Sample Category Title

EURGBP Change In Momentum After 10-Month High

EURGBP hit a ten-month high of 0.8948 in yesterday’s trading before declining to finish the day 0.8% lower.

The RSI indicator is theoretically in bullish territory at 57 but it is heading lower, hinting to a negative short-term momentum currently in place.

Should the price rise, the area around 0.89, a potential psychological level, might act as a barrier to further advancing. Stronger gains would bring into scope the area around yesterday’s ten-month high of 0.8948 for additional resistance.

If the price declines, the area around the 23.6% Fibonacci level (April 18 – July 12 upleg) at 0.8798 could provide support. Additional declines would shift focus to the 38.2% Fibonacci mark, which also currently happens to coincide with the 50-day moving average, as another support area.

Concluding with the medium-term outlook, it remains bullish as a result of significant advancing over the last three months.

USDCHF Consolidates Near 8-Month Low, Bearish Bias In Place But Softer

USDCHF has followed a downward path since the middle of December when it managed to peak above the psychological level of 1.000 for the second time in 2016. Currently, the price is hovering around the 8-month low of 0.9551, reached in the end of June, but the short-term bias is less bearish now.

After the pair crossed below the 50-day and the 200-day moving average (MA) on May 15, the RSI broke into bearish area, while the MACD deepened into negative territory, pointing to a short-term risk to the downside. However, the bearish bias has softened as both indicators have been recently moving closer to neutral ground.

Should the price decline, the swing-low of 0.9551 of the Fibonacci retracement from December to June, would provide an immediate support. Further declines would shift focus first to the area around the psychological level of 0.9500 and second to the area near 0.9400 which were of significance in the past.

Alternatively, if prices go up, a resistance would be found at the latest high of 0.9695. Further up, the 23.6% Fibonacci mark of 0.9737 could be an additional resistance, while a steeper increase would meet the 38.2% Fibonacci of 0.9852.

Looking at the medium-term picture, the outlook seems neutral as the pair has been moving in a range since the end of 2015. Yet, if the pair falls below 0.9400 then the outlook would turn bearish as the market action would lead to a resumption of the longer-term downtrend.

Yellen Sends Dollar Low Against Majors, Euro Recovers, Aussie Firms

The dollar eased against the yen on Wednesday, following Federal Reserve Chair Janet Yellen's dovish speech. The dollar index fell 0.23% during the Asian session today, confirming weakness in the US currency. The euro gained, erasing most of yesterday's losses on the back of falling bond yields.

Janet Yellen started her two-day testimony to Congress yesterday with a more dovish take on monetary policy that sent the greenback plunging below the 113 level. The Fed Chair anticipates interest rates hikes to be gradual and that the Fed may not be able to raise rates by “all that much”. This induced a drop in US Treasury yields, which was subsequently reflected in dollar/yen weakening 0.7% yesterday and by a further 0.2% to 112.91 during the Asian session. Janet Yellen is scheduled to continue her testimony today, starting at 14:00 GMT.

Led by increasing Australia-US 10-year bond spread, the aussie gained today for the fifth consecutive day. Aussie/dollar rose to 0.7713 during the Asian session. Additionally, strong trade data out of China boosted the Australian dollar against its US counterpart. China's exports in June grew 11.3% year-on-year, above the expected 8.7%, while imports rose 17.2% vs. the 13.1% forecast.

The euro recovered most of yesterday's losses during the Asian session today. Following the Fed Chair testimony, the euro fell as yields on government bonds across the EU slid. However, the euro managed to recover during Asian trading, raising to $1.1450. Final inflation figures for the major EU economies were released ahead of the European session, confirming the flash data and hence without significant impact on the euro.

In the UK, divergence of opinions on the country's monetary policy is remerging as Bank of England member Ian McCafferty expressed a stronger hawkish take. He said in an interview to the Times that the BoE should consider tapering its quantitative easing program earlier than planned. Mr. McCafferty, who was one of three voting members for an interest rate hike during last month's policy meeting, confirmed that he plans to mirror his decision in the upcoming meeting. By contrast, BoE deputy governor Ben Broadbent was more dovish in his recent speech. Sterling rose for the second consecutive day against the greenback, reaching $1.2934. On the political front, the UK government is expected to publish its Brexit Repeal Bill today, a landmark law set to pave the path for UK's exit from the EU. At the same time, the Bill will be a major area of dispute among the MPs in the coming months.

The loonie continued gaining during Asian trading, following yesterday's significant uplift due to the interest rate hike by the Bank of Canada. Dollar/lonnie fell to 1.2730, a 13-month low, ahead of the European open.

Oil prices managed to remain above the $45 level, despite some pressure today. WTI was last trading at $45.40 a barrel while Brent was at $47.62.

Gold continued to strengthen as a weaker US currency lifted demand for the precious metal. Gold was last trading at $1,222.84 an ounce.

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

It was a really bad day for the greenback, but the common currency was unable to benefit from its rivals' weakness, plunging with the strong momentum triggered in worldwide equities by Fed's Yellen. The chief of the American central bank testified before the Congress, with her statement released 90 minutes before the event. The document was seen as dovish, as policymakers noted uncertainty surrounding inflation, and while reaffirming that they are still in the tightening path, it won't take much more rate hikes to reach what they consider 'normal.' After the statement and the Q&A, market players reconsidered that Yellen was not that dovish after all, but the dollar remained under pressure anyway, as news coming from different fronts, such as Canada rising rates, or strong employment data in the UK, fueled demand for high yielding currencies.

The EUR/USD pair closed the day above the 1.1400 figure, having reached a fresh 2017 high of 1.1489 at the beginning of the day, and despite the sharp intraday retracement, the downward potential remains limited according to the 4 hours chart, as the price settled a few pips above a still bullish 20 SMA, whilst technical indicators are currently bouncing from their mid-lines, after correcting overbought conditions reached earlier on the day. The pair has an immediate support in the 1.1380/90 region, where buying interest surged ever since the week started, followed by a daily ascendant trend line currently around 1.1340.

Support levels: 1.1385 1.1340 1.1290

Resistance levels: 1.1460 1.1490 1.1525

USD/JPY

The USD/JPY pair plunged to 112.92, down for a second consecutive day on softening US Treasury yields following Yellen's latest remarks. The head of the Fed gave her semi-annual monetary policy testimony before the Congress, and while the statement was not actually dovish, it stalled short from backing the greenback, as she suggested that, while still in the tightening path, rates won't rise much more during the upcoming years. Stocks and bonds surged, leading to a sharp decline in yields, the main motor for yen crosses. Now trading around 113.20, the 4 hours chart shows that the decline accelerated after the price broke below the base of the daily ascendant channel that led the way since early June, while technical indicators pared their declines, holding near oversold readings. In the same chart, the price remains above its 100 and 200 SMAs, with the shortest now in the 112.50 region, offering a key intraday support, as below it the bearish momentum will likely accelerate.

Support levels: 112.85 112.50 112.10

Resistance levels: 113.60 114.00 114.40

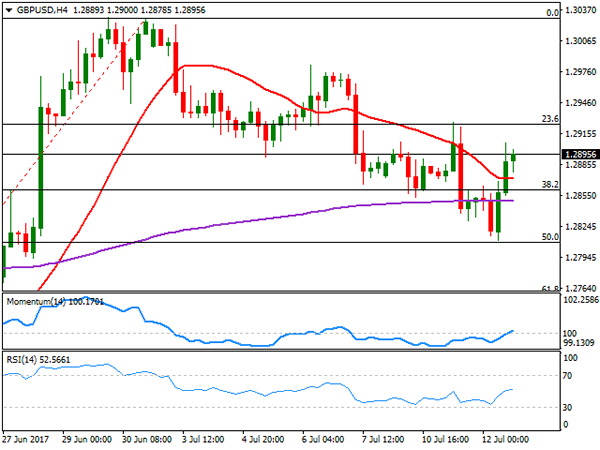

GBP/USD

The Pound surged against the greenback reverting its early weekly losses, getting a boost from solid UK employment data, as in the three months to May, there were 32.01 million people in work, 175K more than in the previous three months, while the unemployment rate fell to its lowest since 1975, down to 4.5%. Wages grew by 2% in June, against an expected 1.9% rate of expansion, and above a revised 1.8% in May, but lag when compared to inflation. The GBP/USD pair settled a few pips below the 1.2900 level, bouncing from a daily low of 1.2811, level achieved after BOE's Broadbent said that he is not ready to hike rates. The pair bounced by the pip from the 50% retracement of its latest rally, recovering also above the 38.2% retracement of the same rally at 1.2860, the immediate support. In the 4 hours chart, the price has settled above a flat 20 SMA, while technical indicators are now stuck around their mid-lines, with no clear directional strength, limiting chances of a steeper recovery, as long as the price remains below 1.2925, the next Fibonacci resistance and this week's high.

Support levels: 1.2860 1.2810 1.2770

Resistance levels: 1.2895 1.2925 1.2960

GOLD

Spot gold advanced for a third consecutive session to close the day at $1,220.20 a troy ounce, albeit gains were once again modest, as despite Fed's Yellen was less hawkish than expected, she confirmed the US Central Bank plans to keep on rising rates and start shrinking its balance sheet later this year. The commodity posted a daily high of 1,225.63 before retreating, and the overall outlook keeps favoring the downside, as the recovery was rejected from its 200 DMA, with technical indicators in the daily chart still heading modestly higher within negative territory, and the 20 DMA extending its slide well above the current level. In the 4 hours chart, spot met intraday buying interest around a horizontal 20 SMA whilst technical indicators lost upward momentum and turned lower, still holding within positive territory. Below 1,212.80, the risk turns towards the downside, with scope then to extend its slide pass the 1,2000 threshold.

Support levels: 1,212.80 1,204.75 1,194.95

Resistance levels: 1,225.60 1,236.50 1,242.50

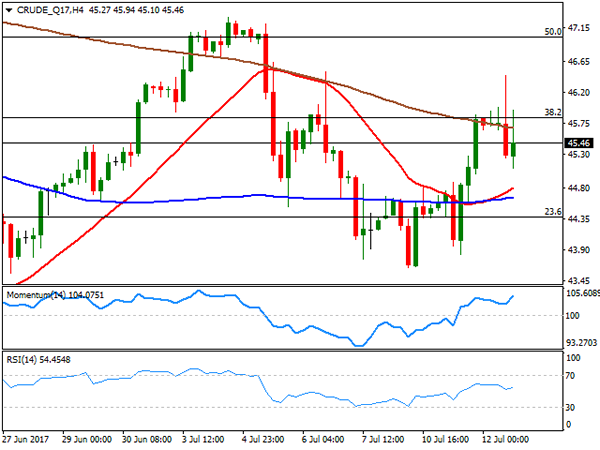

WTI CRUDE OIL

West Texas Intermediate crude oil futures closed the day down at $45.50 a barrel after peaking at 46.45 on a surprise drawdown in US crude stockpiles. The EIA weekly report showed that US crude stockpiles fell by 7.6 million barrels in the week ended July 7th, with the headline sending the price higher. The report, however, also showed that total local crude production edged up by 59,000 barrels a day to 9.397 million barrels in the same week. Additionally, gasoline stockpiles fell by 1.6 million barrels, but distillate stockpiles climbed by 3.1 million barrels. In the news, the OPEC said it will hold an extraordinary meeting on July 17th. Daily basis, the commodity was unable to sustain gains beyond 46.60, the 38.2% retracement of its latest decline still trading above a flat 20 SMA but far below bearish 100 and 200 SMAs, whilst technical indicators have turned lower, lacking clear directional strength right above their mid-lines. In the 4 hours chart, technical indicators head north within positive territory, with the price still below a bearish 200 SMA.

Support levels: 45.10 44.60 43.70

Resistance levels: 45.90 46.60 47.25

DJIA

Wall Street soared, with the Dow Jones Industrial Average reaching an all-time high and ending the day 123 points higher at 21,532.14. The Nasdaq Composite added 67 points or 1.10% to end at 6,261.17 while the S&P closed the day at 2,443.25, up 17 points. Gains were a result of Fed's Chair Janet Yellen semi-annual testimony before the Congress, as she said the Central Bank is likely to start reducing its massive $4.5 trillion portfolio sometime this year, but also that won't take much more rate hikes to reach a neutral level, providing the exact dose of confidence in the local economy, without overwhelming investors with higher rates. Within the Dow, only JP Morgan edged lower, ending the day -0.36%, while El du Pont was the best performer, up 2.89%, followed by Microsoft which gained 1.63%. The daily chart for the Dow shows that the index extended its recovery beyond its 20 DMA, whilst technical indicators aim north within positive territory, with plenty of room to extend their advances. In the 4 hours chart, the index stands far above all of its moving averages, with the 20 SMA now advancing above the 100 SMA, and technical indicators losing upward strength, retreating modestly from overbought levels.

Support levels: 21,499 21,451 21,406

Resistance levels: 21,527 21,581 21,640

FTSE100

London equities benefited from rising oil prices and the positive mood triggered by US Fed's Yellen among stocks' traders, as a slower pace or rate hikes usually supports demand for high-yielding assets. The Footsie added 88 points or 1.19% to settle at 7,416.93, accelerating north ahead of the close as US equities jumped to record highs. Pharmaceuticals and miners led the advance, with Mediclinic up 4.72%, followed by Burberry Group that gained 3.16% and Antofagasta that gained 3.14%. Micro Focus International was the worst performer, down 8.10%, followed by Pearson that shed 4.73%. The technical picture becomes to look more constructive in the daily chart, as the index advanced above its 20 and 100 DMAs, whilst technical indicators extended their advances, now entering positive territory. In the 4 hours chart, technical indicators began easing from near overbought levels, whilst the index is stuck around its 100 and 200 SMAs, but above a bullish 20 SMA, limiting chances of a bearish movement.

Support levels: 7,386 7,345 7,302

Resistance levels: 7,439 7,482 7,529

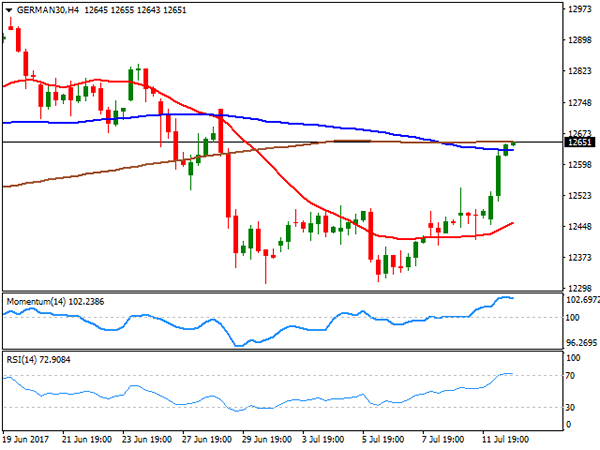

DAX

The German DAX closed at 12,626.58, up 192 points or 1.52%, as European equities soared after Fed's Chair Yellen cooled down expectations of more than a few rate hikes in the next few years. European indexes were already in the rise ahead of the announcement, back by energy and mining-related equities' gains. Within the DAX, only banks closed lower, with Commerzbank shedding 1.10% and Deutsche Bank down 0.72%. Automakers and pharmaceuticals were on the winning side also, but the best performer was Deutsche Post, up 2.67%, followed by Infineon Technologies that added 2.61%. The index advanced further in after-hours trading, following the lead of Wall Street, gaining upward potential in the daily chart, as the index recovered above its 20 DMA whilst technical indicators extended its advance, still below their mid-lines. In the 4 hours chart technical indicators have pared gains in overbought territory, whilst the index is now struggling around its 100 and 200 SMAs. Further gains seem likely for this Thursday, particularly if stocks' traders maintain the positive mood in Asia.

Support levels: 12,617 12,565 12,521

Resistance levels: 12,689 12,732 12,774

EUR/USD Seems Exhausted, EUR/GBP Breakout Needs Confirmation, EUR/CHF Upside Paused

EUR/USD seems exhausted

The currency pair increased in the morning, trying to recover after the yesterday's drop, is approaching an important confluence area, where could find resistance again. Price increases as the USDX is under massive selling pressure, the index is approaching the 95.50 psychological level, a drop below the 95.45 previous low will invalidate a rebound at this moment.

I've said in the last days that the USDX could continue to drop on the short term because could still be attracted by a major dynamic support before will really have enough bullish energy to start a broader upside movement.

The German Final CPI rose by 0.2%, matching expectations, while the French Final CPI may increase by 0.0%. We have a busy calendar today, so will be better to keep an eye on it as the US is to release high impact data, which will bring life on the EUR/USD.

Price increased and is very close to reach the confluence formed by the median line (ML) with the 1.1466 static resistance, we could have a trading opportunity from there. A valid breakout through this area will accelerate the rally, while a rejection will bring us a very good selling opportunity. Technically, another leg lower is favored after another false breakout above the median line (ML) and above the sliding line (sl). A strong selling opportunity will come if the Rising Wedge pattern will be confirmed.

EUR/GBP breakout needs confirmation

EUR/GBP dropped sharply in the yesterday's session and now is pressuring a broken dynamic resistance, this could be confirmed as a strong support if will hold. We may have a buying opportunity these days if the price stays much above the previous extended sideways movement.

Is pressuring the broken warning line (wl2), so we still need a confirmation that will resume the upside movement. We could have a buying opportunity if the rate will come down to test the confluence area formed by the median line (ML) with the warning line (wl2). The upside targets are at the 50% Fibonacci line (ascending dotted line), at the 0.9226 swing high and at the upper median line (UML) of the ascending pitchfork.

EUR/CHF upside paused

EUR/CHF decreased in the yesterday's trading session and could come back down to test and retest some important support levels before will try to climb towards new peaks. Has found strong resistance at a confluence area and now is into a corrective phase. The current retreat is natural after the impressive rally, dropped as much as 1.0997 level, but now is trading much above the 1.1000 psychological level.

Was rejected by the confluence formed by the upper median line (UML) with the median line (ml), could retest the WL1 and the lower median line (lml) of the ascending pitchfork in the upcoming days. The outlook remains bullish on the short term despite the minor retreat.

Yellen’s Dovish Tone

US equities continued upward on Wednesday, with the DJ30 improving 0.5% on the day and trading to an all-time high of 21,576.90. The impetus behind this was Fed Chair Yellen's testimony to Congress that she had confidence in the US economy and suggesting that US inflation will not force the Fed's hand. In other words, there will be no rush to tighten monetary policy (aka raise interest rates). USD fell against the majors and gold as the markets are still digesting the release of emails from Donald Trump Jr. regarding his controversial meeting with a Russian lawyer during last year's presidential campaign. The 'scandal' could delay US fiscal stimulus initiatives, which would hold back many corporations spending plans. As expected the Bank of Canada raised interest rates for the first time in 7 years, increasing the overnight rate from 0.5% to 0.75%. The interest rate increase had been widely expected after senior Bank of Canada officials signaled recently that lower rates had done their job, and the Canadian economy was performing well with growth for 2017 expected to improve to 2.8%.

USDJPY lost 0.4% on the day trading from an early high of 113.714 to a low on the day of 112.922. USDJPY is currently trading around 113.00.

EURUSD gave up some of its early gains after hitting a 14-month high of 1.14791. Currently EURUSD is trading around 1.1448.

Better than expected UK Payroll data, and UK Unemployment falling to a 43 year low of 4.5%, saw GBPUSD climb off early lows to trade as high as 1.29069 on the day. Similarly, EURGBP backed off from early highs giving up 0.5% on the day. However, wage growth continued to fall behind inflation which could result in interest rate increases being delayed as the UK Monetary Policy Committee have made it clear that they would want to see a 'firming' in wage growth before voting to raise rates. Currently, GBPUSD is trading around 1.2900 and EURGBP is around 0.8875.

With the expected 0.25% interest rate rise by the Bank of Canada, USDCAD continued its recent downward path with USD giving up over 1.6% on Wednesday to trade as low as 1.26955. The markets are expecting further growth in the Canadian economy which may lead to further rate increases before the end of 2017. USDCAD is currently trading around 1.2748.

Gold extended its recent gains gaining 0.5% on the day to trade as high as $1,225.60. Gold is currently trading around $1,223.70.

WTI rose above $46.50pb on Wednesday as data of declining inventories in the US raised hopes that the glut is easing. The U.S. Energy Information Administration reported that domestic crude supplies dropped 7.6 million barrels for the week ended July 7. However, OPEC stated on Wednesday that its oil production rose in June and forecasts that world demand for its crude will decline next year as rivals pump more, pointing to a market surplus in 2018 despite an OPEC-led output cut. WTI is currently trading around $45.55pb.

At 13:30 BST US Initial Jobless Claims (Jul 7) will be released. A reduction from the previous 248K to 245K is expected. If the continuing downward trend is maintained it will give further credence to a tightening labour market and improved economic growth.

Fed Chair Yellen continues her testimony to congress at 15:00 BST – markets are looking for further clues as to when the Federal Reserve will start reducing its balance sheet.

Equity Markets Cheer Dovish Yellen, Dollar Falls

Equity investors across the globe welcomed Chair of the Federal Reserve, Janet Yellen's testimony with open arms.

The Dow Jones Industrial Average jumped 123 points on Wednesday – a record high. The S&P 500 and Nasdaq Composite rallied 0.7% and 1.1% respectively. Meanwhile, the positive sentiment spread into Asian stocks, with all major indices surging across the board.

Although Yellen did not diverge from her statement at the most recent FOMC meeting by remaining committed to raising rates and reducing the Fed's balance sheet as the U.S. economy continues to grow, she was apparently worried about the inflation outlook.

U.S. monetary policy makers have been trying to convince the markets that the incline in inflation is temporary. However, Yellen's statement that "the Fed stands ready to adjust policy if it appears the inflation undershoot appears consistent" suggests that September rate hikes might be off the table for now and rates will not go much higher in the longer run.

The uncertainty about the course of inflation and the less hawkish tone from the Fed's Chair sent yields on long-term bonds lower, which dragged the dollar index down. The combination of low yields, a weak dollar and untightened financial conditions is welcomed by equity investors, thus expect to see a continuation of the equities rally, especially if earnings season does not disappoint.

Currency traders will need to watch today's U.S. PPI and tomorrow's CPI figures very carefully. Inflation data will likely be the dominant influence on the dollar's direction, and if prices do not show signs of strength, we are likely to see new lows on the greenback.

The most recent shift in statements from the central banks were translated yesterday, with Bank of Canada raising rates for the first time in nearly seven years. Markets are trying to figure out who is next in line to remove the extreme accommodative policies. Will it be Bank of England, European Central Bank, Sweden's Riksbank or Norges Bank? The bottom line here is central banks are no longer diverging from the Fed, and albeit on different trajectories, it seems a coordinated move towards tighter policies, which is likely to narrow the spreads in fixed income markets and keep the dollar under pressure.

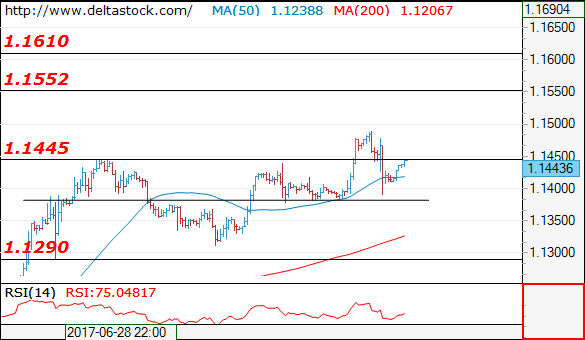

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1443

Despite yesterday's dip to 1.1390, the outlook remains bullish, for a rise towards 1.1550, en route to 1.1610. Crucial on the downside is 1.1380.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1490 | 1.1550 | 1.1380 | 1.1290 |

| 1.1550 | 1.1610 | 1.1380 | 1.1020 |

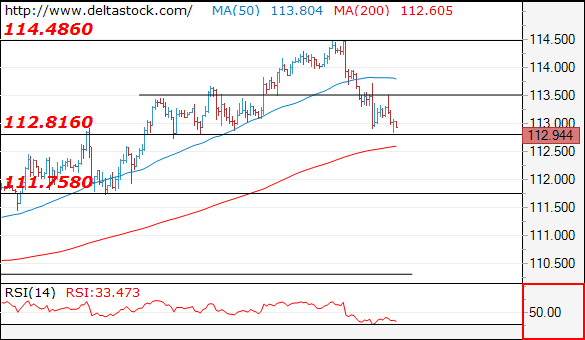

USD/JPY

Current level - 112.94

The bias remains bearish, for a break through 112.80, towards 111.75 zone. Initial resistance lies at 113.50.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 113.50 | 115.50 | 112.80 | 111.75 |

| 114.50 | 115.50 | 111.75 | 110.20 |

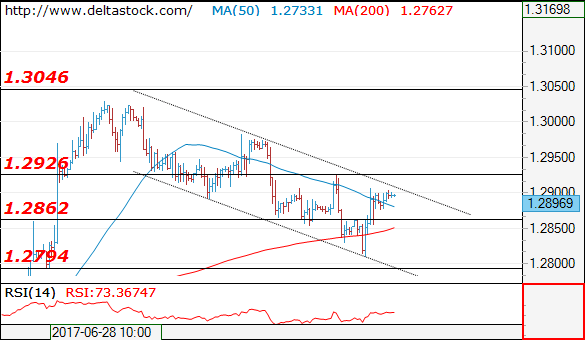

GBP/USD

Current level - 1.2896

Yesterday's dip to 1.2810 should be considered a completion of the whole slide from 1.3025 and my outlook here is bullish, for a break through 1.2920 crucial high, towards 1.3050 resistance. Initial intraday support lies at 1.2860.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2920 | 1.3050 | 1.2860 | 1.2635 |

| 1.2980 | 1.3500 | 1.2790 | 1.2480 |

BoC Hikes Interest Rates, Yellen Testimony, Remains Non-Committal

The Bank of Canada hike interest rates by 25 basis points as widely expected. The markets are expecting to see further rate hikes from the central bank which saw the Canadian dollar strengthening.

In the US, the Fed Chair Janet Yellen continued to remain non-committal in regards tofurther rate hikes. According to many economists, Yellen's congressional testimony suggested that a September rate hike is unlikely to happen. In her prepared remarks, the Fed chair said that the strong labor market would eventually put pressure on wages and inflation.

In the UK, the jobs data showed that the UK's unemployment rate fell to 4.5%, marking a 43-year low. Wages continued to remain mixed and weak with wages excluding bonuses posting a modest increase while wages including bonuses stayed subdued.

Looking ahead, Ms. Yellen will continue her second day of testimony to the US congress. The producer prices index data will also be coming out later today.

EURUSD intraday analysis

EURUSD (1.1436): The EURUSD closed bearish yesterday after posting a fresh intraday high at 1.1489. Price action is seen consolidating above the 1.1400 handle. On the 4-hour chart, we can see that EURUSD is currently trading within a rising wedge pattern. Expect to see a near term retest towards 1.1444 region. A reversal here by means of establishing resistance could signal a near-term weakness in price. Support comes in at 1.1312 - 1.1311 which could be tested on a downside breakout. Given the bullish momentum in the EURUSD, a breakout above 1.1444 could, however, signal continuation to the upside.

GBPUSD intraday analysis

GBPUSD (1.2897): The GBPUSD turned bullish yesterday, and the price action is expected to continue its consolidation at the current levels. On the 4-hour chart, the decline towards 1.2800 has not yet been complete which could suggest aweakness to the downside. However, if GBPUSD manages to break above 1.2890 level of resistance where it is trading currently, then expect further upside in price. The next technical resistance is found at 1.2970 which could be tested on the upside breakout.

USDJPY intraday analysis

USDJPY (113.04): The USDJPY broke below the downside range at 113.71 from the outside bar that was formed two days ago. The downside breakout was led by a strong bearish momentum. Therefore, we can expect to see a continuation to the downside with the next main support seen at 111.77 on the daily chart. On the 4-hour chart, price action is seen currently testing the lower end of the rising median line. Resistance is seen at 113.39 which could be tested in the near term. A reversal off this level will signal a continuation towards the initial support at 111.77 followed by a further decline to the next support at 110.81.

Currencies: Dollar Stays Soft Post-Yellen

Sunrise Market Commentary

- Rates: Counting down to tomorrow's US eco data

Today's eco calendar won't inspire trading. In light of most recent events (Yellen's Testimony), we expect that core bonds could correct somewhat higher without eking out technically relevant levels ahead of tomorrow's important US eco releases (CPI & retail sales). - Currencies: Dollar stays soft post-Yellen

The dollar was in the defensive ahead of Yellen's testimony before Congress. This picture didn't change as markets focus on Yellen's inflation comments. EUR/USD stabilizes near the recent top. USD/JPY corrects south. The dollar needs outright good news and that probably won't come today. The focus turns to tomorrow's US CPI and retail sales

The Sunrise Headlines

- US stock markets gained up to 1.1% after Fed Yellen's testimony suggested that the central bank gives some additional weight to disappointing inflation, suggesting a slow tightening cycle. Asian markets copy WS overnight.

- China reported better-than-expected June trade data, suggesting the economy is holding up well thanks to firmer global demand, despite a cooling property market at home amid a financial crackdown that has put firms under pressure.

- The US economy expanded at a 'slight to moderate' rate in June, with the labour market continuing to tighten and price growth still modest, the Federal Reserve said in its anecdotal Beige Book report.

- The Bank of Korea held its seven-day repo rate unchanged at 1.25%, after last cutting rates by 25 bps in June 2016. The Korean won firmed though as the BoK upgraded GDP forecasts.

- Senate Majority Leader McConnell faced intensifying pressure from President Trump to push through a health-care overhaul next week, but he appeared to make little progress in bridging the deep divides imperilling his party.

- The German government has expanded its powers to block the takeover of German companies amid growing concerns in Berlin at the scale of Chinese deal making in the German high-tech sector.

- Today's eco calendar is thin with only final national EMU inflation data, US weekly jobless claims and US PPIO. It's the second day of Yellen's testimony before US Congress and Therese May presents her Repeal Bill to UK parliament. The US, Ireland and Italy tap the market

Currencies: Dollar Stays Soft Post-Yellen

USD declines further on 'political noise'

The dollar started the session on a weak footing yesterday as markets pondered the potential fall-out from the Trump Jr. emails. Gradually, the focus turned to Yellen's statement before Congress. Yellen stayed close to the Fed's assessment from June, but indicated that soft inflation needs close monitoring. The USD reaction was mixed. USD/JPY stayed under pressure even as equities rallied. The pair closed the session at 113.17. EUR/USD reversed an initial topside test to finish the day at 1.1412.

Asian equities join the post-Yellen rebound on WS, but there is a loss of momentum as the session evolves. Strong Chinese foreign trade data (both imports and exports stronger than expected) are supporting Chinese and Australian markets. Chinese data and an overall soft dollar propelled AUD/USD close to the 0.77 mark. USD/JPY underperforms despite recent attempts by the BoJ to cap the rise in Japanese yields. USD/JPY hovers in the low 113 area. EUR/USD trades in the 1.1440 area, holding within reach of the recent top.

Today, there are again only second tier eco data in Europe. In the US, jobless claims and the PPI producer prices will be published. Headline and core PPI are expected to rise 0.2% M/M, but Y/Y-measures are expected to ease to 1.9% and 2.0% respectively. The focus will be on tomorrow's key US data (CPI, retail sales, Michigan confidence). However, disappointing PPI data might keep the dollar in the defensive. Yellen will bring the second part of her semi-annual testimony before the Senate. Fed's Brainard will also speak. She spoke rather soft of late.

Dollar sentiment remained fragile after Friday's payrolls. The potential political fall-out Donald Trump Jr's leaked emails was an additional source of USD caution. Yesterday's assessment of Fed's Yellen before Congress was balanced, but the market gave most weight to some pockets of Fed softness on inflation. This keeps the dollar in the defensive, even as the reaction was slightly different across USD cross rates. We expect USD softness to persist going into tomorrow's US CPI and retail sales. The dollar needs outright good news to succeed a sustained rebound and this news probably won't to come today, keeping the dollar near the recent lows. US politics remain a wildcard. Of late, the political headlines were USD negative. We also keep a close eye on whether Congress can reach a deal on healthcare in the near future. If realized, the political context might become less USD negative. For now, this is only hypothetical thinking and it is too early to play this card in a daily perspective.

Technical picture: USD looking for a bottom

A combination of hawkish ECB comments and soft US data pushed EUR/USD above the 1.1300/66 resistance area end June. The payrolls were not good enough to trigger a sustained USD rebound. Next resistance in the 1.15 area is looming. LT-correction tops stand at 1.1616/1.1714. A break would end the long consolidation period that followed the sharp decline of EUR/USD in 2014/early 2015. Such a key area will be difficult to break for now. A return below the 1.13 area would be a first indication of a loss in upside momentum. EUR/USD 1.1119/10 is the next important support.

The USD/JPY rally ran into resistance in early May and the pair returned lower in the 108.13/114.37 range. The post-Fed USD rebound pushed the pair above the 112.13 correction top, but follow-through gains remain modest. USD/JPY 114.37 resistance was tested, but for now the test is rejected. This at least suggests a pause in the recent USD/JPY uptrend. We stay cautious on USD/JPY long positions despite the recent good performance.

EUR/USD stays near correction top post-Yellen on broad-based USD softness

EUR/GBP

Brexit to return as factor for sterling trading?

Sterling was again in better shape yesterday after a sharp correction on Tuesday. The May UK labour market report was solid. The unemployment rate dropped to a multi-decade low of 4.5% and job growth was stronger than expected. Weekly earnings rose modestly from 1.8% Y/Y to 2.0% Y/Y (1.9% Y/Y was expected). This leaves real wage growth negative given a May inflation reading of 2.9%. The jury is still out what this means for the August BoE policy decision, but the report was good enough to trigger profit taking on sterling shorts. EUR/GBP returned below the 0.89 barrier and closed the session at 0.8857, reversing most of Tuesday's gain. Cable also rebounded, partially supported by underlying USD softness. The pair finished the day at 1.2885.

Overnight, the UK RICS house price balance was weaker than expected (7% vs. 15%). The report has little impact on sterling trading. Markets will keep a close eye of the Brexit 'Repeal Bill'. This will provide the groundwork for post-Brexit UK legislation. The approval will be key for May's political fate. Of late, Brexit and political issues were only of second tier importance for sterling trading. Political uncertainty might return to the forefront, at least temporary.

From a technical point of view, EUR/GBP set a minor top north of 0.8854/66 resistance (2017 top), but initially a sustained break didn't occur. However, a sharp short-squeeze propelled the pair north of 0.89 earlier this week. Quite some sterling negative news should already be discounted at current levels. Even so, the short-term trend remains euro positive/sterling negative. A test of the 0.90 barrier might be on the cards.

EUR/GBP technical break higher needs to be confirmed