Sample Category Title

Brent Crude – Oil Eyes Break of Key Confluence Level on Chinese Optimism

- Oil prices rose due to declining US stockpiles and renewed Chinese optimism after President Xi Jinping pledged to promote growth.

- Mixed results from Chinese manufacturing data may indicate that government stimulus programs are starting to work.

- A Reuters poll predicts oil prices will remain around $70 a barrel in 2025.

- From a technical perspective, price action suggests a breakout may be imminent.

Oil prices have been on a march higher this week thanks to declining US stockpiles and renewed Chinese optimism. The first trading day of the new year began with an optimistic eye on China’s economy and fuel demand after a pledge by President Xi Jinping to promote growth.

Has Chinese Data Turned the Corner?

China’s factory activity increased in December, according to a Caixin/S&P Global survey on Thursday, but it grew more slowly than expected due to worries about the impact of tariffs proposed by U.S. President-elect Donald Trump on trade.

This follows the NBS manufacturing and non-manufacturing data released on Tuesday. The NBS data was mixed with non-manufacturing PMI data coming in better than expected while the manufacturing data dropped from November but remains above the key 50 level. Market participants may be seeing this as a sign that Government stimulus programs announced at the back end of 2024 may be starting to pay dividends.

Some analysts believe that weaker Chinese data might actually boost oil prices, as it could lead Beijing to speed up its stimulus efforts.

At present developments around China may be crucial to oil prices moving forward and worth keeping an eye on.

Reuters Poll & Other Notable News

Oil prices are expected to stay around $70 a barrel in 2025, marking the third year of decline after dropping 3% in 2024. This is due to weak demand from China and increasing global supplies, which are counteracting OPEC+’s attempts to support the market, according to a Reuters poll.

As we have said above, demand and the stimulus question around China will be central to Oil prices in 2025.

US data on Friday may provide further insight to the performance of the US economy as markets brace for a Trump Presidency. OPEC+ will be watching closely as rumors of slashing regulations and increasing Oil output from the US could also be crucial factors moving forward.

Technical Analysis

From a technical perspective, Oil prices are eyeing a break above a key level of confluence. The level around 76.35 has kept gains at bay since price broke below this level on October 14, 2024.

Looking at price action and the rangebound nature we have seen over the past 3 months, it points to an imminent breakout.

Usually the longer a instrument remains in a tight range and price toils, it precedes a breakout.

A break above the the 76.35 handle could bring the 200-day MA into focus at 79.66. However before that we do have some resistance resting at 78.97.

A rejection of 76.35 may retest support at the 100-day MA resting at 74.68 before the 72.38 handle comes into focus.

Brent Crude Oil Daily Chart, January 2, 2024

Source: TradingView (click to enlarge)

Support

- 74.68

- 72.38

- 70.00 (psychological level)

Resistance

- 76.35

- 78.97

- 79.66

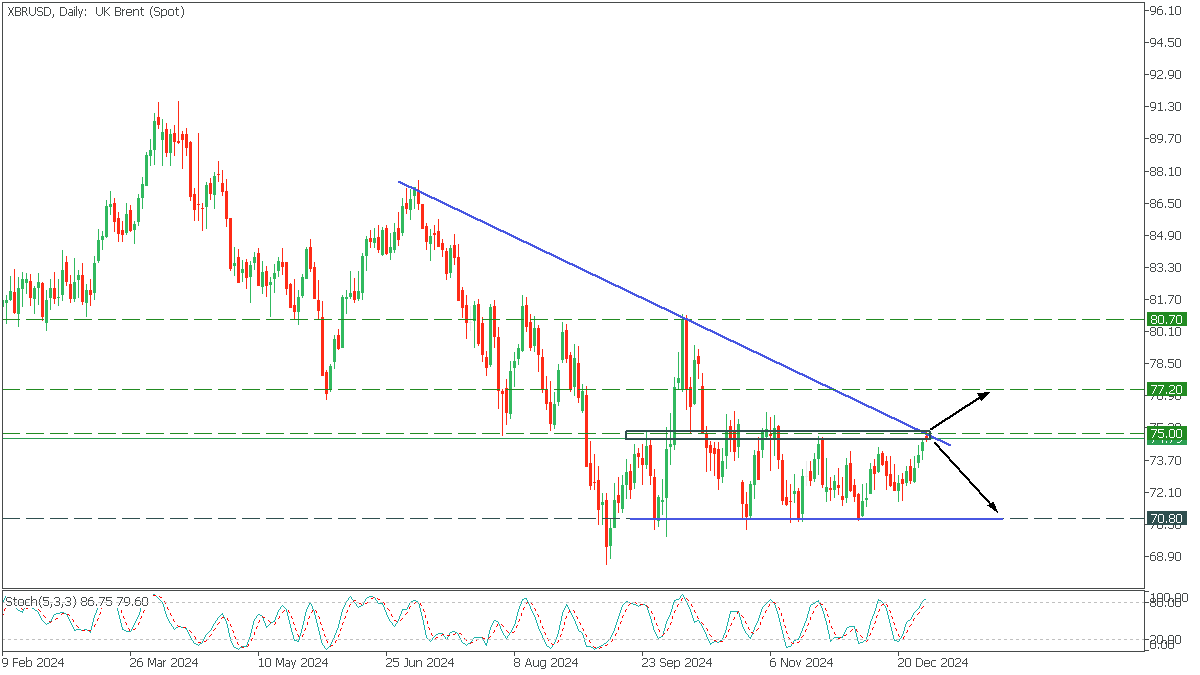

XBRUSD: Global Trend Test

XBRUSD, Daily

In the Daily timeframe, XBRUSD is forming a descending triangle, but the price has reached the upper trendline, testing a critical resistance level. Despite the bullish momentum, the Stochastic indicates overbought.

- A break of the trend line above 75.00 will start XBRUSD rising to 77.20;

- A rebound from the trendline will drop Brent back to 70.80;

UK PMI manufacturing finalized at 47, sentiment at two-year low

UK PMI Manufacturing was finalized at 47.0 in December, down from 48.0 in November, marking the third consecutive month of contraction. Persistent challenges, both domestic and international, weighed heavily on the sector, resulting in the sharpest production decline in nearly a year.

Rob Dobson, Director at S&P Global Market Intelligence, highlighted a “stalling domestic economy, weak export sales, and future cost concerns” as key drivers of the downturn. Business confidence fell to its lowest point in two years.

Small and medium-sized enterprises have been hit hardest during the downturn, while labor market pressures intensify. December saw the steepest job cuts since February, as firms moved to restructure in anticipation of 2025 National Insurance and minimum wage increases. Export sales also suffered due to weaker demand from Europe, Asia, and the US.

Input costs continued to rise, fueled by higher transportation, labor, and material expenses, with some increases linked to ongoing supply chain challenges. Looking ahead, the impact of Budget 2025 measures is expected to drive costs higher, potentially complicating BoE’s decision on further rate cuts despite mounting signs of economic stress.

Eurozone PMI manufacturing finalized at 45.1, Spain outshines peers with low China exposure

Eurozone PMI Manufacturing was finalized at 45.1 in December, down from November's 45.2, marking the sector’s 30th consecutive month of contraction. Key indicators, including new orders and inventory levels, signaled ongoing struggles across the bloc.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, emphasized the continued downturn: “New orders have dropped even more than in the previous two months, crushing any hopes for a quick recovery.” Inventories of intermediate and finished goods declined sharply, reflecting weak demand expectations.

Job cuts persisted across Eurozone, with the pace of reductions remaining significant, despite a slight deceleration. This trend is expected to continue as companies restructure operations amid weak industrial activity.

Spain remained a bright spot, with its PMI rising to 53.3, indicating robust expansion. Greece also posted growth at 53.2, a five-month high. However, the largest economies continued to struggle: Germany (42.5) reached a three-month low, France (41.9) fell to a 55-month low, and Italy (46.2) managed only a slight improvement.

Spain’s relative resilience stems from its low export exposure to China (2%) and benefits from lower energy costs, which have helped it weather the industrial crisis better than its peers. However, with Spain accounting for only 12% of Eurozone GDP, its strength alone cannot offset the widespread industrial recession.

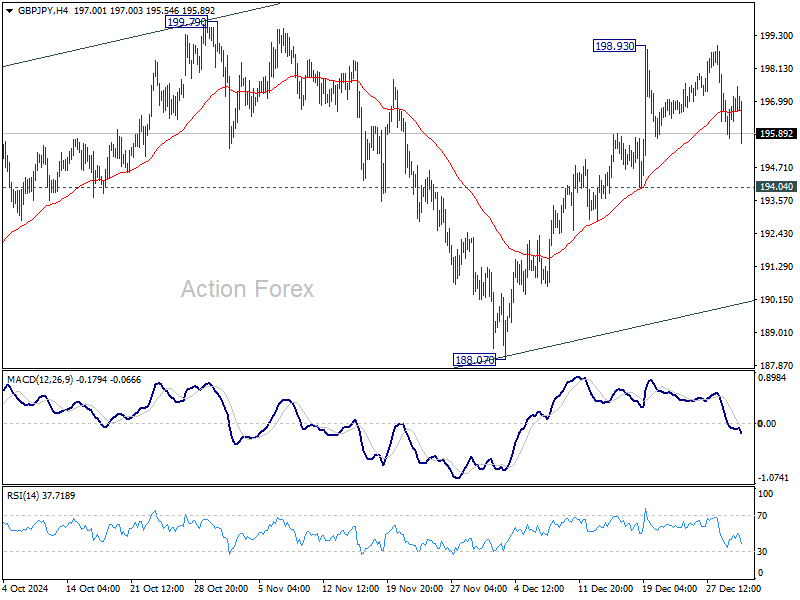

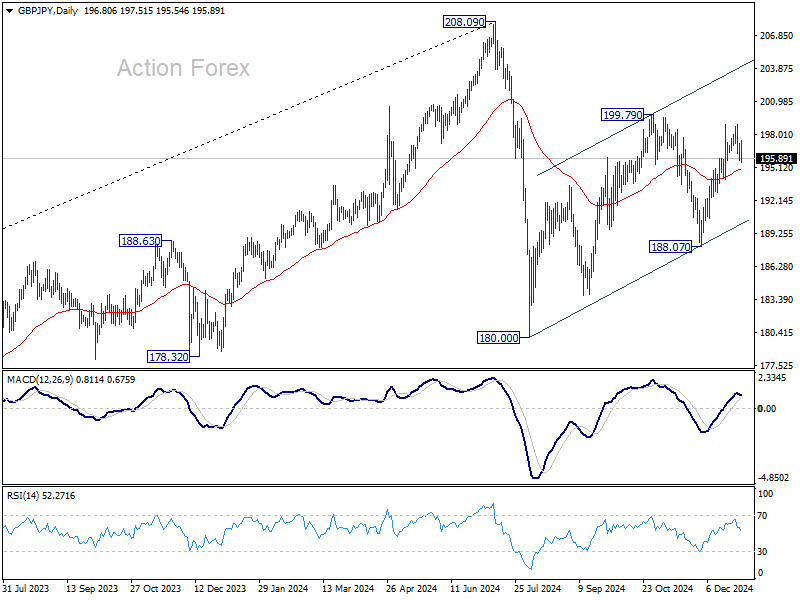

GBP/JPY Daily Outlook

Daily Pivots: (S1) 195.99; (P) 197.48; (R1) 198.63; More...

Range trading continues in GBP/JPY and intraday bias remains neutral. Corrective pattern from 180.00 is extending with another rising leg. Further rise is expected as long as 194.04 support holds. On the upside, above 1999.79 will will target channel resistance (now at 203.90).

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

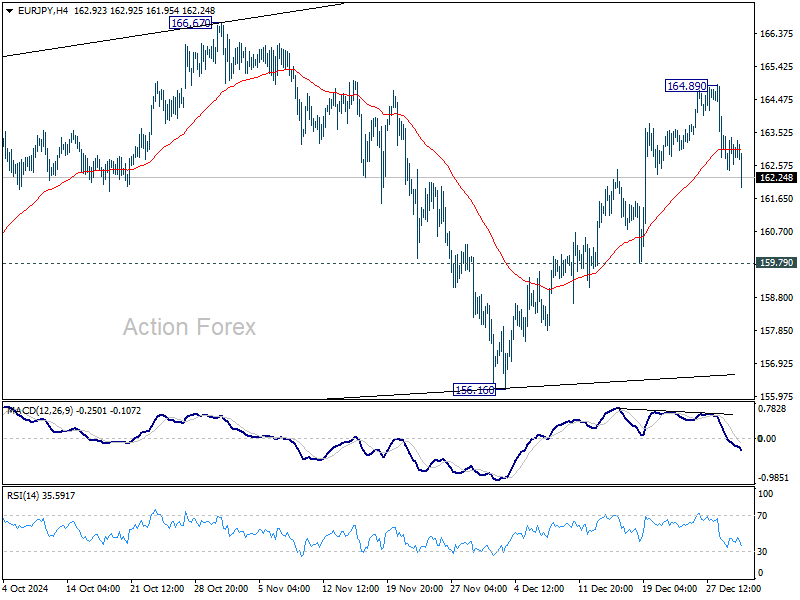

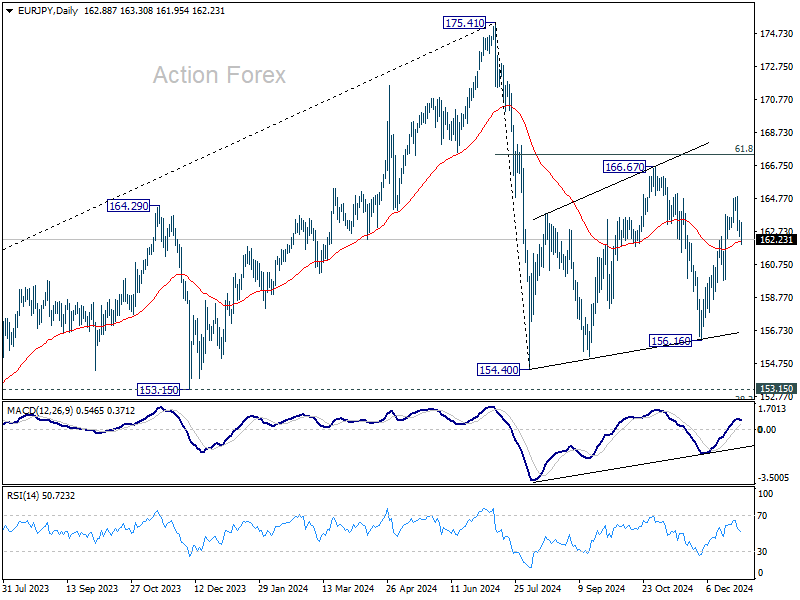

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.26; (P) 163.58; (R1) 164.39; More...

Intraday bias in EUR/JPY is turned neutral first with current retreat. Some consolidations would be seen, but another rise is mildly in favor as long as 159.79 support holds. Rise from 156.16 is seen as another rising leg in the corrective pattern from 154.04. Above 164.89 will target 166.67 resistance next.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

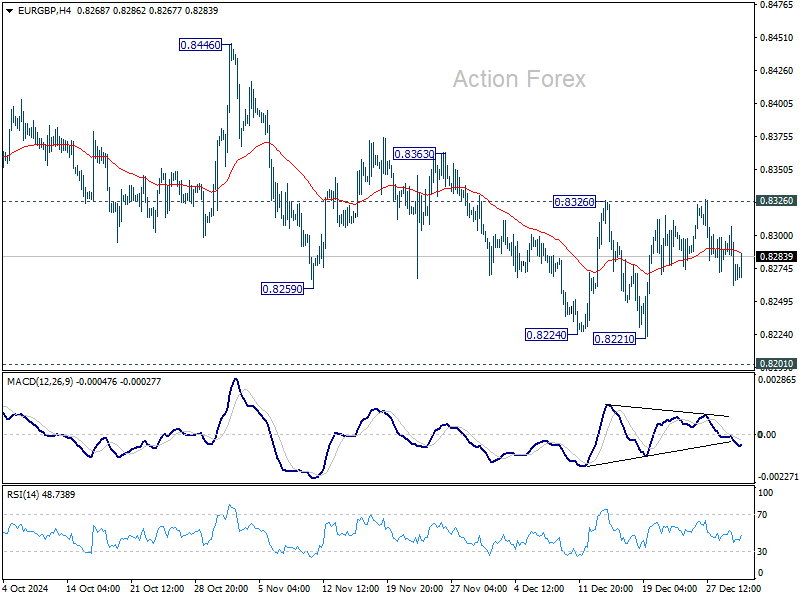

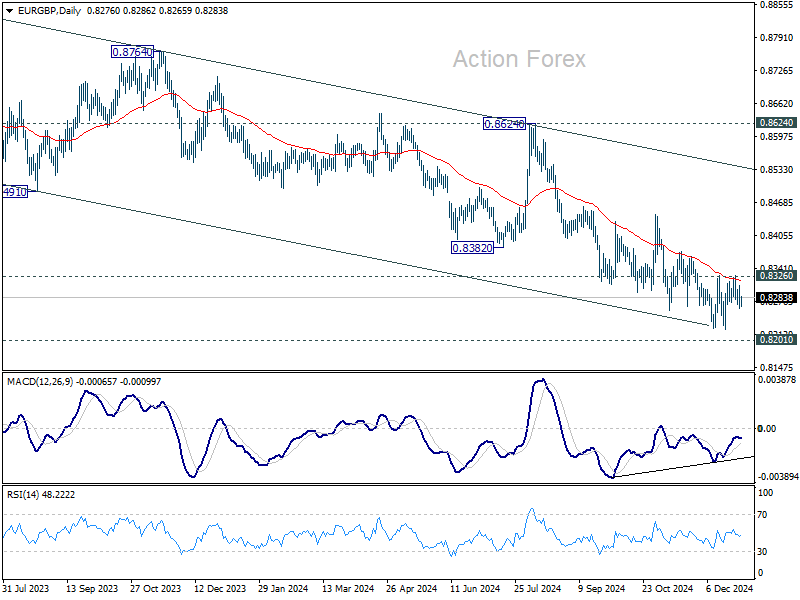

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8264; (P) 0.8284; (R1) 0.8298; More...

EUR/GBP is still bounded in range of 0.8221/8326 and intraday bias stays neutral. On the upside, firm break of 0.8326 resistance will confirm short term bottoming at 0.8221, ahead of 0.8201 key support. Intraday bias will be turned back to the upside for 0.8446 structural resistance next.

In the bigger picture, focus is now on whether 0.8201 key support (2022 low) is strong enough to complete the whole down trend from 0.9267 (2022 high). In any case, medium term outlook will be neutral at best until decisive break of 0.8624 key resistance. Otherwise, risk will stay on the downside even in case of strong rebound.

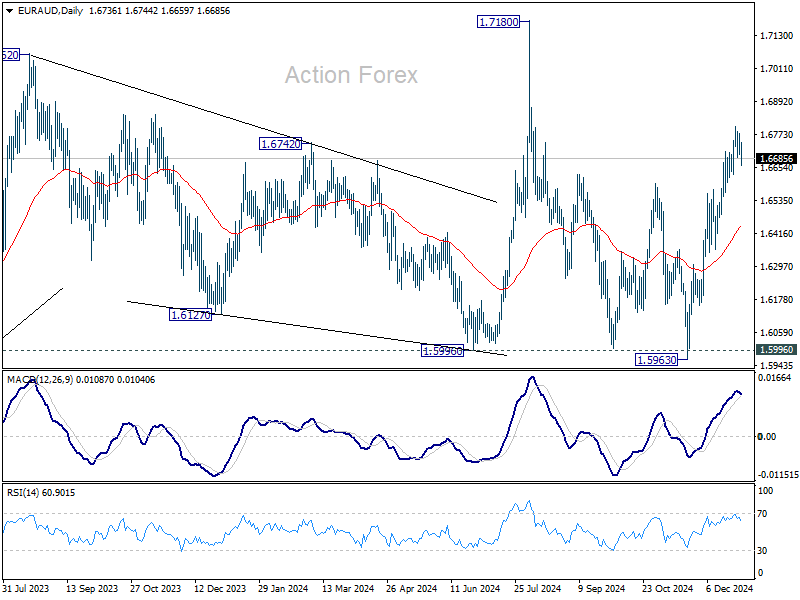

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6695; (P) 1.6733; (R1) 1.6774; More...

Intraday bias in EUR/AUD remains neutral and some more consolidations would be seen below 1.6800. Outlook will stay bullish as long as 1.6573 resistance turned support holds. Above 1.6800 will resume the rally from 1.5963 to retest 1.7180 high next. However, considering bearish divergence condition in 4H MACD, firm break of 1.6573 will confirm short term topping, and turn bias back to the downside instead.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed and deeper decline would be seen.

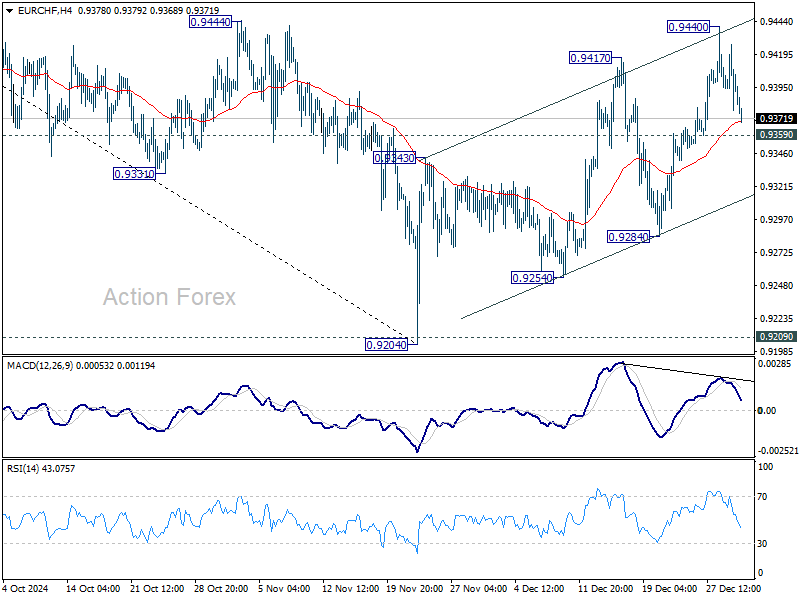

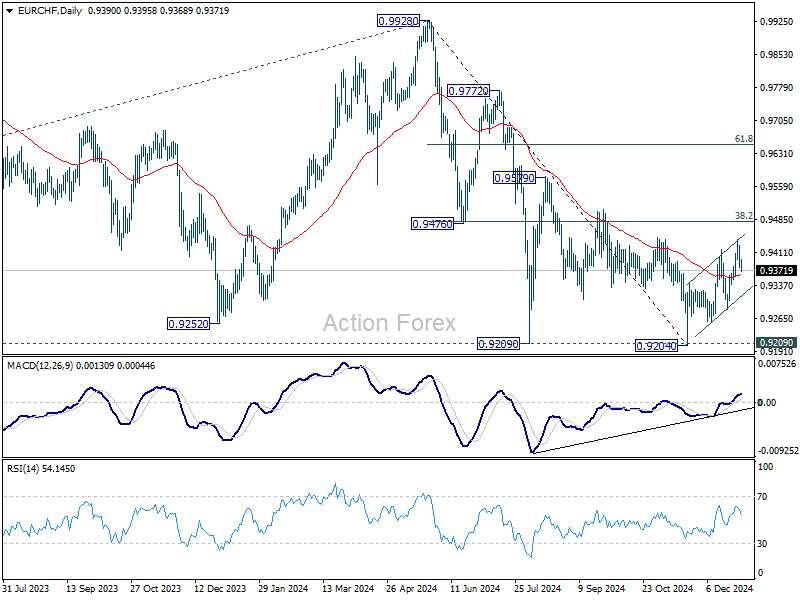

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9378; (P) 0.9412; (R1) 0.9440; More....

EUR/CHF retreated notably after rising to 0.9440 and intraday bias is turned neutral first. On the upside, break of 0.9440 will resume the corrective rebound from 0.9204 to 0.9481 fibonacci resistance next. On the downside, below 0.9359 minor support will turn intraday bias back to the downside for 0.9284 support instead.

In the bigger picture, a medium term bottom is probably in place at 0.9204. More consolidations would be seen above there with risk of stronger rebound to 38.2% retracement of 0.9928 to 0.9204 at 0.9481. But outlook will remain bearish as long as 0.9481 holds and another fall through 0.9204 to resume larger down trend is in favor.

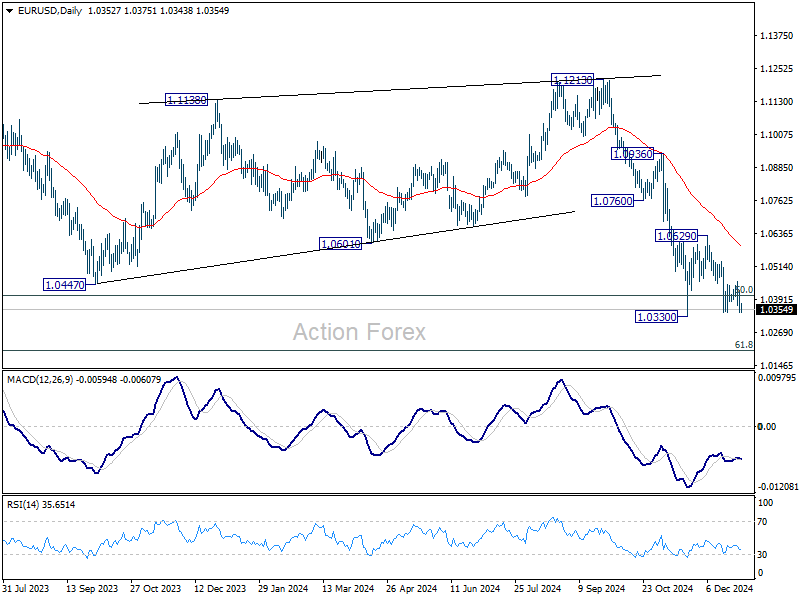

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0321; (P) 1.0389; (R1) 1.0429; More...

EUR/USD's sideway trading continues above 1.0330 and intraday bias remains neutral. Stronger recovery cannot be ruled out, but outlook will remain bearish as long as 1.0629 resistance holds. Firm break of 1.0330 will confirm resumption of whole decline from 1.1213. Sustained trading below 1.0404 fibonacci level will carry larger bearish implications.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.