Sample Category Title

Metals Tumble as Real Yields Shoot

USD outperforms all currencies, while gold and silver were the biggest losers as real bond yields extended higher. US manufacturing ISM to 57.8, reaching its highest since August 2014 from 54.9 in May, with the new orders index hitting 3-month highs. Further accelerating the metals selloff is the decline in the prices paid index of the ISM, which fell to 8-month lows of 55. The 2nd listed trade in the Premium Insights is Ashraf's highest confidence trade in this enviromnment of rising REAL bond yields.

Seasonally, July is the start of a three-month period where bonds strongly outperform while in terms of FX, yen crosses tend to struggle. Over the past 10 years, July has been the worst month for USD/JPY with an average decline of 1.26%.

Finally, oil tends to struggle late in the year but over the past 20 years that weakness has progressively been creeping earlier in the year. July is a soft month over 10 and 30-year periods but it's been severe more recently. In the past three years the average decline has been a whopping 13.8%.

On the fundamental side, the global theme of a hawkish shift from central banks remains new and fresh. The June comments from the BOE, BOC, RBA and ECB were surprises and led to a welcome dose of volatility.

The reason that central banks create trends in the market is that they rarely change course once they commit, especially when global central banks all move in the same direction. What remains incredible is that the near-universal belief in central banks that inflation is going to pick up contrasts to a skeptical market. The hopes is that clear answers are coming in months ahead but the story is rarely that simple. Expect markets to ebb and flow aggressively on conflicting signals and data.Those types of aggressive moves are clear in the last few weeks of positioning data as traders piled into Canadian dollar shorts only to scramble out.

CFTC Commitments of Traders

Speculative net futures trader positions as of the close on Tuesday. Net short denoted by - long by +.

- EUR +59K vs +45K prior

- GBP -39K vs -38K prio

- JPY -61K vs -50K prior

- CHF -5K vs -3K prior

- CAD -49K vs -82K prior

- AUD +20K vs +15K prior

- NZD +25K vs +21K prior

Euro longs were +79K two weeks ago, then dropped to +45K and now have rebounded to +59K in a sign that the market is changing its mind on the fly.

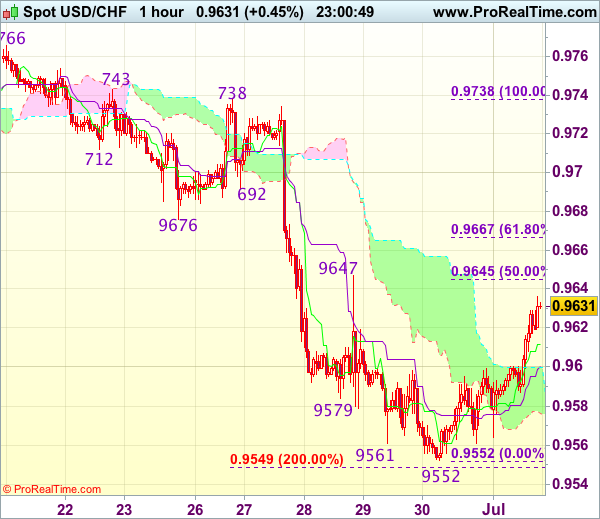

Trade Idea Wrap-up: USD/CHF – Buy at 0.9600

USD/CHF - 0.9633

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9612

Kijun-Sen level : 0.9600

Ichimoku cloud top : 0.9600

Ichimoku cloud bottom : 0.9576

Original strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9600, Target: 0.9700, Stop: 0.9565

Position : -

Target : -

Stop : -

As the greenback has continued moving higher after staging a strong rebound from 0.9552, suggesting a temporary low is possibly formed there and consolidation with upside bias is seen for further gain to 0.9645-47 (50% Fibonacci retracement of 0.9738-0.9552 and previous resistance), then 0.9676 (previous support turned resistance), however, break of latter level is needed to add credence to this view, bring further gain to 0.9700 but price should falter below resistance at 0.9738.

In view of this, we are looking to turn long on pullback as the Kijun-Sen (now at 0.9600) should limit downside and bring another rise later. Below the lower Kumo (now at 0.9576) would abort and signal intra-day top is formed, risk retest of 0.9552 first.

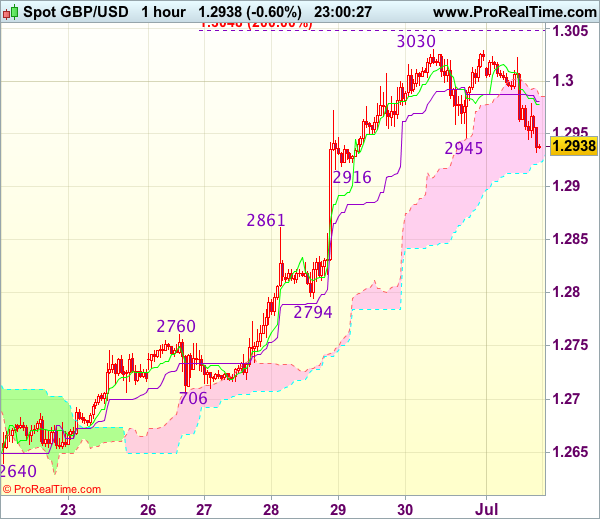

Trade Idea Wrap-up: GBP/USD – Buy at 1.2865

GBP/USD - 1.2941

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2978

Kijun-Sen level : 1.2981

Ichimoku cloud top : 1.2985

Ichimoku cloud bottom : 1.2923

Original strategy :

Buy at 1.2900, Target: 1.3020, Stop: 1.2865

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2865, Target: 1.3000, Stop: 1.2830

Position : -

Target : -

Stop : -

As cable has retreated after faltering below last week’s high of 1.3030, suggesting consolidation below this level would be seen, hence weakness to 1.2916 support cannot be ruled out, however, reckon downside would be limited to 1.2865-70 and bring another upmove later, above said resistance at 1.3030 would signal recent upmove is still in progress and may extend further gain towards recent high 1.3048 but loss of near term upward momentum should prevent sharp move beyond 1.3075-80 today and reckon 1.3100 would hold on first testing.

In view of this, would not chase this rise here and we are looking to buy cable again on pullback as 1.2900 should limit downside and bring another rally. Below previous resistance at 1.2861 would suggest a temporary top is formed instead, risk weakness to 1.2830-35 but support at 1.2794 should remain intact.

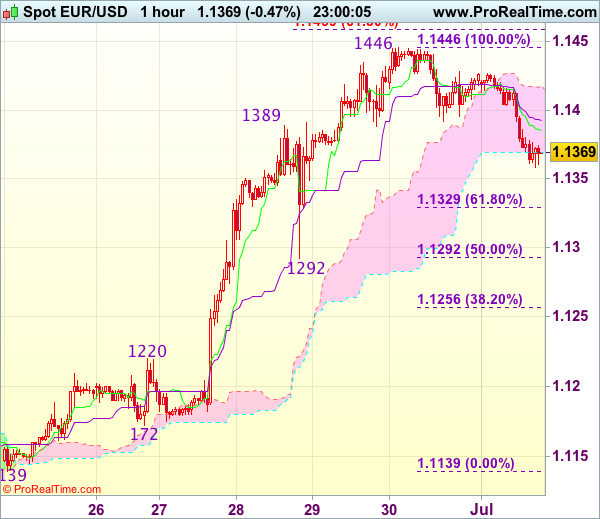

Trade Idea Wrap-up: EUR/USD – Buy at 1.1325

EUR/USD - 1.1368

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1385

Kijun-Sen level : 1.1393

Ichimoku cloud top : 1.1418

Ichimoku cloud bottom : 1.1369

Original strategy :

Buy at 1.1330, Target: 1.1440, Stop: 1.1295

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1325, Target: 1.1440, Stop: 1.1290

Position : -

Target : -

Stop : -

As the single currency met resistance at 1.1446 late last week and has retreated, suggesting consolidation below this level would be seen and pullback to 1.1350 cannot be ruled out, however, reckon 1.1325-30 (38.2% Fibonacci retracement of 1.1139-1.1446) would limit downside and bring another rise later, above said resistance at 1.1446 would extend recent rise to 1.1455-60 (61.8% projection of 1.1119-1.1389 measuring from 1.1292), then 1.1480 but overbought condition should prevent sharp move beyond 1.1500, risk from there has increased for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy euro on pullback as 1.1325-30 should limit upside. Below 1.1292 (previous support as well as 50% Fibonacci retracement of 1.1139-1.1446) would abort and signal a temporary top is formed, bring correction to 1.1255-60 later.

Trade Idea Wrap-up: USD/JPY – Stand aside

USD/JPY - 113.30

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.92

Kijun-Sen level : 112.63

Ichimoku cloud top : 112.33

Ichimoku cloud bottom : 112.21

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the greenback has surged again after finding renewed buying interest just below 112.00, dampening our near term bearishness and near term upside risk remains for recent upmove to extend gain to 113.45-50, however, near term overbought condition should prevent sharp move beyond 113.75-80 and reckon 114.00-10 would hold from here, bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below the Kijun-Sen (now at 112.64) would bring test of the lower Kumo (now at 112.21) but break of 111.90-95 is needed to signal an intra-day top is formed, bring test of 111.73 support first.

US Dollar Recovers ahead of July 4th Holiday; Global Manufacturing PMIs Paint Upbeat Picture

The dollar managed to regain a part of its recent losses today, as Purchasing Managers' Indices from around the world painted an upbeat picture of the global economy.

As the dollar strengthened, particularly noteworthy was its break above 113 versus the yen; a 1 ½ – month high for the greenback. The yen was also near its 1 ½ -year low against the euro as it traded around 128.40. In Japan, signs of optimism from large manufacturers and services' companies in the quarterly Tankan survey were countered by news that the Prime Minister's party lost the elections for the Tokyo regional assembly.

Euro/dollar backed down below the 1.14 mark to trade at 1.1360, despite a slightly better-than-expected June Manufacturing Final PMI reading for the Eurozone. The index came in at 57.4 compared to 57.3 which was the preliminary estimate. The reading marked a 6-year high for Eurozone manufacturing activity and this bodes well for the region's economic expansion going forward. However, the region's unemployment rate did not fall to 9.2% in May as expected but remained constant at 9.3%.

There were disappointing news out of UK factories as the Markit/CIPS manufacturing index dropped to 54.3 in June from May's 56.7. Analysts were expecting a more modest drop to 56.3. The pound fell once again below the 1.30 level against the US dollar to as low as 1.2941, but its losses were relatively in line with those of the euro against the greenback. The pound has been boosted lately by speculation that the Bank of England will raise interest rates in the coming months, as the Bank's governor, Mark Carney, has hinted he might join the hawks if conditions warrant it. A speech by Carney today did not address the topic of monetary policy.

In US data, the ISM Manufacturing PMI for July climbed to 57.8 from 54.9 the previous month. Analysts were expecting a rise to 55.2. The upside surprise occurred despite a sharp drop in the prices paid component to 55 from 60.5 the previous month. Both the 10-year Treasury yield and dollar/yen rose sharply following the ISM announcement.

In the commodities space, crude oil continued to rally and the US-traded WTI oil futures contract reached $46.50 a barrel. On the other hand, gold remained under pressure and made fresh 1 ½ month low at $1224 an ounce.

Looking ahead, an early close of US financial markets ahead of the July 4th holiday should also lead to diminished trading for forex markets. June US vehicle sales will come out later today. During Tuesday's Asian session, the policy statement from the Reserve Bank of Australia will likely dominate the news, while traders will also be looking at Australian retail sales for May.

Yen Dips as US Manufacturing PMI Jumps

USD/JPY has posted gains in the Monday session, gaining 0.74%. In the North American session, the pair is trading slightly above the 113 level. On the release front, Japanese Tankan Indices were both within expectations. The Tankan Manufacturing Index improved to 17, easily beating the estimate of 12. The Tankan Services Index improved to 23, just shy of the forecast of 24. Japanese Consumer Confidence softened to 43.3, missing the estimate of 43.9. In the US, ISM Manufacturing PMI climbed to 57.8, beating the estimate of 55.0.

The Japanese economy has shown some improvement, but consumer spending and inflation remain sore points. Japanese retail sales slowed to just 2.0% in May, compared to 3.2% a month earlier. The weak figure points to a Japanese consumer who is hesitant to open the purse strings. Wages have been stagnant, which has hampered consumer spending, a key driver of economic growth. Inflation is stuck below 1 percent, well below the BoJ's target of 2 percent. Tokyo Core CPI, the primary gauge of consumer inflation, edged down to 0.0%, below the estimate of 0.2%. The index has posted just one gain in the past 18 months, underscoring that the BoJ's ultra-loose monetary policy has not been able to raise inflation levels anywhere near the bank's target of 2 percent.

There was no getting around the fact that the US economy slowed down in the first quarter, but there was some good news, as the revised GDP reading was raised to 1.4%, better than the initial estimate of 1.2% in May. The improvement was attributed to stronger consumer spending and an increase in exports. Earlier in the year, the markets were braced for a very poor quarter, with the first estimate in April projecting a gain of only 0.7%. Inflation remains stubbornly low, and consumer spending is also soft, despite high consumer confidence levels. In May, Personal Spending softened to 0.1%, down from 0.4% a month earlier. If inflation levels don't show some improvement, the Federal Reserve may have second thoughts about a December rate hike.

Trade Idea: EUR/GBP – Stand aside

EUR/GBP - 0.8778

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the single currency has retreated after rising briefly to 0.8882 last week, retaining our view that a temporary top is possibly formed there and few days of consolidation would be seen with mild downside bias, below 0.9755-60 would add credence to this view, bring retracement of recent upmove to 0.8730-35, however, still reckon downside would be limited to 0.8719 support.

In view of this, would be prudent to stand aside for now and look to turn short on recovery as 0.8840-50 should limit upside. Above 0.8882 would revive bullishness and extend recent upmove from 0.8304 low to 0.8900-10, having said that, as broad outlook remains consolidative, reckon current c leg of larger degree wave b should be limited to 0.8950 and price should falter well below 0.9000 psychological level.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Sell at 1.3115

USD/CAD - 1.2986

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term down

Original strategy :

Sell at 1.3115, Target: 1.2915, Stop: 1.3175

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.3115, Target: 1.2915, Stop: 1.3175

Position: -

Target: -

Stop:-

As the greenback has recovered after falling to 1.2946 on Friday, suggesting minor consolidation would be seen and corrective bounce to 1.3045-50 and possibly 1.3080 is likely, however, reckon 1.3115-20 would limit upside and bring another decline later, below said support would extend the fall from 1.3794 top (wave c of larger degree wave b top) to 1.2920, however, near term oversold condition should limit downside to 1.2900 and reckon 1.2870 would hold from here, risk from there has increased for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell the pair again on recovery as 1.3115-20 should limit upside. Above 1.3160-70 would defer and suggest low is formed, bring a stronger rebound to 1.3215-20 and possibly towards 1.3260-65 but only break there would abort and signal a temporary low is formed instead, then test of resistance at 1.3308 would follow.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Sterling Hardly Suffers from Disappointing PMI

- European equities are showing gains of around 1%. American indices are joining the positive momentum. Major US indices start the quarter with gains of about 0.5% Trading volumes are light before Tuesday's US 4th of July holiday. The dollar strengthened as positions are set ahead of key US data later this week.

- Average unemployment in the Eurozone held at 9.3% in May, its lowest level since 2009, as the number of people who registered as jobless fell by 5,000 in the month. It was the weakest monthly performance of the year.

- IHS Markit's Eurozone manufacturing PMI posted another bumper month of activity with the overall index hitting 57.4 in June, its best level since April 2011 and up from the flash reading of 57.3 and the 57 in May. This makes the quarterly performance the best in over six years.

- The UK June manufacturing PMI unexpectedly declined to 54.3 from 56.3 (revised from 56.7) while a stabilisation was expected. Output, order book and employment growth all slowed and positive sentiment slipped to a seven-month low amid reports of uncertainty regarding the political outlook.

- The US manufacturing ISM improved from 54.9 to 57.8. The consensus expected only a rise to 55.3. The rebound was supported by strong orders (63.5) and a rise of the employment component. Prices rise eased more than expected. (55.0 from 60.5).

- German Chancellor Angela Merkel's party and her Bavarian CSU allies say in election platform that they oppose pooling euro-area debt. They added that they are ready to develop the Eurozone further together with the French government, for instance with the creation of its own monetary fund.

- US Carmakers outsold June estimates in US. Y/Y changes are still negative as base year 2016 was a record year.

Rates

German bonds start the week with cautious gains

After a savage sell-off last week, German bonds cautiously reversed course in technical trading, but only after a shy test of the key Bund support at 161.68/58 (Bund opened at 161.55). The down-leg was exhausted or at least needed a pause. Ahead of the closure of US markets tomorrow, that isn't a big surprise. The German 10-yr yield virtually touched the key 0.5% yield resistance. The upturn in German bonds wasn't because of bad news as the final PMI was even marginally revised higher and the unemployment rate was in line with expectations. The corrective movement was visible in other markets too, with equities and the dollar gaining some ground. With all boats rising, we cannot but conclude that the quarter started well. However, it is too early to jump on the current technically inspired rise of "all" assets. Going towards the publication of the key ISM report (after the closure of our report) core bonds are declining marginally.

At the time of writing, the German yield curve flattened slightly with yields down between 1.9 bp (2-yr) and 0.2 bp (30-yr). The US yield curve was little changed (less than 1 bp) with yields marginally up in the 2-to-5-yr sector and slightly down in the 10-30-yr segment. On intra-EMU bond markets, 10-yr yield spread changes are little changed with the exception of Italy/Spain and Ireland whose spreads narrow 1.5 to 2.3 bps.

Currencies

Dollar rebound ahead of ISM

The dollar made a cautious comeback at the start of the new trading week as investors prepared for key US eco data today and later this week. The EMU eco data were strong, but the euro didn't profit anymore. EUR/USD declined to trade in the 1.1360 area ahead of the key US ISM manufacturing release. USD/JPY changed hands in the 113 area.

Overnight, Asian equities traded mixed. The Japan Tankan business sentiment was stronger than expected. The Caixin China manufacturing PMI also improved slightly. Decent regional data don't help the yen though. USD/JPY opened slightly in the red on a negative result for PM Abe's party in regional elections, but reversed the initial loss. A further rise in the oil price and a rise in US yields supported the dollar. USD/JPY returned to the 112.50 area. EUR/USD dropped slightly to the 1.1405/20 area.

The dollar USD momentum improved during the European morning session. EUR/USD dropped below 1.14 handle. Dollar strength prevailed even as the EMU eco data remained strong (manufacturing PMI, EMU unemployment). Investors apparently reduced USD short-going into a series of key US eco data to be published this week, starting with the manufacturing ISM today. Changes on the core bond market were limited. If anything, the US/German spread widened marginally if favour of the dollar. USD/JPY also extended the intraday uptrend and rebounded to the high 112 area. The intraday dollar rebound slowed this afternoon as investors awaited the US manufacturing ISM. EUR/USD traded in the 1.1370 area. USD/JPY held close to the 113-pivot.

Sterling hardly suffers from disappointing PMI

Sterling trading was mostly driven by the price moves in the dollar and the euro. The overall rebound of the dollar pushed cable back below the 1.30 barrier. There was also a small fall-out from the EUR/USD decline on EUR/GBP. The pair dropped to the 0.8760 area. Mid-morning, the UK manufacturing PMI unexpectedly declined to 54.3 from 56.3 (earlier reported as 56.7). A stabilisation was expected. Sterling lost modest ground after the release. EUR/GBP rebounded to the 0.8775/80 area. Cable declined further. The release further complicates the internal debate in the BoE on the need for a rate hike. However, in this respect, the services PMI to be published on Wednesday will probably be more important. EUR/GBP trades currently in the 0.8780 area; Cable is changing hands around 1.2950.