Sample Category Title

Euro Treading Water as ECB Draghi Awaited, Yen Steady after BoJ

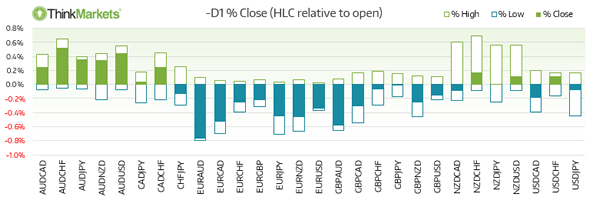

Dollar recovers in general today as markets turned into consolidation mode. Euro is treading water while markets await ECB rate decision and press conference. Traders would be eager to hear how ECB President Mario Draghi would clarify his comments in the past few weeks. Or Draghi will just let markets' perceived ECB hawkishness be an assumed base case. Meanwhile, Yen is steady as BoJ delivered what are expected, keeping policies unchanged, raising growth forecast and lowering inflation forecast. Aussie was lifted briefly by solid job data but quickly retreated.

BoJ left policies unchanged, raised growth forecast, cut inflation projections

BoJ left monetary policies unchanged as widely expected. Short term policy interest rate was held at -0.1%. The central bank also maintained the annual pace of asset purchase at JPY 80T to keep 10 year JGB yield at around 0%. Meanwhile, BoJ noted in the quarterly report that "recent price developments have been relatively weak, as companies remained cautious in raising wages and prices." And, "risks to the economy and price outlook are skewed to the downside." Also as widely expected, BoJ lowered inflation projections and raised growth projections. The timing for meeting 2% inflation target is pushed back for the sixth time. BoJ now expects inflation to hit target in the fiscal year ending March 2020. Here is a summary of the revisions.

For fiscal 2017:

- Core inflation is projected at 1.1%, down from prior forecast of 1.4%

- GDP growth is projected at 1.8%; up from prior forecast of 1.6%

For fiscal 2018:

- Core inflation is projected at 1.5%, down from prior forecast of 1.7%

- GDP growth is projected at 1.4%; up from prior forecast of 1.3%

For fiscal 2019:

- Core inflation is projected at 1.8%, down from prior forecast of 1.9%

- GDP growth is projected at 0.7%; unchanged from prior forecast of 0.7%

Also from Japan, trade surplus narrowed to JPY 0.08T in June. All industry activity index dropped -0.9% mom in May.

Aussie enjoyed brief lift by solid job data

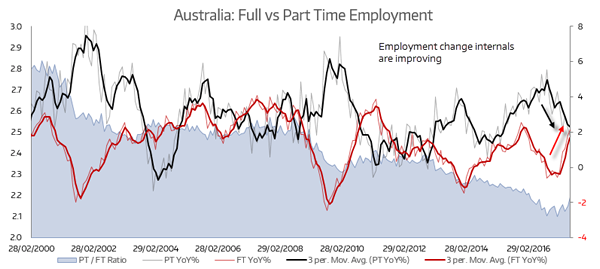

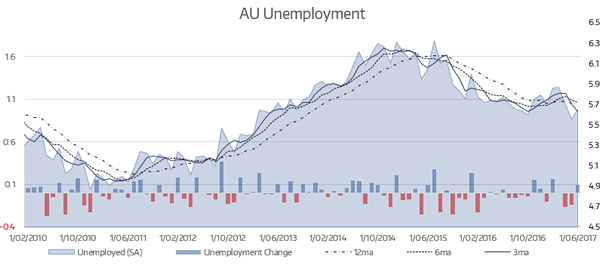

Aussie is lifted earlier today by solid job data but is seen losing momentum. Headline job data showed 14k growth in June, slightly below expectation of 15k. Prior month's figure was revised down from 42k to 38k. Unemployment rate was unchanged at 5.6%. Looking at the details, full-time jobs rose 62k while partly offset by -48k fall in part-time jobs. Australia NAB business confidence was unchanged at 7 in Q2.

Aussie jumped sharply this week as RBA noted that the neutral nominal rate is now at 3.5%. But with reduction in risk aversion and/or increase in trend growth rate, the neutral real interest rate could rise back from current 1.0% to 1.5%. And that indirectly implies that the neutral nominal rate could also follow and rise. Australia Prime Minister Malcolm Turnbull tried to calm the market and said that RBA is only "sending a signal, which is probably prudent, which is to say ... rates are more likely to go up than go down."

Euro cautious ahead of ECB

Euro is trading mixed as markets are awaiting ECB rate decision and press conference. The central bank is widely expected to keep policies unchanged today. The common currency was shot up in late June after ECB President Mario Draghi's upbeat comments on the economy and receding political risks. Draghi further noted that renewed reflationary forces could now give room for "adjustment of parameters" of the current stimulus program. There are speculations that ECB could announce tapering of some sort in the September meeting, or by latest in October. But in any case, today's press conference will give Draghi a chance to clarify if the markets have misjudged him. Without any clarifications, market will take the assumption of tapering in 2018 as a assumption and that could provide additional lift to the Euro.

Elsewhere

UK retail sales will be a focus in European session today. Germany will release PPI. Swiss will release trade balance. from US, jobless claims, Philly Fed survey and leading indicators will be featured.

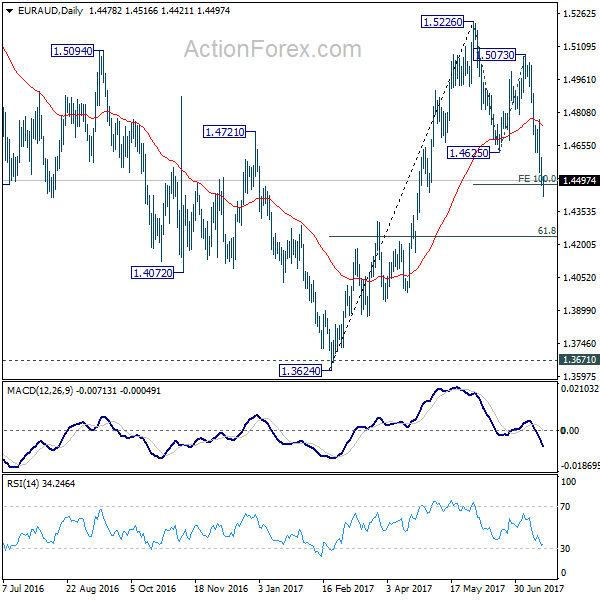

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4432; (P) 1.4518; (R1) 1.4563; More...

EUR/AUD drops to as low as 1.4421 so far today and met 100% projection of 1.5226 to 1.4625 from 1.4472. The cross quickly recovered. But for the moment, with 1.4617 minor resistance intact, intraday bias remains on the downside. Firm break of 1.4472 will pave the way to larger fibonacci level at 61.8% retracement of 1.3624 to 1.5226 at 1.4236. Meanwhile, above 1.4617 will indicate short term bottoming and turn bias back to the upside for 55 day EMA (now at 1.4744).

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. But we will monitor the structure of the decline from 1.5226 to adjust our view. Above 1.5226 will target a test on 1.6587 key resistance. However, further downside acceleration will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| JPY | BOJ Monetary Policy Statement | |||||

| 23:50 | JPY | Trade Balance (JPY) Jun | 0.08T | 0.12T | 0.13T | 0.12T |

| 1:30 | AUD | NAB Business Confidence Q2 | 7 | 6 | 7 | |

| 1:30 | AUD | Employment Change Jun | 14.0k | 15.0k | 42.0k | 38.0k |

| 1:30 | AUD | Unemployment Rate Jun | 5.60% | 5.60% | 5.50% | 5.60% |

| 4:30 | JPY | All Industry Activity Index M/M May | -0.90% | -0.80% | 2.10% | 2.30% |

| 6:00 | CHF | Trade Balance (CHF) Jun | 2.89B | 3.40B | ||

| 6:00 | EUR | German PPI M/M Jun | -0.10% | -0.20% | ||

| 6:00 | EUR | German PPI Y/Y Jun | 2.30% | 2.80% | ||

| 8:00 | EUR | Eurozone Current Account (EUR) May | 23.3B | 22.2B | ||

| 8:30 | GBP | Retail Sales M/M Jun | 0.30% | -1.20% | ||

| 11:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | ||

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | USD | Initial Jobless Claims (JUL 15) | 245K | 247K | ||

| 12:30 | USD | Philly Fed Manufacturing Jul | 23.7 | 27.6 | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jul A | -1.1 | -1.3 | ||

| 14:00 | USD | Leading Indicators Jun | 0.40% | 0.30% | ||

| 14:30 | USD | Natural Gas Storage | 57B |

Euro Weakens Ahead Of ECB Meeting, BoJ And AU Employment In Focus

BoJ meeting, trade data and AU employment make the bulk of Asia data where attention will then shift to tonight's ECB meeting.

The Euro weakened overnight as traders booked profits ahead of today's ECB meeting. The confusion following Draghi's seemingly hawkish speech last month the ECB may use today's meeting to tweak their message to calm the markets. Draghi sent the Euro above 113 at the end of June and ECB officials attempt to tame the run came to little avail as the Euro stopped just shy of 116 overnight. So they may use today's meeting to tweak the message again and take the fun ot of the rally.

EURAUD remains out preferred Euro short as sentiment on AUD remains strong, it is the strongest G10 performer this year whilst Euro faces further profit taking over the near-term. AU employment is expected to soften slightly but unless it throws a curve-ball then AU should remain supported. If there is any concern to the AUD rally it may come from Guy Debelle's speech tomorrow as the temptation to jawbone AUD may now be on his agenda.

The positive sentiment surrounding AUD is likely to help AUDJPY on its way to Y90 following today's BoJ meeting. No major changes are expected on the policy front but a downgraded inflation outlook is viable. With household spending, wage growth CPI all disappointing, it is hard to justify their inflation forecast let alone a 2% target. Large speculators have also piled into Yen shorts in recent weeks whilst bulls remain on the sideline, making Yen the preferred short over the coming weeks.

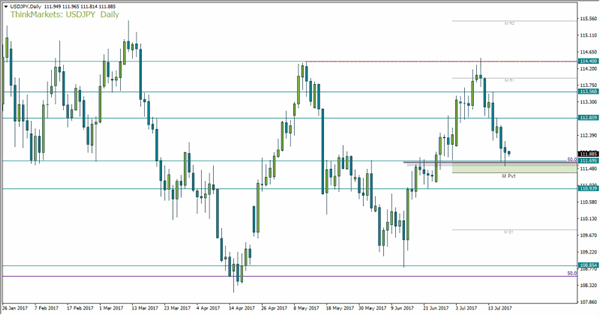

US data bucked the trend by beating forecasts overnight, seeing an improvement in building permits and housing starts. It helped slow the bleeding on the US Dollar index, although the weaker Euro probably provided the bulk of support. USDJPY found support at 111.55 and focus now switches to the BoJ meeting where a corrective rally is expected. The healthcare plan disappointment is largely priced in and Yen outflows are likely to persist as traders are currently net short the Yen by US$12.3bn (as of last week's CFTC report).

The monthly pivot and 50% retracement provide a broad zone up support between 111.37 – 111.68, with yesterday's bullish hammer respecting the upper part of the zone. If we are to see a break of yesterdays low, as long as we remain above the monthly pivot then we do see potential for an eventual upside move so. Bearish momentum on the lower timeframes is waning and the downside appears stretched.

AU Employment Sends AU Close To 80

Close to 80 but no cigar, yet. Markets perceived the employment set to be a net positive to promptly bid AUD higher, only to book profit just shy of the milestone

AUD extended gains as employment was seen as a net positive. As there was an expectation for employment to soften slightly, the realisation of the fact came as no surprise. Unemployment ticked higher to 5.6% as expected and employment change increased by +14k verses +15k expected (down from 38k prior). The higher participation rate took the edge off of the slightly higher unemployment rate, which we expect to soften over the coming months as capacity utilisation continues to increase.

Part-time employment weighed heavily on total jobs number yet full-time employment increased by 62k, allowing markets to see the a healthier underlying employment change other than the 14k presented.

AUDUSD stopped just shy of 80c although we'd be surprised if this key, psychological level broke upon first attempt as temptation to book a quick profit may be high. But unless we hear a verbal intervention of some sorts, we should be above 80c soon enough. Volatility is something to also note as the past two weeks are already bordering on an outlier. Last week's close was its most bullish week since Feb and if you look across the percentage changes, you'll see that volatile weeks are not exceeded and, often, the subsequent week's range is sanguine. As this occurs below the 80c level and the risk of verbal intervention is potentially rising, this may pour water on volatility for the bulls. However, a break above 80c is a milestone worthy of seeking bullish setups on lower timeframes (intraday) if you remember the volatility potential theoretically goes down the higher we trade.

RBA Assistant Governor Guy Debelle speaks tomorrow and traders are on guard for a potential jawbone. With sentiment and technicals on AUD remaining very much bullish we have moved beyond levels which have previously warranted a verbal intervention of some sort. Throughout 2016 the statement included “An appreciating exchange rate could complicate' the economic adjustment when AUD traded between 0.732-0.77. In 2017 this was switched from 'could complicate' to 'would complicate' for the same range, yet AUD now trades just shy of 0.80. The last time AUD traded at these levels was in 2015 when the language used within the statement was quite bluntly 'further depreciation is likely / necessary'.

Focus now shifts to the BoJ meeting where we think AUDJPY is headed for Y90. Yen outflows are likely to persist over the coming weeks and a lower inflation outlook from BoJ should help support carry trades.

In some ways is it not fair to directly compare the levels over time as the economic background has changed over this period. Yet it has not improved to the point where AUD will be comfortable with a higher AUD. In the backdrop of a weaker USD whilst the Fed find data hard to truly justify another hike, it may also be the RBA's perception of this extra hike as to whether they try to publicly talk AUD down between meetings. If they were banking on the Fed to hike and effectively remove the 25bps positive carry AUDUSD currently has, then there is good reason to expect verbal intervention at some point. Tomorrow may just be that day.

Market Morning Briefing: All Eyes Are Fixed On The BOJ Policy Meet In The Morning

STOCKS

Stocks have resumed their uptrend and could possibly face some interim dips within an overall uptrend. Some clarity is needed in Dax which is trading at crucial levels just now.

Dow (21640.75, +0.31%) has bounced back from levels near 21470 and is trading above 21600 just now. Upward momentum looks strong and we could possibly see arise towards 21800 in the coming sessions. Near term trend is firmly up.

Dax (12452.05, +0.17%) is almost stable and is holding above the immediate support near 12400. If the support holds, the price index could further towards 12500-12600. Failure to sustain above 12400 would shift our focus to levels near 12300 or lower. Need to wait and watch.

Shanghai (3237.48, +0.20%) has risen sharply in the last 3-sessions and is heading towards immediate channel resistance near 3250-3260. From there a short correction is possible before resumption of the uptrend. Near term looks firmly bullish.

Nikkei (20092.14, +0.36%) has started to rise from levels near 19950. It could continue to move up towards 20200-20300 in the coming sessions. This could possibly pull up Dollar-Yen also to higher levels in the next few sessions.

Nifty (9899.60, +0.74%) could limit its near term dip at 9800 and could be headed towards 10000 in the coming sessions. Near term looks strongly bullish.

COMMODITIES

Gold (1238) and Silver (16.21) are still trading above their crucial support at 1231 and 16.20 respectively. A break above 1245 is necessary for gold to remain bullish towards 1260 for the near term else a fall below 1230 could take it lower towards 1220. Silver is trading within the range of 16.20-16.50 and only a close above 16.50 could negate our midterm bearish view. As dollar index is highly oversold, it will be difficult for Bullion to maintain this short term bullish momentum. At the same time market is waiting for today’s ECB press conference, at 6:00 pm IST.

Muted price action had been seen in Copper (2.71) for last couple of trading sessions. It is trading within a range of 2.66-78. Only above 2.78, higher resistances of 2.80 can come into consideration. In the medium term 2.55-57 are going to be a strong support and we will remain bullish while it is trading above those levels.

Both Brent (49.66) and WTI (47.28) moved upward as U.S weekly crude inventory data (actual -4.7M B) was highly supportive for the entire energy pack. This is the 4th consecutive week of shortage in weekly U.S crude inventory. We will remain bullish while Brent and WTI are trading above 48.80 and 46.70 on a weekly closing basis. Immediate trading range for Brent and WTI could be 48-52 and 46-50 respectively.

FOREX

All eyes are fixed on the BOJ policy meet in the morning and the ECB meet in the afternoon. Till then, no activity in the markets is expected.

Dollar-Yen (111.97) is being watched for the reaction after the BOJ policy decision due in a few minutes today. We expect the support of 111.00 to be tested before any major short covering emerges.

Then comes the ECB policy decision which may affect Euro (1.1525) which has been trading quietly for the last 2 sessions. Repeat - The trend remains firmly up but it must be noted that the net position in Euro is the largest since 2011 and any surprise from the central bank or any other corner may trigger a very sharp correction. Similarly, the Dollar Index (94.84) may have attracted too many shorts. These two crowded trades may invite nasty surprises eventually as the previous historical instances show. Therefore high caution warranted at the current levels this week.

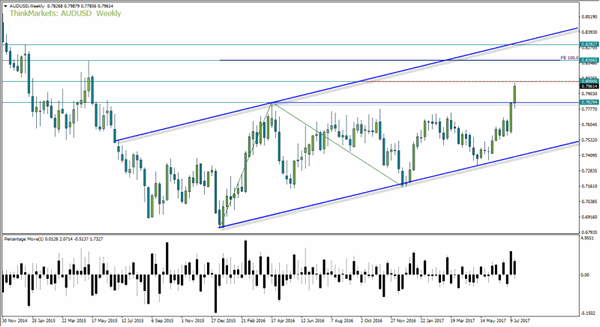

Aussie (0.7940) has almost tested 0.80 levels with a high of 0.7990. While a couple of days of rest after the sharp rally can’t be ruled out, the larger target of 0.8150-75 remains unchanged and a break above 0.80 may provide more impetus.

Pound (1.3024) remains in a shallow corrective mode which is expected to be followed by another leg up towards 1.3125 and then 1.32-1.34 later.

Regarding Dollar-Rupee (64.29), the trend remains firmly down and but some short covering and fresh buying of Dollars can be expected near 64.20.

INTEREST RATES

The US yields have been coming off from channel resistances and could head to lower levels in the near term. The 30Yr (2.85%) could test 2.80% in the near term while the 10?Yr (2.27%) could come off towards 2.20/23%. Medium to long term looks bearish.

The German-US 2Yr (-2.00%) and the German-US 10YR (-1.73%) have dipped a bit but could rise back soon to rise towards -1.95% and -1.70% respectively. We wait for the ECB meeting today to see if that impacts the Euro and the yields.

The Japan yields could start moving higher in the coming sessions and looks bullish just now. This could possibly indicate that the Dollar-Yen may start moving up too in the coming sessions.

USD/JPY Trading In The Red, EUR/GBP Maintains A Bullish Bias, USD/CHF Downside Paused

USD/JPY trading in the red

Price continues the minor retreat and looks determined to take out some important support level in the upcoming days. Is pressuring three important support levels, remains to see if will have enough energy to breakdown.

Continues to move sideways on the short term, is trapped within an extended sideways movement, but I hope that we'll have a clear direction very soon.

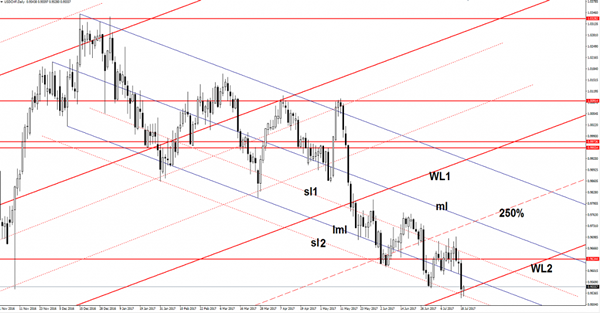

USD/JPY dropped below the 111.68 yesterday's low and reached the 111.54 level, stays lower even if the United States data have come in better in the afternoon. The US Building Permits surged to 1.25M in the previous month, from 1.17M, beating the 1.20M estimate and reached the highest level of the last 3-months. Moreover the Housing Starts jumped from 1.12M to 1.22M in June, exceeding the 1.16M estimate.

Price dropped and resumed the bearish momentum, but found temporary support at the 38.2% retracement level and at the 150% Fibonacci line (ascending dotted line). We have an important confluence area at the intersection between the 38.2% retracement level with the 150% Fibonacci line, a valid breakdown below this obstacle will accelerate the sell-off.

Is trapped between the 50% Fibonacci line and the 23.6% retracement level, we'll have a clear direction once the rate escapes from this range.

Right now we can't be certain that we have a valid breakdown below the black downtrend line, has slipped below this dynamic obstacle, but a further USDX's jump will invalidate the breakdown.

The current retreat was natural after the false breakout above the 23.6% retracement level and after the failure to reach the third warning line (wl3) of the former descending pitchfork. Technically was somehow expected to increase further as the behavior has changed when the rate started to make higher lows. A further increase will be confirmed only if the rate will jump and will stabilize above the wl3 and above the 23.6% retracement level.

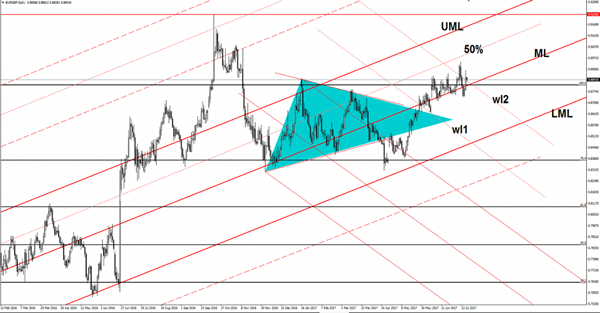

EUR/GBP maintains a bullish bias

EUR/GBP stays above a major support level, signalling that we may still have a bullish momentum in the upcoming days. Personally, I'm still waiting for a confirmation that will increase in further, we may have a great buying opportunity very soon because is located in a crucial area, remains to see the direction.

Is narrowing right above the 100% Fibonacci level and above the median line (ML) of the ascending pitchfork, a retest of the ML will bring us a great buying opportunity. The upside targets are at the 50% Fibonacci line (ascending dotted line) and higher at the median line (UML) of the ascending pitchfork, could find resistance also at the 0.9226 swing high.

However, a drop below the mentioned support levels will open the door for a decline towards the lower median line (LML).

USD/CHF downside paused

Price is fighting hard to recover after the yesterday's massive drop, we'll see if will have enough power to stay above the 0.9550 level. USD/CHF dropped below the second warning line (WL2) of the ascending pitchfork. Looks like that we had another false breakdown below the outside sliding parallel line (sl2), a retest of the WL2 will signal a reversal on the short term.

USDJPY – Weakens Further With Eyes On 111.00 Zone

USDJPY - The pair continues to hold on to its downside pressure closing lower on Wednesday and opening the door for more declines. On the downside, support comes in at the 111.50 level where a break if seen will aim at the 111.00 level. A cut through here will turn focus to the 110.50 level and possibly lower towards the 110.00 level. On the upside, resistance resides at the 112.50 level. Further out, we envisage a possible move towards the 112.00 level. Further out, resistance resides at the 111.50 level with a turn above here aiming at the 111.00 level. On the whole, USDJPY looks to pullback further in the days ahead.

Event Risk Overload

Event risk overload

There hasn't been much progress in the currency markets overnight as both US yield, and the US dollar continues to struggle. And for the time being, equity markets continue to be cheered by improving earnings.

Dealers remain in cautionary wait and see mode ahead today's high-risk events that lay in waiting.The focus today should be on the ECB, BoJ and Australian Employment data.It's been somewhat directionless trading as both USDJPY and EURUSD moderated on the back of profit-taking while AUDUSD carries on higher into the local jobs data.

But President Trump's Administration is worth keeping an eye on as the political quagmire thickens

Australian Dollar

Still waiting for the dust to settle on this trade as the Aussie is holding firm above 0.7950 after breaching the top of the two-year range earlier in the week There been very little retracement as dealers position to continued improvements in the domestic labour market.

AS we approach the A$ 80 level, it suggests we're beyond the fear of missing out on a policy shift trade. And while we can argue till blue in the face this move is overdone the reality is the Aussie is in demand.

Equity markets are getting cheered on from every level, and the steady beat of the Chinese economy has seen Iron ore prices rising.Also, the rally in WTI spurred on by a larger than expected drop in crude oil inventories is helping sentiment across the commodity block this morning and with implied volatility dropping there definitely some yield appeal for Aussie assets.

Australian Jobs Data

The Australian Jobs data just missed estimates, but this is robust enough to push the Aussie dollar higher with the full-time employment change greater than expected. On cue, Australia 3-year yield is trading at the highest since Dec 2015, following full-time employment change

The Aussie is stalling after the initial move suggesting some initial profit taking setting. Regardless the A$ continues with its gravity defying act, and push through A$80 is likely in the cards.

Euro

Despite the mild pullback on profit taking t, which was expected ahead of today's ECB, the trend remains intact. And while there probably a greater chance the ECB will disappoint as opposed to affirm the markets hawkish conviction, but even then, the Euro should continue to be a buy on dip given the US dollar weakness, and the market is looking to September for the key policy shift.The one concern into the ECB is market positioning which needless to say is long so if there is very dovish surprise the short term longs will run for the exits, and it could get messy for a while.

Japanese Yen

The BoJ is unlikely to move markets much on Thursday although it is expected to upgrade the economic assessment more or less. Sources on Tuesday discussed the possibility of CPI estimates being reduced and while unlikely it's still a risk

The USDJPY is more about the crowded EURJPY positioning, so a move lower in EUR on the ECB could see a sudden unwind of EURJPY and drive the USDJPY lower.

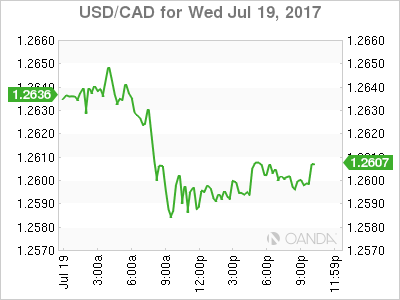

USD/CAD Canadian Dollar Rises After Oil Price Bounce

The Canadian dollar appreciated on Wednesday versus the US dollar. The Canadian currency got a boost from strong manufacturing sales, oil prices gaining on larger than expected drawdowns in the US and the cloud of uncertainty surrounding the healthcare Act in Washington.

US Trade Representative Robert Lighthizer has announced the NAFTA renegotiation talks will begin on August 16 to 20 in Washington. Both Canada and Mexico issued positive statements on the plans and look forward to modernizing the agreement. Presidential elections in Mexico and the US midterm elections in 2018 are incentives for the negotiations to take place as soon as possible and with a speedy outcome.

The USD/CAD lost 0.207 in the last 24 hours. The loonie rose against the US dollar as oil prices rose with a bigger than expected drawdown in the US and the continuing saga of political uncertainty surrounding healthcare reform in Washington. The currency pair is trading at 1.2594 breaking below the 1.26 with the help of oil prices.

Canadian manufacturing sales rose 1.1 percent in May. Auto sales drove the record high sales beating expectations of 0.8 percent increase. The Canadian economy is keeping pace with growth expectations that lead the Bank of Canada (BoC) to raise its benchmark interest rate for the first time in 7 years. The benchmark was hiked 25 basis points to 0.75 percent with another rate raise expected for later this year if growth marches on. Canadian retail sales and inflation data due this Friday will add more arguments for monetary policy.

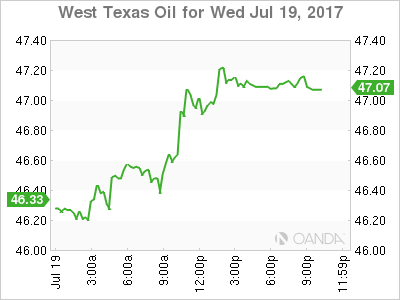

Energy prices surged 2.146 percent on Wednesday. The price of West Texas Intermediate is trading at $47.22 after the release of the Energy Information Administration (EIA) weekly US crude inventories showed a larger drawdown than he market expected. Crude stocks fell by 4.7 million barrels last week, the third time in as many weeks that drops in inventory are higher than forecasted. Gasoline and distillate inventories also had losses bigger than anticipated pushing the price of energy higher.

US production has increased which makes the shrinking inventories more puzzling without signs of demand growth. The Organization of the Petroleum Exporting Countries (OPEC) and other major exporters agreement to cut production has stabilized prices, but American shale producers have taken advantage and ramped up their operations.

The meeting between OPEC and Russia to discuss compliance later this month will open the door for the next steps for energy producers. A bigger cut in production after the agreed extension is in the cards, but there are some voice of dissent as current levels are causing distress for countries who depend on oil sales to balance their budget.

Ecuador is the latest OPEC member to disclose a smaller than agreed to levels of production. Oil minister Carlos Perez said that there is an unwritten agreement within the OPEC to allow “flexibility” to smaller producers. Nigeria and Libya were excluded from the agreement after suffering disruptions to their productions but are now close to normal levels so there is talk that they could be brought into the fold, which could prove difficult if other nations are not holding up their production quotas.

Market events to watch this week:

Wednesday, July 19

9:30 pm AUD Employment Change

Tentative JPY Monetary Policy Statement

Thursday, July 20

Tentative JPY BOJ Outlook Report

Tentative JPY BOJ Policy Rate

2:30 am JPY BOJ Press Conference

4:30 am GBP Retail Sales m/m

7:45 am EUR Minimum Bid Rate

8:30 am EUR ECB Press Conference

8:30 am USD Unemployment Claims

Friday, July 21

8:30 am CAD CPI m/m

8:30 am CAD Core Retail Sales m/m

Will the ECB and BoJ Have Any Surprises in Store?

The last month has seen G7 central banks re-emerge as the dominant driver of financial market volatility with policy makers becoming increasingly uncomfortable with the direction of travel, at least in most cases.

All of a sudden the Federal Reserve appears to be questioning the need to raise interest rates so quickly, the Bank of England is considering tightening as it's more worried about inflation than the economy and the Bank of Canada has already raised interest rates despite falling well short of its inflation target.

Two central banks that have so far continued to operate with some predictability are the ECB and the Bank of Japan, both of which are due to announce their latest monetary policy decisions on Thursday. Can we still rely on them not to have the sudden change of heart that their peers have had?

BoJ Refusing to Fall in Line With Other Central Banks

Given the shift that we've seen in recent weeks, it's difficult to say with any degree of certainty but of all the above, I think the BoJ and ECB may be the two that will follow a more predictable path (famous last words).

The BoJ has shown no desire to deviate from its ultra-accommodative stance, in fact it recently increased its bond purchases because the yield on 10-year JGBs was ticking higher, driven by similar moves elsewhere. With the central bank vowing to keep the 10-year yield around 0%, the move was a signal to markets that it is not in the same camp as a number of its peers. With that in mind and considering inflation remains far from target, I don't expect any sudden shifts on Thursday.

Source - Thomson Reuters Eikon

The ECB could be more interesting though, with the asset purchase program in its current form - €60 billion per month - due to expire at the end of the year. While the central bank will likely wait until September to announce how the program will be extended, it may use this month's press conference - being the last before September - to lay the groundwork for such an announcement.

We may therefore get some insight into what the central bank is considering doing next. For example, will it lay out plans to phase out asset purchases over a certain period of time? Or will it simply announce another short extension while reducing the size of the program, as it did in December, while insisting it is not tapering? We may get some insight into this on Thursday.

Of course, there is always the possibility that it simply extends the program as it is, although this appears the least likely option, which it may allude to.

Will Dovish Draghi Throw a Spanner in the Works?

Whatever the central bank does, these events often stir up some volatility in the markets, particularly in the euro and eurozone bonds. And in the current environment, these may be particularly vulnerable to any unexpected suggestions, intentional or otherwise.

With the euro trading near the highs of the last two and a half years against the dollar, it's potentially looking a little overstretched which could leave it vulnerable to a dovish surprise from ECB President Mario Draghi.

The flip side of this of this, of course, is that a more hawkish message could trigger a move through this major resistance which in turn could be very bullish for the pair. Clearly we're in for a very interesting end to the year for markets and the ECB could well be at the centre of it all.

Gold Pauses After Gaining on Trump Troubles

Gold is showing little movement in the Wednesday session. In the North American session, spot gold is trading at $1241.66. On the release front, Building Permits climbed to 1.25 million, beating the estimate of 1.20 million. Housing Starts improved to 1.22 million, above the forecast of 1.16 million.

US housing numbers have been mixed in recent months, but Tuesday's releases pointed to a strengthening housing sector. Building Permits improved to 1.25 million in June, up from 1.17 million a month earlier. Housing Starts jumped to 1.22 million, up sharply from 1.09 in the May report. The solid numbers will give a boost to second quarter numbers. US Advance GDP will be released next week, and the markets don't want to see a repeat of the first quarter reading, which missed expectations with a gain of just 0.7%.

Gold has been moving higher, gaining 2.1% since Friday. The metal moved higher after CPI and retail sales disappointed, and the rally has continued this week. The dollar lost ground after President Trump suffered a major defeat on Capitol Hill on Tuesday, and gold responded with gains of 0.08%. Political risk in the US has reduced investor appetite for risk and boosted gold prices.

President Trump hasn't done very well at learning how to tango with Congress, and this week's debacle on Capitol Hill could make the gap between Trump and Republican lawmakers even harder to bridge. Trump had vowed to replace Obamacare, but his health care bill has stalled in the Senate before lawmakers even had a chance to vote on the proposal. With some conservative Republicans coming out against the bill, it's questionable if the Republicans can pass another version before Congress takes a recess in August. Trump had promised to pass a health care before the summer break, so his credibility will take another hit if he's unable to do so. Trump has been in office for six months, but has been unable to get Congress to pass any significant bills, even though the Republicans enjoy a majority in both houses of Congress. With this latest setback, there is growing skepticism as to whether Trump will be able to convince Congress to pass other key parts of his agenda – tax reform and fiscal spending. This paralysis on Capitol Hill has deepened investor pessimism about Trump's legislative agenda and is weighing on the US dollar.