Sample Category Title

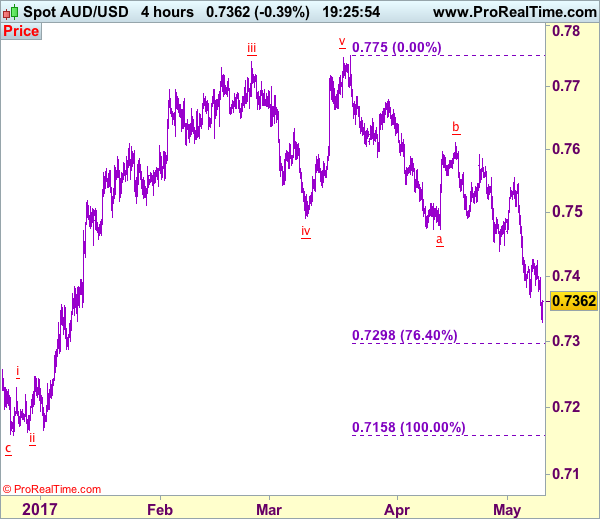

Trade Idea: AUD/USD – Buy at 0.7300

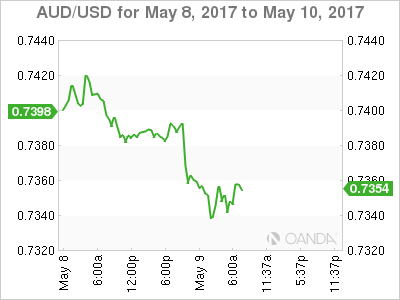

AUD/USD – 0.7354

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term down

Original strategy :

Sell at 0.7470, Target: 0.7300, Stop: 0.7530

Position: -

Target: -

Stop: -

New strategy :

Buy at 0.7300, Target: 0.7500, Stop: 0.7240

Position: -

Target: -

Stop:-

Although aussie has fallen again after brief recovery and near term downside risk remains for recent decline to extend further weakness to 0.7320, loss of downward momentum should prevent sharp fall below 0.7295-00 (76.4% retracement of 0.7158-0.7750) and bring rebound later, above 0.7425-30 would bring rebound to 0.7490-00 but break of 0.7510 is needed to signal low is formed, bring test of subsequent rise towards resistance at 0.7556 which is likely to hold from here.

In view of this, we are inclined to turn long on next decline. Below 0.7245-50 would risk weakness to 0.7200-10, however, reckon previous support 0.7158 would contain downside and aussie may stage another strong rebound from there later this week.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

Focus Switches To Central Banks As Political Risk Fades

- Odds on June Fed rate hike hits 88% as USD rebounds;

- European yields rise as traders anticipate tightening message from ECB next month;

- Commodity bounce aids equities rise but Gold remains under pressure.

As the dust continues to settle on the French election result, it seems calm has returned to financial markets with Monday’s brief relief rally coming to an abrupt halt before attention shifted straight back to the upcoming movements from central banks.

With the eurozone political distraction now seemingly being put to one side, it would appear that traders are once again focused on the upcoming central bank meetings with June being seen as a big month for both the Fed and the ECB. The US dollar is rising for a second day today, having fallen to its lowest level since November prior to this. Traders appear increasingly confident about the prospect of a second rate hike this year in June, with it now 88% priced in according to implied odds from Fed Funds futures rates. A third this year is also more than 60% priced in.

It seems that the passing of the French election has also switched the conversation back to the ECB, with traders anticipating that the central bank will put in place for further reductions in bond buying and possible rate increases by the end of the year. We could get some hint of this in June and with 10-year yields on the rise in European bond markets again today, we may already be starting to see this being priced in.

Having rallied into the French second round result, EURUSD is trading in the red for a second day after failing to hold above 1.10 – an important resistance level for the pair. With the pair having broken below 1.09 today, further downside could be on the cards, with 1.0850 being an important level below.

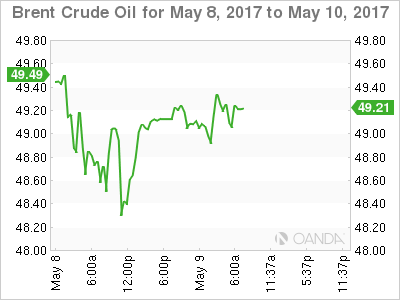

Equity markets are being supported today, partly by improved risk appetite but more broadly by the bounce in commodity markets. Oil is trading slightly higher today having pared substantial losses over the last couple of days. Still, it continues to hold below a prior support zone, with $50 in Brent and $47.50 in WTI now being notable levels to the upside.

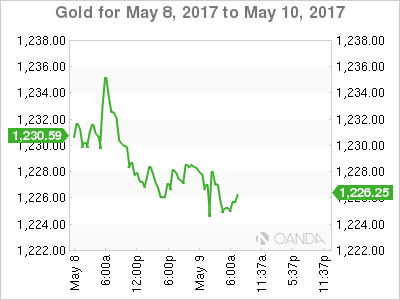

Gold on the other hand continues to trade in the red today, with stronger dollar, improved risk sentiment and reduction in political risk all weighing on the yellow metal. There’s been a notable inverse correlation with the euro over the last few weeks, highlighting the link between political risk and its safe haven appeal but with the election now behind us, that link may start to weaken. With the dollar showing positive signs, Gold may remain under pressure, with $1,220 below being the next notable support level.

Markets Revert To Normalized Risk Tolerance

Euro geo-political risks have abated somewhat, at leas until next month's French Parliamentary elections, now that Emmanuel Macron handily won the French Presidential election over the weekend. Long euro asset profit taking has been the order of the day over the past 36-hours.

For the time being, for investors and dealers, they now have to revert back to basic fundamentals and focus again on the possibility of rate differentials widening, similar to 'old' school FX.

Overnight, global equity markets were mixed, with Asian shares slipping after a rally to a two-year high while European stocks were bolstered by corporate earnings. The 'mighty' U.S dollar has found some traction, while crude oil reversed some of its losses, but remains in trouble.

1. Global equities mixed results

Asian stocks were largely quiet in the overnight session after strong gains yesterday.

In Japan, the Nikkei eased -0.1% after Monday's +2.3% jump to a 17-month high. If signs of a Fed June rate hike increase many dollar 'bulls' now see Yen under performing towards ¥115.00 region, which could see the Nikkei get to 20,500. The broader Topix fell -0.3% after closing at the highest since December 2015 in the previous session.

In Hong Kong, the Hang Seng index rose +0.2%, as China fell further after yesterday's slide. The Shanghai Composite pared early losses to recently to close -0.3% lower on the session.

In China, stocks fluctuated after erasing more than -$500B from equity values amid a crackdown on financial leverage.

Markets in Korea are closed as voters there elect a new president. The Kospi hit a record high Monday while jumping +2.3%, the biggest daily gain in 20-months.

Down-under, the Aussie S&P/ASX 200 Index dropped -0.5%, hurt mostly by financials on rumours that the Government set to impose a +A$6B levy on lenders in today's budget.

In Europe, equities trade higher across the board, with financials leading the way on the Eurostoxx. Energy shares on the FTSE 100 are under pressure on news that the Conservative Party has pledged to cap energy tariffs.

U.S equities are set to open a tad higher (+0.1%).

Note: The VIX (volatility index) has tumbled to its lowest level in 24-years. it fell -8% to +9.77% Monday

Indices: Stoxx50 +0.5% at 3661, FTSE +0.4% at 7331, DAX +0.5% at 12757, CAC-40 0.4% at 5407, IBEX-35 0.2% at 1124, FTSE MIB +0.9% at 21616, SMI +0.4% at 9074, S&P 500 Futures +0.1%.

2. Oil gives up earlier gains as rising U.S. output, gold lower

Crude oil prices have given up earlier gains overnight, as concerns over slowing demand and a relentless rise in U.S crude output continues to undermine the impact of hopes that OPEC-led production cuts could be extended.

Brent crude futures are at +$49.33 per barrel, down from a high of +$49.60 earlier in the session and near their last close. U.S. West Texas Intermediate (WTI) crude oil futures are trading at +$46.40 per barrel, down from an intra-day high of +$46.66.

In the U.S, increase in production is coming from shale producers. Since the middle of 2016, U.S. crude production has risen by over +10% to +9.3m bpd, which is close to the output of top producers Russia and Saudi Arabia.

Note: The energy market is also eyeing the concerns of China's growth as both imports and exports have slowed.

A decision on whether to continue OPEC and non-OPEC member production cuts is expected at the next official meeting on May 25 in Vienna.

Ahead of the U.S open, gold prices have hit their lowest price in nearly two-months as safe-haven demand diminished on easing political worries after the weekend's France's Presidential election. Spot gold is steady at +$1,226.13 per ounce, after touching +$1,223.34, its lowest since mid-March.

3. Fixed income yields slow march higher

Global yields have trended upward in recent weeks, as alarming geopolitical headlines fade into the background and investors increasingly focus on the potential for the Fed to raise interest rates at their meeting next month. The odds of that happening are currently trading at +80%.

The yields on 10-year Treasury notes are little changed at +2.39%, after climbing +4 bps in yesterday's session. Down-under, yields on Aussie debt with a similar maturity have pushed back +1 bps to +2.68%, while in France, 10-year OAT's yields increased +2 bps to +0.87%.

It seems that the days of these ultra lows yields are numbered, in Germany, 10-year Bunds currently yield +0.44%. It was only 18-months ago that Bunds reached minus -0.19%.

There are a couple of central banks in the frame this week, on Wednesday May 10, the Reserve Bank of New Zealand (RBNZ) and on Thursday, the Bank of England (BoE) – neither are expected change monetary policy soon.

4. Dollar shines brightly

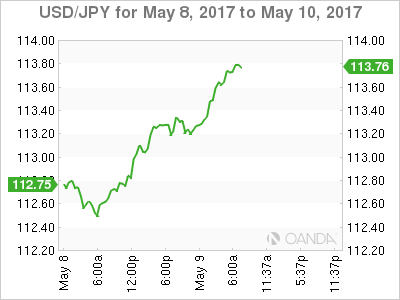

The dollar has gained broadly in the overnight session, rising to an eight-week high against the low-yielding yen of ¥113.69, while the EUR and the pound stay below key resistance levels of €1.1000 and $1.3000, respectively.

The “mighty' dollar continues to derive some support from higher U.S. yields, both nominal and real. Falling commodity prices are also providing support to the greenback, especially against commodity-linked and emerging market currencies.

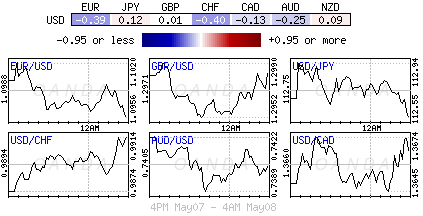

The EUR/USD trades down -0.1% at €1.0919, while the AUD/USD drops to a four-month low A$0.7347 pressured by a dismal retail sales print overnight (see below).

The pound as been given some support by a strong BRC retail sales survey (British Retail Consortium) overnight, but trades only slightly higher outright, up +0.1% at £1.2952.

5. Blame the weather: Aussie retail sales disappoints

Data overnight showed that Australian retail sales unexpectedly fell -0.1% in March. The market had anticipated a +0.3% rise. The disappointing data may suggest that the Aussie economy is facing headwinds from a weak job market and slack wage growth.

Digging deeper, the demand for food retail and household goods contributed to the monthly fall. The March data contribute to Q1 retail sales rising just +0.1%, below the +0.5% growth expected.

Blame it on the weather – a number of analysts are blaming Cyclone Debbie for the disappointing retail sales headline. Cyclone Debbie damped spending significantly. Sales in Queensland, which bore the brunt of the cyclone, fell by -1.3%. In contrast, sales across the rest of Australia rose by +0.2%.

CAC Unchanged, Markets Eye French Budget Deficit

The CAC is unchanged in the Tuesday session, as the index is trading at 5,399.00. It’s a quiet day on the release front, with no major eurozone of French releases on the schedule. France will release the budget deficit, which is expected to climb to EUR 29.6 billion in March. German Industrial Production declined 0.4%, better than the forecast of -0.6%. On Wednesday, ECB President Mario Draghi will speak about monetary policy at the Dutch House of Representatives.

With the French presidential election now behind us, it’s business as usual for European stock markets. The markets had priced in a decisive Macron win, and perhaps the only surprise is that Emmanuel Macron’s margin of victory for was larger than expected. Throughout the second round of the election campaign, opinion polls showed Macron with a comfortable 20-point edge, and in the end, he beat expectations, beating Marie Le Pen by a margin of 64% to 36%. Although Macron scored a convincing win, fully one third of French voters either abstained or voted a blank ballot as a protest vote. This means that Macron was viewed by many voters as a default choice, as he was seen as more palatable than Le Pen, head of the extremist right-wing party National Front. Macron won’t have much time to bask in the sunlight of victory, with parliamentary elections slated for mid-June. Macron’s En Marche! party is barely a year old and is unlikely to win a majority, which would mean a power-sharing setup in parliament, likely between Macron’s party and the center-right. One important factor in the presidential election was that in both rounds, opinion polls were surprisingly accurate – the concern that many voters would vote Le Pen but wouldn’t admit it to the pollsters did not occur. (In the US election, a sizeable numbers of Trump voters were embarrassed to admit so before the vote, thus skewing opinion polls in favor of Hillary Clinton.) Similar to the presidential election, the parliamentary election is full of uncertainty, and opinion polls during the election campaign will be important as fundamental releases and should be treated as market-movers.

With the US posting solid employment numbers in March, we’re likely to see the Federal Reserve press the rate trigger at the June meeting. Nonfarm Payrolls improved to 211 thousand, easily beating the forecast of 194 thousand. The unemployment rate fell to an impressive 4.4%, compared to the estimate of 4.6%. This was the lowest rate since May 2007. Wage growth remained weak at 0.3%, but still matched the forecast. Still, with such little slack in the labor markets, we should see wage growth start to move higher. If that happens sooner rather than later, the Fed will have to weigh raising rates three more times in 2017. As things stand now, two more moves is the likely scenario. The strong job numbers have cemented a rate hike in June, as the odds of a June hike continue to rise and are currently at 87%, according to the CME Group.

GOLD Consolidating Below $1230, SILVER Weakening Towards $16.00, CRUDE OIL Consolidating.

GOLD Consolidating below $1230.

Gold continues its decline after the yellow metal has faded near the hourly resistance at 1295 (18/04/2017 high). Hourly support is now located at 1195 (10/03/2017 low). The road is wide-open for further decline.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Weakening towards $16.00.

Silver's bearish pressures are still lively. Strong support is given at 15.63 (20/12/2017 low). Closest support is given at 16.20 (04/05/2017 low). Key resistance is given at a distance at 19.00 (09/11/2017 high). Expected to see continued bearish pressures until at least $16.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Consolidating.

Crude oil is bouncing back on short-squeeze move. The commodity has reached a level below $44. Strong support is given at 42.20 (14/11/2017 low). Expected to see renewed bearish pressures.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

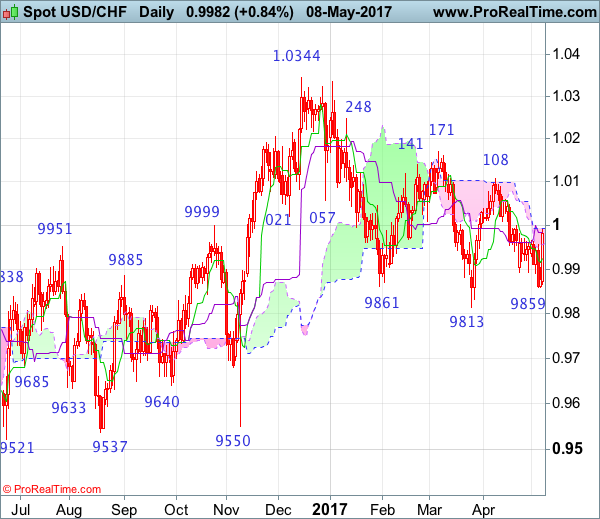

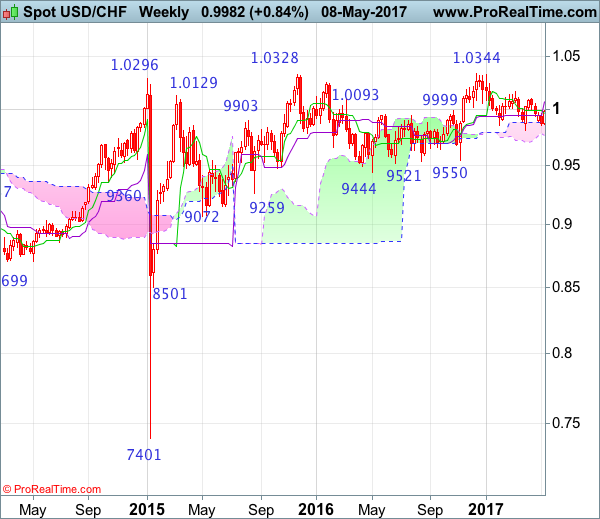

USD/CHF Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 7 Mar 2017

• Trend bias: Sideways

Daily

• Last Candlesticks pattern: Morning star

• Time of formation: 9 May 2017

• Trend bias: Near term up

USD/CHF – 1.0009

Although the greenback fell to as low as 0.9859 late last week, the pair continued finding support there and has staged a strong rebound yesterday (formed a long white candlestick), suggesting a potential bullish reversal pattern (morning star) was formed, hence consolidation with upside bias is seen for test of 1.0067 resistance, however, a daily close above there is needed to signal the fall from 1.0108 has ended at 0.9859, bring retest of this level later. Looking ahead, only above there would signal early rise from 0.9813 (Mar low) is underway for headway to 1.0150 but resistance at 1.0171 should remain intact.

On the downside, whilst initial pullback to the Kijun-Sen (now at 0.9984) cannot be ruled out, reckon the Tenkan-Sen (now at 0.9941) would limit downside and bring another rise later. Below 0.9900-05 would risk another test of said support at 0.9859 but break there is needed to revive bearishness and extend the fall from 1.0108 to previous support at 0.9813. Looking ahead, only a drop below this support would indicate the decline from 1.0344 top has resumed instead and extend further fall to 0.9735-40 (76.4% retracement of 0.9550-1.0344) and later towards 0.9700 but reckon 0.9650-60 would hold.

Recommendation: Buy again at 0.9970 for 1.0170 with stop below 0.9870.

On the weekly chart, as the greenback found good support at 0.9859 last week and has rebounded strongly this week, suggesting the retreat from 1.0108 has possibly ended there and consolidation with upside bias is seen for gain to 1.0067, however, break of said resistance at 1.0108 is needed to retain bullishness and signal the rise from 0.9813 low has resumed for test of previous resistance at 1.0171. Looking ahead, a weekly close above there is needed to signal the fall from 1.0344 (Dec high) has ended, bring further rise to 1.0248, a sustained breach above this key level would signal early upmove has possibly resumed, bring test of 1.0335-44 resistance area, above there would provide confirmation and headway to 1.0400-10 and later 1.0500 would follow.

On the downside, although pullback to 0.9970 cannot be ruled out, reckon downside would be limited to 0.9900-10 and bring another rebound later. Below said support at 0.9859 would bring test of strong support at 0.9813 but only break of this level would abort and signal the erratic fall from 1.0344 top is still in progress, bring further decline for retracement of early upmove to 0.9735-40, then 0.9700 but reckon downside would be limited to 0.9640-50 and price should stay well above support at 0.9550.

EUR/JPY Ready For Another Leg Higher, EUR/GBP Moving Lower, EUR/CHF Strong Bullish Pressures.

EUR/JPY Ready for another leg higher.

EUR/JPY's buying pressures are there. Strong resistance standing at 124.10 (15/12/2016 low) has been broken. Major support is given at 114.90 (18/04/2017low). Expected to see further renewed buying pressures towards 125.00.

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Moving lower.

EUR/GBP is trading lower. The technical structure remains negative as long as the resistance at 0.8530 (25/04/2017 low) holds. Expected to show continued weakness until support given at 0.8304 (05/12/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

EUR/CHF Strong bullish pressures.

EUR/CHF's volatility is getting stronger and is now targeting resistance given at 1.0898 (08/12/2017 high). Despite the sharp increase and the recent bullish breakout which is very likely psychological, we believe that the medium-term pattern suggests us to see at some point renewed bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low).

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

USD/CHF Short-Term Bounce, USD/CAD Renewed Bullish Pressures, AUD/USD Wide-Open For Further Decline.

USD/CHF Short-term bounce.

USD/CHF is pushing higher. The technical structure has invalidated the short-term negative momentum. Hourly resistance is given at 1.0107 (10/04/2017 high).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Renewed bullish pressures.

USD/CAD has declined after failing to reach 1.3800 before bouncing back. Hourly support can be found at 1.3411 (24/04/2017 high) then 1.3353 (20/01/2017 high). Expected to show renewed bullish pressures as long as the pair remains above 1.3530 (27/04/2017 low).

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Wide-open for further decline.

AUD/USD is trading below 0.7500. As long as prices remain below the resistance at 0.7608 (17/04/2017 high), the short-term technical structure is negative. Key resistance stands at 0.7681 (30/03/2017 high). Expected to show further weakness.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Profit-Taking, GBP/USD Pushing Higher Towards 1.3000, USD/JPY Strengthening.

EUR/USD Profit-taking.

EUR/USD is trading lower. Hourly support is given at 1.0875 (04/05/2017 low) then 1.0682 (21/04/2017 base). Stronger support can be found at 1.0494 (22/02/2017 low). Expected to show another leg higher towards 1.10.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Pushing higher towards 1.3000.

GBP/USD is trading mixed. The pair is trading around former hourly resistance given at 1.2966 (30/04/2017 high). Hourly support can be found at 1.2757 (21/04/2017 low). An unlikely break of this support would indicate further weakness. Expected to push higher.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Strengthening.

USD/JPY is pushing higher since the pair broke resistance given at 112.20 (31/03/2017 high). Hourly support can be found at 110.88 (26/04/2017 low). Stronger support is located at 108.13 (17/04/2017 low). Other key supports lie at a distant 106.04 (11/11/2016 low). Expected to show continued bullish pressures.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

Market Update – European Session: Initial Euphoria Fades A Bit Following The French Elections

Notes/Observations

Ratings agencies sound warning on Australia's AAA sovereign rating ahead of budget release

Overnight:

Asia:

BOJ Gov Kuroda reiterated Japan's virtuous economic cycle was strengthening but still saw some distance to price target. Confident it be would reached with current easing conditions

Japan Mar Labor Cash Earnings Y/Y: -0.4% v +0.5%e (biggest decline since June 2015)

Australia Mar Retail sales registers its 2nd straight decline (MoM -0.1% v +0.3%e; Q/Q ex-inflation: +0.1% v 0.5%e)

Europe:

G7 Finance ministers final statement at the upcoming at May 11-13th meetings in Germany to maintain G20 forex language (**Reminder: On Mar 18th G20 Communique noted that excess FX volatility was bad for growth, affirmed commitment against competitive devaluation; omitted language on promoting free trade)

UK April BRC LFL Sales Y/Y: +5.6% v -1.0% prior (highest since Apr 2011)

Latest Survation poll sees support for ruling Conservatives at 47% and Labour at 30% ahead of next month's snap elections

Greece's creditors said to be considering linking debt relief measure to specific financial targets. MF was opposed to this and wanted unconditional debt relief

Economic Data

(NL) Netherlands Mar Manufacturing Production M/M: -0.8% v 1.9% prior; Y/Y: 4.0% v 4.8% prior, Industrial Sales Y/Y: 12.1% v 7.3% prior

(NL) Netherlands Apr CPI M/M: 0.5% v 0.3% prior; Y/Y: 1.6% v 1.1% prior

(NL) Netherlands Apr CPI EU Harmonized M/M: 0.9% v 0.6%e; Y/Y: 1.4% v 1.2%e

(CH) Swiss Apr Unemployment Rate: 3.3% v 3.3%e, Unemployment Rate (Seasonally Adj): 3.3% v 3.2%e

(DE) Germany Mar Industrial Production M/M: -0.4% v -0.7%e; Y/Y: 1.9% v 2.6%e

(DE) Germany Mar Current Account: €30.2B v €26.5Be; Trade Balance: €25.4B v €21.5Be, Exports M/M: +0.4% v +0.2%e; Imports M/M: +2/4% v +1.6%e

(FR) Bank of France Business Sentiment: 104 v 103e

(IT) Italy Mar Retail Sales M/M: 0.0% v 0.2%e v -0.3% prior; Y/Y: -0.4% v +0.7%e

Fixed Income Issuance:

(IN) India sold total INR140B vs. INR140B indicated in 3-month and 12-month Bills

(NL) Netherlands Debt Agency (DSTA) sold €2.2B in €2.0-3.0B in 0% 2022 DSL; Avg Yeild: -0.244% v -0.197% prior

(DK) Denmark sold DKK1.72 in 6-month Bills Yield: -0.673% v -0.680% prior; bid-to-cover: 1.12x v 1.67x prior

(ES) Spain Debt Agency (Tesoro) sold total €4.68B vs. €4.0-5.0B indicated rangein 6-month and 12-

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 +0.5% at 3661, FTSE +0.4% at 7331, DAX +0.5% at 12757, CAC-40 0.4% at 5407, IBEX-35 0.2% at 1124, FTSE MIB +0.9% at 21616, SMI +0.4% at 9074, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes European Equities trade higher across the board with EON, Commerzbank, K+S some of the notable risers this morning following their results. To the downside Munich Re is trading lower after missing estimates. Energy shares in the UK are under pressure as the Conservative Party pledged to cap energy tariffs, with Centrica the notable decliner lower by over 2.5%. As we approach the tail end of Earnings season in the US this mornings notable earners include AON, Valiant, QVCA, Duke Energy and Allergan

Equities

Consumer discretionary [Continental [CON.DE] -1.2% (Earnings)]

Materials: [K+S [SDF.DE] +1.7% (Earnings)]

Industrials: [Elringklinger [ZIL2.DE] +2.8% (Earnings), Fraport [FRA.DE.DE] -2.0% (Earnings)]

Financials: [Commerzbank [CBK.DE] +2.2% (Earnings), Munich Re [MUV2.DE] -1.9% (Earnings)]

Technology: [Dialog Semi [DLG.DE] -2.6% (Earnings), MicroFocus [MCRO.UK] -11.2% (Trading and transaction update), Agfa Gevaert [AGFB.BE] -9.6% (Earnings)]

Utilities: [ EON [EOAN.DE] +0.7% (Earnings)]

Energy: [Uniper [UN01.DE] +0.7% (Earnings)]

Speakers

France govt official: Incoming President Macron targets to reduce unemployment to 7.0% by 2022 (**Note: Q4 ILO Unemployment Rate came in at 10.0%)

Iceland Central Bank (Sedlabanki) Gov Gudmundsson: Can hit inflation target with lower interest rates than before. Believed that real FX rate in the country would come down. Interest rate cuts in 2016 were not targeting FX. Recent FX rate fluctuations had been mostly benign and added it was hard to maintain FX peg with free movement of capital . ECB taper would help Iceland; would welcome such a move

Currencies

EUR/USD continued to drift away from its post French election 6-month high of 1.1022. The pair hovered just above the 1.09 level throughout today's session. Dealers noted that the outcome of the upcoming French Parliamentarian election in June would determine if Macron could work with a government which believes in similar reform idea

USD/JPY was higher in Asia after Japan registered disappointing real cash earnings data. Dealers noted that BoJ yield curve management might stay in place for longer. USD/JPY pair approaching the 113.70 just ahead of the NY morning.

AUD/USD was lower by 0.5% ahead of the Treasury budget projections. Rating agencies will pay particular attention on the extent and pace of fiscal consolidation and its likely sustainability. Australia is currently rated AAA

Fixed Income

Bund futures trade at 160.19 down 27 ticks, under pressure into wave of core auction supply. A break of 159.60 support level could see lows target 159.01 followed by 157.50. Resistance lies at 160.81 level followed by 162.10.

Gilt futures trade at 127.16 lower by 33 ticks, after a strong stock open. A continuation of the pullback from the 129.14 April 18th high has price eyeing the 126.41 support level. An acceleration lower could test the 125.80 region. Resistance stands at 128.30 then 128.81 followed by 129.14.

Tuesday's liquidity report showed Monday's excess liquidity fell to €1.643T a loss of €7B from €1.650T prior. Use of the marginal lending facility dropped to €291M from €296M prior.

Corporate issuance saw over $13.3B come to market via 6 issues.

Looking Ahead

(PT) Bank of Portugal reports Apr ECB financing to Portuguese Banks: €B v €23.7B prior

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (AU) Australia FY17/18 Federal Budget

05:30 (EU) ECB allotment in 7-Day Main Refinancing Tender

05:30 (HU) Hungary Debt Agency (AKK) to sell 3-month Bills

05:30 (DE) Germany to sell 0.1% 2046 Inflation-linked bonds (Bundei)

05:30 (BE) Belgium to sell €1.8-2.2B in 3-Month and 12-Month Bills

06:00 (US) Apr NFIB Small Business Optimism: 104.0e v 104.7 prior

06:45 (US) Daily Libor Fixing

07:00 (BR) Brazil Apr FGV Inflation IGP-DI M/M: -1.0%e v -0.4% prior; Y/Y: 3.0%e v 4.4% prior

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:15 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada Mar Building Permits M/M: +2.8%e v -2.5% prior

08:30 (SI) Slovenia Debt Agency to sell 6-month and 12-month Bills

08:50 (FR) France Debt Agency (AFT) to sell combined €5.2-6.4B in 3-month, 6-month and 12-month BTF Bills

08:55 (US) Weekly Redbook Sales

09:00 (MX) Mexico Apr CPI M/M: 0.1%e v 0.6% prior; Y/Y: 5.8%e v 5.4% prior; Core M/M: 0.5%e v 0.6% prior

09:00 (EU) Weekly ECB Forex Reserves: No est v €280.1B prior

09:00 (US) Fed's Kashkari (Voter, dove)

09:00 (RU) Russia announces weekly OFZ bond auction

10:00 (US) Mar JOLTS Job Openings: 5.73Me v 5.743M prior

10:00 (US) Mar Wholesale Inventories (Final) M/M: -0.1%e v -0.1% prelim; Wholesale Trade Sales M/M: No est v 0.6% prior

11:30 (US) Treasury to sell 4-Week Bills

12:00 (US) DOE Short-Term Crude Outlook

12:00 (DE) German Fin Min Schaeuble at event in Berlin

13:00 (US) Treasury to sell 3-Year Notes

13:00 (US) Fed's Rosengren (non-voter) at NYU on risk management

16:15 (US) Fed's Kaplan (Voter) in Dallas

16:30 (US) Weekly API Oil Inventories