Sample Category Title

BoE Leaves Its Bank Rate At 0.25%, Maintains Bond Purchases At £435B

'The medium-term inflation forecast is lower and that's why markets have taken it as dovish.' — Alan Clarke, Scotiabank

At its latest policy meeting, the Bank of England's Monetary Policy Committee voted by a majority of 7-1 to leave the bank rate at 0.25%, with Kristin Forbes being the only one favouring an immediate hike in rates on the back of an uptick in pipeline inflation pressures that, in her opinion, has pushed the CPI to somewhat uncomfortable levels. Overall, the 'no move' came as no surprise, as the vast majority of economists were not expecting to see any change in the monetary policy. In the report, the BoE said that sustainability of the current loose policy would to a great extent depend on inflation expectations holding steady. Despite that, some of the MPC members commented they would give up their dovish stance relatively soon should they see any signs of an upside momentum establishing in GDP or inflation. In the meantime, the British Central Bank also decided to maintain its government bond-purchase programme at £435B, while holding corporate bond-buying plans at up to £10B. Furthermore, there also were some alterations to the Bank's UK economic forecasts, with officials slashing their 2017 growth outlook to 1.9% from 2%.

US Producer Prices Increase Above Expectations In April

'April's PPI report underlined this with a strong set of data that suggests that input costs are rising at the fastest rate in five years.' - Michael Shaoul, Marketfield Asset Management

The seasonally adjusted Producer Price Index for final demand rose more than expected in April, official data showed on Thursday. According to the Bureau of Labour Statistics, US producer prices rose 0.5% for the month of April, following the preceding month's 0.1% decline and surpassing analysts' expectations for a 0.2% hike. On a yearly basis, the Producer Price Index posted a gain of 2.5% in the reported month, the strongest increase since February 2012, compared to 2.3% registered in March. A 0.4% advance in prices for final demand services caused over 60% of the rise in the final demand PPI. That climb was mainly driven by higher costs of investment advice, dealing, securities brokerage and related services. Furthermore, the report showed prices for goods and food rose 0.5% and 0.9% respectively, while energy prices climbed 0.8%, supported by a 3.9% jump in the gasoline cost. In the meantime, the so-called core PPI, which excludes volatile items, showed a monthly advance of 0.4% and a 1.9% gain year-over-year with both readings going beyond economists' forecasts.

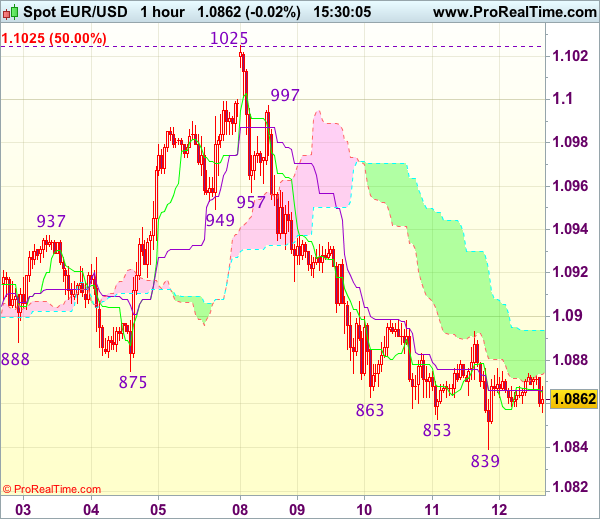

Trade Idea : EUR/USD – Sell at 1.0955

EUR/USD - 1.0860

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.0865

Kijun-Sen level : 1.0866

Ichimoku cloud top : 1.0894

Ichimoku cloud bottom : 1.0874

Original strategy :

Sell at 1.0955, Target: 1.0840, Stop: 1.0990

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0955, Target: 1.0840, Stop: 1.0990

Position : -

Target : -

Stop : -

Euro’s recovery after falling briefly to 1.0839 yesterday suggests consolidation above this level would be seen and corrective bounce to 1.0895-00 is likely, however, reckon upside would be limited to 1.0930-35 and renewed selling interest should emerge around 1.0955-60, bring another decline later. A break of said support at 1.0839 would extend the fall from 1.1025 top for at least a strong retracement of early upmove towards 1.0800 but reckon 1.0770-75 would hold from here.

In view of this, we are looking to sell euro on recovery as 1.0955-60 should limit upside. Above 1.0970 would defer and risk a stronger rebound but a break above resistance at 1.0997 is needed to signal pullback from 1.1025 has ended, bring retest of this level later.

Technical Outlook: EURUSD – Downside Remains At Risk While 10 SMA Caps Recovery Attempts

Double long-legged Doji candles of past two days signal that bear-leg from 1.1020 peak may be losing traction, as fall was contained by rising 20SMA at 1.0838, which underpins today's action after forming bull-cross with 200SMA.

Another supportive factor could be reversal of slow stochastic from oversold zone, however, recovery attempts were so far capped by hourly cloud base (cloud is spanned between 1.0870 and 1.0892).

The pair needs to break above 10SMA (currently at 1.0906) to signal stronger recovery and sideline existing downside risk.

Otherwise, fresh attempts lower could be expected after consolidation, with extension below 200SMA (1.0824) to threaten of filling the gap of 24 Apr and open way for further downside.

The pair on track for weekly close in red and forming weekly bearish engulfing pattern that is seen as strong bearish signal.

Res: 1.0870, 1.0892, 1.0906, 1.0932

Sup: 1.0852, 1.0838, 1.0824, 1.0794

US Dollar Looking Weaker Into Friday’s Close

Economic data from the US continued to remain robust with the initial jobless claims declining to 236,000 for the week ending May 6 while the producer prices rose 0.5% on the month. The markets will be looking to today's consumer price index data. The US dollar was seen rather muted as the US dollar index struggled near the 95.50 resistance level.

In the UK, the Bank of England's monetary policy meeting saw no chance to interest rates and asset purchase. In the inflation forecasts, the central bank expected inflation to overshoot the central bank's target rate and remain around 2.7% this year while growth is expected to show a 0.4% increase in the second quarter.

The British pound was trading weaker on the day with the BoE's meeting and the weak economic numbers released earlier that showed a contraction in manufacturing, construction, and industrial output.

Looking ahead, FOMC members Harker and Evans are due to speak later today while the U.S. will be reporting the monthly CPI and retail sales numbers.

EURUSD intraday analysis

EURUSD (1.0866): EURUSD formed another doji yesterday posting a new one-month low at 1.0838. The price action indicates that the momentum is likely to be slowing and we could expect to see some upside retracement today. 1.0900 remains the key resistance level to the upside

Price action as remained steady near the support level of 1.0863 - 1.0854 and we could expect to see prices bounce off to the upside in the near term. However, resistance is likely to form at 1.0900 - 1.0950. This level also sits close to the 38.2 and 61.8% Fibonacci levels measuring the current decline. A reversal on this pullback will signal a continuation to the downside.

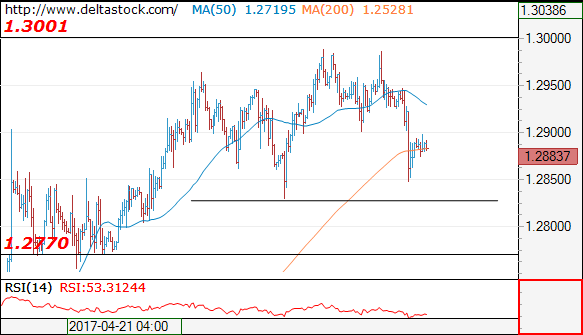

GBPUSD intraday analysis

GBPUSD (1.2885): The British pound slipped yesterday following a weak set of construction, manufacturing and industrial production numbers with the Bank of England's meeting offering little support for the British pound.

However, the GBPUSD looks resilient, and unless we see a close below 1.2800, there is a scope of prices to remain consolidating at the current levels.

Furthermore, the reversal just below 1.3000 handle without the level being tested correctly infers that there is a risk of prices pulling back higher to test this level. For the moment, after the break down below 1.2900, GBPUSD is seen pushing back higher, and an intraday close above this level will signal that prices will consolidate within 1.2900 and 1.2965 levels.

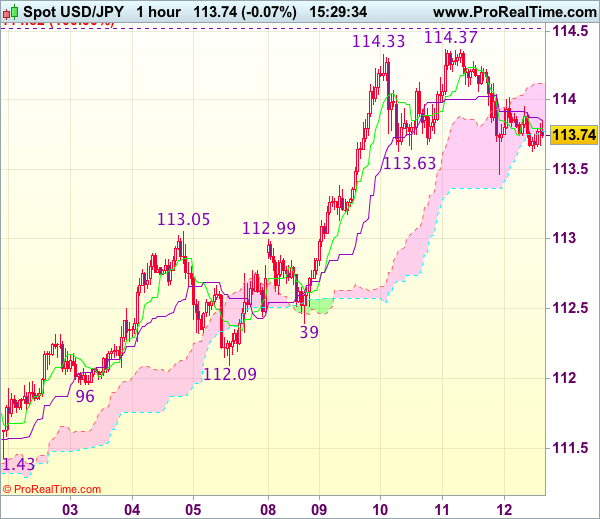

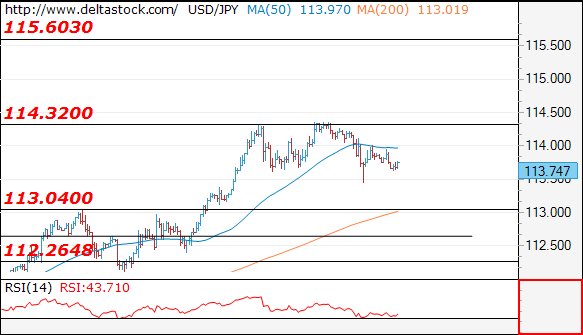

USDJPY intraday analysis

USDJPY (113.74): The US dollar closed on a bearish note yesterday which comes after five straight days of gains. This possibly hints at a short-term correction in prices which could see a test towards 112.50 - 112.875 support level.

On the 4-hour chart, price action has been consolidating near the resistance level of 114.00 - 113.78 region with the previous 4-hour session closing in a doji. A bearish close on the current 4-hour session after the doji could signal a correction towards 112.875 - 112.50 level which could be a strong support level and marks a short-term correction in prices.

Trade Idea : USD/JPY – Buy at 113.15

USD/JPY - 113.75

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.79

Kijun-Sen level : 113.85

Ichimoku cloud top : 114.12

Ichimoku cloud bottom : 113.77

Original strategy :

Buy at 113.15, Target: 114.25, Stop: 112.80

Position : -

Target : -

Stop : -

New strategy :

Buy at 113.15, Target: 114.25, Stop: 112.80

Position : -

Target : -

Stop : -

Dollar’s retreat after rising marginally to 114.37 yesterday has retained our view that further consolidation below this level would be seen and pullback to 113.35-40 is likely, however, still reckon previous resistance at 113.05 (now support) would contain downside and bring another rise later to 114.50-55 (100% projection of 108.13-111.78 measuring from 110.87) but overbought condition should limit upside to 114.75-80 and price should falter below 115.00.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as 113.15-20 should contain downside. A firm break below previous resistance at 112.99-05 would defer and suggest top is formed, bring correction of recent upmove to 112.65-70 but reckon support at 112.39 would remain intact.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 10869

The intraday bias remains negative, for a slide towards 1.0770, en route to 1.0700 support area. Initial intraday resistance lies at 1.0900 and crucial on the upside is 1.0950.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.0950 | 1.1020 | 1.0828 | 1.0770 |

| 1.1020 | 1.1150 | 1.0770 | 1.0676 |

USD/JPY

Current level - 113.74

The corrective pattern below 114.30 is still underway and my intraday outlook is bearish, for a slide towards 113.00 area. Only a break through 114.30 will signal, that the uptrend is renewed, towards 115.60.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 114.30 | 113.50 | 113.00 | 109.40 |

| 115.60 | 115.60 | 112.35 | 108.12 |

GBP/USD

Current level - 1.2883

Yesterday's break through 1.2900 has fixed a minor 'double top' at 1.2985 and the bias is bearish, for a break through 1.2830, towards 1.2770. Initial intraday resistance lies at 1.2900.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2900 | 1.3120 | 1.2830 | 1.2770 |

| 1.3000 | 1.3500 | 1.2770 | 1.2610 |

The Bank Of England (BoE) Kept All Policy Measures Unchanged

Market movers today

German GDP growth for Q1 is due for release today and we estimate strong growth of 0.6% q/q, up from 0.4% q/q in Q4 16, as business sentiment has shown optimism throughout Q1, especially observed in strong PMIs and ifo expectations. Additionally, the euro area reported quarterly GDP growth of 0.5% q/q in Q1 already, which – although not as strong as indicated by the PMI figures – suggests that the German figure should also be solid.

Focus will also be on US inflation with the release of the CPI figure for April. We expect some reversal in both headline and core inflation after they fell sharply in March, driven partly by the timing of Easter and by lower energy prices. We estimate CPI core inflation was 2.0% y/y and headline inflation was 2.3% y/y, which would mean headline inflation has fallen from 2.8% to 2.3% in just two months, with a large part of this due to the base effects of oil prices. Note that although these numbers are at or above 2%, the Fed is more concerned about PCE core inflation, which is still below 2% and showing no signs of accelerating.

US retail sales figures for April are also due for release. Since October 2016, consumer confidence has been very high, indicating tailwinds for private consumption. However, we believe that consumer confidence has run ahead of actual developments and will come down rather than retail sales accelerating. The weak GDP growth in Q1 was driven largely by weak private consumption. Hence, if GDP growth is to pick up in Q2, we need a strong print in the retail sales control group for April. The University of Michigan consumer confidence is also due to be released today and in line with the argument above, we estimate a decline.

Selected market news

The Bank of England (BoE) kept all policy measures unchanged at yesterday's meeting and kept its neutral stance by repeating it could move ‘in either direction'. However, the BoE believes the current market pricing of hikes will be a bit too soft should the economy live up to expectations. One member of the Monetary Policy Committee voted again for a hike, but she is leaving the BoE at the end of June. We still believe the BoE will remain on hold for the next 12 months, as it seems unlikely it will tighten monetary policy in a time of elevated political uncertainty, while a substantially slower growth and/or higher unemployment is likely to be needed before easing. See BoE review:Mainains hawkish twist to neutral stance, 11 May.

ECB Vice-President Vitor Constancio argues that maintaining its ultra-loose monetary policy for longer is a safer way for the ECB to avoid an economic relapse. ECB Chief Economist Peter Praet also attempted to dampen rate hike expectations saying, ‘there is a very strong chain of logic behind the decision to first scale back QE, raising the term premium included in long-term rates, and only then hiking short-term rates'. The market is currently pricing in the first 10bp deposit rate hike from the ECB for the summer next year.

The European Commission is warning France on risks to its public finances, arguing that reining in spending would prove more difficult than previously thought. Presidentelect Emmanuel Macron has promised to bring France's deficit under the 3% ceiling this year given this has consistently been missed since the financial crisis.

According to the FT, Italy is set to remain a concern for EU officials. The country is expected to be the slowest growing euro area country, while its debt ratio will grow to 133.1% this year.

Currencies: US Data To Decide On The Next Directional USD Move

Sunrise Market Commentary

- Rates: Litmus test for US Treasuries

Bonds will especially be sensible to downside US eco surprises today even if we side with consensus (CPI) or even see upside risks (retail sales). US stock markets yesterday also showed first cracks in the armour, suggesting a more profound correction could be coming up. Thus, the bond reaction could be asymmetric (limited room for losses, more potential for gains). - Currencies: US data to decide on the next directional USD move

Today's US CPI and retail sales will be key for ST USD sentiment. We expect both the CPI and the retail sales to meet the consensus or even come out stronger. This should support a further USD rebound. However, a negative surprise might raise doubts on the Fed rate hike path and trigger a significant setback of the dollar. Especially USD/JPY is vulnerable.

The Sunrise Headlines

- US stock markets initially lost around 0.75%, dragged down by the retail sector as Nordstorm followed Macy's and Kohl's with weaker earnings, but eventually erased most of the losses. Most Asian bourses lose ground overnight.

- The Trump administration agreed with Beijing on a broad range of measures aimed at improving the access of American beef producers, electronic-payments providers and natural-gas exporters, among others, to China.

- En Marche! has picked political novices to run in parliamentary elections next month. Only 24 on the list of 428 candidates are sitting MPs, all Socialists, and 52% have never held elected office. Half are women and the average age is 46.

- The PBOC injected fresh funds through a MT lending facility while keeping a tight rein on ST funding in a further effort to dampen speculative investment while keeping the economy adequately funded.

- Austria's political elite is steeling itself for possible early elections after a government crisis that could provide a boost to a far right party just months after it narrowly failed to secure the country's presidency.

- Concern about Canada's heavily indebted households and hot housing market ratcheted higher after Moody's downgraded the ratings for Canada's major banks.

- Today's eco calendar heats up in the US with inflation data, retail sales and University of Michigan consumer confidence. Voting FOMC governors Evans and Harker are scheduled to speak. In EMU, only outdated production data will be released.

Currencies: US Data To Decide On The Next Directional USD Move

US CPI and retail sales to decide on ST USD trend

Yesterday, EUR/USD and USD/JPY initially drifted sideways. Both cross rates lost ground as equities fell prey to modest profit taking . The US eco data (PPI and claims) were better than expected. Core yields rose temporary, but were not able to trigger more USD gains. Technical trading ahead of today's US CPI and retail sales prevailed. EUR/USD closed session at 1.0861, little changed from Tuesday (1.0868). USD/JPY finished the day at 113.86 (from 114.28) on equity softness.

Overnight, the picture on Asian equity markets has changed. Most indices are losing modest ground as investors take profit. Some caution ahead of the US retail sales may be in play. China is the positive exception to the rule as authorities provided additional liquidity to prevent further losses. EUR/USD is stabilizing in the 1.0875 area. USD/JPY trades at 113.65/70, off the recent highs, but above yesterday's correction low. Commodity currencies like the AUD and the CAD show some tentative signs of bottoming after the recent setback.

Today, the US CPI and retail sales are key for global trading, including the dollar. Last month the core CPI unexpectedly declined, questioning whether underlying inflation would trend higher as the Fed assumes. Part of the decline was due to the timing of Easter. That should be reversed this month. However, other structural factors might also be at work. Yesterday's producer prices surprised on the upside which caused some relieve. However, this relief will have to be confirmed in a CPI rebound today. April retail sales are expected to rebound (0.6% M/M) after two monthly declines. Consumption was tepid in Q1, but the Fed assumes it was temporary. We side with the Fed and even see room for an upward surprise. That said, a shortfall won't pass unnoticed. Finally, the May Michigan consumer sentiment is expected to have stabilized at 97. Earlier this week, fortunes changed in favour of the dollar, but the USD/JPY rebound ran into resistance yesterday as equities stabilized. Today's US retail sales and CPI might be a ST game changer for the dollar. We expect that the consensus will be reached, or even surpassed. Such a scenario could inspire further USD gains, as it would cement the expected Fed rate hike path. This is our preferred scenario. If so, EUR/USD might revisit the 1.0821/1.0778 support (gap). However, a negative surprise also won't pass unnoticed. Especially USD/JPY might see further profit taking in case of disappointing US data

From a technical point of view, USD/JPY broke the 112.20 resistance improving the technical picture. The rebound continues in a gradual way, but looks quite robust. Next intermediate resistance comes in at 115.51. EUR/USD extensively tested the topside of the MT range (1.0874/1.0906 area) late March. The pair finally broke above the 1.09/1.0950 resistance last week, but the break wasn't confirmed and a correction kicked in. A sustained break higher would improve the ST picture. Next resistance stands at 1.1129 (62% retracement) and at 1.1366 (correction top). A decline below 1.0821 would suggest that the dollar is regaining traction against the euro. Will today's US data be strong enough to do this Job?

EUR/USD: Will USD data be strong enough to push the pair to/below the 1.0821 support

EUR/GBP

BoE: no game-changer for sterling trading

UK eco data (production and trade balance) disappointed again, but the focus was on the BoE's policy assessment. The BoE kept a balanced approach. The BoE indicated that an earlier rate hike might be needed in case of a smooth Brexit. However, what are the chances for this scenario? The moves in sterling remained modest, but the market apparently concluded that the BoE will give slightly more weight to supporting growth rather than fighting inflation. The vote was again 7-1 for an unchanged decision. There was no additional support for a rate hike, what some apparently expected. Sterling lost moderate ground after the decision. EUR/USD closed the session at 0.8428 (from 0.8400). Cable drifted further away from 1.30 resistance and closed the session at 1.2886.

There are no eco data in the UK today. The focus will be on the global market reaction to the US data. A further technical correction/rejected test of the GBP/USD 1.30 area might be slightly negative for sterling overall. Yesterday's BoE meeting was no game changer for sterling trading. The BoE remains in wait-andsee modus. For now, there is no trigger available to push EUR/GBP out of the established consolidation pattern.

EUR/GBP is locked in a ST sideways range (0.83/0.85) after a substantial decline in March/April. The pair came within reach of key 0.8305 support (Dec low), but no real test occurred. After a late April EUR/GBP rebound, the range bottom looks better protected. Longer term, Brexit-complications remain potentially negative for sterling. On technical considerations, we slightly prefer a EUR/GBP buy-ondips approach.

EUR/GBP: sterling declines slightly after BoE, but the policy statement was no game changer for sterling trading

Market Update – Asian Session: China Achieves Trade Deal With US After Trump-Xi Talks

Asia Mid-Session Market Update: China achieves trade deal with US after Trump-Xi talks; Investors await key US Retail Sales and CPI reports

US Session Highlights

(US) Fed’s Dudley (voter, dove): Trade protectionism is a dead-end and destructive to US economy; would hurt US exporters, productivity and workers - comments from India

OPEC Apr Monthly Report: Maintains 2017 global oil demand growth at 1.27M bpd; raises 2017 Non-OPEC oil supply growth from 580K bpd to 950K bpd

(US) INITIAL JOBLESS CLAIMS: 236K V 245KE; CONTINUING CLAIMS: 1.92M V 1.98ME

(US) APR IMPORT PRICE INDEX M/M: 0.5% V 0.1%E; Y/Y: 4.1% V 3.6%E; Ex-Food&Energy M/M: 0.4% v 0.2%e; Y/Y: 1.9% v 1.6%e

(US) APR PPI FINAL DEMAND M/M: 0.5% V 0.2%E; Y/Y: 2.5% V 2.2%E

Stocks felt the weight of drops in sales from two of the nation's largest retailers, Macy's and Kohl's. Concerns that consumers were staying away from stores sparked fears the lack of spending may spread to other industries. Financials and consumer discretionary were the laggards on the day, down 0.6% and 0.5% respectively.

US markets on close: Dow -0.1%, S&P500 -0.2%, Nasdaq -0.2%

Best Sector in S&P500: Consumer Staples

Worst Sector in S&P500: Consumer Discretionary

Biggest gainers: NVDA +4.3%; TXT +3.6%; MYL +3.2%

Biggest losers: M -17.0%; FTR -9.1%; KSS -7.8%

At the close: VIX 10.6 (+0.4pts); Treasuries: 2-yr 1.34% (-2bps), 10-yr 2.40% (-1bps), 30-yr 3.03% (-1bps)

US movers afterhours

TTD Reports Q1 $0.11 v $0.01e, R$53.4M v $43.4Me; Guides Q2 R$67M v $59.2Me, adj EBITDA 14.5M; +22.1% afterhours

JWN Reports Q1 $0.37 v $0.27e, R$3.28B v $3.36Be; Affirms FY17 guidance; -4.1% afterhours

VJET Reports Q1 -€0.65 v -€0.84 y/y, Rev €4.5M v €4.9M y/y; Affirms FY17 Gross margin above 40%, EBITDA "neutral to positive", and CAPEX €8-9M; -6.3% afterhours

CYBR Reports Q1 $0.28 v $0.23e, R$59M v $57.8Me; Cuts FY17 $1.18-1.22 v $1.23e; -6.4% afterhours

DAR Reports Q1 $0.04 v $0.07e, R$880.1M v $848Me; -9.1% afterhours

Key economic data

(JP) JAPAN APR M2 MONEY STOCK Y/Y: 4.3% V 4.3%E; M3 MONEY STOCK Y/Y: 3.6% V 3.6%E

(NZ) NEW ZEALAND APR BUSINESS MANUFACTURING PMI: 56.8 V 58.0 PRIOR; First sequential decline in 3 months

(NZ) New Zealand REINZ April House Sales Y/Y: -31% v -10.7% prior; -32% m/m

Asia Session Notable Observations, Speakers and Press

Asian indices mixed going into critical US CPI and Retail Sales data on Friday that could make or break the case for anticipated June Fed hike as US central bank grapples with "transitory" Q1 soft patch and better labor data last month. Political turbulence that followed yesterday's firing of FBI chief may take a back seat to news of a US-China trade agreement set to expand rade in beef/chicken and also boost access for financial firms. This could further reduce the anxiety over US-China trade war and serve as evidence of a fruitful Trump-Xi bilateral round of talks. China MOFCOM vice min also said the 2 sides will discuss the framework of 1-year economic cooperation plan with US.

Regionally, PBOC confirmed CNY459B MLF operation while also skipping daily OMO. Yuan fix was firmer for 2nd straight day and by a more sizeable margin. FX majors remained in narrow ranges.

China

(CN) China Vice Commerce Min Yu Jianhua: To discuss a 1-year economic cooperation plan with US; Looking to strengthen bilateral economic cooperation and hold further talks this summer - press

(CN) China Apr vehicle sales 2.1M units, -2.2% y/y v +4.0% in Mar; Biggest decline since Aug 2015 - China Association of Automobile Manufacturers (CAAM)

(CN) China Banking Regulator (CBRC) notes risks related to China banks' support to Belt and Road projects - Chinese press

(CN) US and China reportedly have reached broad agreement on expanding some US exports, including liquefied natural gas - press

Japan

(JP) BOJ exec director Amamiya : Reiterates it is too early to consider ways to withdraw monetary stimulus - press

Australia/New Zealand

(AU) Moody’s: Australia budget supports fiscal strength, but deficit likely wider than gov’t expects

Asian Equity Indices/Futures (01:00ET)

Nikkei -0.6%, Hang Seng +0.1%, Shanghai Composite +0.4%, ASX200 -0.8%, Kospi -0.5%

Equity Futures: S&P500 -0.1%; Nasdaq -0.2%, Dax -0.1%, FTSE100 -0.1%

FX ranges/Commodities/Fixed Income (01:00ET)

EUR 1.0860-1.0875; JPY 113.65-113.95; AUD 0.7370-0.7390; NZD 0.6825-0.6850

June Gold +0.2% at 1,227/oz; June Crude Oil +0.2% at $47.90/brl; July Copper +0.2% at $2.51/lb

(CN) PBOC SETS YUAN MID POINT AT 6.8948 V 6.9051 PRIOR; 2nd straight firmer setting; Biggest margin of strength in the fix since Apr 24th

(CN) PBoC: Confirms CNY459B MLF operation; Offers 6-month MLF at 3.05%; Offers 1-year MLF at 3.2%

(AU) Australia MoF (AOFM) sells A$800M in 3.25% 20 Bonds; avg yield: 2.8033%; bid-to-cover: 3.15x

(NZ) New Zealand sells NZ$100M in 2.50% 2035 inflation indexed bonds; bid to cover 4.71x

Asia equities notable movers

Australia

A2Milk (A2M) -4.9%; CEO share sale

Japan

Nissan (7201) +3.0%; FY result

Panasonic (6752) -2.2%; FY result

Sharp (6753) +3.0%; May apply for TSE 1 tier

Toshiba (6502) -1.8%; Chip unit sale may be delayed

Hong Kong

Hua Hong Semi (1347) +4.4%; Q1 result

Rusal (486) +4.0%; Q1 result