Sample Category Title

US 30 Index Close to All-time high; Remains Bullish in the Medium-term

The US 30 index reached an all-time high of 21,681.30 during Friday's trading. It has been declining so far this week but remains close to the all-time high level.

The MACD indicator is positive and above the red signal line, suggesting a bullish bias in place. Despite this, the momentum in the very short-term seems to be negative as indicated by the stochastics. Specifically, the %K line is heading lower after crossing below the slow %D line.

Should the index advance, a barrier to the upside might be formed by the upper Bollinger band and the index's all-time high, ranging from 21,654.49 to 21,681.30. If there is a cross above this area, additional resistance could come around the 22,000 level, a potential psychological level.

On the downside, support might be found around the middle Bollinger line, which is a 20-day moving average (MA) line, at 21,462.65. If this is violated, additional support could come from the lower Bollinger band and 50-day MA, ranging from 21,270.48 to 21,252.46.

Concluding with the medium-term picture, it is strongly bullish given the significant gains by the index since the start of the year. It is of note though, that the considerable divergence between the index value and the 200-day MA might be a warning sign of an overextended rally.

AUDJPY Points Higher ahead of BoJ and Employment

Australian employment and the BoJ meeting tomorrow make AUDJPY of interest as it considers a run to Y90.

Currency markets remained fairly quiet in Asia, in stark contrast to yesterday when the Australian Dollar dominated headlines and volatility. With the technicals supporting further gains we await to see if Australian employment and the BoJ meeting allow for the run to continue.

As expectations for unemployment are to rise slightly and employment drop to 15k (42k prior) then we only have to achieve the consensus to remain supported, or exceed expectations to send AUD higher. If this is coupled with a lowered outlook by BoJ then the potential for AUDJPY to test or even break 90 are fairly high.

As we expect no changes to policy tomorrow, it may be the outlook report that is more telling about their confidence of the recovery to be sustained. Inflation forecasts will likely be lowered in response to the sanguine realised inflation and expectations endured this past quarter. With household spending, low wage growth and weak producer prices, it is hard to justify their forecasts, let alone a 2% target. Its highly unlikely QQE or the YCC (yield curve control) policies will be changed which makes tomorrow's meeting more likely to be around the outlook. Further out, as global bond markets remain threatened by central bank hawks, we cannot rule out a change to the yield control policy at some point as it will become unattainable if yields continue to rise.

This leaves potential for further Yen weakness which could help AUDJPY head for Y90. Currently the strongest performer this year among the G10, sentiment and technicals point higher for AUD which makes AUDJPY longs a high probability trade over the coming sessions.

RSI on D1 has risen above 70 which some would consider an area of 'overbought'. Yet as there are no clear signs of a bearish divergence and that RSI is merely backing up the bullishness of the preceding rally from 81.77, we see no immediate threat to further gains over the near-term. If we move down to H4 then a bearish divergence has been forming since the 29th June yet the spike higher yesterday puts this minor threat on the back-burner.

We also see a case for USDPY correcting higher following the meeting. This may also be the case for USDJPY. Despite traders being net short USD overall, traders are long USD against the Yen by $12.3bn after spiking higher last week. This suggests upwards pressure on JPY and the BoJ meeting may be the catalyst to help USDJPY recover from the 112 lows.

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 0.9635

Original strategy :

Exit long entered at 0.9555,

Position : - Long at 0.9555

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback recovered after falling to 0.9523 yesterday, near term downside risk remains and below said support would extend recent selloff to 0.9500 and possibly towards 0.9475-80, however, loss of near term downward momentum should prevent sharp fall below latter level and reckon 0.9440-50 would hold from here, risk from there is seen for another rebound later.

In view of this, would be prudent to stand aside for now. Above 0.9575 (38.2% Fibonacci retracement of 0.9659-0.9523) would bring a stronger recovery to previous support at 0.9595 but reckon upside would be limited to 0.9605-10 (61.8% Fibonacci retracement) and resistance at 0.9635 should remain intact, bring another decline later.

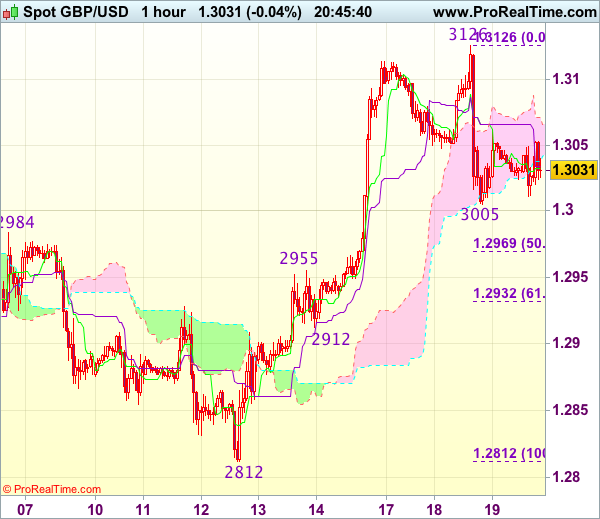

Trade Idea Update: GBP/USD – Sell at 1.3090

GBP/USD - 1.3036

Original strategy :

Sell at 1.3090, Target: 1.2990, Stop: 1.3125

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3090, Target: 1.2990, Stop: 1.3125

Position : -

Target : -

Stop : -

Although the British pound rose briefly to 1.3126, the subsequent retreat suggests temporary top is possibly formed and consolidation below this level would be seen with mild downside bias, below support at 1.3005 would add credence to this view, bring retracement of recent upmove to 1.2965-70 (50% Fibonacci retracement of 1.2812-1.3126), then test of previous resistance at 1.2955 but reckon 1.2930-35 (61.8% Fibonacci retracement) would limit downside and support at 1.2912 should remain intact.

In view of this, we are looking to sell cable on recovery as 1.3090-00 should limit upside. Only break of said yesterday’s high at 1.3126 would signal recent upmove has resumed and extend gain to 1.3150-60 but upside should be limited to 1.3190-00, bring retreat later.

Trade Idea Update: EUR/USD – Buy at 1.1495

EUR/USD - 1.1537

Original strategy :

Buy at 1.1495, Target: 1.1595, Stop: 1.1460

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1495, Target: 1.1595, Stop: 1.1460

Position : -

Target : -

Stop : -

As the single currency has retreated after surging to 1.1583 yesterday, suggesting consolidation below this level would be seen and pullback to 1.1500-05 (38.2% Fibonacci retracement of 1.1370-1.1583) cannot be ruled out, however, reckon previous resistance at 1.1490 would contain downside and bring another upmove later, above said resistance at 1.1583 would extend recent upmove to 1.1600-10 and then 1.1630 but loss of upward momentum should prevent sharp move beyond 1.1650-60.

In view of this, we are looking to buy euro on further pullback as previous resistance at 1.1490 should turn into support and contain downside, bring another rise. Below 1.1475-76 (another previous resistance and 50% Fibonacci retracement of 1.1370-1.1583) would defer and signal top is formed, risk correction to 1.1450-55 (61.8% Fibonacci retracement) and then test of support at 1.1435 which is likely to hold from here.

Dollar Gasps for Air While Euro Bulls Take a Breather

The Greenback received a thorough pummelling on Tuesday after reports of Republican legislators failing to pass a revised healthcare bill rekindled concerns over Trump's ability to implement tax cuts and infrastructure spending. Sentiment was already turning increasingly bearish towards the Dollar following last week's soft US inflation reading, with sellers swiftly exploiting the fresh setback to Trump's domestic agenda, in order to attack prices further. With the Greenback displaying signs of sensitivity to monetary policy speculations and the probability of a 25-basis-point rate increase in December dropping to 43% according to CME FedWatch Tool, further downside could be on the cards.

As the US economic calendar is fairly thin today, with only US building permits and housing starts in focus, price action is likely to dictate where the Dollar Index trades. Technical traders could be tempted to utilize the technical bounce on the daily time frame to drive the Index lower. A solid breakdown and daily close below 94.60 may encourage a further selloff towards 94.00.

Euro bulls wait for Draghi

Thursday's main risk event for the Euro will be the European Central Bank meeting, which is widely expected to conclude with monetary policy left unchanged in July. Investors will closely scrutinize the meeting and press conference for clues on whether the central bank may announce plans to reduce its bond-buying program in September. With ECB President Mario Draghi's optimistic speech in Sintra sparking speculations of QE tapering and also playing a role in the current Euro rally, he may choose his words carefully on Thursday. Although the economic conditions in Europe continue to stabilize, inflation is still far from the 2% target and it will be interesting to hear Draghi's thoughts on this. While the improving macro-fundamentals and absence of political risk in Europe have heavily supported the Euro, bulls may need further inspiration in the form of QE tapering expectations. It becomes a question of whether Draghi will offer the bulls what they crave or will end up clipping their wings.

From a technical standpoint, the EURUSD is heavily bullish on the daily charts. The breakout and daily close above 1.1500 could encourage a further incline higher towards 1.1615.

Commodity Spotlight - WTI Crude

WTI Crude Oil edged slightly lower on Tuesday after API reported US inventories increased by 1.63 million barrels last week. Although prices ventured towards $46.55 during Wednesday's trading session this had nothing to do with a change of bias, but rather profit taking, as sentiment remained bearish. Recent reports of Ecuador publicly admitting that it will not meet OPEC's cut commitments, presents a threat to the production cut deal, with fears of a domino effect exposing oil prices to further downside risks. The bias towards oil remains bearish and further downside may be expected as the supply overhang erodes investor attraction towards the commodity. Much attention will be directed towards the pending report from the US Energy Information Administration (EIA) this afternoon, which could compound to oils woes if there is a build in crude inventories.

Trade Idea Update: USD/JPY – Sell at 112.70

USD/JPY - 111.90

Original strategy :

Sell at 112.70, Target: 111.70, Stop: 113.05

Position : -

Target : -

Stop : -

New strategy :

Sell at 112.70, Target: 111.70, Stop: 113.05

Position : -

Target : -

Stop : -

Although the greenback recovered after falling to 111.68 yesterday and minor consolidation above this level would be seen, as the selloff from 114.50 signals top has been formed there, reckon upside would be limited to the upper Kumo (now at 112.73) and bring another decline, below said support at 111.68 would extend the fall from 114.50 top to 111.50, then 111.20-25 but reckon 111.00 would hold from here due to loss of downward momentum.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 112.70-75 should limit upside. A firm break above resistance at 112.87 would defer and risk a stronger rebound to 113.10-20 but price should falter below resistance at 113.58, bring another selloff later.

USD/CAD Undecided ahead the US and Canadian Data, Brent Oil Another Breakout Attempt, NZD/USD Reached Another Upside Target

USD/CAD undecided ahead the US and Canadian data

The currency pair changed little in the last hours, but will move aggressively in the upcoming hours as the fundamental factors will take the lead again. The US and Canada data could bring life on the pair, which maintains a bearish perspective, will drop much deeper if the US data will disappoint again.

Is trading much above the 1.2580 yesterday's low, but is under pressure because is located deep in the seller's territory, only an USDX's impressive rally will will force the USD/CAD to increase again in the upcoming period. Another leg higher is uncertain right now because the pair is trapped below some important resistance levels.

The Loonie could receive more support from the Canadian Manufacturing Sales, which is expected to increase by 0.9% in May, but less versus the 1.1% growth in the former reading period. On the other hand, the greenback needs a bullish spark from the US economy, the Building Permits could increase from 1.17M to 1.20M in the previous month, moreover the Housing Starts are expected to climb from 1.09M to 1.16M in June. The USD will increase only if the US data will come in line with expectations or better.

Price is trading in the red and maintains a bearish perspective on the short term as long as is trading within the minor descending pitchfork's body. Is located also much below the 1.2678 broken static support and below the third warning line (wl3) of the former minor ascending pitchfork.

The next downside targets are at the lower median line (lml) of the minor descending pitchfork and at the 1.2460 swing low, a further USDX's drop will send the rate towards these objectives.

Brent Oil another breakout attempt

The Brent Oil is trading in the green and is located much above the 48.58 yesterday's closing price, technically is somehow expected to increase further.

Is still trying to break above the 48.89 static resistance, a valid breakout will attract more buyers on the short term, which will drive the rate towards the outside sliding line (SL) of the descending pitchfork. Is expected to increase after the failure to reach and retest the 38.2% retracement level and the 50% Fibonacci line (ascending dotted line).

Only a breakout above the outside sliding line (SL) will confirm a broader upside movement in the upcoming weeks.

NZD/USD reached another upside target

Price rallied and climbed much above the 0.7372 yesterday's high and above the 0.7375 major static resistance, remains to see if will have a valid breakout above the long term resistance because has found resistance at the up sloping red line.

A false breakout above the 0.7375 level will signal an exhaustion and a potential corrective phase, however the perspective remains bullish as long as stays above the fourth warning line (WL4), only breakdown below this level will open the door for more declines.

DAX in Holding Pattern Ahead of ECB Statement

The DAX index is unchanged in the Wednesday session. With no major events on the schedule, we can expect investors to concentrate on earnings news, so it could continue to be a quiet day for the DAX. Currently, the DAX is trading at 12,430.00, unchanged on the day. On Thursday, the ECB will release its monthly rate statement.

The Trump administration continues to flounder, as a key plank in Trump's agenda appears dead in the water. Trump's proposed health care bill, which replaces much of Obamacare, has stalled in the Senate before lawmakers even voted on the bill. With some conservative Republicans against the bill, it's questionable if the Republicans can craft a new proposal which could be passed before Congress takes a recess in August. Trump had promised to pass a health care before the summer break, so his credibility will take another hit if he's unable to do so. With this latest defeat, there is growing skepticism as to whether Trump will be able to convince Congress to pass other key parts of his agenda – tax reform and fiscal spending. The Republicans also have egg on their faces, as they have been unable to pass any significant legislation since Trump took over, despite having control of both houses of Congress and the White House. This paralysis on Capitol Hill has deepened investor pessimism about the Trump administration and has hurt the US dollar.

Investors are keeping a close on the ECB, which holds its policy meeting on Thursday. What can we expect from Mario Draghi & Co.? The bank is unlikely to make any changes to its asset-purchase program (QE). With the eurozone showing improvement in 2017, there has been speculation that the bank might taper QE or change the expected end of the scheme, which is December of this year. The ECB makes every attempt to avoid shaking up the markets, but this policy doesn't always work. Case in point – at the ECB forum in June, upbeat comments by ECB President Mario Draghi about tweaking QE led to a sharp rally by the euro. If the eurozone economy continues to show strong numbers, we could see the ECB make some adjustments in its September meeting. In December 2016, the bank tapered QE while extending the scheme until December, and this type of scenario could be adopted once again. Analysts will be combing through the July statement, as well as Draghi's press conference, looking for any nuances to tweaks which could hint at substantive changes to come in September.

Euro Zone Bond Yields A Touch Lower As Markets Eye Cautious ECB

Borrowing costs in the euro area dipped on Wednesday, with investor sentiment underpinned by a view that the ECB is unlikely to signal significant policy tweaks when it meets this week, given subdued inflation and a stronger euro.

Reduced expectations of another rise in U.S. interest rates this year and the expansionary fiscal policies flagged by U.S. President Donald Trump that could boost inflation helped push down bond yields.

European Central Bank chief Mario Draghi is expected to use Thursday's meeting to calm market expectations of a scaling back of stimulus in coming months.

Comments he made three weeks ago in Sintra, Portugal were seen opening the door to tapering of asset purchases and sparked a sharp selloff in bonds.

Data this week confirmed that euro zone inflation remains tame at 1.3 percent – well below the ECB's near 2 percent target – while further strength in the single currency could dampen inflation by keeping down import costs.

The euro hit its highest level in more than a year against a broadly weaker dollar on Tuesday and is up roughly 3 percent since just before Draghi's Sintra speech.

“A strong euro has also raised expectations that they will not sound overly hawkish,” said Benjamin Schroeder, a rates strategist at ING.

Most euro zone government bond yields were 1-2 basis points lower. Germany's benchmark 10-year Bund yield dipped 1 bps to 0.55 percent, off recent 18-month highs.

Germany on Wednesday sold 805 million euros of 30-year government paper.

Concerns that central banks globally are gearing up for a tighter monetary policy stance have been eased in the past week by weak U.S. economic data. On Tuesday, weaker-than-expected inflation numbers in Britain also dampened talk of a rate hike in the months ahead, lifting broader bond market sentiment.

“On the issue of tapering, which has been obsessing the market, we're unlikely to get anything tomorrow and that is reassuring the market,” said Antoine Bouvet, rates strategist at Mizuho. “But that doesn't mean the ECB will be dovish or pessimistic about growth – there's no reason for that either.”