Sample Category Title

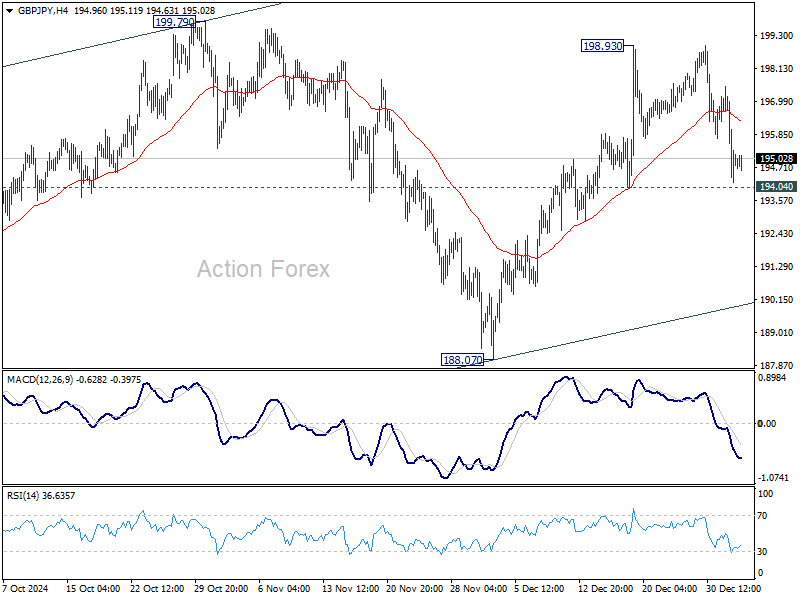

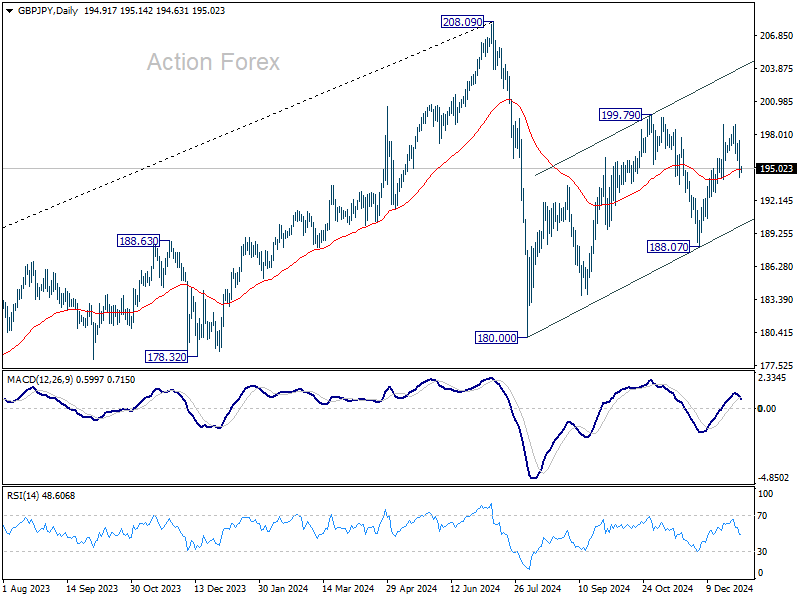

GBP/JPY Daily Outlook

Daily Pivots: (S1) 193.63; (P) 195.58; (R1) 196.97; More...

Intraday bias in GBP/JPY remains neutral for the moment. Further rise is still in favor with 194.04 minor support intact. Corrective pattern from 180.00 is extending with another rising leg. On the upside, above 1999.79 will will target channel resistance (now at 203.90). However, firm break of 194.04 will turn bias to the downside fro 188.07 support instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

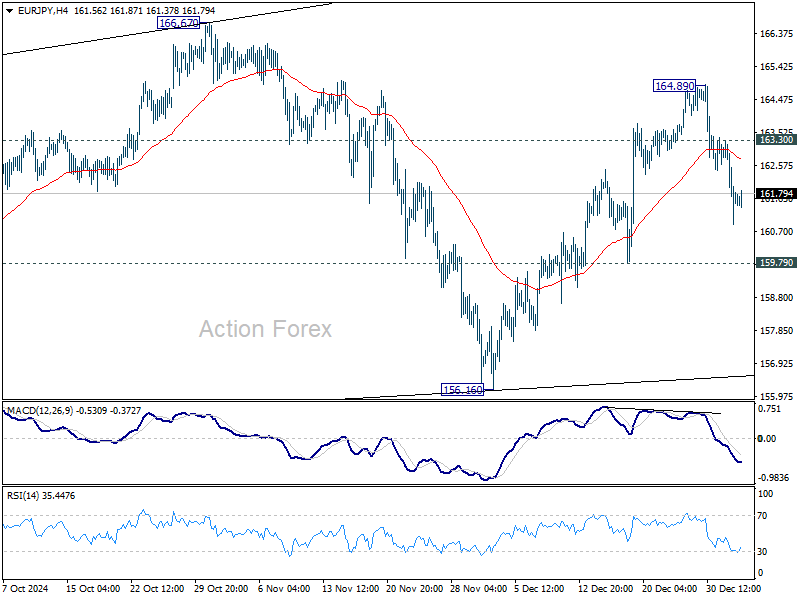

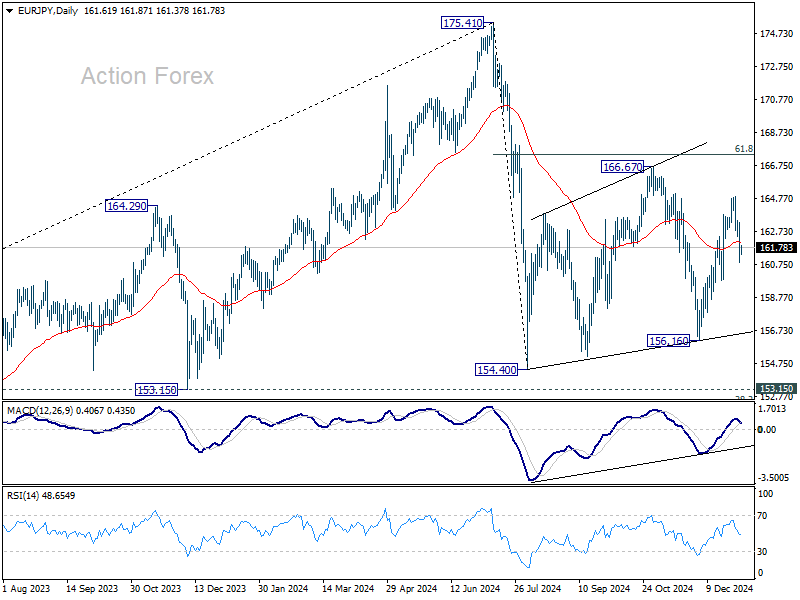

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.65; (P) 161.98; (R1) 163.06; More...

Intraday bias in EUR/JPY remains neutral for the moment. Some more consolidations could be seen, but another rally is mildly in favor as long as 159.79 support holds. Above 163.30 minor resistance will turn bias back to the upside. Rise from 156.16 is seen as a rising leg in the corrective pattern from 154.04. Break of 164.89 will target 166.67 resistance next.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

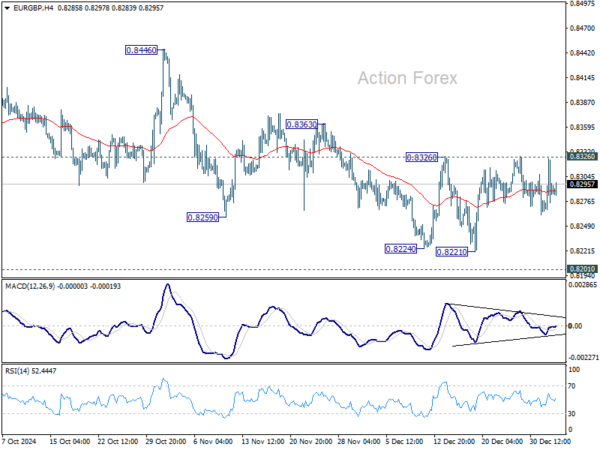

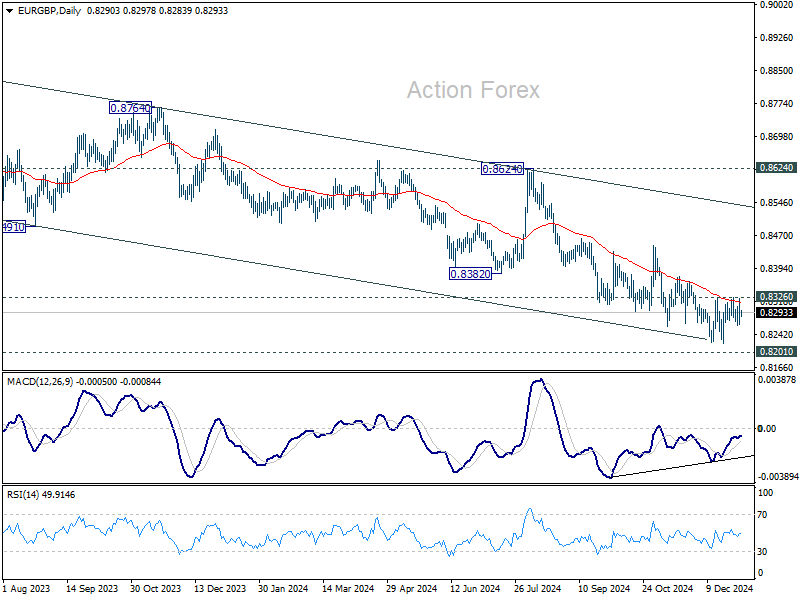

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8263; (P) 0.8295; (R1) 0.8324; More...

No change in EUR/GBP's outlook as range trading continues. Intraday bias remains neutral for the moment. On the upside, firm break of 0.8326 resistance will confirm short term bottoming at 0.8221, ahead of 0.8201 key support. Intraday bias will be turned back to the upside for 0.8446 structural resistance next.

href="https://www.actionforex.com/wp-content/uploads/2025/01/eurgbp20250103a1.png">

In the bigger picture, focus is now on whether 0.8201 key support (2022 low) is strong enough to complete the whole down trend from 0.9267 (2022 high). In any case, medium term outlook will be neutral at best until decisive break of 0.8624 key resistance. Otherwise, risk will stay on the downside even in case of strong rebound.

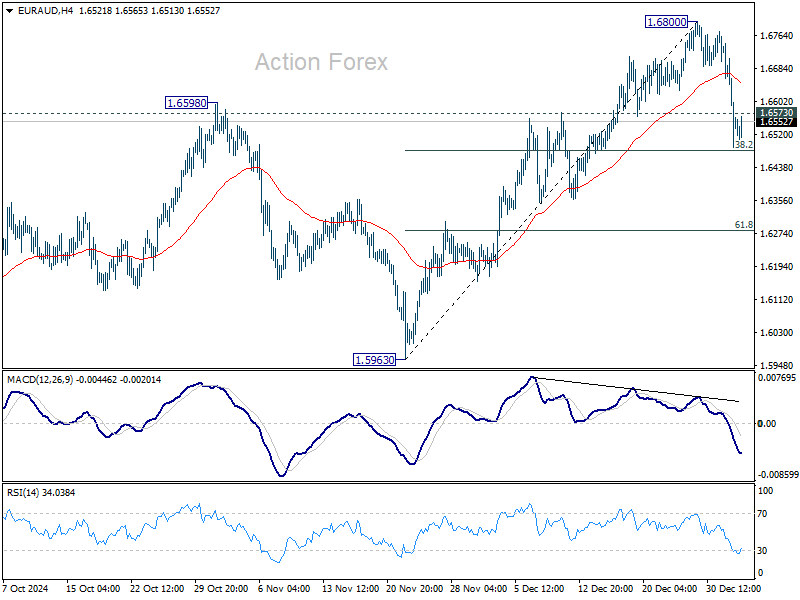

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6441; (P) 1.6600; (R1) 1.6710; More...

EUR/AUD's pull back from 1.6800 extended lower today and intraday bias is now on the downside. Firm break of 38.2% retracement of 1.5963 to 1.6800 at 1.6480 will bring deeper fall to 61.8% retracement at 1.6283. For now, risk will stay mildly on the downside as long as 1.6800 resistance holds, in case of recovery.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed and deeper decline would be seen.

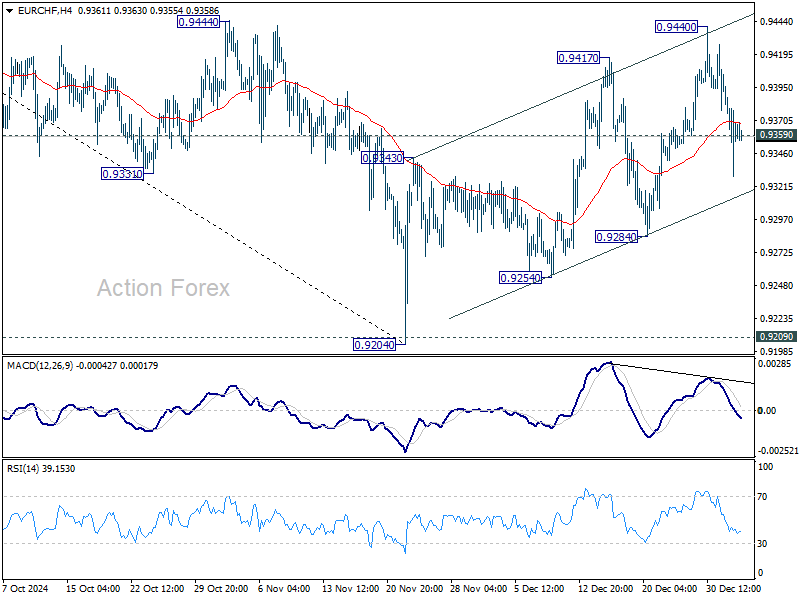

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9333; (P) 0.9365; (R1) 0.9401; More....

Intraday bias in EUR/CHF is back on the downside with break of 0.9359 minor support. Deeper fall should be seen to 0.9284 support next. Rebound from 0.9204 is current seen as a corrective move. In case of another rise through 0.9440, strong resistance would be seen from 0.9481 fibonacci resistance to limit upside.

In the bigger picture, a medium term bottom is probably in place at 0.9204. More consolidations would be seen above there with risk of stronger rebound to 38.2% retracement of 0.9928 to 0.9204 at 0.9481. But outlook will remain bearish as long as 0.9481 holds and another fall through 0.9204 to resume larger down trend is in favor.

EUR/USD Started 2025 at Its Lowest Point in 25 Months

According to the EUR/USD chart, on 2nd January, the first trading day of the year, the EUR/USD pair fell below the psychological level of 1.025, the lowest mark since November 2022.

There are few news events, and the EUR/USD rate decline may be attributed to:

→ The holiday period still affecting financial markets, reducing liquidity and creating vulnerabilities for volatility spikes;

→ Market participants potentially rebalancing their portfolios for the new calendar year;

→ Reassessing the strength of the dollar amid uncertainty about the actual steps of President-elect Trump, whose inauguration is scheduled for this month.

Meanwhile, technical analysis of the EUR/USD chart reveals that:

→ In 2024, price fluctuations formed a downward channel, with key pivot points marked by red circles. Notably, the previous holiday period led to the formation of the first of these points.

→ The bullish "Cup and Handle" pattern, which we discussed on 30th December, resulted in a false bullish breakout (indicated by an arrow). Seizing the bulls' failure, the bears pushed the price to the lower boundary of the mentioned channel.

The area where the lower boundary of the channel intersects the psychological level of 1.025 could serve as strong support. The recovery observed on the morning of 3rd January may confirm this.

The holiday period may lead to the formation of a new key pivot point on the EUR/USD chart, as has happened before.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

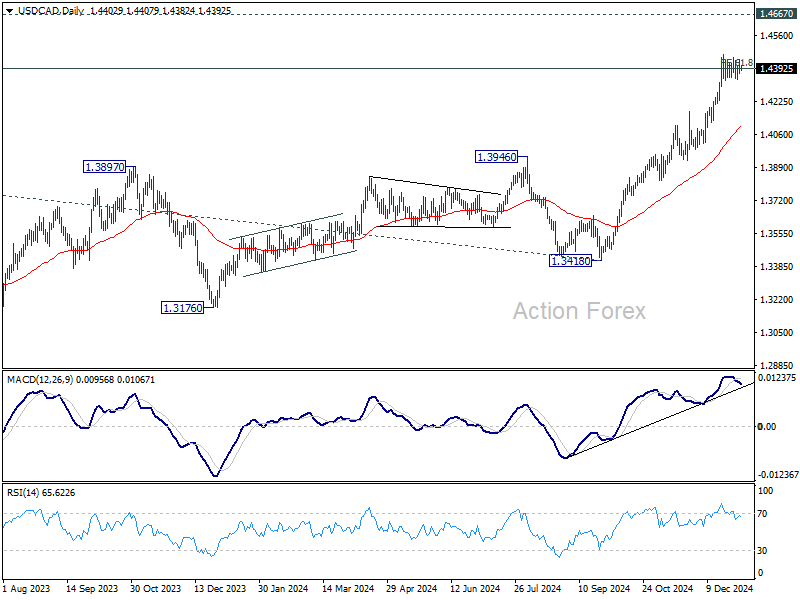

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4367; (P) 1.4405; (R1) 1.4440; More...

USD/CAD is staying in consolidations below 1.4466 and intraday bias remains neutral. Another retreat cannot be ruled out, but outlook will stay bullish as long as 1.4177 resistance turned support holds. On the upside, break of 1.4466 and sustained trading above 1.4391 will pave the way to retest 1.4667/89 long term resistance zone.

In the bigger picture, up trend from 1.2005 (2021) is in progress and met 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391 already. Sustained trading above there will pave the way to 1.4667/89 key resistance zone (2020/2015 highs). Medium term outlook will remain bullish as long as 1.3976 resistance turned holds, even in case of deep pullback.

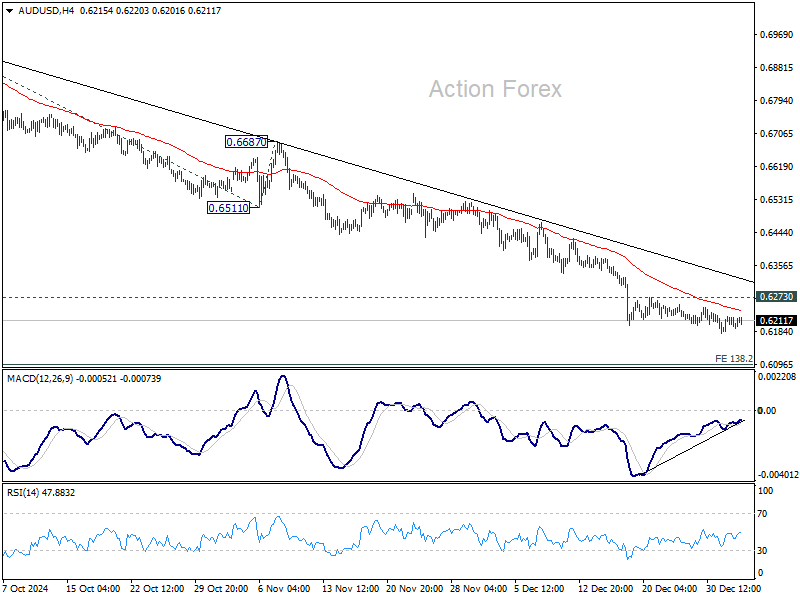

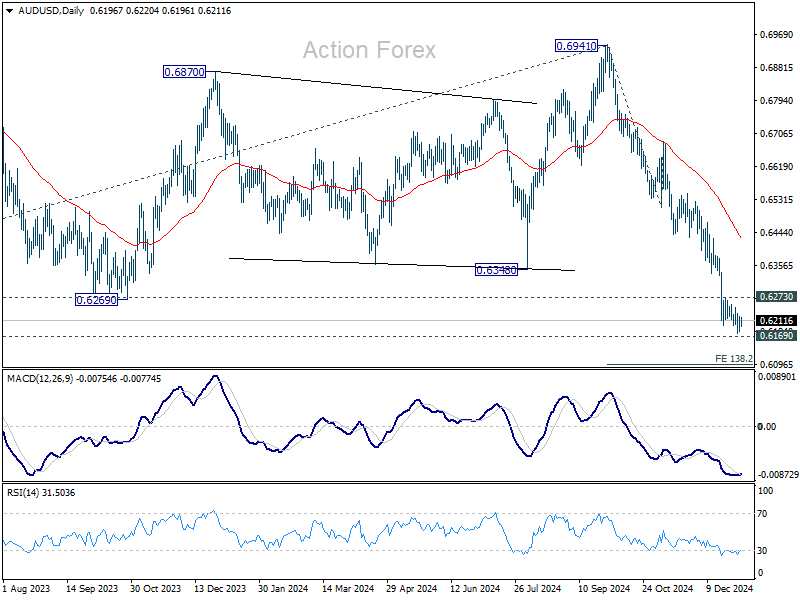

AUD/USD Daily Report

Daily Pivots: (S1) 0.6183; (P) 0.6203; (R1) 0.6224; More...

Intraday bias in AUD/USD remains mildly on the downside despite loss of momentum as see in 4H MACD. Current fall from 0.6941 should target .6169 long term support, and then 138.2% projection of 0.6941 to 0.6511 from 0.6687 at 0.6074. However, considering bullish convergence condition in 4H MACD, break of 0.6273 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. Firm break of 0.6169 support will confirm down trend resumption for 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6573) holds.

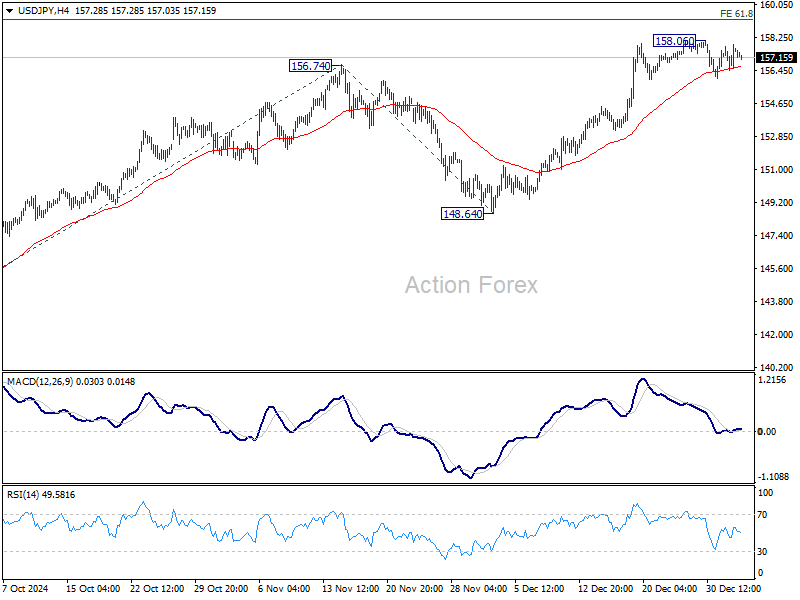

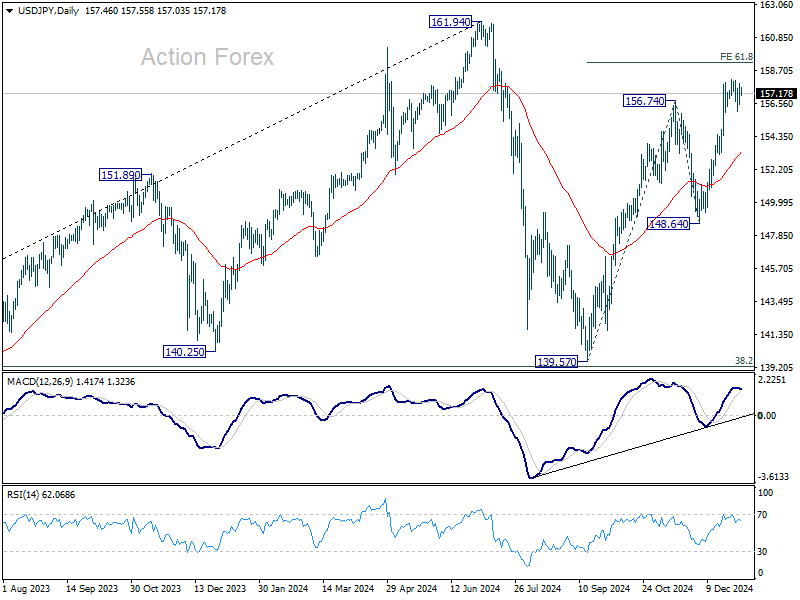

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.69; (P) 157.27; (R1) 158.10; More...

Intraday bias in USD/JPY stays neutral as consolidations continue below 158.06. While another retreat cannot be ruled out, outlook will stay bullish as long as 55 D EMA (now at 153.34) holds. On the upside, above 158.06 will resume the rally from 139.57 to 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25. Firm break there will pave the way back to 161.94 high.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

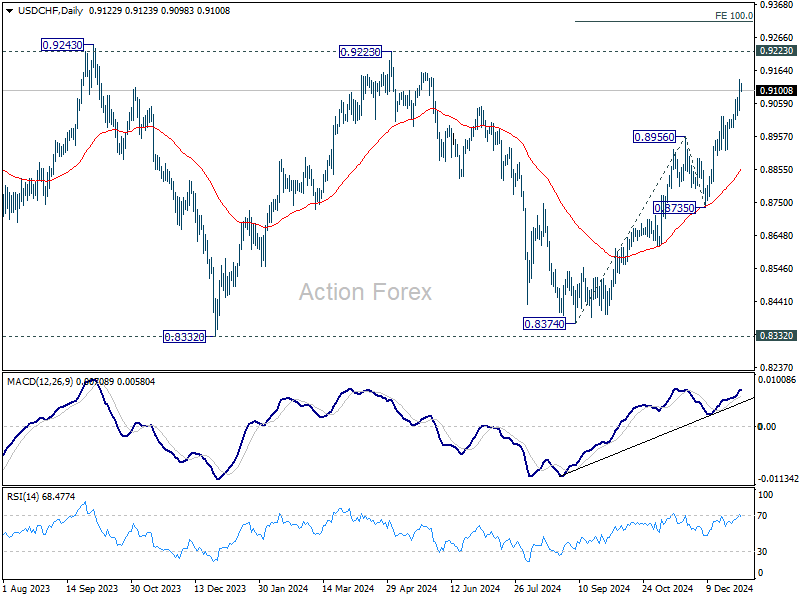

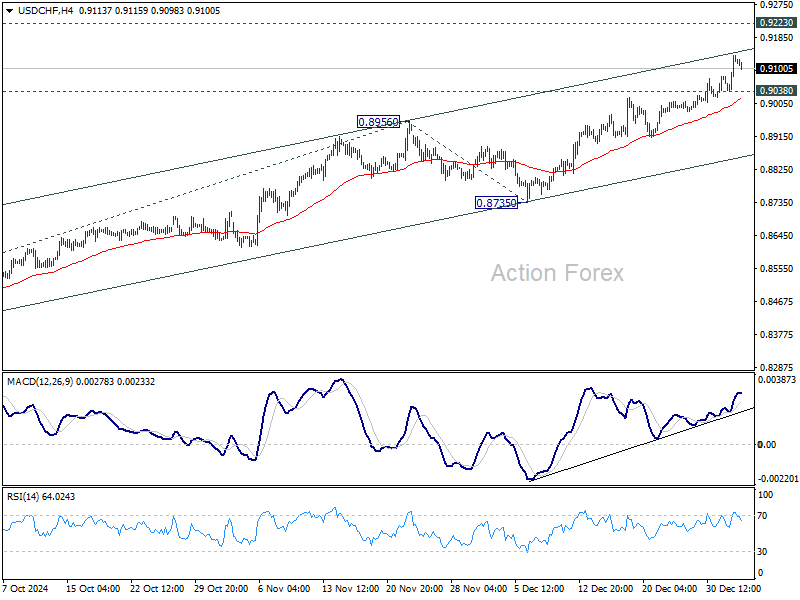

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9063; (P) 0.9100; (R1) 0.9161; More…

Intraday bias in USD/CHF remains on the upside as rally from 0.8374 is in progress. Next target is 0.9223 key resistance. Strong resistance is expected there to limit upside, at least on first attempt. On the downside, below 0.9038 minor support will turn intraday bias neutral first. Nevertheless, decisive break of 0.9223 will carry larger bullish implications.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.