging that both headline and core metrics have declined and are no longer running just "somewhat" below 2%.

Having said that, the Fed does not appear to be willing to alter its plans, at least as far as balance sheet normalization is concerned. The statement's wording that reinvestments/roll-overs will only continue "for the time being" with balance sheet run-off expected to start "relatively soon" suggests that the Committee is readying to initiate balance sheet normalization at its September meeting, with the run-off starting the following month.

Fed Will Start Balance Sheet Normalization “Relatively Soon”, But Dollar Bulls Clearly Dissatisfied

Dollar bulls are clearly unhappy with the FOMC statement today. Fed kept target range for the federal funds rate at 1 to 1.25% as widely expected. The new FOMC statement was almost a carbon copy of the May's one. The exceptions are firstly, Fed indicated that it will start the "balance sheet normalization program relatively soon". Secondly, Fed took the part that "job gains have moderated" and just described that "job gains have been solid". It's clear that markets are taking the message that Fed is going to announce the plan to shrink the balance sheet in September. And Fed will hold it cards for another rate hike till December to see how the economy evolves.

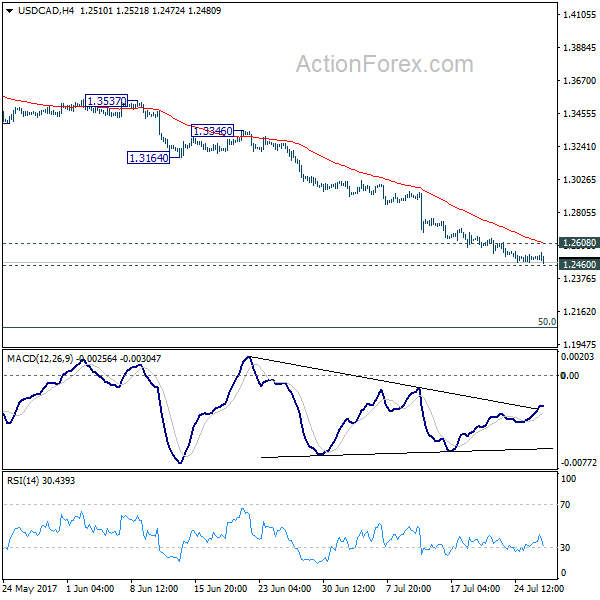

At the time of writing, USD/CAD has already breached this week's low to extend recent down trend. Strength in oil price after inventory data is certainly a factor Key focus will remain on 1.2460 major support. We stay cautious on strong support from this level to bring rebound, considering loss of downside momentum as seen in bullish convergence condition in 4 hour MACD. But sustained break of 1.2460 will pave the way to next medium term fibonacci level at 1.2048.

Despite the strong rebound since making a low at 110.61 on Monday, USD/JPY was held well below 112.41 resistance. Near term outlook remains bearish. Break of 110.61 will affirm our bearish view that recent fall from 118.65 is still in progress for another low below 108.12, possibly to next medium term fibonacci level at 106.48.

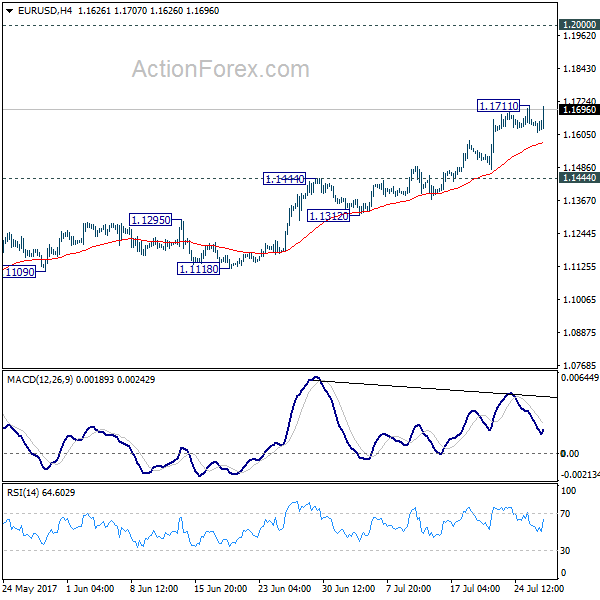

At the time of writing, EUR/USD is still limited below 1.1711 temporary top. But overall outlook stays bearish with the pair kept well above 1.1444 resistance turned support. We'd expect a break of 1.1711 to extend recent rally to 1.2 handle.

(FED) FOMC Statement Jul 26, 2017

Information received since the Federal Open Market Committee met in June indicates that the labor market has continued to strengthen and that economic activity has been rising moderately so far this year. Job gains have been solid, on average, since the beginning of the year, and the unemployment rate has declined. Household spending and business fixed investment have continued to expand. On a 12-month basis, overall inflation and the measure excluding food and energy prices have declined and are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee continues to expect that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace, and labor market conditions will strengthen somewhat further. Inflation on a 12-month basis is expected to remain somewhat below 2 percent in the near term but to stabilize around the Committee's 2 percent objective over the medium term. Near-term risks to the economic outlook appear roughly balanced, but the Committee is monitoring inflation developments closely.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 1 to 1-1/4 percent. The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

For the time being, the Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. The Committee expects to begin implementing its balance sheet normalization program relatively soon, provided that the economy evolves broadly as anticipated; this program is described in the June 2017 Addendum to the Committee's Policy Normalization Principles and Plans.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Patrick Harker; Robert S. Kaplan; Neel Kashkari; and Jerome H. Powell.

Gold Ticks Lower as Markets Eye Federal Reserve Statement

Gold has edged lower in the Wednesday session. In North American trade, spot gold is trading at $1248.46, down 0.18% on the day. On the release front, New Home Sales was unchanged at 610 thousand, short of the estimate of 615 thousand. Later in the day, the Federal Reserve releases its rate statement and is expected to maintain the benchmark at 1.25%. On Thursday, the US will release two key indicators – Unemployment Claims and Core Durable Goods Orders.

The Federal Reserve is unlikely to make a rate move at its policy meeting later on Wednesday. So what can we expect to hear from the Fed? The rate statement will be under careful scrutiny, as analysts will be looking for any references to the "I" word. Inflation continues to hover around 1.4% (based on the Fed's calculations), well below the Fed target of 2%. In June, Janet Yellen described low inflation as "transitory", and policymakers sent broad hints about a December rate hike. However, recent comments from Yellen and other policymakers have shifted in tone, an apparent acknowledgment that inflation may remain stuck at low levels. This has raised doubts as to whether the Fed will indeed raise rates one more time this year. No move is expected before December, and the odds of a December hike have fallen to just 37%, according to the CME Group. If today's rate statement fails to reassure the markets that a December hike is planned, investors could respond by selling dollar-denominated assets in favor of other currencies or gold.

Another key issue on the Fed's agenda is when to begin tapering the Fed's $4.2 trillion bond portfolio. The bloated balance sheet is a result of the aggressive quantitative easing program which was put in place after the financial crisis in 2008. In June, the Fed outlined plans to taper purchases, with experts circling September as the start date of the reduction. This would involve the Fed tapering the purchases of Treasury bonds and mortgage securities, with an initial taper likely of $10 billion/month. Analysts expect the taper to begin in September, so we could see the Fed make reference to this in the July statement.

Pound Edges Higher as British Preliminary GDP Matches Forecast

GBP/USD has posted slight gains in Wednesday trade. In the North American session, the pair is trading at 1.3050, up 0.19% on the day. On the release front, British Preliminary GDP edged up to 0.3% in the second quarter, matching the forecast. In the US, New Home Sales remained steady at 610 thousand, short of the estimate of 615 thousand. Later in the day, the Federal Reserve releases its rate statement and is expected to maintain the benchmark at 1.25%. On Thursday, the US will release two key indicators – Unemployment Claims and Core Durable Goods Orders.

There were no surprises from British Preliminary GDP in the second quarter, which gained 0.3%, compared to 0.2% in the first quarter. This follows first quarter growth of 0.3%. Government statisticians are saying that the economy experienced a "notable slowdown" in the first half of 2017. Although the services sector expanded by 0.5% in the quarter, construction declined 0.9% and manufacturing dropped 0.4%. The soft numbers have dampened expectations for a rate hike from the Bank of England. Policymakers have engaged in a public debate about rate policy, but a second straight quarter of low growth will be ammunition for those policymakers who are against a rate hike before 2018. Although economic expansion remains weak, inflation levels are higher than the BoE would like, courtesy of a weak British pound. The currency's woes have also hurt the British consumer, who has seen her purchasing power reduced.

The Federal Reserve will be in the spotlight later on Wednesday, as it concludes its monthly policy meeting and releases a rate statement. The Fed is not expected to alter its interest rate policy, but the rate statement could still be a market-mover. The rate statement will be under careful scrutiny, as analysts will be looking for any references to the "I" word. Inflation continues to hover around 1.4% (based on the Fed's calculations), well below the Fed target of 2%. In June, Janet Yellen described low inflation as "transitory", but recent comments from Yellen and other policymakers have shifted in tone, an apparent acknowledgment that inflation may remain stuck at low levels. This has raised doubts as to whether the Fed will indeed raise rates one more time this year. No move is expected before December, and the odds of a December hike have fallen to just 37%, according to the CME Group. If today's rate statement fails to reassure the markets that a December hike is planned, investors could respond by selling dollar-denominated assets in favor of other currencies or gold.

Another key issue on the Fed's agenda is when to begin tapering the Fed's $4.2 trillion bond portfolio. The bloated balance sheet is a result of the aggressive quantitative easing program which was put in place after the financial crisis in 2008. In June, the Fed outlined plans to taper purchases, with experts circling September as the start date of the reduction. This would involve the Fed tapering the purchases of Treasury bonds and mortgage securities, with an initial taper likely of $10 billion/month. Analysts expect the taper to begin in September, so we could see the Fed make reference to this in the July statement.

U.K. Mid-Year Economic Outlook

Executive Summary

Economic growth in the United Kingdom remained modest in Q2, growing at a 1.2 percent annualized rate over the quarter. Monthly data suggest that a deceleration in consumer spending has played a role in the downshift in the British economy as rising inflation and stagnant wage growth have taken a bite out of household purchasing power. This combination of rising inflation, sluggish wage growth and tepid economic activity has put the Bank of England (BoE) in a bit of a bind. Although five members voted to keep Bank Rate unchanged at 0.25 percent at the last policy meeting on June 14, three members voted to hike rates by 25 bps at that meeting. We believe that the views of the majority will continue to prevail, and that policymakers at the BoE will refrain from raising rates through at least the end of 2017 as inflationary pressures from weak sterling begin to subside. Looking ahead, we forecast that real GDP growth will strengthen modestly in 2018 as some of the forces that have led to a slowdown this year reverse, although uncertainty related to Brexit continues to lurk in the background as a major downside risk to the economy.

Economic Growth Trudges Along in Q2

The 1.2 percent annualized growth rate in Q2 matched expectations (Figure 1). The data are preliminary and could be subsequently revised. Moreover, a breakdown of the overall GDP data into its underlying demand components will not be released until next month. In general, the 1.7 percent year-over-year growth rate that was registered in the second quarter indicates that the underlying pace of economic growth in the United Kingdom is only modest at present.

As noted above, a detailed breakdown of the Q2 GDP data into its underlying demand components is not yet available. Service industries accounted for all of the growth, while production-oriented industries such as manufacturing and construction contracted in the quarter.

In addition, monthly data suggest that a deceleration in consumer spending has played a role in the downshift that is underway in the British economy. Yes, real retail sales grew 1.5 percent (not annualized) on a sequential basis in the second quarter. On a year-over-year basis, however, real retail spending was up only 2.6 percent in Q2, which clearly represents a slowdown relative to the breakneck pace of the past few years (Figure 2).

This ratcheting back in the pace of consumer spending reflects a combination of two factors. First, although the unemployment rate has dropped to only 4.5 percent, the lowest rate in more than 40 years, wage growth in the United Kingdom remains painfully slow (Figure 3). At the same time, CPI inflation has shot higher due, at least in part, to the marked depreciation of sterling in the wake of last year's Brexit referendum (Figure 4). The combination of slow wage growth and higher inflation means that growth in real disposable income (i.e., purchasing power) has taken a hit. With the household savings rate at an all-time low of only 1.7 percent of disposable income, consumers have needed to reduce spending growth due to slower growth in real income.

Bank of England Likely To Remain on Hold

The surge in the overall rate of CPI inflation in the past year or so presents a conundrum to policymakers at the Bank of England (BoE). The British government tasks the BoE with maintaining an inflation rate of two percent over the medium term. With CPI inflation well above the BoE's target at present, some members of the Monetary Policy Committee (MPC) have felt compelled to tighten policy. Although five members voted to keep Bank Rate unchanged at 0.25 percent at the last policy meeting on June 14, three members voted to hike rates by 25 bps at that meeting. The next policy meeting is scheduled for August 3.

We believe that the views of the majority will continue to prevail, and that the MPC will refrain from raising rates through at least the end of 2017. As noted above, the depreciation of sterling—it weakened 20 percent on a trade-weighted basis between late 2015 and late 2016 (Figure 5)— helped to push CPI inflation higher. However, the trade-weighted value of sterling has largely moved sideways over the past few months, and we expect it to remain more or less stable in coming months. Therefore, the inflationary impulses hitting the economy from higher import prices should start to dissipate. The recent decline in energy prices should also help to reduce inflation. Although the overall CPI inflation rate could very well drift higher over the next month or two, we look for it to recede later this year as disinflationary forces come to the fore. Meanwhile, although we forecast that real GDP growth in the United Kingdom will firm somewhat, the pace of growth will generally remain lackluster through the end of the year (Figure 6). In our view, the combination of receding inflation and sluggish GDP growth should stay the MPC's hand for the remainder of the year.

We look for real GDP growth to strengthen modestly in 2018 as some of the forces that have led to a slowdown this year reverse. Namely, the decline in the CPI inflation rate that we forecast should help to boost growth in real disposable income again, which should translate into stronger growth in consumer spending. Stronger growth in the global economy, especially in the Eurozone, to which the United Kingdom sends 40 percent of its exports, should also contribute positively to real GDP growth. In that regard, the volume of British exports was up more than 7 percent in the first two months of Q2 relative to the same period in 2016. As the economic outlook improves, we look for the MPC to hike rates in late spring/early summer 2018. That said, any tightening that the MPC should undertake likely will remain gradual. We also expect that the MPC will maintain the size of its quantitative easing program at £445 billion (£435 billion government bonds plus £10 billion corporate bonds) through at least the end of 2018.

Brexit: The Elephant in the Room

The United Kingdom has built extensive economic and financial ties with other European Union (EU) countries over the past 44 years during which it has been an EU member. Exports to and imports from the other EU members accounts for one-half of British trade, and those countries own one-half of the directly invested capital in the United Kingdom. London has become the unquestioned financial capital of Europe.

But the decision by the United Kingdom to leave the EU means that new relationships governing these economic and financial ties must now be renegotiated by March 2019, and there is considerable uncertainty regarding the ultimate configuration of these new relationships. Will goods and services continue to be traded freely between the United Kingdom and other EU members after 2019? Will citizens of other EU countries be allowed to live and work in the United Kingdom after it leaves the EU? Will the unfettered access to European financial markets that the EU "passport" gives to London-based financial institutions continue? At this time, nobody knows the answers to these and myriad other questions regarding the Brexit process.

This uncertainty appears to be affecting investment spending in the United Kingdom. Survey data that measure investment intentions, which tend to be highly correlated with actual investment spending, weakened throughout 2016 (Figure 7). Investment intentions have rebounded somewhat this year, but they generally remain low. Until some of the uncertainty regarding the Brexit process is cleared up, many businesses in the United Kingdom may adopt a wait-and-see attitude regarding investment spending. We do not believe the uncertainty is enough to derail the current economic expansion in the British economy, but we freely acknowledge the risk that the economy weakens significantly more than we and other forecasters anticipate. Stay tuned.

Conclusion

Economic growth in the United Kingdom has slowed from its cycle-high reached in 2014, but the deceleration has not been as sharp as originally feared in the wake of Brexit. That said, production in investment-oriented sectors of the economy remains soft, and consumer spending has begun to suffer amid wages that have struggled to maintain their purchasing power. The recent stabilization of the sterling should help relieve some of the inflationary pressure caused by imports, and stronger growth in the global economy, especially in the Eurozone, should also contribute positively to real GDP growth. This in turn should keep the policymakers at the BoE on hold through at least the end of 2017. As such, we look for a modest strengthening in the U.K. economy over the next 18 months. The ongoing negotiations related to Brexit will likely continue to loom over the U.K. economy over the next few years, representing a major downside risk moving at a glacial pace.