Sample Category Title

Trade Idea: AUD/USD – Buy at 0.7500

AUD/USD – 0.7550

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term down

Original strategy :

Buy at 0.7500, Target: 0.7650, Stop: 0.7440

Position: -

Target: -

Stop: -

New strategy :

Buy at 0.7500, Target: 0.7650, Stop: 0.7440

Position: -

Target: -

Stop:-

Outlook remains supportive for recent upmove to resume after consolidation and break of last week’s high at 0.7567 would extend recent upmove from 0.7329 low towards 0.7592, then test of resistance at 0.7611 but break of latter level is needed add credence to this bullish count and encourage for subsequent upmove towards resistance at 0.7680 but price should falter below chart point at 0.7750.

In view of this, we are looking to buy aussie on dips as 0.7500 should limit downside and bring another rise. Below support at 0.7457 would abort and suggest top is possibly formed, bring weakness to 0.7415-20 but price should stay well above key support at 0.7372, bring another rebound later.

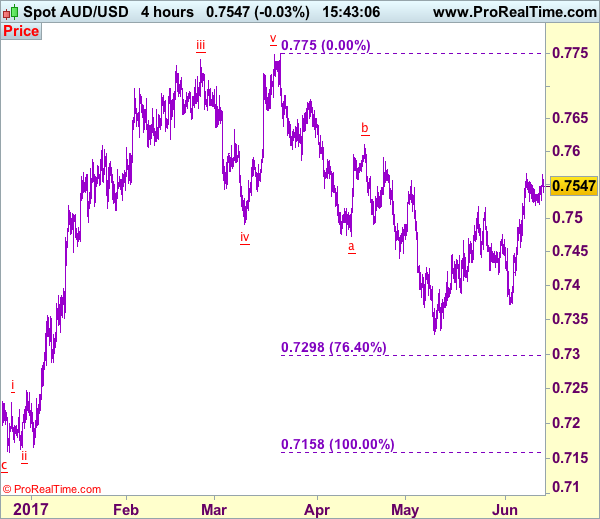

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

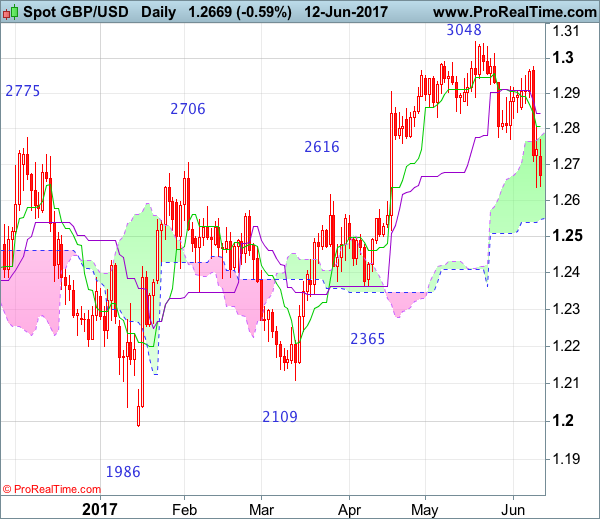

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2608; (P) 1.2689; (R1) 1.2739; More...

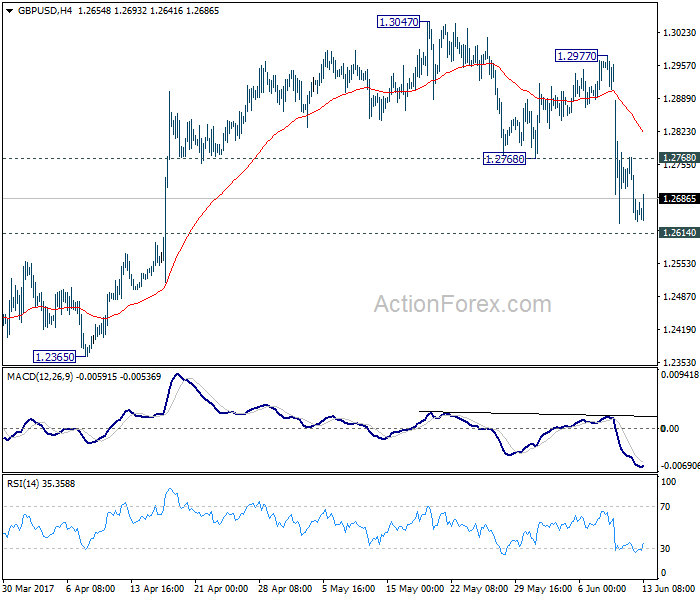

At this point, intraday bias in GBP/USD stays on the downside for deeper decline. As noted before, we favor the case that consolidation pattern from 1.1946 has completed at 1.3047 already. Decisive break of 1.2614 resistance turned support would confirm our bearish view and target a test on 1.1946 low next. On the upside, above 1.2768 will bring turn bias neutral and bring recovery. But outlook will remain bearish as long as 1.2977 resistance holds.

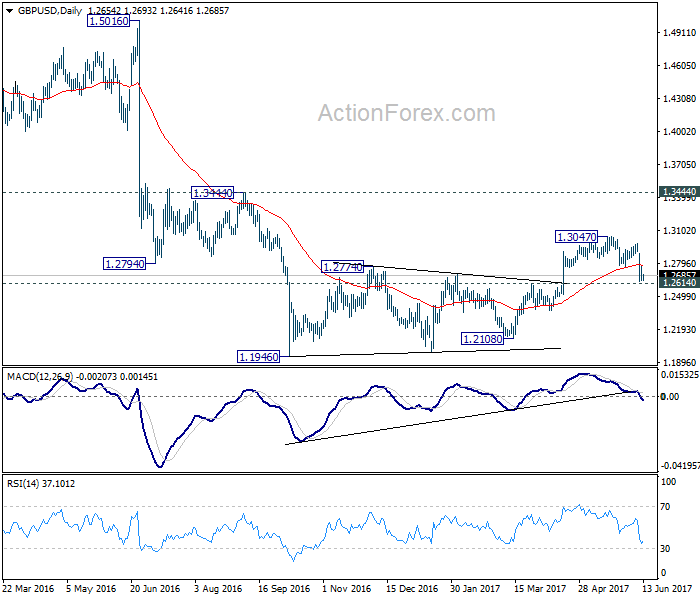

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. Price actions from 1.1946 medium term low are seen as a consolidation pattern, which could have completed after hitting 55 week EMA. Break of 1.1946 low will target 61.8% projection of 1.5016 to 1.1946 from 1.3047 at 1.1150 next. In case the consolidation from 1.1946 extends, outlook will stay remain bearish as long as 1.3444 resistance holds.

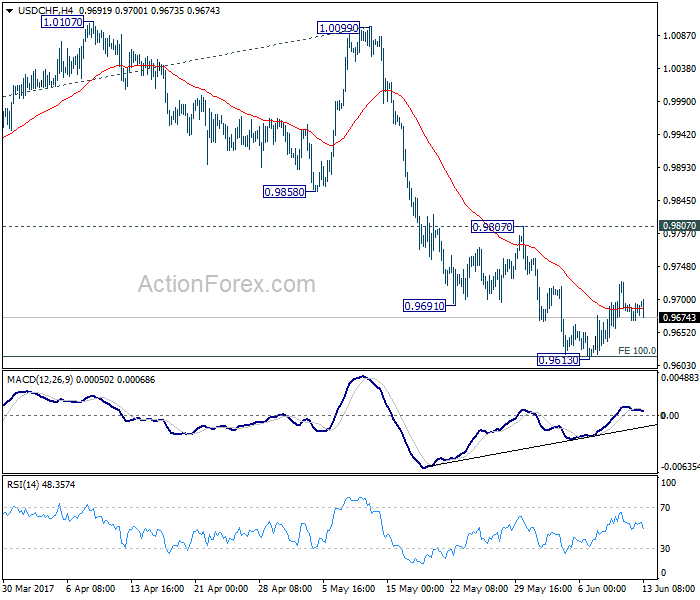

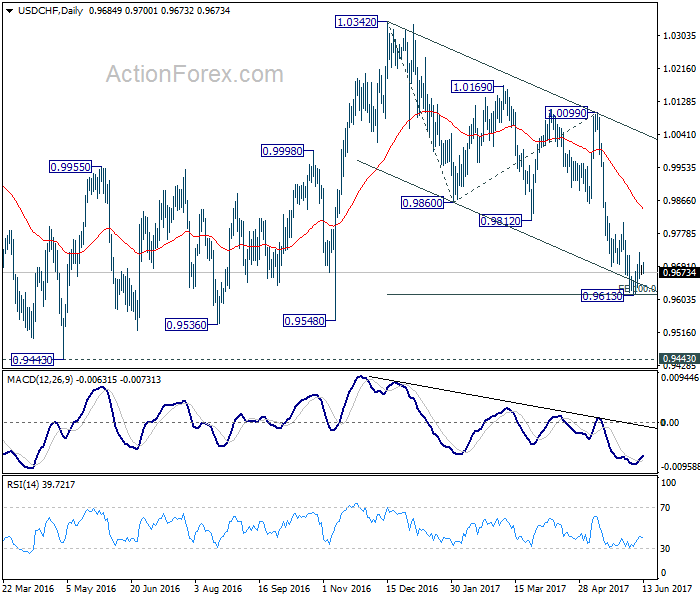

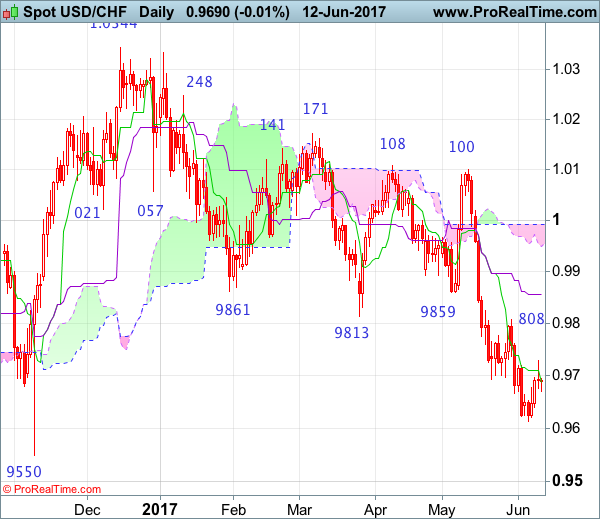

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9672; (P) 0.9683; (R1) 0.9697; More.....

Intraday bias in USD/CHF remains neutral as the consolidation pattern from 0.9613 is still extending. Since 0.9807 resistance stays intact, near term outlook is cautiously bearish for further fall. Break of 0.9613 will extend the whole decline from 1.0342 to 0.9548 support and below. We'd start to look for bottoming signal again as it approaches 0.9443 key support level. However, considering bullish convergence condition in 4 hour MACD, break of 0.9807 will indicate near term reversal and turn outlook bullish for 1.0099 resistance next.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

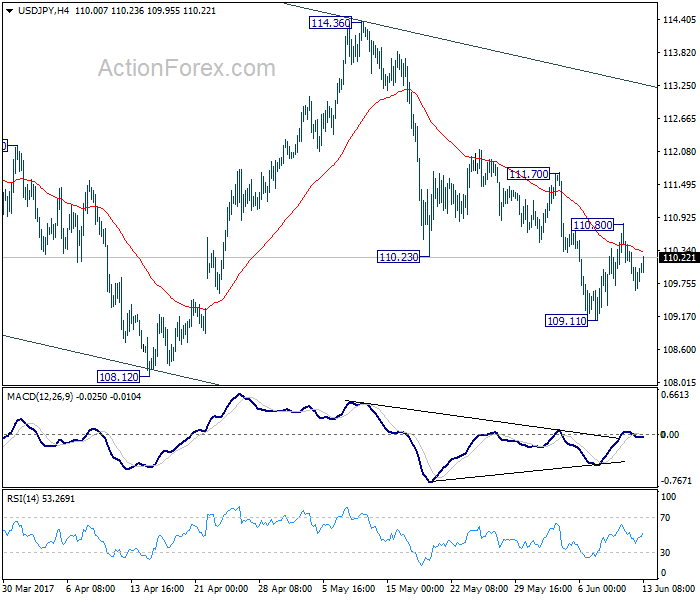

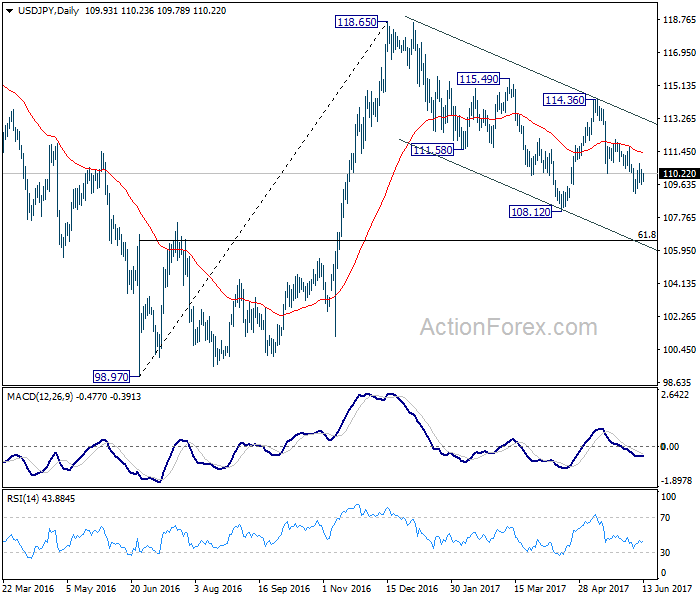

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.56; (P) 109.99; (R1) 110.37; More...

USD/JPY continues to stay in range of 109.11/110.80 and intraday bias remains neutral at this point. Overall outlook is unchanged. With 111.70 resistance intact, , near term outlook remains mildly bearish and deeper fall is expected. Below 109.11 will target 108.12 low first. Break will extend the whole corrective fall from 118.65 to 61.8% retracement of 98.97 to 118.65 at 106.48. We will look for bottoming sign there. Meanwhile, break of 110.70 will indicate near term reversal and turn bias back to the upside for 114.36 resistance instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

GBP/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 16 Jan 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 18 Apr 2017

• Trend bias: Near term up

GBP/USD – 1.2655

Although cable recovered last week, as renewed selling interest emerged around 1.2978 and has dropped sharply, a long black candlestick was formed on the daily chart, suggesting top has been formed at 1.3048 and consolidation below this level would be seen with mild downside bias for test of previous resistance at 1.2616, a daily close below this level would add credence to this view, bring retracement of early upmove to 1.2550, then 1.2500 support but near term oversold condition should limit downside to 1.2440-50 and price should stay well above key support at 1.2365, bring rebound later.

On the upside, whilst initial recovery to 1.2770-80 cannot be ruled out, reckon the Tenkan-Sen (now at 1.2807) would limit upside and bring another decline. A daily close above the Kijun-Sen (now at 1.2842) would defer and risk a stronger rebound to 1.2885-90 but price should falter well below said resistance at 1.2978 and bring another decline later. Only a sustained breach above this level would suggest the correction from 1.3048 top has ended and bring further gain towards this level, a break of this level would revive bullishness and extend recent upmove from 1.1986 low (Jan low) for retracement of early downtrend to 1.3050-60, then 1.3100. having said that, loss of near term upward momentum should prevent sharp move beyond 1.3140-50 (38.2% Fibonacci retracement of 1.5018-1.1986) and reckon 1.3200 would hold.

Recommendation: Sell at 1.2800 for 1.2600 with stop above 1.2900.

On the weekly chart, as cable has remained under pressure after forming a black candlestick last week, suggesting further consolidation below recent high of 1.3048 would be seen and mild downside bias is for the retreat from 1.3048 to bring retracement of recent rise to previous resistance at 1.2616, a sustained breach below this level would add credence to this view, bring further weakness to 1.2550-60, however, still reckon downside would be limited and previous support at 1.2515 should remain intact, bring rebound later.

On the upside, expect recovery to be limited to the Tenkan-Sen (now at 1.2782) and renewed selling interest should emerge around 1.2800-10 and price should falter below 1.2870-80, bring another decline. Only above resistance at 1.2978 would signal the retreat from 1.3048 has ended, bring retest of this level first, once this recent high is penetrated, this would signal the erratic upmove from 1.1986 low (2017 low) has resumed, bring retracement of early decline to 1.3090-00, then towards 1.3140-50 (38.2% Fibonacci retracement of 1.5018-1.1986) but price should falter well below 1.3200-10, risk from there is seen for a retreat to take place later.

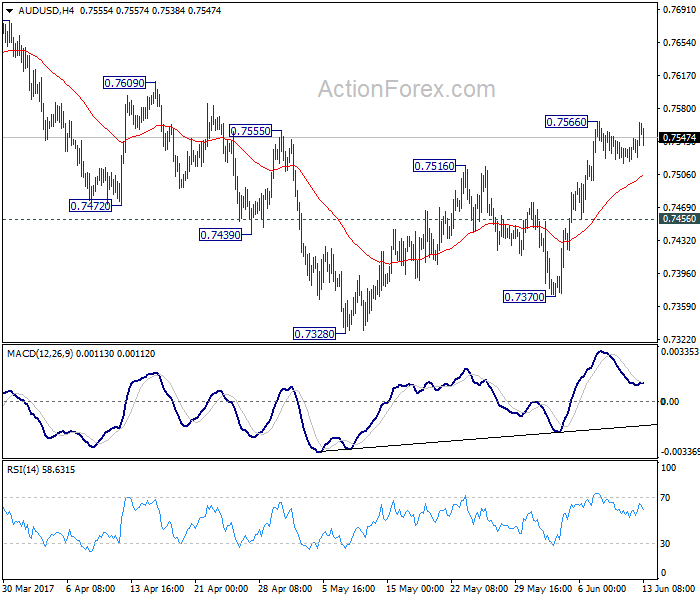

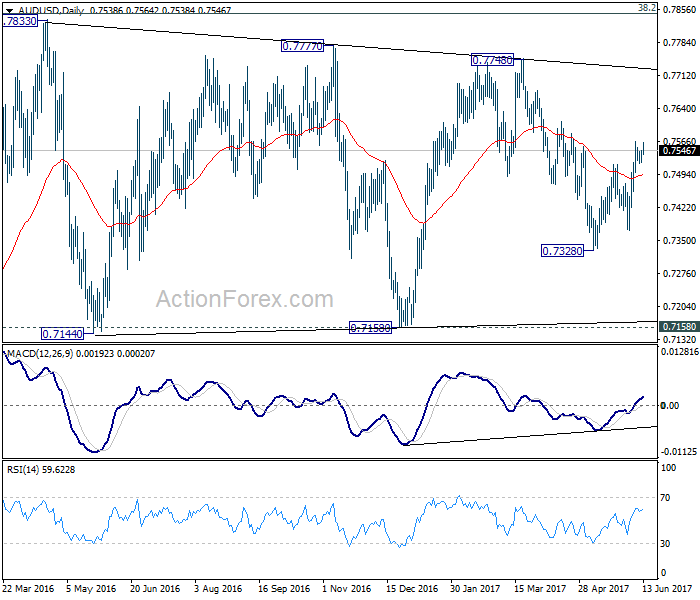

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7526; (P) 0.7536; (R1) 0.7552; More...

AUD/USD recovers today but it's staying below 0.7566 temporary top. Intraday bias remains neutral for the moment. With 0.7456 minor support intact, further rise is in favor. Above 0.7566 will target 0.7748 resistance. In that case, we'll be cautious on topping again as it approaches medium term fibonacci level at 0.7849. On the downside, below 0.7456 minor support will turn bias back to the downside for 0.7328 short term bottom.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8091) and above.

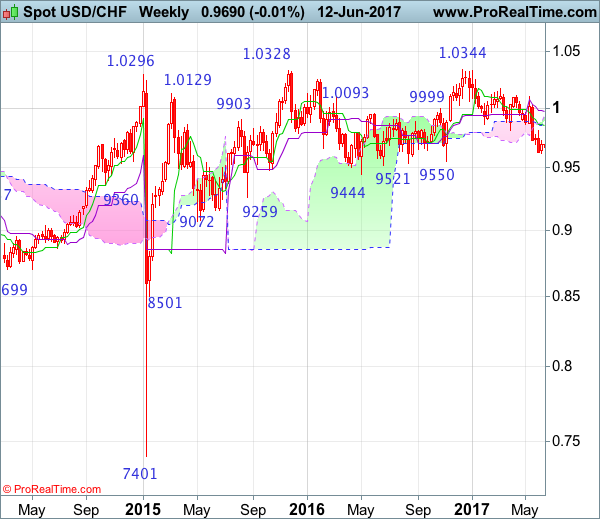

USD/CHF Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 7 Mar 2017

• Trend bias: Sideways

Daily

• Last Candlesticks pattern: Morning star

• Time of formation: 9 May 2017

• Trend bias: Near term up

USD/CHF – 0.9690

As the greenback has recovered after falling to 0.9613, suggesting consolidation above this level would be seen and another bounce to 0.9725-30 is likely, however, reckon upside would be limited to resistance at 0.9808 and bring another decline later, below said support at 0.9613 would extend recent decline from 1.0344 top (2016 high) towards support at 0.9550 but near term oversold condition should prevent sharp fall below this level and price should stay above psychological level at 0.9500, risk from there has increased for a rebound later.

On the upside, whilst initial recovery to 0.9725-30 and 0.9760-70 is likely, reckon upside would be limited to said resistance at 0.9808, bring another decline. A daily close above 0.9857-59 (current level of the Kijun-Sen and previous support now resistance) would defer and suggest a temporary low is formed, bring a stronger rebound to the lower Kumo (now at 0.9949) but price should falter below 1.0000 and bring another selloff.

Recommendation: Sell at 0.9805 for 0.9605 with stop above 0.9905

On the weekly chart, as the greenback has remained under pressure recent selloff, adding credence to our bearish view that early erratic fall from 1.0344 top is still in progress, hence bearishness remains for this move to bring retracement of early upmove to 0.9600, then towards previous support at 0.9550, however, reckon downside would be limited to 0.9500 and another previous support at 0.9444 should remain intact, risk from there has increased for a strong rebound later.

On the upside, although initial recovery to 0.9750-60 cannot be ruled out, reckon said resistance at 0.9808 would limit upside and bring another decline. A weekly close above the Tenkan-Sen (now at 0.9857) would defer and risk a stronger rebound to 0.9940-50 but 1.0007 (previous resistance) should limit upside and price should falter well below 1.0100, bring another selloff later. Above 1.0100 would signal low is formed instead and suggest the aforesaid decline from 1.0344 has ended, bring test of 1.0171 resistance next.

Market Update – Asian Session: BOJ Speculated To Maintain Assessment This Week

US Session Highlights

(US) New York Fed Consumer Expectations May survey: 1-year ahead inflation expectations at 2.6% v 2.8% prior; 3-year ahead inflation expectations at 2.5% v 2.9% prior (lowest since Jan)

(US) TREASURY'S $24B 3-YEAR NOTE AUCTION DRAWS 1.500% (lowest yield since Feb); BID-TO-COVER RATIO: 3.00 V 2.76 PRIOR AND 2.78 AVG OVER THE LAST 12 (highest BTC since Dec 2015)

(US) Pres Trump: administration will have 'major' legislation on steel and aluminum dumping - press

The sell-off from Friday rolled into today's start to the week, albeit in a less dramatic way. Techs continued to be the under-performers today as well. The Tech sell-off initiated Friday spread to Europe this morning with STOXX 600 losing nearly 1%. Worst performing sectors for the S&P were Technology and Materials losing 0.7% and 0.6% respectively, best performing sectors were Energy and Real Estate, gaining 0.7% and 0.5% respectively.

US markets on close: Dow +0.2%, S&P500 +0.2%, Nasdaq +0.3%

Best Sector in S&P500: Telecom

Worst Sector in S&P500: Technology

Biggest gainers: UA +5.8%; KIM +4.0%; FTR +3.7%

Biggest losers: NFLX -4.2%; IDXX -3.9%; ALB -3.7%

At the close: VIX 11.5 (+0.8pts); Treasuries: 2-yr 1.36% (flat), 10-yr 2.21% (+2bp), 30-yr 2.87% (+1bps)

US movers afterhours

SYNA Acquires CNXT Holdings for $300M cash from MRVL; Guides Q4 R$420-430M v $431Me - filing; +2.5% afterhours

XLRN Announces top-line results from DART Phase 2 study of Dalantercept in advanced renal cell carcinoma; -5.2% afterhours

SAIC Reports Q1 $1.08 v $1.00e, Rev $1.10B v $1.11Be; -10.1% afterhours

Politics

(GE) Germany Chancellor Merkel's Conservatives have support of 37.5% v 23.5%for the Social Democrats - INSA Poll

Key economic data

(AU) AUSTRALIA MAY NAB BUSINESS CONFIDENCE: 7 V 13 PRIOR; CONDITIONS: 12 V 13 PRIOR

(JP) JAPAN Q2 BUSINESS SURVEY INDEX (BSI) LARGE ALL INDUSTRY Q/Q: -2.0 V 1.3 PRIOR; BSI LARGE MANUFACTURING Q/Q: -2.9 V 1.1 PRIOR

Speakers and Press

Japan

(JP) Japan Fin Min Aso: USD can strengthen if Fed raises rates

(JP) BOJ's Amamiya: Amount of BOJ's JGB purchases fluctuates

(JP) BOJ expected to maintain economic assessment at this week's policy board meeting - Japan press

Korea

(KR) Bank of Korea (BOK) Gov Lee: Fed rate hikes, household debt are risks to growth; to closely cooperate with Govt on economy

Asian Equity Indices/Futures (00:00ET)

Nikkei flat, Hang Seng +0.5%, Shanghai Composite +0.4%, ASX200 +1.2%, Kospi +0.6%

Equity Futures: S&P500 +0.1%; Nasdaq +0.2%, Dax +0.1%, FTSE100 +0.4%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1190-1.1210; JPY 109.80-110.10; AUD 0.7540-0.7565; NZD 0.7190-0.7225

Aug Gold flat at 1,269/oz; July Crude Oil +0.4% at $46.24/brl; July Copper +0.2% at $2.62/lb

(CN) PBOC SETS YUAN MID POINT AT 6.7954 V 6.7948 PRIOR

(CN) PBOC to inject combined CNY50B v CNY40B prior

(JP) Japan's MoF sells ¥0.9T in 0.6% (0.7% prior) 20-year JGBs; Avg yield: 0.583% v 0.560% prior; bid-to-cover: 3.98x v 3.84x prior

(AU) Australia Finance Ministry (AOFM) sells A$150M in 1.25% 2022 Indexed bonds; avg yield 0.2776%; bid-to-cover 3.63x

Asia equities notable movers

Australia

Bluescope (BSL) +4.6%: Market conditions remain stable and at elevated levels; stronger pricing, volumes and margins in H2 FY17 v H2 2016 - investor presentation

Ansell (ANN) +4.1%; Raised at Morgan Stanley

CSL Ltd (CSL) +1.3%; To acquire 80% stake in Chinese plasma fractionator for $352M

Japan

Fujitsu (6702) +2.0%; Said to mull raising dividend for FY17 - Nikkei

Toshiba (6502) -0.3%; Western Digital said to submit a new chip proposal to Toshiba this week; May raise offer to ¥2T ($18.2B) - Japan press

Softbank (9984) -1.2%; Reportedly reaches agreement to combine India's Flipkart with Snapdeal - Nikkei

Hong Kong

Ping An (2318) +1.1%; Reports May YTD gross premium CNY211.2B, +38.6% y/y

L'Occitane (973) +0.8%; Reports Final FY16/17 Net €131.9M v €121.3Me, Rev €1.32B, +3.2% y/y

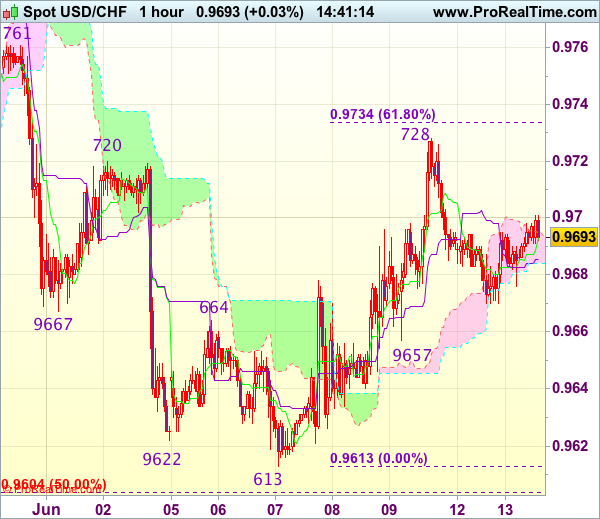

Trade Idea : USD/CHF – Hold short entered at 0.9720

USD/CHF - 0.9689

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9691

Kijun-Sen level : 0.9686

Ichimoku cloud top : 0.9695

Ichimoku cloud bottom : 0.9684

Original strategy :

Sold at 0.9720, Target: 0.9620, Stop: 0.9720

Position : - Short at 0.9720

Target : - 0.9620

Stop : - 0.9720

New strategy :

Hold short entered at 0.9720, Target: 0.9620, Stop: 0.9720

Position : - Short at 0.9720

Target : - 0.9620

Stop : - 0.9720

The greenback met resistance at 0.9728 late last week and has retreated, retaining our bearishness and consolidation with mild downside bias remains for weakness to 0.9657 support, however, break of 0.9640 is needed to signal the rebound from 0.9613 has ended, bring retest of this level first. A break below this level would extend recent decline to 0.9600-05 (50% projection of 1.0100-0.9692 measuring from 0.9808) later.

In view of this, we are holding on to our short position entered at 0.9720. Above said resistance at 0.9728 would abort and signal a temporary low has been formed at 0.9613 last week instead, bring a stronger rebound to 0.9761 resistance but price should falter below resistance at 0.9808.

Countdown To FOMC And UK Inflation Figures

The FOMC meeting is scheduled for Wednesday, and the markets are likely to remain flat in the near term. The economic calendar was light yesterday. In the UK, politics continued to bring uncertainty to the markets, which kept the British pound subdued.

Looking ahead, a lot of economic releases lined up for today. This includes the UK inflation figures, which is expected to show that consumer prices rose 2.7% in May. Germany's ZEW economic sentiment will also be released which is expected to show a modest increase to 21.6 on the index. In the U.S. producer price index is expected to remain flat following a 0.5% increase.

EURUSD intraday analysis

EURUSD (1.1191): EUR/USD closed with a doji candlestick yesterday, and the price action is likely to push lower ahead of the FOMC meeting. On the 4-hour chart, the retracement seen yesterday saw price action retesting the break-out level from the rising wedge pattern.

This puts EURUSD in place to post declines down to 1.1100 in the near term. We expect this to occur towards mid-week with the FOMC meeting in focus. To the upside, any retracement is likely to test the resistance level at 1.1245. Failure to reverse gains here will put EURUSD on a bullish trajectory with further gains likely if we see a daily close above 1.1245.

GBPUSD intraday analysis

GBPUSD (1.2652): GBPUSD continued to extend the declines, and now the support at 1.2600 will be likely tested in the near term. This completes the break-down of the head and shoulders pattern. Price action could possibly find support at 1.2600 with a little retracement likely although price action is likely to remain flat within 1.2600 and 1.2800.

In the event of a continued bearish momentum, GBPUSD will test the lower support at 1.2400. However, with the Stochastics currently overbought, we could see some near-term upside at 1.2800.

USDJPY intraday analysis

USDJPY (1266.44): Gold price remains rather subdued yesterday after posting strong declines for nearly three days at a stretch. Support on the daily chart is seen at 1250.00. On the 4-hour chart, price tested the support at 1263 closing with a doji. A near-term upside move could see gold prices retest 1274 where resistance could be established.

Thus, Gold could remain range bound within 1274 and 1263. Below 1263, the support at 1250 remains to the downside, while above 1274, gold prices could test 1287 - 1288 resistance level.