Sample Category Title

Lack of Data Leaves Pound Unchanged, UK Retail Sales Next

GBP/USD is subdued on Wednesday, and is unchanged on the day. In the North American session, the pair is trading at 1.3040. In economic news, there are no British events on the schedule. In the US, housing numbers were sharp, as Building Permits and Housing Starts improved in June and beat expectations. On Thursday, the UK will release retail sales, and the US will publish unemployment claims and the Philly Fed Manufacturing Index.

British CPI has been gaining strength, but the indicator slowed to 2.6% in June, down from 2.9% in May. This was considerably lower than the estimate of 2.9% and the first time in 2017 that inflation levels have not increased from the previous reading. The soft data eases the pressure on the BoE to raise rates in order to curb high inflation levels. Policymakers at the BoE have been at odds over raising rates – even though inflation is high, the economy has been showing signs of weakness, raising concerns that the economy does not need higher interest rates. On Tuesday, BoE Governor Mark Carney said that the main factor behind high inflation was the fall in the pound, which has dropped sharply since the Brexit vote in June 2016. The BoE hold its next policy meeting on August 4, and analysts expect the policymakers to hold the benchmark rate at 0.25%, where it has been pegged since August 2016.

Britain and European Union negotiators met in Brussels on Monday, marking the start of substantive negotiations on Britain's exit from the EU. After weeks of "discussions about what to discuss", the UK agreed to the European demand that the negotiations would focus on the rights of EU citizens in the UK and Britain's bill for leaving the EU, before entering talks on a new trade agreement. Britain has presented its position on guaranteed rights for EU citizens living in the UK, but EU negotiators have said that this offer doesn't go far enough. The EU has handed Britain an exit bill of EUR 69 billion, and although the May government has agreed that it owes funds to Brussels, it certainly will counter with a much lower figure. With significant gaps between the parties on both of these issues, the negotiations promise to be difficult. Another complication is internal dissent within the May government, with senior officials at odds over a 'transition period' for Britain after leaving Brexit. Finance Minister Philip Hammond has suggested a transition period of two years, but Brexit Secretary David Davis has said he wants the UK completely out of the single market when Brexit negotiations terminate in March 2019.

Yen Hits 3-Week High, BOJ Meeting Looms

The US dollar remains under pressure, as USD/JPY has posted gains for a second straight day. In Wednesday's North American session, USD/JPY is trading at 111.70, down 0.31% on the day. On the release front, there are no Japanese data releases, but the markets will be paying close attention to the BoJ rate statement. In the US, there was positive news from the housing sector. Building Permits climbed to 1.25 million, beating the estimate of 1.20 million. Housing Starts improved to 1.22 million, above the forecast of 1.16 million.

US housing numbers have been mixed in recent months, but Tuesday's releases pointed to a strengthening housing sector. Building Permits improved to 1.25 million in June, up from 1.17 million a month earlier. Housing Starts jumped to 1.22 million, up sharply from 1.09 in the May report. The solid numbers will give a boost to second quarter numbers. US Advance GDP will be released next week, and the markets don't want to see a repeat of the first quarter reading, which missed expectations with a gain of just 0.7%.

The Bank of Japan is in the spotlight, as policymakers gather for a policy meeting later on Wednesday. Unlike other central banks, such as the ECB and the Federal Reserve, there are no expectations of a tightening of monetary policy in the near future. However, investors will be looking for any tweaks to current monetary policy, which could trigger some movement from the yen. Inflation continues to hover below 1.0%, well below the BoJ's target of 2%. Most analysts expect the bank to push back the timeline for the 2% target, which is currently "around fiscal 2018", but do not anticipate the bank lowering the target. The BoJ has consistently said that it will not reduce its radical stimulus program until inflation levels move higher. Given current economic conditions, this is unlikely before 2018 at the earliest.

President Trump hasn't done very well at learning how to tango with Congress, and this week's debacle on Capitol Hill could make the gap between Trump and Republican lawmakers even harder to bridge. Trump had vowed to replace Obamacare, but his health care bill has stalled in the Senate before lawmakers even had a chance to vote on the proposal. With some conservative Republicans coming out against the bill, it's questionable if the Republicans can pass another version before Congress takes a recess in August. Trump had promised to pass a health care before the summer break, so his credibility will take another hit if he's unable to do so. Trump has been in office for six months, but has been unable to get Congress to pass any significant bills, even though the Republicans enjoy a majority in both houses of Congress. With this latest setback, there is growing skepticism as to whether Trump will be able to convince Congress to pass other key parts of his agenda – tax reform and fiscal spending. This paralysis on Capitol Hill has deepened investor pessimism about Trump's legislative agenda and is weighing on the US dollar.

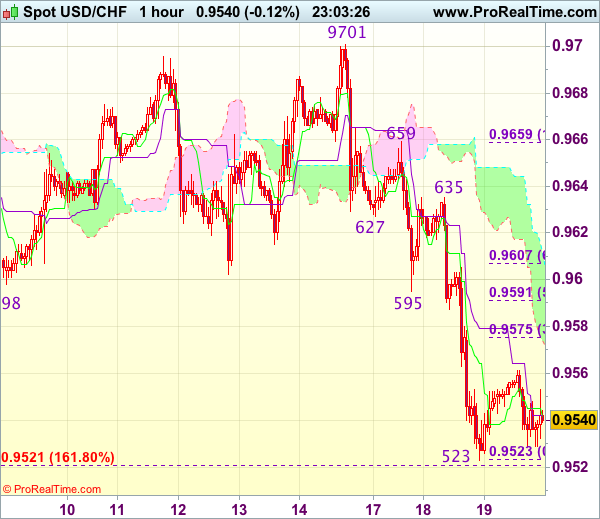

Trade Idea Wrap-up: USD/CHF – Stand aside

USD/CHF - 0.9640

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9542

Kijun-Sen level : 0.9542

Ichimoku cloud top : 0.9612

Ichimoku cloud bottom : 0.9574

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the greenback has remained under pressure after dropping sharply from 0.9701, suggesting near term downside risk remains and below support at 0.9523 would extend recent selloff to 0.9500 and possibly towards 0.9475-80, however, loss of near term downward momentum should prevent sharp fall below latter level and reckon 0.9440-50 would hold from here, risk from there is seen for another rebound later.

In view of this, would be prudent to stand aside for now. Above 0.9575 (38.2% Fibonacci retracement of 0.9659-0.9523) would bring a stronger recovery to previous support at 0.9595 but reckon upside would be limited to 0.9605-10 (61.8% Fibonacci retracement) and resistance at 0.9635 should remain intact, bring another decline later.

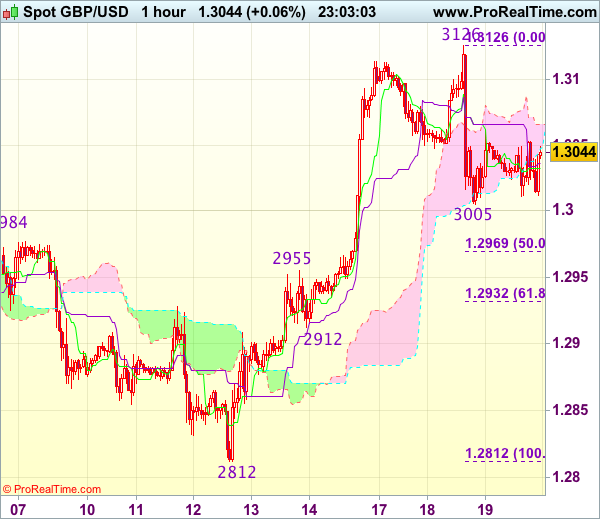

Trade Idea Wrap-up: GBP/USD – Sell at 1.3090

GBP/USD - 1.3043

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3037

Kijun-Sen level : 1.3066

Ichimoku cloud top : 1.3076

Ichimoku cloud bottom : 1.3029

Original strategy :

Sell at 1.3090, Target: 1.2990, Stop: 1.3125

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3090, Target: 1.2990, Stop: 1.3125

Position : -

Target : -

Stop : -

Although the British pound rose briefly to 1.3126, the subsequent retreat suggests temporary top is possibly formed and consolidation below this level would be seen with mild downside bias, below support at 1.3005 would add credence to this view, bring retracement of recent upmove to 1.2965-70 (50% Fibonacci retracement of 1.2812-1.3126), then test of previous resistance at 1.2955 but reckon 1.2930-35 (61.8% Fibonacci retracement) would limit downside and support at 1.2912 should remain intact.

In view of this, we are looking to sell cable on recovery as 1.3090-00 should limit upside. Only break of said yesterday’s high at 1.3126 would signal recent upmove has resumed and extend gain to 1.3150-60 but upside should be limited to 1.3190-00, bring retreat later.

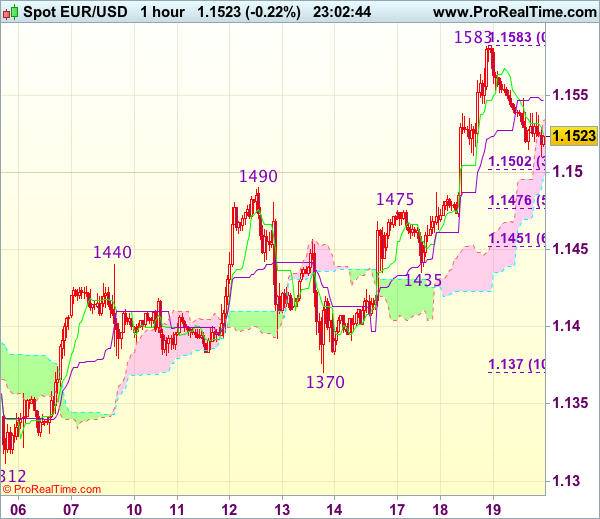

Trade Idea Wrap-up: EUR/USD – Buy at 1.1495

EUR/USD - 1.1529

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1525

Kijun-Sen level : 1.1547

Ichimoku cloud top : 1.1534

Ichimoku cloud bottom : 1.1497

Original strategy :

Buy at 1.1495, Target: 1.1595, Stop: 1.1460

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1495, Target: 1.1595, Stop: 1.1460

Position : -

Target : -

Stop : -

As the single currency has retreated after surging to 1.1583 yesterday, suggesting consolidation below this level would be seen and pullback to 1.1500-05 (38.2% Fibonacci retracement of 1.1370-1.1583) cannot be ruled out, however, reckon previous resistance at 1.1490 would contain downside and bring another upmove later, above said resistance at 1.1583 would extend recent upmove to 1.1600-10 and then 1.1630 but loss of upward momentum should prevent sharp move beyond 1.1650-60.

In view of this, we are looking to buy euro on further pullback as previous resistance at 1.1490 should turn into support and contain downside, bring another rise. Below 1.1475-76 (another previous resistance and 50% Fibonacci retracement of 1.1370-1.1583) would defer and signal top is formed, risk correction to 1.1450-55 (61.8% Fibonacci retracement) and then test of support at 1.1435 which is likely to hold from here.

Oil Surges on Inventories Draw; Dollar Drops Against Yen Despite Upbeat Construction Figures

Today's European session was a relatively quiet day as no major data releases were reported. US figures pointing to healthy construction activity and crude oil inventories were the main figures of the day. The dollar continued sliding against the yen while sterling and the euro were under some pressure against the greenback.

US homebuilding rebounded more than expected in June after declining for three consecutive months. However, this pick-up did little for the second quarter expansion that remained subdued when compared to the prior two quarters. Housing starts rose 8.3% relative to the previous month, standing at 1.215 million units. This was above the expected rate of 5.8%. The rise in construction activity was broad-based. At a monthly rate of 7.4%, building permits increased as well to reach a total amount of 1.254 million. This was well above the expected growth rate of 3% and the estimated number of issued permits of 1.2 million. Even though the figures came in above expectations, builders' sentiment slid to an eight-month low. An industry report released yesterday showed that homebuilders in the US have lost their post-election enthusiasm as rising costs for materials started to pinch and there are no signs of expected deregulation and tax-reform to help growth.

Looking at the forex markets, the dollar ignored the upbeat figures released today and fell further against the yen. Dollar/yen was last trading at 111.62.

The euro was under some pressure against the greenback today ahead of the European Central Bank meeting tomorrow. It will be ECB President Mario Draghi's first public appearance following the meeting in Sintra, Portugal. Market participants are eager to get his latest thinking on the outlook for monetary policy in the eurozone and potential for monetary tightening from this autumn. Euro/dollar was last trading at 1.1516.

Sterling was also under pressure against the dollar during the day, to last trade at $1.3017.

The loonie reacted positively on upbeat manufacturing sales data out of Canada. Manufacturing sales rose 1.1% in May relative to the previous month, coming in above expectations of 0.8%. Sales in the transportation equipment and chemical manufacturing industries drove the gain. However, this boost was also helped by a downwardly revised figure for April (down to 0.4% from 1.1%). Dollar/loonie slid to 1.2585 following the release.

Oil prices surged on a bigger than expected fall in US crude inventories for the week ending July 14, a report by the US Energy Information Administration showed. The draw was 4.727 million barrels, against expectations of 3.214 million barrels. Brent was up 1.3% to last trade at $49.46 a barrel, while WTI was up 1.4% to last trade at $47.03 a barrel.

Gold was under pressure today with the precious metal trading at $1,241.03 an ounce as the European session was about to close.

Trade Idea Wrap-up: USD/JPY – Sell at 112.70

USD/JPY - 111.70

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.88

Kijun-Sen level : 111.89

Ichimoku cloud top : 112.50

Ichimoku cloud bottom : 112.20

Original strategy :

Sell at 112.70, Target: 111.70, Stop: 113.05

Position : -

Target : -

Stop : -

New strategy :

Sell at 112.70, Target: 111.70, Stop: 113.05

Position : -

Target : -

Stop : -

As the greenback has remained under pressure after recent selloff, suggesting the decline from 114.50 top is still in progress and bearishness remains for further weakness to 111.50, then 111.20-25, however, reckon 111.00 would hold from here due to loss of downward momentum, risk from there has increased for a rebound to take place probably tomorrow.

In view of this, would not chase this fall here and would be prudent to sell dollar on subsequent recovery as 112.70-75 should limit upside. A firm break above resistance at 112.87 would defer and risk a stronger rebound to 113.10-20 but price should falter below resistance at 113.58, bring another selloff later.

FTSE100 Index Regained Traction

FTSE100 index regained traction on Wednesday and retested previous high at 7378 (07 July high) after strong indecision was signaled on Tuesday when trading ended in long-legged Doji. Today's rally probed above another pivotal barrier at 7367 (Fibo 38.2% of 7587/7232, 02/30 June downleg) but so far without clear break higher, after several attempts above this resistance failed in recent days. The index price is holding at the breakpoint (barriers are reinforced by daily Kijun-sen line) clear break of which would trigger further retracement of 7587/7232 descend and expose next key barrier at 7451 (daily cloud top/Fibo 61.8%). Near-term price action remains well supported by daily cloud top, reinforced by daily Tenkan-sen, which holds congestion of past few days. Mixed outlook on daily technicals (MA's are bullishly aligned while indicators hold below their midlines) suggesting that break of either side of near-term range (7300/7380) would give clearer signals for near-term direction.

Res: 7378; 7387; 7409; 7451

Sup: 7337; 7310; 7291; 7235

Dollar Decline Halts, at Least Temporary

- European equity indices got a lift from corporate results (Euro Stoxx 50 +0.42%), with room to rally after a strong lead-in from Asia picked up the mood. American equities opened on the same positive footing with the Nasdaq again outperforming (+0.47%).

- Construction output in the Eurozone shrunk by 0.7% M/M in May (+0.3% in April), marking the second contraction in the last three months. Output rose by 2.6% Y/Y, a decline from the 3.3% (revised) figure of April. Output fell in Germany, France and Spain in May but grew in Italy – the bloc's third largest economy.

- Amid deepening concern in the EU over an undermining of the Polish supreme court's independence, the European Commission said it is considering whether to ask other countries in the bloc to issue a formal warning against Warsaw's steps to erode the rule of law.

- US housing starts and permits both surprised to the upside. Housing starts rose from an upwardly revised 1122k in May (-2.8% M/M) to 1215k in June (8.3% M/M) while 1160k was expected (6.2%M/M). Building permits increased from 1168k (-4.9% M/M) to 1254k (7.4% M/M), 53k above the consensus (2.8% M/M).

Rates

Listless trading ahead of ECB meeting

Global core bonds (and most other assets) traded uneventful in a news poor, holiday-thinned and order-driven trading session. The price action occurred in a tight range, slightly above opening levels. The Bund evolved between 161.61 and 161.90 and changes hands now at 161.85, about 20 ticks above opening levels. News agencies ran articles about the ECB, mentioning that staff were examining options for the APP programme, but no details were given and they added that these options would not be subject of decision tomorrow. The sole EMU data release was May construction output. It disappointed, but triggered no reaction. US Treasuries moved sideways too , after a small dip in Asian trading, between 125-30 to 106-03. Even better than expected US housing starts and building permits were unable to bring some excitement. However, as the T-Note didn't drop on stronger starts/permits, it might have been the trigger for some (temporary buying) afterwards which brought the T-Note future to opening levels and the Bund to the intraday highs.

At the time of writing, German yields are nearly unchanged (flat to -1.3 bps). Changes on the US yield curve range between flat (2-yr) and +0.6 bps (30-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany are negligible (0-to-1 bp).

Regarding tomorrow's ECB meeting, we don't expect important new decisions. That's for the September meeting when new projections are available. Mario Draghi will likely be prudent in his comments, as after his Sintra comments, bonds sold off and the euro strengthened. That was maybe intended as investors need to be prepared, but repeating it too fast might trigger too strong market moves. Nevertheless, we expect the press to pressure Draghi on his recent rhetoric. Draghi might stress that the ECB will change policy gradually and keep a high grade of accommodation available. That should cap the rise of the euro and rates. There is nevertheless a minor chance that the forward guidance will again be tweaked to arrive at a complete neutral bias. More particularly, the ECB may skip the possibility that the ECB will buy more assets in case financial conditions worsen too much.

The German Finanzagentur started this week's EMU bond supply with a 30-yr Bund auction (€1B 2.5% Aug2046). Total bids amounted €1.43B, which is bank in line with the average at the previous 4 30-yr Bund auction. The Bundesbank set aside €0.195 for secondary market operations resulting in an official bid cover of 1.8 (real bid cover 1.4). The auction tailed 1 cent. The auction yield (1.29%) was the highest since the end of 2015.

Currencies

Dollar decline halts, at least temporary

Trading in in the major USD cross rates shifted into holiday modus after yesterday's steep USD losses. The inability of the US government to amend Obamacare returned to the background as a driver for USD trading and there was no other high profile market theme available. EUR/USD hovered close to, mostly slightly below 1.1550. USD/JPY initially didn't go anywhere holding near the 112 big figure, but EUR/JPY finally pushed USD/JPY to the 111.65 area.

Overnight, Asian equities rebounded as the tensions due to the Obamacare stalemate ebbed. The dollar stabilized slightly off yesterday's lows.

A lacklustre sentiment persisted in Europe. The dollar traded with a tentative positive bias, but the gains were negligible compered to recent losses. EUR/USD hovered close to, mostly slightly below the 1.1550 barrier. Interest rate differentials re-widened marginally, but the move was too small to trigger directional position taking just one day before the ECB (and BOJ) policy meetings. USD/JPY was almost paralyzed near the 112 level.

US housing starts and permits rebounded more than expected after several disappointing readings over the previous months. However, it didn't inspire USD trading. In technical trading, EUR/USD lost a few more ticks and trades currently in the 1.1525/30 area. USD/JPY even returned below 112. Stop-loss EUR/JPY selling (currently 128.75) is also weighing on USD/JPY headline pair.

Sterling going nowhere

Calm also returned for sterling trading after yesterday's inflation-driven sell-off. There were no UK eco data and we also didn't see Brexit headlines with market moving potential. EUR/GBP basically hovered in the mid 0.88 area. The modest decline in EUR/USD also helped blocking the topside in EUR/GBP. The pair trades in the 0.8850 area. Trading in cable was also order-driven and without a clear trend (currently 1.3030). Tomorrow, the UK retail are quite interesting input for the BoE . Will the erosion in disposable income due to the decline of sterling continue to weigh on spending?

Canadian Manufacturers Recorded Solid, Broadly-Based Sales Growth in May

Highlights:

- Manufacturing shipments rose 1.1% in May, the third consecutive monthly increase. April's 0.4% gain was revised down from a previously-reported 1.1% increase.

- The gain was widespread with higher sales in 16 of 21 sub-industries. The transportation sector and chemical manufacturing posted the largest contributions.

- Machinery sales posted a fifth consecutive monthly increase and were up 22% from a year ago. The increase reflects both stronger exports and improving M&E investment at home.

- Price movements were not a factor on net as sales volumes also rose 1.1% in May.

- With some drawdown in inventories, we don't expect the entire 1.1% gain in sales volumes will be captured in May's manufacturing GDP that more closely reflects new production. We look for a slightly smaller 1/2% increase on a GDP basis.

Our Take:

A resurgent goods-producing sector is part of the broadening growth picture that was a factor in the Bank of Canada raising their trend-setting interest rate a week ago. While a rebound in goods production has been led by the energy mining industry, stronger manufacturing activity has also helped boost Canada's GDP growth. Today's manufacturing report points to that trend continuing with shipment volumes rising at their fastest year-over-year pace since the end of 2014. We look for a 1/2% gain in manufacturing GDP to add to May's output figures, though that increase is expected to be swamped by a drag from the construction sector reflecting a week-long strike in Quebec. Even with overall activity expected to be flat in the month, a solid trend to start Q2 supports our forecast for a 2.7% annualized increase in GDP in the quarter.