Sample Category Title

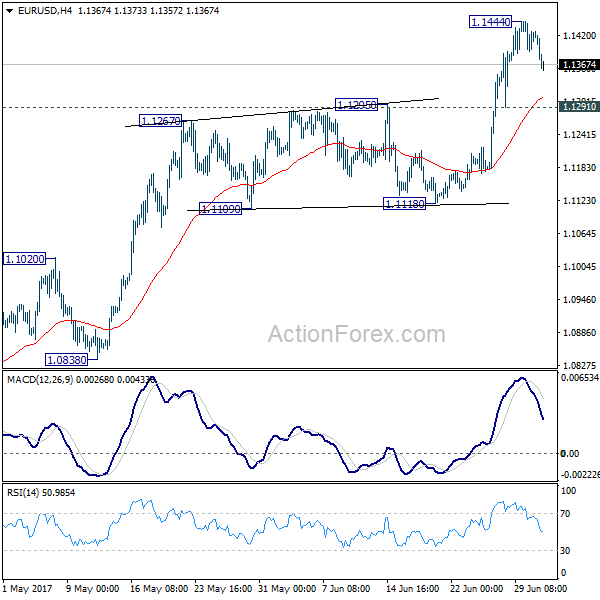

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1394; (P) 1.1419 (R1) 1.1447; More.....

EUR/USD's retreat from 1.1444 is still in progress and intraday bias remains neutral. Deeper fall cannot be ruled out. But downside should be contained by 1.1291 support to bring another rise. Break of 1.1444 will extend the rally from 1.0339 low to 1.1615 resistance next.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1776). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

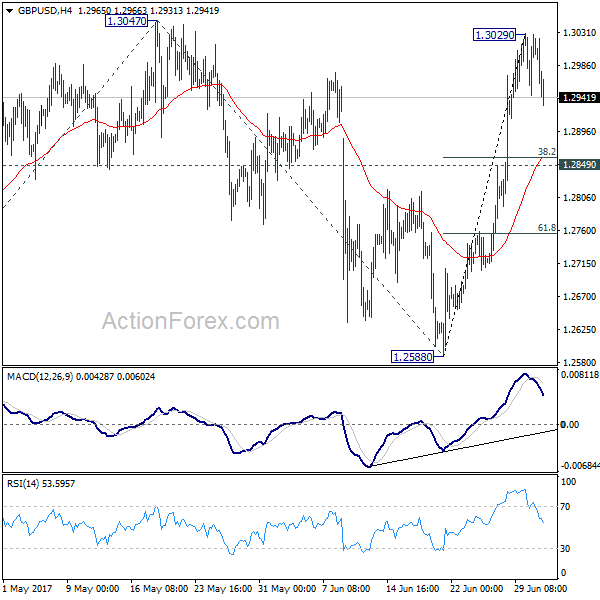

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2970; (P) 1.3000; (R1) 1.3056; More...

GBP/USD's consolidation from 1.3029 is still in progress and intraday bias remains neutral. Deeper retreat could be seen but downside should be contained above 1.2849 support to bring rise resumption. Break of 1.3029 should then send GBP/USD through 1.3047 to 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 next.

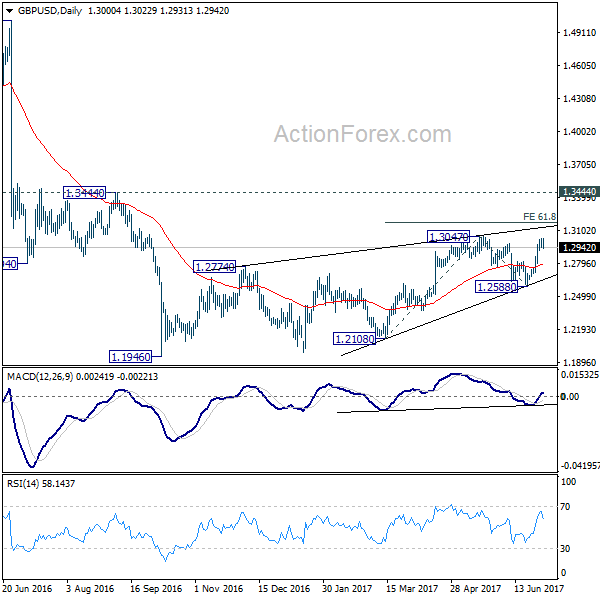

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is now in favor, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

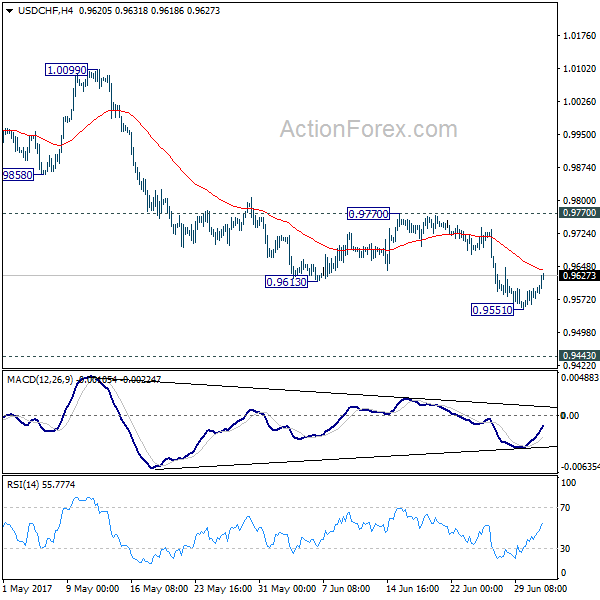

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9558; (P) 0.9578; (R1) 0.9604; More......

USD/CHF's recovery continues in early US session and outlook is unchanged. Intraday bias remains neutral for consolidation above 0.9551. Upside of recovery should be limited below 0.9770 resistance and bring resumption. Below 0.9551 will extend the decline from 1.0342 to 0.94443 key support level. At this point, we'd expect strong support from there to bring rebound.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

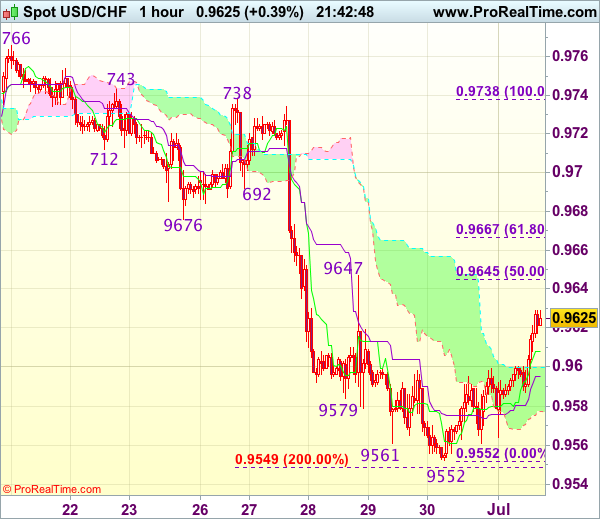

Trade Idea Update: USD/CHF – Sell at 0.9645

USD/CHF - 0.9623

Original strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

Dollar’s recovery after falling to 0.9552 last week suggests minor consolidation would be seen and corrective bounce to 0.9645-47 (50% Fibonacci retracement of 0.9738-0.9552 and previous resistance) is likely, however, reckon upside would be limited and bring another decline later, below 0.9585-90 would bring test of said support, break there would signal recent decline from 0.9771 top has resumed for further weakness to 0.9545-49 (2 times extension of 0.9771-0.9676 measuring from 0.9738) but reckon downside would be limited to 0.9525-30 (50% projection of 1.10100-0.9613 measuring from 0.9771) and 0.9500 should hold, price should stay above 0.9470 (61.8% projection), bring rebound later.

In view of this, would not chase this fall here and we are looking to sell dollar on further recovery as resistance at 0.9647 should limit upside. Only above previous support at 0.9676 (now resistance) would defer and suggest a temporary low is formed, risk test of another previous support at 0.9692.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.85; (P) 112.23; (R1) 112.73; More...

USD/JPY's rise from 108.81 resumed by taking out 112.91 and reaches as high as 113.27 so far. The break of medium term channel resistance suggests that whole corrective pull back from 118.65 has completed at 108.12 already. Intraday bias is back on the upside for 114.36 resistance. Decisive break there should confirm this bullish view and target 118.65 again. On the downside, break of 111.72 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

Dollar Regaining Ground in Subdued Trading, With a Little Help from ISM Manufacturing

Trading remains rather subdued in the forex markets today. Dollar is trying to regain some ground after last week's steep selloff. The stronger than expected ISM manufacturing is giving the greenback extra fuel. But the recovery looks nothing more than a recovery so far, except versus Yen. Sterling is also under some pressure after PMI disappointment. But loss is limited. Yen, on the other hand, is trading weakly, in particular to greenback, despite an upbeat Tankan report. The biggest news from Japan was the humiliating defeat of Prime Minister Shinzo Abe's fulling LDP in Tokyo's local election. Meanwhile, Canadian Dollar is staying firmly in tight range as WTI crude oil is extending it's rebound to as high as 46.65.

Sterling mildly lower as PMI manufacturing dropped

Sterling trades mildly lower today after PMI disappointment. UK PMI manufacturing dropped to 54.3 in June, down from 56.3 and missed expectation of 56.3. Markit noted that "while the survey data add to signs that the economy is likely to have shown stronger growth in the second quarter, further doubts are raised as to whether this performance can be sustained into the second half of the year." There are talks after the releases that the economy data could paint a picture that counter the view of the BoE hawks. But judging from reactions in the markets, traders don't buy into this view.

Economist said Eurozone PMIs exaggerated

Eurozone PMI manufacturing was finalized at 57.4 in June, revised up from 57.3. The global economist and managing director at UBS Wealth Management Paul Donovan, interviewed by CNBC, criticized that the numbers point to 3.5 or 4% growth in Europe and that is wildly exaggerated. He pointed out that the PMI is a "sentiment indicator" and "not a real-world indicator." Also he said that the survey quality has been in decline in recent years. Also from Eurozone, Italy PMI manufacturing rose to 55.2 in June, up from 55.1. Eurozone unemployment rate was unchanged at 9.3% in May.

Also from from Europe, Swiss retail sales dropped -0.3% yoy in May. SVME PMI rose to 60.1 in June.

Japan large manufacturers sentiment hits 3 year high

Japan Tankan large manufacturers index jumped to 17 in Q2, up fro 12, and beat expectation of 15. That's the highest reading in three years. Large manufacturers outlook improved to 15, up from 11, above expectation of 14. Non-manufacturing index rose to 23, up from 20, and met consensus. Non-manufacturing outlook rose to 18, up from 16, but missed expectation of 21. The survey was generally consistent with recent upgrade of economic assessment by BoJ. But still, the positive developments in the economy is not being translated into price pressure yet. And BoJ is far from stimulus exit.

Rebound in China manufacturing may be temporary

The Caixin China PMI manufacturing rose to 50.4 in June, up from 49.6 and beat expectation of 49.8. That's back in expansion territory and was the highest level in three months. However, a CEBM Group economist noted in the accompany statement for the release that "based on the inventory trends and confidence around future output, the June reading was more like a temporary rebound, with an economic downtrend likely to be confirmed later."

Elsewhere, Australia TD Securities inflation rose 0.1% mom in June. Building approvals dropped -5.6% mom in May.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.85; (P) 112.23; (R1) 112.73; More...

USD/JPY's rise from 108.81 resumed by taking out 112.91 and reaches as high as 113.27 so far. The break of medium term channel resistance suggests that whole corrective pull back from 118.65 has completed at 108.12 already. Intraday bias is back on the upside for 114.36 resistance. Decisive break there should confirm this bullish view and target 118.65 again. On the downside, break of 111.72 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Tankan Large Manufacturers Index Q2 | 17 | 15 | 12 | |

| 23:50 | JPY | Tankan Large Manufacturers Outlook Q2 | 15 | 14 | 11 | |

| 23:50 | JPY | Tankan Non-Manufacturing Index Q2 | 23 | 23 | 20 | |

| 23:50 | JPY | Tankan Non-Manufacturing Outlook Q2 | 18 | 21 | 16 | |

| 23:50 | JPY | Tankan Small Mfg Index Q2 | 7 | 7 | 5 | |

| 23:50 | JPY | Tankan Small Mfg Outlook Q2 | 6 | 4 | 0 | |

| 23:50 | JPY | Tankan Small Non-Mfg Index Q2 | 7 | 6 | 4 | |

| 23:50 | JPY | Tankan Small Non-Mfg Outlook Q2 | 2 | 3 | -1 | |

| 00:30 | JPY | Manufacturing PMI Jun F | 52.4 | 52 | 52 | |

| 01:00 | AUD | TD Securities Inflation M/M Jun | 0.10% | 0.00% | ||

| 01:30 | AUD | Building Approvals M/M May | -5.60% | -1.30% | 4.40% | |

| 01:45 | CNY | Caixin PMI Manufacturing Jun | 50.4 | 49.8 | 49.6 | |

| 05:00 | JPY | Consumer Confidence Jun | 43.3 | 43.9 | 43.6 | |

| 07:15 | CHF | Retail Sales (Real) Y/Y May | -0.30% | -0.80% | -1.20% | |

| 07:30 | CHF | SVME PMI Jun | 60.1 | 56.3 | 55.6 | |

| 07:45 | EUR | Italy Manufacturing PMI Jun | 55.2 | 55.3 | 55.1 | |

| 07:50 | EUR | France Manufacturing PMI Jun F | 54.8 | 55 | 55 | |

| 07:55 | EUR | Germany Manufacturing PMI Jun F | 59.6 | 59.3 | 59.3 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun F | 57.4 | 57.3 | 57.3 | |

| 08:30 | GBP | PMI Manufacturing Jun | 54.3 | 56.3 | 56.7 | 56.3 |

| 09:00 | EUR | Eurozone Unemployment Rate May | 9.30% | 9.30% | 9.30% | |

| 14:00 | USD | ISM Manufacturing Jun | 57.8 | 55 | 54.9 | |

| 14:00 | USD | ISM Prices Paid Jun | 55 | 58.5 | 60.5 | |

| 14:00 | USD | Construction Spending M/M May | 0.00% | 0.20% | -1.40% | -0.70% |

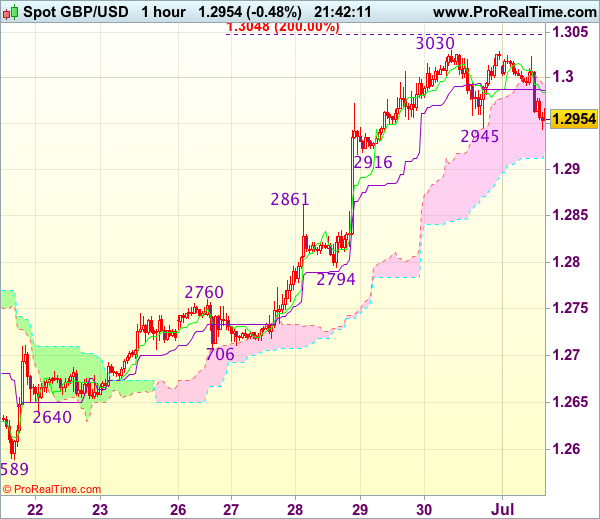

Trade Idea Update: GBP/USD – Buy at 1.2900

GBP/USD - 1.2947

Original strategy :

Buy at 1.2920, Target: 1.3020, Stop: 1.2885

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2900, Target: 1.3020, Stop: 1.2865

Position : -

Target : -

Stop : -

As cable has retreated after faltering below last week’s high of 1.3030, suggesting consolidation below this level would be seen, hence weakness to 1.2916 support cannot be ruled out, however, reckon downside would be limited to 1.2900 and bring another upmove later, above said resistance at 1.3030 would signal recent upmove is still in progress and may extend further gain towards recent high 1.3048 but loss of near term upward momentum should prevent sharp move beyond 1.3075-80 today and reckon 1.3100 would hold on first testing.

In view of this, would not chase this rise here and we are looking to buy cable again on pullback as 1.2900 should limit downside and bring another rally. Below 1.2870-75 would defer and risk test of previous resistance at 1.2861, break there would suggest a temporary top is formed instead, risk weakness to 1.2830-35 but support at 1.2794 should remain intact.

CAC Gains Ground as French Manufacturing PMI Improves

The CAC index has moved higher in the Monday session. The index is currently trading at 5172.80 and is up 1.02% on the day. On the release front, French Final Manufacturing PMI climbed to 54.8, which was within expectations. The reading improved from the May reading of 53.8. As well, Eurozone Manufacturing PMI climbed to 57.4, beating the forecast of 57.3.

President Emmanuel Macron's election win has galvanized the French public, and there is renewed optimism for real change in the country. The French consumer is feeling more confident about the economy and is also spending more. French consumer spending climbed 1.0% in June, easily beating the estimate of 0.5%. This marked the indicator's strongest gain since January 2015. The solid manufacturing data points to stronger optimism in the business sector. The economy appears to be improving – a recent INSEE report revised upwards its estimate for France's GDP for the first quarter to 0.5%, up from 0.4% earlier in June. Still, inflation levels remain stubbornly low, as underscored by French Preliminary CPI, which dropped to a flat 0.0%.

ECB President Mario Draghi surely got more than he bargained for, after speaking at the ECB forum in Portugal. The markets responded to his comments, as EUR/USD jumped 2.0%. Draghi restated the obvious when he gave an upbeat assessment of the eurozone economy,but his positive remarks about inflation shook the markets, as investors snapped up euros last week. Draghi said that "deflationary forces have been replaced by reflationary ones" and added that the ECB's stimulus program was needed for now, but would be gradually withdrawn once inflation moved higher. One could make the argument that Draghi was not saying anything new, but the markets seized on Draghi's remarks as a declaration that the ECB was planning to tighten policy. After the euro jumped, the ECB tried to backtrack, with ECB sources saying that the markets had "misinterpreted" Draghi's remarks. However, the markets shrugged this off, and if there are any indications that the ECB plans to tighten policy, the stock markets could respond with gains.

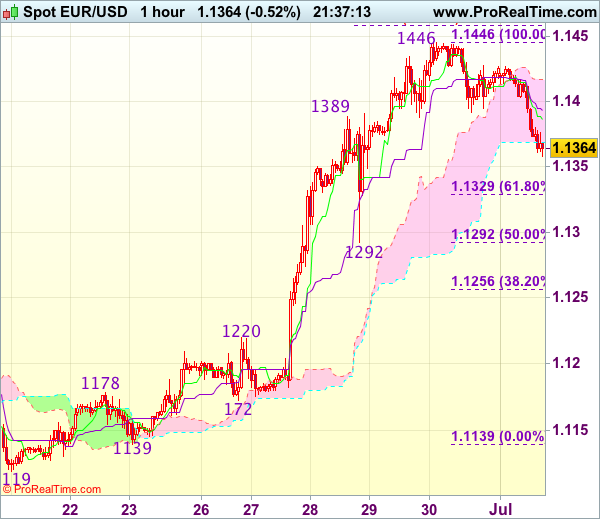

Trade Idea Update: EUR/USD – Buy at 1.1330

EUR/USD - 1.1370

Original strategy :

Buy at 1.1330, Target: 1.1440, Stop: 1.1295

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1330, Target: 1.1440, Stop: 1.1295

Position : -

Target : -

Stop : -

As the single currency met resistance at 1.1446 late last week and has eased, suggesting consolidation below this level would be seen and pullback to 1.1350 cannot be ruled out, however, reckon 1.1325-30 (38.2% Fibonacci retracement of 1.1139-1.1446) would limit downside and bring another rise later, above said resistance at 1.1446 would extend recent rise to 1.1455-60 (61.8% projection of 1.1119-1.1389 measuring from 1.1292), then 1.1480 but overbought condition should prevent sharp move beyond 1.1500, risk from there has increased for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy euro on pullback as 1.1325-30 should limit upside. Below 1.1292 (previous support as well as 50% Fibonacci retracement of 1.1139-1.1446) would abort and signal a temporary top is formed, bring correction to 1.1255-60 later.

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 113.02

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the greenback has surged again after finding renewed buying interest just below 112.00, dampening our near term bearishness and near term upside risk remains for recent upmove to extend gain to 113.20, then towards 113.40-50, however, near term overbought condition should prevent sharp move beyond later level and reckon 113.75-80 would hold from here, bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below the Kijun-Sen (now at 112.51) would bring test of the lower Kumo (now at 112.17) but break of 111.90-95 is needed to signal an intra-day top is formed, bring test of 111.73 support first.