Sample Category Title

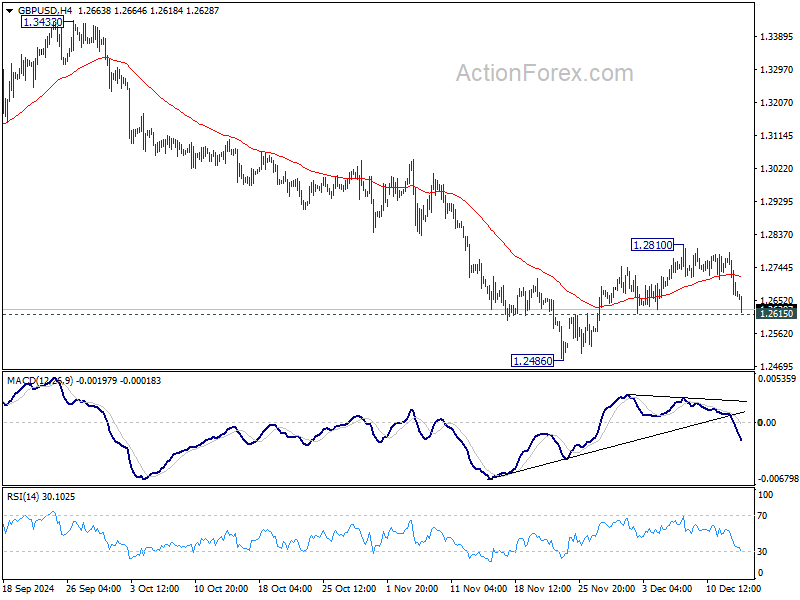

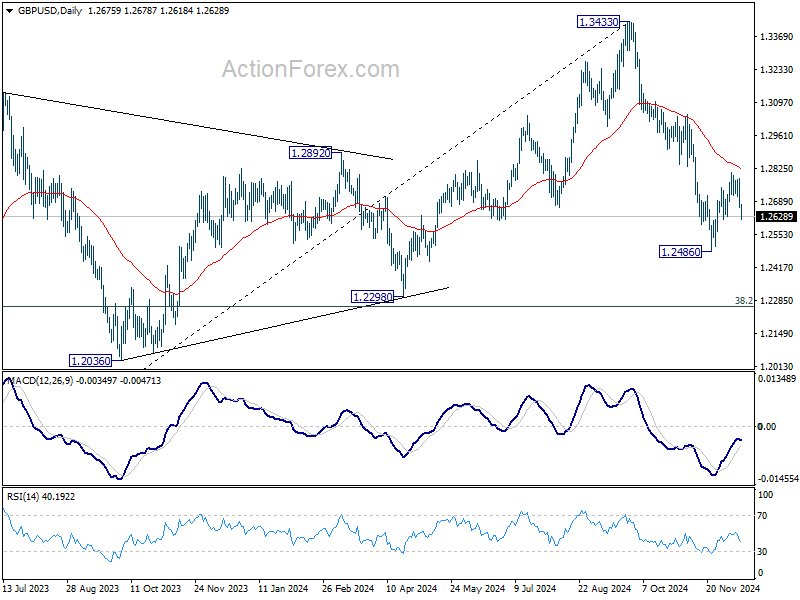

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2631; (P) 1.2710; (R1) 1.2752; More...

Sterling's extended decline today suggests that corrective rebound from 1.2486 has completed at 1.2810 already. Immediate focus is now on 1.2615 minor support. Firm break there will bring retest of 1.2486 first. Break there will resume whole decline from 1.3433 to 1.2298 cluster support zone.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

Sterling Drops on Surprise UK GDP Contraction, Dollar Strengthens

Sterling slumped broadly today after UK GDP unexpectedly contracted in October, missing forecasts of modest growth. This contraction underscores the challenges facing the UK economy, which has been grappling with persistent inflation and uncertainty following the Autumn Budget. The government’s recent pledge to transform the UK into the fastest-growing G7 economy now seems even more "ambitious". While BoE is expected to keep interest rates unchanged at next week’s meeting, deteriorating economic conditions could challenge expectations of four rate cuts in 2025, particularly if the growth outlook weakens further.

Meanwhile, Dollar surged overnight, supported partly by the dovish 25bps rate cut by ECB and stronger-than-anticipated US PPI data. 10-year Treasury yield climbed above the 4.3% mark, reflecting worries over ongoing inflationary pressures. Coupled with recent CPI data showing a plateau in disinflation, Fed remains on track for a pause in its rate-cutting cycle after this month’s expected 25bps reduction. The path of rate easing next year looks more set to be gradual, with terminal rates potentially higher than previously anticipated, reinforcing support for the greenback.

So far this week, Dollar has emerged as the strongest performer, followed by Australian Dollar, which drew strength from surprisingly robust employment data. Canadian Dollar ranks third. At the other end of the spectrum, Japanese Yen is the weakest, with limited reaction to the Tankan Survey data released today. Swiss Franc and New Zealand Dollar also underperformed, while Euro and Sterling occupy a neutral middle ground.

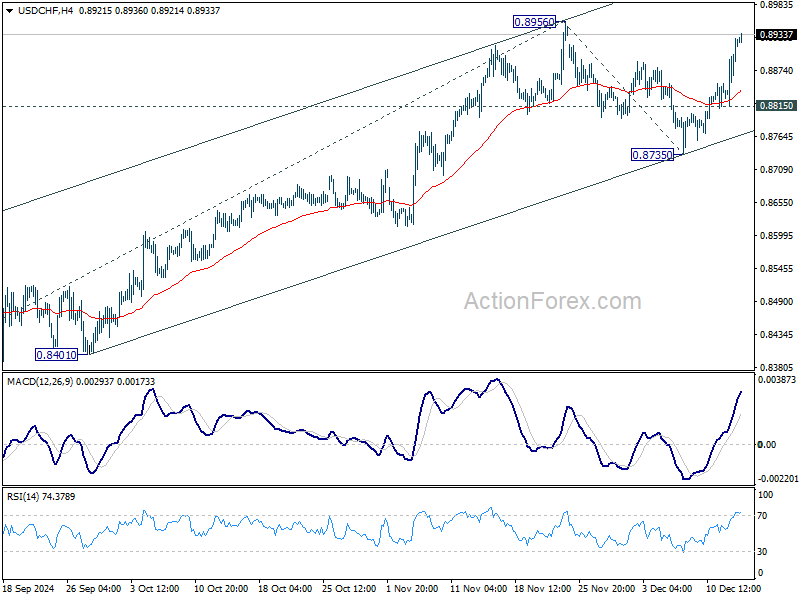

Technically, Dollar is gaining bullish momentum again with break of 1.0471 minor support in EUR/USD. Retest of 1.0330 should be seen next. To solidify Dollar's momentum, some more progress will be needed including breaking of 1.2615 minor support in GBP/USD, 0.6336 support in AUD/USD, and 0.8956 resistance in USD/CHF.

In Asia, Nikkei fell -0.95%. Hong Kong HSI is down -1.82%. China Shanghai SSE is down -2.01%. Singapore strait times is up 0.16%. Japan 10-year JGB yield fell -0.0083 to 1.043. Overnight, DOW fell -0.53%. S&P 500 fell -0.54%. NASDAQ fell -0.66%. 10-year yield rose 0.053 to 4.324.

UK economy contracts -0.1% mom in Oct, dragged down by weak production

UK GDP fell by -0.1% mom in October, disappointing expectations for 0.1% mom growth. The decline was primarily driven by a -0.6% mom contraction in production output, with no growth observed in services and a -0.4% mom decline in construction output.

On a rolling three-month basis, GDP showed a marginal increase of 0.1% in the period ending October, compared to the prior three-month period. This modest growth was supported by a 0.1% expansion in services and a 0.4% rise in construction output. However, production output contracted by -0.3%, weighing on overall performance.

Japan's Tankan Survey: Manufacturing Confidence Improves to 14

Confidence among Japan’s major manufacturers showed a modest recovery in Q4, breaking a two-quarter decline. The Tankan large manufacturing index rose to 14 from 13, slightly exceeding market expectations. However, the outlook dipped marginally from 14 to 13, though still better than the anticipated 11.

In contrast, the non-manufacturing sector, which includes services, saw its index decline to 33 from 34, marking the first deterioration in two quarters. The outlook for non-manufacturers held steady at 28.

On a bright note, large Japanese companies across sectors plan to boost capital expenditure by 11.3% in the fiscal year ending March 2025. This is a notable increase from the 10.6% projection in the September survey and surpasses market forecasts of 9.6%.

NZ BNZ PMI falls to 45.5, 21st month of contraction

New Zealand’s BNZ Performance of Manufacturing Index dipped from 45.7 to 45.5 in November, marking its lowest reading since July 2024 and extending the contraction streak to 21 consecutive months. Despite some improvement in select components, the sector remains under significant strain, highlighting the challenges of achieving a meaningful turnaround.

Production weakened further, dropping from 44.0 to 42.5, signaling continued struggles in output. New orders also plunged from 48.5 to 44.8, underlining the persistent lack of demand. In contrast, employment improved modestly from 46.0 to 46.9, and finished stocks edged higher from 47.8 to 49.3. Deliveries saw the most notable recovery, rising from 44.9 to 49.9, yet still narrowly missed returning to expansion territory.

The sentiment among respondents remains predominantly negative, with 56% of comments in November reflecting pessimism, slightly up from 53.5% in October. Recurring concerns revolve around weak order volumes and the enduring pressures of high living costs. However, this negativity has moderated from its peak of 71.1% in mid-2024, suggesting some stabilization.

Doug Steel, Senior Economist at BNZ, noted that while manufacturers are beginning to show improved confidence about the future, “the main message of a manufacturing sector still under significant pressure remains. There is scant evidence of a general turnaround in activity to date.”

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2631; (P) 1.2710; (R1) 1.2752; More...

Sterling's extended decline today suggests that corrective rebound from 1.2486 has completed at 1.2810 already. Immediate focus is now on 1.2615 minor support. Firm break there will bring retest of 1.2486 first. Break there will resume whole decline from 1.3433 to 1.2298 cluster support zone.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

UK economy contracts -0.1% mom in Oct, dragged down by weak production

UK GDP fell by -0.1% mom in October, disappointing expectations for 0.1% mom growth. The decline was primarily driven by a -0.6% mom contraction in production output, with no growth observed in services and a -0.4% mom decline in construction output.

On a rolling three-month basis, GDP showed a marginal increase of 0.1% in the period ending October, compared to the prior three-month period. This modest growth was supported by a 0.1% expansion in services and a 0.4% rise in construction output. However, production output contracted by -0.3%, weighing on overall performance.

Keeping Up With the Central Banks

This week has been rich in terms of interest rate cuts from major central banks. The Reserve Bank of Australia (RBA) didn’t cut its rates but gave an unexpectedly dovish statement, citing that the RBA officials are turning more confident that inflation is on path toward their policy goal. The Bank of Canada (BoC) delivered a second 50bp cut in a row, following three 25bp cuts before that. Then, the Swiss National Bank (SNB) delivered a 50bp cut – it was not the base case scenario but it was not a surprise, either. The SNB has recently stepped up efforts to counter the franc’s appreciation, especially given the accelerated selloff in the euro since Trump’s election which pulled the EURCHF down to the lowest levels on record. The EURCHF rebounded after the SNB decision, the USDCHF also made a significant move to the upside and the SMI gained. The aggressive messaging from the SNB – warning that it could go negative on rates if it is needed – will hopefully help the franc lose field in the coming months. But one thing is certain, the SNB should remain more dovish than its peers to give the franc the opportunity to weaken without intervention. Otherwise, the global political and geopolitical uncertainties will continue to play in favour of the franc. What a problem to have!

Elsewhere, the European Central Bank (ECB) also cut, but the European officials decided to go ahead with a cautious 25bp cut before Xmas, and Lagarde didn’t say much about what the ECB would do in the next meetings. She stuck to the ‘data dependence’ rhetoric. But, still, the ECB lowered its growth and inflation forecasts – reviving hope of back-to-back cuts next year – but not too much either as Lagarde highlighted that inflation has come down but remains strong and that risks to inflation remains high. She talked about geopolitical risks that could boost energy prices and climate risks that could boost food prices. She didn’t mention Trump, she rather said that the euro zone countries should consider Mario Draghi’s innovation booster plan to give the European economies a boost. She is right but the Europeans have bigger problems today, they should first get their leadership issues right. Anyway, the ECB decision and Lagarde’s speech had a hawkish flavour yesterday, the Stoxx 600 index closed slightly down.

The EURUSD fell, however, but the selloff was mostly explained by a higher-than-expected US PPI print that landed just between the ECB decision and Lagarde’s press conference. The data showed that the producer price inflation in the US ticked higher to 3% in November, up from 2.6% printed a month earlier and expected by analysts. But the surge in egg prices was one of the major drivers. As such, the November reading was interpreted as being ‘probably less informative (and threatening) on the overall trend’ than the headline figure suggested. Nonetheless, the US 2-year yield advanced past the 4.20%, the major equity indices gave back gains and the US dollar jumped – the rise of the dollar was also due to the weakening yuan after the Chinese authorities said this week that they would let the yuan weaken to boost exports, and due to rate cuts from other major central banks throughout this week. As a result, the dollar looks stronger this Friday than it looked last Friday. The probability of a 25bp cut slightly eased but activity on Fed funds futures continues to asses a very comfortable 96% probability for an additional 25bp cut that the US probably doesn’t need in December. But it’s probably too late to turn for the gigantic Fed ship a few days before their next decision – they only do that when it’s a dovish surprise. But the chances of a January cut are melting by the day, and that’s supportive of the US dollar. As such, the ECB’s cautious tone could slow down the euro’s depreciation but will not stop it if the Fed expectations turn more hawkish at the beginning of next year. The EURUSD fell yesterday to 1.0460, Cable was lower too, on the back of a broadly stronger US dollar, and the USDJPY is flirting with the 153 level this morning as traders are scaling back their Bank of Japan (BoJ) rate hike bets for next week. Still, around 60% of economists in a recent Reuters poll think that a 25bp hike is still on the menu of the December meeting – an expectation that should limit the USDJPY’s upside potential into 155.

ECB Lowered Interest Rates by 25bp as Widely Expected

In focus today

In the euro area, we receive data on industrial production from October, which will give the first hard data point for production in Q4. Industrial production has been on a negative trend for two years without any sign of stabilisation.

Statistics Sweden publishes the latest labour force surveys outcome at 8:00 CET. Whereas the increase in unemployment has started to slow down, it is still somewhat too early to hope for a drop in unemployment, we do however expect the numbers to improve during next year.

Economic and market news

What happened overnight

In Japan, the Tankan survey showed that the business confidence index for big manufacturers rose to 14 (cons: 12; prior 13). The index for the big non-manufacturers decreased slightly to 33 but remained elevated (cons: 32; prior 34). This bodes well for Bank of Japan's plans to begin hiking interest rates from still very low levels. However, the survey also showed that companies expect business conditions to worsen over the next three months. This should be seen in the light of intensified labour shortage becoming an increasing problem, which could lead to a constraint on growth. Furthermore, global demand is still weak, and threats of higher tariffs from US president-elect Trump could also have played a role in the weaker expectations.

What happened yesterday

In the euro area, the ECB delivered a 25bp rate cut bringing the deposit rate down to 3.0%. In our view the decision was not clear cut. The ECB could have opted for a 50bp rate cut considering the weak economic growth outlook. However, staff projections showing inflation at the target led the ECB to conclude that a 25bp rate cut was sufficient. The decision was a dovish 25bp rate cut, though, and we assess the communication around it to be as close as possible to a 50bp cut without delivering such a cut. Lagarde also said that there were deliberations of a 50bp rate cut. Markets did not take any cues from the press conference and continues to price in 125bp of rate cuts in 2025. See Flash: ECB Review - A dovish 25'er, 13 December.

In Switzerland, the Swiss National Bank (SNB) lowered the policy rate by 50bp to 0.50%. Markets had been pricing in around a 35bp cut prior to the decision. The cut marked the fourth consecutive cut and was the first cut of 50bp. EUR/CHF increased after the announcement. The inflation forecast was adjusted significantly lower in the near term to around 0.2-0.3% y/y in the coming quarters before it is expected to pick up again in 2026.

In Norway, the regional network survey was not too far from the expectation, but if anything, it was slightly to the hawkish side. We note that capacity utilisation and labour shortage were unchanged. Wage growth expectations for this year were unchanged but lifted to 4.5% next year. This was a hawkish surprise amid other indicators pointing to a downside risk to Norges Bank's 4.3% wage growth estimate for next year. Growth expectations for Q1 2025 were as expected at 0.3%. On the back of this report, we see it as highly unlikely that Norges Bank will open the door for a January cut after next week's meeting.

In Sweden, the headline flash estimate was confirmed (0.3% m/m; 1.6% y/y). CPIF y/y was revised down to 1.8% from 1.9% in the flash release (so merely a rounding effect). CPIF excluding energy flash estimate was confirmed as well (-0.2% m/m; 2.4% y/y).

Equities: Global equities declined yesterday as negative macroeconomic data overshadowed the messages from the ECB and SNB. The slightly stagflationary signals from the US PPI and jobless claims caused the US to underperform compared to the rest of the world, with most US indices ending at their daily lows. Yields rose for the "wrong" reasons, leading to defensives outperforming alongside large caps. The VIX edged slightly higher, and while investors are currently behaving relatively calmly, we would not be surprised to see volatility increase significantly if a series of negative macroeconomic data emerges in the current exuberant environment. In the US yesterday, the Dow fell by 0.5%, the S&P 500 by 0.5%, the Nasdaq by 0.7%, and the Russell 2000 by 1.4%. Asian markets and European futures are lower this morning, influenced by the negative late-hour movements on Wall Street yesterday. US futures are mixed, with large-cap tech standing out on the positive side.

FI: EUR rates declined during most of Lagarde's press conference yesterday, only to reverse direction following her remarks that the ECB 'has already covered a lot of grounds' in terms of policy easing. Markets took this as a hint that the terminal rate could be closer to today's level than previously assumed. 10Y EUR rates rose 7bp throughout the session, with the 2s10s curve was close to unchanged. Peripheral spreads saw noticeable widening with the BTP-Bund spread up by 8bp for the day, while the Bund ASW-spread was unchanged at 2bp.

FX: EUR/USD fluctuated within a half-figure range multiple times before closing lower, below the 1.05 mark, as the anticipated 25bp ECB rate cut had limited impact on the pair. AUD/USD experienced a volatile trading week but continues to trend lower, hovering around the 0.64 mark. The SNB's unexpected 50bp rate cut prompted a sharp rise in EUR/CHF. EUR/SEK has traded within a narrow range this week, holding above 11.50, while EUR/NOK ended the week unchanged around 11.70 after a brief decline.

Japan’s Tankan Survey: Manufacturing Confidence Improves to 14

Confidence among Japan’s major manufacturers showed a modest recovery in Q4, breaking a two-quarter decline. The Tankan large manufacturing index rose to 14 from 13, slightly exceeding market expectations. However, the outlook dipped marginally from 14 to 13, though still better than the anticipated 11.

In contrast, the non-manufacturing sector, which includes services, saw its index decline to 33 from 34, marking the first deterioration in two quarters. The outlook for non-manufacturers held steady at 28.

On a bright note, large Japanese companies across sectors plan to boost capital expenditure by 11.3% in the fiscal year ending March 2025. This is a notable increase from the 10.6% projection in the September survey and surpasses market forecasts of 9.6%.

NZ BNZ PMI falls to 45.5, 21st month of contraction

New Zealand’s BNZ Performance of Manufacturing Index dipped from 45.7 to 45.5 in November, marking its lowest reading since July 2024 and extending the contraction streak to 21 consecutive months. Despite some improvement in select components, the sector remains under significant strain, highlighting the challenges of achieving a meaningful turnaround.

Production weakened further, dropping from 44.0 to 42.5, signaling continued struggles in output. New orders also plunged from 48.5 to 44.8, underlining the persistent lack of demand. In contrast, employment improved modestly from 46.0 to 46.9, and finished stocks edged higher from 47.8 to 49.3. Deliveries saw the most notable recovery, rising from 44.9 to 49.9, yet still narrowly missed returning to expansion territory.

The sentiment among respondents remains predominantly negative, with 56% of comments in November reflecting pessimism, slightly up from 53.5% in October. Recurring concerns revolve around weak order volumes and the enduring pressures of high living costs. However, this negativity has moderated from its peak of 71.1% in mid-2024, suggesting some stabilization.

Doug Steel, Senior Economist at BNZ, noted that while manufacturers are beginning to show improved confidence about the future, “the main message of a manufacturing sector still under significant pressure remains. There is scant evidence of a general turnaround in activity to date.”

RBA’s Big Pivot and Head Fakes Ahead

The RBA’s language change this week revealed a change in thinking driven by shifts in the data. But some data surprises might just be head fakes.

Something happened between 28 November and 9 December to shift the RBA’s thinking. The first of these dates marked a speech by Governor Bullock that can only be described as hawkish. It highlighted the RBA’s post-Review framework of treating instances of inflation above target as a sign of a positive output gap. The labour market was characterised as being too tight to be consistent with full employment. The slowdown in wages growth was not even mentioned.

Roll forward less than two weeks, and the language in the Board statement following the December meeting was rather different. The post-meeting statement highlighted that ‘some of the upside risks to inflation appear to have eased’. The possibility of a rate hike was no longer canvassed. And it dropped the ‘not ruling anything in or out’ and ‘vigilant’ language that had been in the post-meeting statement for most of the year.

Post-meeting comments by both the Governor and Deputy Governor have highlighted that both wages growth and the national accounts were weaker than expected. The Wage Price Index data were already available in time for the Governor’s speech, so it must have been the combination of the two that forced the shift in thinking. (The national accounts also include important measures of growth in wages and labour costs, which slowed noticeably in the quarter.)

The change in language certainly shifted market pricing of future rate moves. And to be fair, the probability of a rate cut earlier than our current base case of May 2025 has lifted, both because of the data flow and the RBA’s evident response to it. But a lot can happen between now and May.

One example of the ‘lot that can happen’ is that, since then, we have seen the surprisingly strong labour market data for November. But, Westpac Economist Ryan Wells cautions that this could, like last year, be a bit of a ‘head fake’ related to shifting seasonal patterns rather than an indication of a genuinely stronger labour market. Black Friday sales are becoming a bigger thing than they used to be, which is shifting the seasonal pattern of both employment and consumer spending. (Normal seasonal adjustment processes can’t fully offset seasonality that is shifting.)

Given ongoing cost-of-living pressures, it is no surprise that households are responding by going hard in the sales and holding back when things aren’t on sale. This also means that the next couple of months of household spending data could also be a bit of a ‘head fake’. And because Black Friday came late in the month, the December figures will be affected as well, as we saw in the Westpac Card Tracker this week. The RBA, and other observers of the economy, will need to be careful that they don’t jump at economic shadows in the next few months.

Along with seasonality, the labour market data might be providing a bit of a ‘head fake’ because of the skewed nature of current employment growth. As we have previously highlighted, most of the growth in employment over the past year or so has been in the non-market sector. Governor Bullock correctly pointed out in her post-meeting media conference that the expansion of the care economy represents important work in its own right – and work that frees up family members from unpaid care work.

But, as we have noted previously, the current skew towards care work has two implications that can be misleading if not treated carefully.

Firstly, care work tends to be lower-paid and less capital-intensive than many other jobs. So these jobs account for less GDP per hour worked than most other jobs. The result is apparent weakness in productivity growth driven by compositional change, even though individual workers and firms are not becoming less productive. If you wondered at Deputy Governor Hauser’s comment this week – that the narrative about slow productivity did not resonate with the RBA Board members involved in businesses – this is why. They are involved in market-sector industries, where labour productivity growth has been reasonable in recent quarters.

The problem here is that the models the RBA uses to estimate the output gap rely on estimates of trends in potential output that in turn rely on estimates of trend productivity growth. These estimates of trend are based on statistical techniques that impose considerable smoothness on those estimated trends. They are not designed to capture the kinds of compositional effects currently occurring.

Secondly, the current run-up in non-market employment will not last forever. The rapid run-up in spending in these areas has already spurred a reaction. Some news reports suggest that growth in NDIS spending is slowing a bit earlier than originally planned. As spending on these programs slows, so will the expansion of care-related employment. When that occurs, what will keep employment growth swift enough to keep pace with still-rapid population growth?

One thing working in the other direction is that labour force participation might not stay where it is either. Participation rates in Australia have been on a multi-decade upward trend, reflecting rising female participation in the workforce as well as increased participation by older people of both sexes as life expectancy and health outcomes improve. Around that upward trend, participation can fluctuate in line with job opportunities. At least some of the recent increase in participation was likely to have been a response to cost of living pressures, as we have previously noted. As those pressures ease, so too could the participation rate. As was the case this month, this could hold down unemployment due to people exiting the labour market. It would also contribute to other measures of labour market slack and could even mislead some observers about the true state of demand and the labour market.

Given all this, it will be worth taking care to avoid getting too hung up on every data point in the next few months, and instead focus on how they fit together.

Cliff Notes: The Detail Matters

Key insights from the week that was.

While the RBA’s decision to leave the cash rate unchanged at 4.35% was widely anticipated, there were noteworthy shifts in language in the decision statement. Most poignant was the removal of the “not ruling anything in or out” guidance that stood in place for the much of this year, suggesting risks to the outlook are becoming more balanced. Indeed, the Board also made it known that it is “gaining some confidence that inflationary pressures are declining in line with [their] recent forecasts”, and that it is relatively less concerned about upside inflation risks. Mirroring these developments, Governor Bullock adopted a decidedly less hawkish tone in the subsequent press conference, speaking at length about the dataflow since the previous meeting which, on balance, has supported the shift towards more neutral language. When pressed on the possible timing of interest rate relief, the Governor conceded that there are scenarios in which the next meeting, in February, could see an initial rate cut, but stopped short of describing one, however.

Given these developments, an interest rate cut in February or April cannot be entirely ruled out; but on balance, May remains the most likely candidate for the start of the normalisation cycle. The next few months of data will prove critical to both the timing and scale of the rate cutting cycle. We continue to expect a relatively short episode, a cumulative 100bps of easing delivered from May through Q4 2025 to 3.35%, a rate we consider to be broadly neutral for the economy.

Data-wise, this week also saw some significant surprises in the latest labour market update, employment rising at a solid clip (+35.6k) and the unemployment rate falling sharply to 3.9%. We caution against reading too much into these results given some underlying anomalies – a ‘pull-forward’ of jobs from December to November due to shifting seasonal patterns and weaker supply jolted the unemployment rate lower in November but may reverse in December. On a multi-month view, it is notable that all key measures of underutilisation are finishing the year near where they started; all the while, wages growth has been decelerating at pace. Provided these dynamics persist, there is a risk that the RBA might find the labour market is closer to balance than its current forecasts imply.

Major US data releases over the last seven days dominated the dataflow offshore. Last Friday’s labour market report was broadly in line with market expectations and our view that slack in the US labour market is building gradually. The payrolls figures showed a 227k increase in November and modest revisions of 56k to the September and October readings. These outcomes left the six-month average gain at 143k, down from 207k in the first half of the year and below the 200k per month we believe are necessary to keep the labour market in balance. The unemployment rate was 4.2%, up 0.1ppts from the prior month and 0.5ppts from the beginning of the year. Nevertheless, growth in hourly earnings remained unchanged at 4%yr, at the top of the range broadly consistent with consumer price inflation of 2%yr. The gradual softening of the labour market should see wage growth continue to soften, limiting inflationary pressures across the economy.

This week’s US CPI release was also broadly as expected and consistent with our view that US disinflation is proceeding. Headline and core CPI indices were both up 0.3% for respective annual rates of 2.7%yr and 3.3%yr, little changed from October. Core goods stood out in the detail, with the steepest increase in 1½ years of 0.3%mth. It was mainly driven by increases in the used and new car categories, likely linked to the impact of recent hurricanes. The shelter component was also up 0.3%mth, leaving the annual rate at 4.7%yr, 1.5ppts below the rate seen at the end of last year. Leading indicators point to the downtrend in shelter inflation continuing, although admittedly it has been slower to come through than expected. Overall, this week’s data has seen market pricing for a 25bp cut at the December FOMC meeting firm to a near certainty. We concur with the market’s view. Critical for 2025 will be the FOMC’s current assessment of risks, as evinced by both the quantitative forecasts and Chair Powell’s guidance in the meeting press conference.

Other major central banks continued easing monetary policy this week. The ECB delivered another 25bp cut at their December meeting, as expected. The tone of the post policy-meeting communication was dovish, with the downtrend in inflation given weight by ECB staff revising their forecasts lower and President Lagarde making known the Governing Council’s confidence and commitment to ease policy towards neutral in coming quarters. Meanwhile, the Bank of Canda acted more forcefully, delivering another 50bp cut. The outsized move followed a further increase in the unemployment rate, disappointing activity growth in Q3 and partial data pointing to further weakness in Q4 which seems likely to persist into next year. With the policy rate now close to its neutral level, decisions about further easing will be made meeting by meeting based on the Bank's assessment of risks.

After this week’s Chinese CPI data release showed annual inflation remaining near zero into year end, at 0.2%yr, the focus for China quickly turned to news headlines from the latest Politburo meeting and the Central Economic Work Conference. While subtle in tone, the wording used in post-meeting communications carries significant meaning. According to press reports from the official Xinhua news agency cited by Bloomberg, the Politburo has made clear that, for the first time since the GFC, 2025 will see “moderately loose” monetary policy as well as “more” pro-active fiscal policy. Premier Li Qiang subsequently pledged to “forcefully lift consumption” by “every means possible” and, after the Work Conference, a similar message was given as “lifting consumption vigorously” and stimulating overall domestic demand were made authorities’ top priority, reportedly for only the second time in 10 years. Press reports also carried references to improving the social safety net, a long-needed reform. We will likely have to wait until early-2025 for clear guidance on policy detail, but it a material increase in policy support is coming. To what extent its benefit is offset by US trade policy will only be known in time. Westpac remains constructive on China’s real economy in 2025, but believe it will take time for participants to gain confidence and markets to price improving fundamentals.

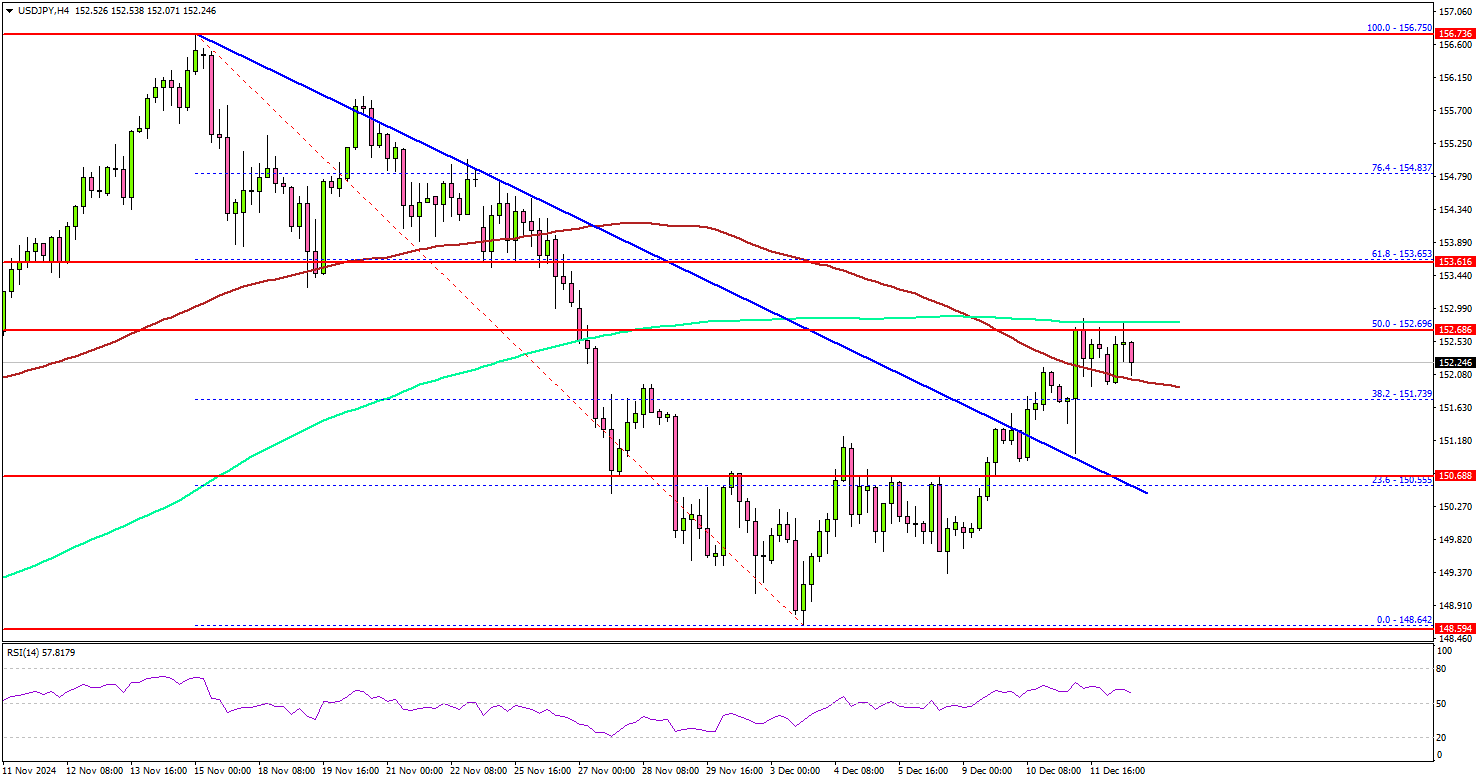

USD/JPY At Crossroads: Key Levels In Focus

Key Highlights

- USD/JPY started a fresh increase above the 151.00 resistance zone.

- It cleared a key bearish trend line with resistance at 151.20 on the 4-hour chart.

- EUR/USD failed to recover above the 1.0620 level and trimmed some gains.

- Ethereum extended gains and might stabilize above the $4,000 level.

USD/JPY Technical Analysis

The US Dollar started a fresh increase from the 148.65 zone against the Japanese Yen. USD/JPY surpassed 150.50 and 151.00 to move into a short-term positive zone.

Looking at the 4-hour chart, the pair surpassed the 38.2% Fib retracement level of the downward move from the 156.75 swing high to the 148.64 low. It cleared a key bearish trend line with resistance at 151.20.

The bulls even pushed the pair above the 100 simple moving average (red, 4-hour) but they faced hurdles near the 200 simple moving average (green, 4-hour).

The 50% Fib retracement level of the downward move from the 156.75 swing high to the 148.64 low also acted as a resistance. On the upside, the pair could face resistance near the 152.70 level.

The first major resistance is near the 153.20 level. A close above the 153.20 level could set the tone for another increase. The next major resistance could be the 154.50 level, above which the price could climb higher toward the 155.00 resistance.

On the downside, immediate support sits near the 151.00 level. The next key support sits near the 150.50 level. Any more losses could send the pair toward the 150.00 level.

Looking at EUR/USD, there was no upside break above the 1.0620 resistance and the pair might now start another decline.

Upcoming Economic Events:

- US Import Price Index for Nov 2024 (MoM) – Forecast -0.2%, versus +0.3% previous.

- US Export Price Index for Nov 2024 (MoM) – Forecast -0.2%, versus +0.8% previous.