Sample Category Title

Housing Starts Rebound in June

Homebuilders made up for previous months' contractions breaking ground on 1215k units in June - the highest level since February. This surprised to the upside, with expectations for a 1160k print. Compounding this is the healthy reading for building permits that also surpassed expectations and clocked in at 1254k on the month, the highest level since March.

Single family homebuilding accounted for the bulk of the growth, rising by 50k from last month, while the volatile multi-family segment wasn't far behind at 43k. This is enough to leave the quarter with a net gain of 25k in the construction of single-family units. Activity in the multifamily segment was largely unchanged in the quarter.

Permits surpassed expectations, with the single family segment posting the strongest gain since December 2016, rising by 32k in June. Multi-family permits also increased by a strong 54k on the month. These are welcome developments, suggesting further strength in homebuilding will follow.

The Northeast saw the strongest growth in starts (+72k) since the first half of 2016 while the Midwest also saw activity expand by a robust 37k. In contrast, the South added to a string of consecutive declines in activity as starts fell by 21k in June. Activity in the West was little changed (+5k).

Key Implications

After a dismal start to Q2, homebuilding activity finally picked up in June to end the quarter with a net gain in housing starts. While costs for homebuilders have increased amid land supply constraints, labor shortages, and rising building material costs - with softwood lumber prices, already under upward pressure from softwood lumber tariffs, rising further as a result of the fires in British Columbia - builders have so far passed on the costs to consumers. Overall, builders are maintaining confidence as demand has remained strong with this sentiment echoed in the July NAHB survey that indicated optimism amongst builders.

Strong demand from homebuyers will continue to underpin construction activity as rising incomes offset any drag from rising mortgage rates. This notion is corroborated by the fact that the less volatile single-family segment accounted for the bulk of the increase, with permitting activity boding well for near-term starts.

While today's report erases the contraction in starts at the beginning of the quarter, the level of activity during the second quarter still remained below that in the first quarter with residential construction expected to be a drag on growth in the second quarter, which should still clock in at a relatively healthy 2.7%. The strong handoff into the third quarter suggests that residential investment should once again become supportive of economic growth in the third quarter.

Canadian Manufacturing Posts Solid Gains in May, But Downward Revisions Put Blemish on Report

Canadian manufacturing sales increased 1.1% in May, bettering market expectations for a 0.8% gain, but came with a downward revision to April sales which increased 0.4% (prev. reported as 1.0%). After accounting for price swings the volume of sales was up an even more impressive 1.1% on the month. But again, this came atop of downward revision to the previous month, where the 0.5% gain was revised to a 0.2% decline.

The gain was entirely due to durables, which advanced 2.2% in May. Amongst durables, it was motor vehicles (+8.6%), motor vehicle parts (+5.7%), miscellaneous mfg. products (+5.7%) and electrical equipment (4.5%) that led the way. On the other hand, nondurables were little changed (-0.3%) as gains in chemicals (+2.4%) and paper (+1.8%) were offset by declines in petroleum & coal products (-3.4%),) and food (-1.2%).

Regionally, manufacturing sales were up in six provinces, led by N.S. (+3.7%), Ontario (+2.6%), B.C. (+1.8%). Shipments increased by 1.3% in both Alberta and N&L, while P.E.I. (-12.9%) and N.B. (-1.7%) exhibited the largest losses.

Inventories were down 0.2% on the month, with the inventory-to-sales ratio down slightly to 1.35. Forward looking indicators were disappointing with new and unfilled orders down 3.6% and 1.5%, respectively in May.

Key Implications

While May marked a good month for Canadian manufacturing, the downward revisions to April's sales in both value and volume terms have dampened our enthusiasm somewhat. Still, the solid volume print in May suggests healthy activity during the second quarter, with the performance supportive of economic growth which should come in close to 3% during the second quarter.

This performance is not likely to last however. Leading indicators, such as new and unfilled orders, were largely disappointing with both metrics down sharply during the month, although some solace is to be had in industrial production in the U.S. manufacturing and auto sector, which advanced 0.2% and 0.7%, respectively, in June.

Overall, while continued U.S. growth should remain supportive of Canadian manufacturing activity, the recent spike in the loonie's value on account of tighter monetary policy by the Bank of Canada will likely pose some downside to growth. The sectoral outlook may be further complicated by the upcoming NAFTA renegotiations, with the U.S. Trade Representative publishing rather stringent objectives this week. Discussions will likely begin in mid-August and are likely to last for some time given significant sticking points.

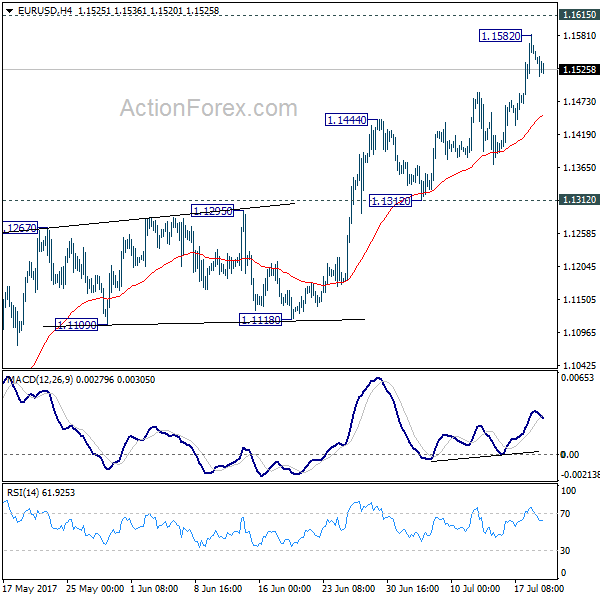

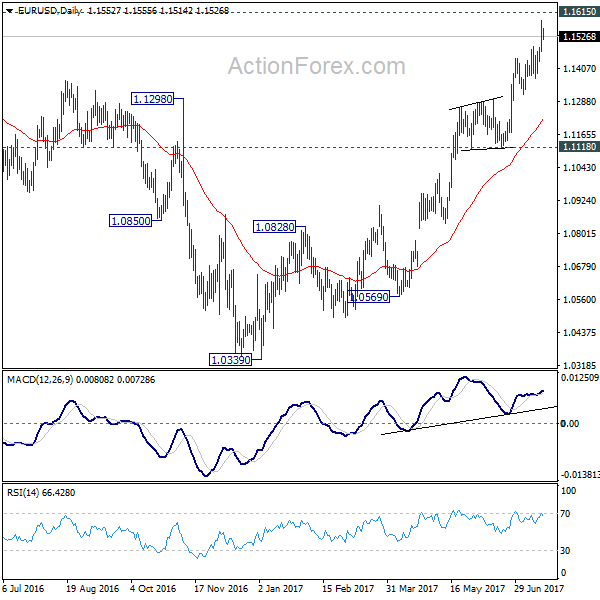

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1488; (P) 1.1536 (R1) 1.1600; More.....

A temporary top is in place at 1.1582 in EUR/USD. Intraday bias is turned neutral first for some consolidations. But overall, outlook will remain bullish as long as 1.1312 support holds. Above 1.1582 will target 1.1615 key resistance. Decisive break there will pave the way to 1.2 handle next.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1756). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

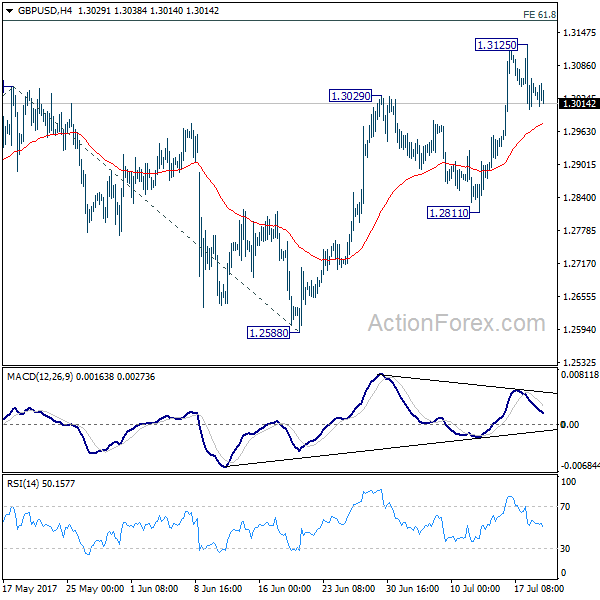

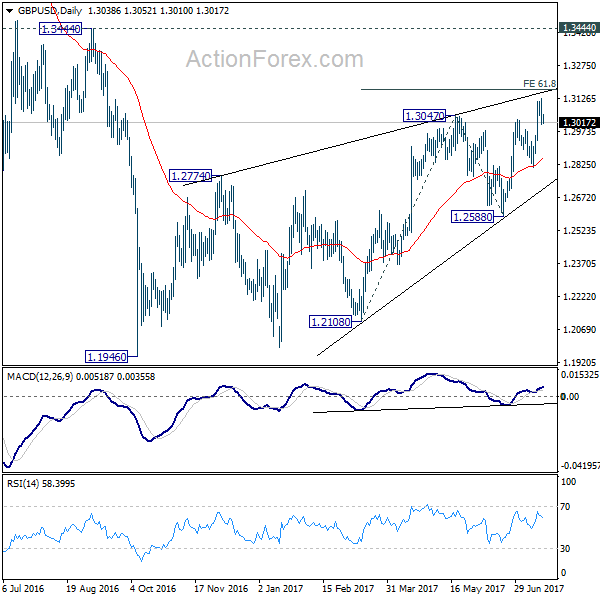

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2988; (P) 1.3056; (R1) 1.3109; More...

Intraday bias in GBP/USD remains neutral for consolidation below 1.3125 temporary top. Another rise would be seen as long as 1.2811 support holds. Break of 1.3125 will target 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168. Overall, choppy rebound from 1.1946 is seen as a corrective pattern, hence, we'd be cautious on strong resistance from 1.3168 to limit upside. But firm break of 1.3168 will bring further rise towards 1.3444 key resistance. Meanwhile, break of 1.2811 support will be the first sign of reversal and will turn bias to the downside to target 1.2588 key support next.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

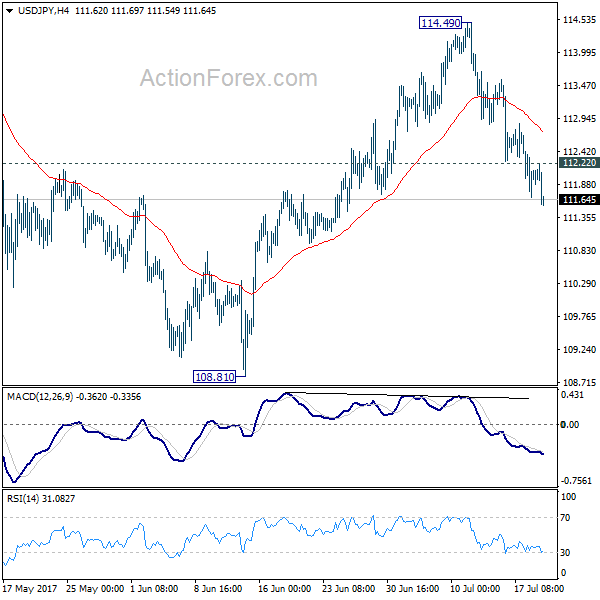

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.60; (P) 112.13; (R1) 112.59; More...

USD/JPY's fall from 114.49 is still in progress and intraday bias remains on the downside. Sustained trading below 55 day EMA (now at 112.02) will target 197.71 support. As noted before, whole correction from 118.65 is possibly still in progress. Break of 108.81 will confirm and target 61.8% retracement of 98.97 to 118.65 at 106.48. On the upside, above 112.22 minor resistance will turn intraday bias neutral first.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

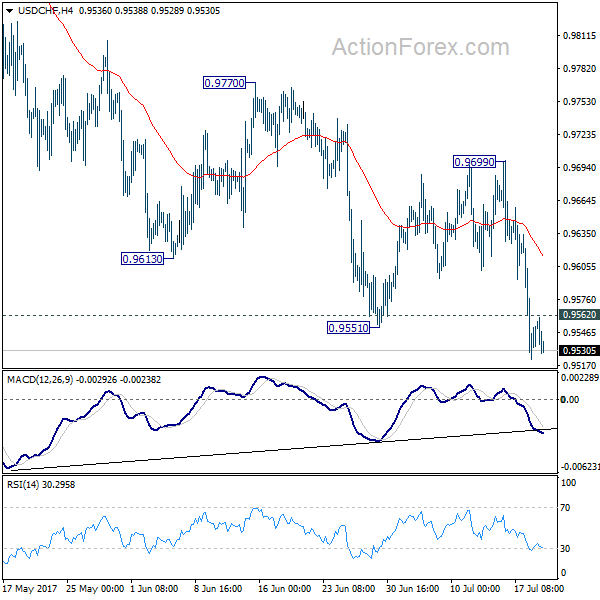

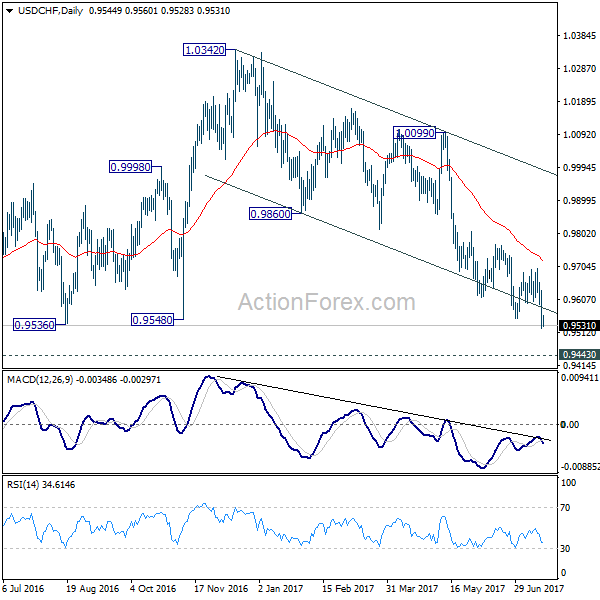

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9503; (P) 0.9569; (R1) 0.9614; More...

Intraday bias in USD/CHF remains on the downside for the moment. Current fall from 1.0342 should target 0.9443 key support level next. At this point, we'd expect strong support from there to bring rebound. On the upside, above 0.9562 minor support will turn intraday bias neutral first. Nonetheless, break of 0.9699 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

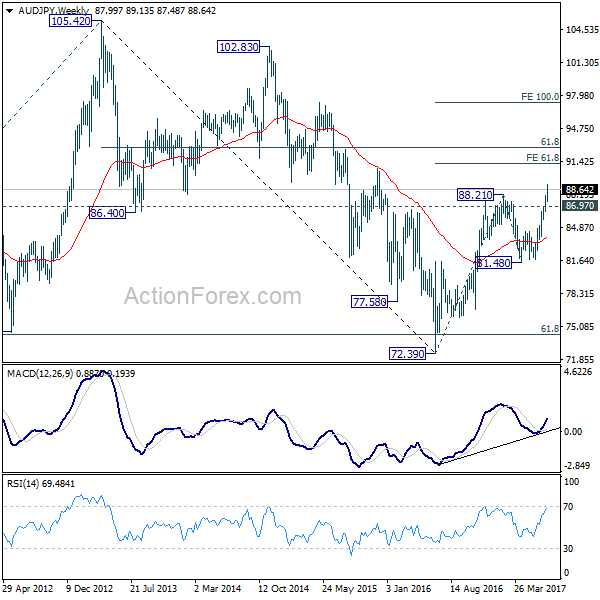

AUD/JPY Firm ahead of BoJ Policy Decision and Australia Employment Data

The forex markets are in rather dull mode today with lack of new drivers. Sterling remains the weakest currency for the week and markets continue to pare back expectation of a near term BoE hike. Dollar follows closely as there are talk emerging that US President Donald Trump would achieve nothing this year after the collapse of the health care bill. Euro also trades generally lower today as markets await ECB rate decision and press conference. But some volatility could be see in the upcoming Asian session first, with Australia employment data and BoJ policy decisions featured.

Australia to release job data

Aussie and Yen are both trading broadly higher today as markets await some key events tomorrow. Australian employment data will be one of the major focuses. Markets are expecting Australia to show 15k in job growth in June while unemployment rate is expected to climb back to 5.6%. The Aussie surged sharply earlier this week as hawkish RBA minutes revived speculations of rate hike. In particular, the minutes noted that 'employment growth had been strong in May for the third consecutive month. Members noted that growth in the preceding few months had been driven entirely by full-time employment and that total hours worked had trended higher as a result'. Strong job data will certainly give Aussie another lift.

Markets look into BoJ board shuffle

BoJ will also announce policy decision tomorrow. While no change is expected by the central bank, the markets are eager to see how the reshuffle in the board would shape the balance. New member Goushi Kataoka is a known dove who advocate massive stimulus. He wrote in a research note at Mitsubishi UFJ Research and Consulting earlier this year that "full-blown monetary and fiscal policies coupled with a growth strategy are crucial to break completely out of prolonged economic stagnation." Another new member Hitoshi Suzuki is believed to be a neutral. On the other hand, the usual dissenters Takehiro Sato and Takahide Kiuchi left.

AUD/JPY resumed medium term rebound

AUD/JPY's strong break of 88.21 resistance this week confirmed resumption of rise from 72.39 medium term low. Near term outlook will now stay bullish as long as 86.97 support holds. Next targets are 61.8% projection of 72.39 to 88.21 from 81.48 at 91.25 and then 61.8% retracement of 105.42 (2013 high) to 72.39 at 92.80. We'll be cautious on stopping in this resistance zone on first attempt.

Euro retreats ahead of ECB

Euro retreats mildly today as markets are preparing for ECB rate decision and press conference. The central bank is widely expected to keep interest rates and the asset purchase program unchanged. It's reported that ECB staff are looking at scenarios of future policy path and decisions could be made in September. The details might include the path tapering, extension of asset purchase as a slow pace, or a combination. There is no solid proposal for the moment and ECB policy makers are unlikely to change the language to signal a policy shift yet. Yet, it should be consensus that the central bank has to take the shift very carefully. Recent comments from ECB President Mario Draghi has also shot up the Euro and yields in Eurozone, that pushed global yields much higher.

Trump could achieve nothing this year

After the repeal of Obamacare failed on the second attempt earlier this Tuesday. Trump then declared that his plan now is to "let Obamacare fail" and said after that, the Democrats would come to see out Republicans to work on a plan to replace it. Focus is now turned to Trump's tax reform. It's reported that Some Republican leaders are working on high-levels principles for the reform. But it's believed that Trump may not be able to even release a broad outline until September. The last time White House did a major tax bill back in 1986, it took more than a year to complete the work.

On the data front

US housing starts rose to 1.22m annualized rate in June, building permits rose to 1.25m. Canada manufacturing shipments rose 1.1% mom May. Australia Westpac leading index dropped -1.0% mom in June.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9503; (P) 0.9569; (R1) 0.9614; More...

Intraday bias in USD/CHF remains on the downside for the moment. Current fall from 1.0342 should target 0.9443 key support level next. At this point, we'd expect strong support from there to bring rebound. On the upside, above 0.9562 minor support will turn intraday bias neutral first. Nonetheless, break of 0.9699 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Jun | -0.10% | 0.00% | ||

| 12:30 | CAD | Manufacturing Shipments M/M May | 1.10% | 0.70% | 1.10% | |

| 12:30 | USD | Housing Starts Jun | 1.22M | 1.16M | 1.09M | 1.12M |

| 12:30 | USD | Building Permits Jun | 1.25M | 1.20M | 1.17M | |

| 14:30 | USD | Crude Oil Inventories | -7.6M |

Trade Idea: EUR/GBP – Stand aside

EUR/GBP - 0.8848

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

Original strategy :

Sold at 0.8845, stopped at 0.8885

Position : - Short at 0.8845

Target : -

Stop : - 0.8885

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the single currency retreated after rising briefly to 0.8950 last week, as euro found support at 0.8743 and has staged a strong rebound, suggesting further choppy trading would be seen but reckon upside would be limited to 0.8900 and price should falter well below said resistance at 0.8950, bring retreat later. Only a break of 0.8950 would signal recent erratic rise has resumed and extend gain to 0.9000 first.

On the downside, whilst weakness to 0.8800-10 cannot be ruled out, break of 0.8780-85 is needed to signal the rebound from 0.8743 has ended, bring another test of this level, break there would extend the fall from 0.8950 for retracement of recent upmove to support at 0.8719 and possibly towards 0.8700. As near term outlook has turned mixed, would be prudent to stand aside for now.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Sell at 1.2765

USD/CAD - 1.2601

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway with wave iii ended at 1.4690, wave v of C may bring one more marginal rise probably in 2018

Trend: Near term down

Original strategy :

Sell at 1.3010, Target: 1.2850, Stop: 1.3070

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.2765, Target: 1.2565, Stop: 1.2825

Position: -

Target: -

Stop:-

The greenback only recovered to 1.2944 before dropping again, adding credence to our bearish view and we took the count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii still in progress, bearishness remains for this fall to extend weakness to 1.2550-60, then towards 1.2500-10, however, oversold condition should prevent sharp fall below 1.2440-50, risk from there is seen for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell the pair again on recovery as 1.2760-70 should limit upside. Above 1.2800-10 would defer and risk a stronger rebound to 1.2850-60 but only break of latter level would signal a temporary low is formed instead, bring retracement of recent decline to 1.2900-10, then 1.2940-50, however, price should falter below 1.3000 and the greenback shall head south again from there.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

CAC Edges Higher, Markets Eye ECB Rate Statement

The CAC index has posted small gains in the Wednesday session. Currently, the index is trading at 5187.80, up 0.29% on the day. In economic news, there are no French or eurozone events on the schedule. We're likely to see more movement from European stock markets on Thursday, as the ECB will release its monthly rate statement.

On Tuesday, the CAC suffered its worst day this month, dropping 0.8 percent. French stock markets were down in response to soft investor confidence surveys in Germany and the eurozone. The ZEW Economic Sentiment surveys gauge the optimism of institutional investors and analysts. Both surveys indicated that investor confidence in June had weakened compare to the May readings. With the eurozone economy improving, analysts attributed the dip in investor confidence as due to the stronger euro, which is making European exports more expensive and thus less attractive for foreign buyers.

The markets are keeping close tabs on the ECB, which will release a rate statement on Thursday. The meeting could prove to be a non-event, as the bank is unlikely to make any changes to its asset-purchase program (QE). With the eurozone showing improvement in 2017, there has been speculation that the bank might taper QE or change the expected end of the scheme, which is December of this year. The ever-cautious ECB was shocked last month, when comments from ECB President Mario Draghi about tweaking QE triggered a sharp rally from the euro. If the eurozone economy continues to show strong numbers, we could see the ECB make some adjustments to monetary policy in its September meeting. In December 2016, the bank tapered QE while at the same time extending the scheme until December of this year, and this type of scenario could be adopted once again. Analysts will be combing through the July statement, as well as Draghi's press conference, looking for any nuances or tweaks which could hint at substantive changes come September.

With the election of President Emmanuel Macron, who ran a campaign promising political and economic change, France is looking to take on a bigger role in Europe and on the international scene. French officials are keeping a close eye on Brexit developments, as the messy departure of Britain from the EU could be a golden opportunity for France, both politically and economically. One likely casualty of Brexit will be the City of London, which until now has been a key financial center in Europe. However, with Britain leaving the EU, many European companies and banks will be downsizing their London operations, and the French are eager to snare a share of the spoils. France plans to cut its corporate tax from 33.3% to 25% by 2022, and French officials are actively courting companies to consider moving to Paris, rather than to other locations such as Frankfurt.