Sample Category Title

GOLD – Risk Remains Lower On Further Declines

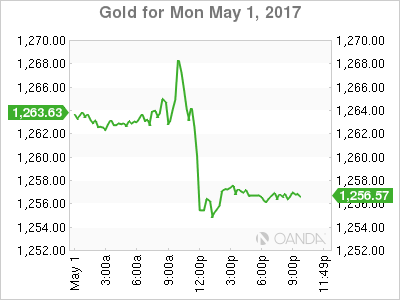

GOLD - The commodity continues to hold on to its downside pressure as it looks for more correction. On the downside, support comes in at the 1,260.00 level where a break will turn attention to the 1,250.00 level. Further down, a cut through here will open the door for a move lower towards the 1,240.00 level. Below here if seen could trigger further downside pressure targeting the 1,230.00 level. Conversely, resistance resides at the 1,270.00 level where a break will aim at the 1,280.00 level. A turn above there will expose the 1,290.00 level. Further out, resistance stands at the 1,300.00 level. All in all, GOLD looks to weaken further.

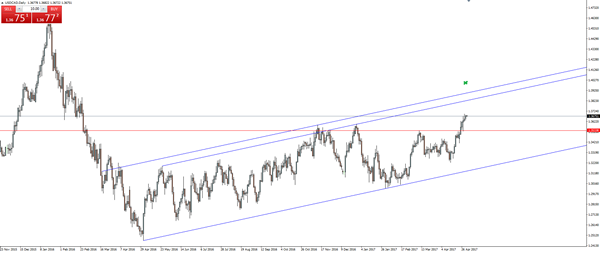

USD/CAD’s Bullish Channel With Room To Move

Good morning!

And just like that, a deal has been reached on a bill to fund the US government for the final five months of this fiscal year. An agreement that is likely to avert a government shutdown and save traders another headline driven mish-mash that we dealt with barely 12 months ago.

In holiday trade that was expected to remain fairly quiet, this deal has definitely given markets a slightly unexpected kick.

Just check out USD/CAD.

USD/CAD Daily:

I've redrawn the daily USD/CAD bullish channel from January's blog, but the direction and setup stay the same.

The subjective nature of trend lines mean that there are a few ways that you could have drawn this one. However, as usual the best way to go about drawing them is to connect the most obvious touches. Usually these are the first two that immediate jump out at you.

In a sometimes overly complicated industry such as trading, keeping it simple (stupid) really is best.

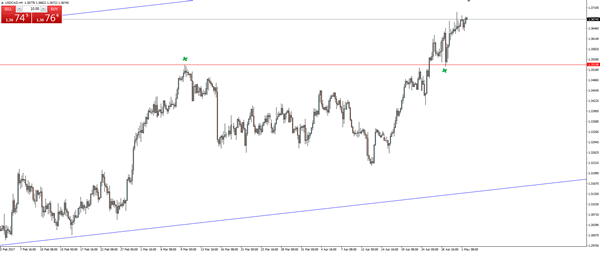

USD/CAD 4 Hourly:

Taking a step downward, into the intraday charts with the 4 hourly, you can see a nice breakout and retest of the swing high level.

With the amount of white space on the chart between the market price and the top of the bullish channel, could we be in for a further upward move?

Sleepy Markets But About To Get Interesting

Sleepy markets but about to get interesting

It was a quiet session overnight, as both Asia and London were on holiday and New York was unable to muster any steam. Despite the slow start, this week's diary picks up with an important RBA meeting today, FOMC mid-week followed by the granddaddy of economic data on Friday – the key US Nonfarm Payrolls report. On the Trump watch, investors took some relief that House and Senate representatives have reached a USD1.1t trillion deal to fund the government through the remainder of this fiscal year. While on the currency markets, with little fresh to gather from the overnight markets, the two main impressions were the resilience of the AUDUSD, now trading above .7500, and USDJPY now within striking distance of 112.00.

Australian Dollar

The Australian dollar is discernibly higher this morning, suggesting that pre-RBA Rate Decision flow is skewed towards a stronger response from the RBA than had been anticipated. Despite recently trapped in a downtrend due to trade and commodity factors, last week's slight CPI miss and recent employment data are supporting the view the RBA will lean more towards the next move a rate hike than a rate cut. For this week at least, it appears domestic factors are trumping external factors for the Aussie dollar.

Later in the week, the Federal Reserve Board are unlikely to alter policy, but with the string of subpar economic data, the urgency for increasing interest rates has lessened somewhat, so the market does view a play on the tale of the two central bank themes. But for June US rate hike probabilities it likely comes down the firmer wages component of the NFP data which should get the dollar bulls excited.

Japanese Yen

Despite weaker US economic data overnight, the market is still in risk catch up mode with the French election uncertainty all but diminished. Also, the US funding extension will keep market expectations high, so that we could see a deal on Obamacare, which could make a path for Tax Reform.

The BOJ minutes indicated little new, and while currency concerns are not within the BOJ's overall purview, the Yen's near to medium term tangent to be determined by interest rate differentials., the BOJ was cautious to avoid any language that could be misconstrued as an adjustment toward tapering or monetary easing. Members agreed that inflation lacks strength, but the economy continued to recover moderately.

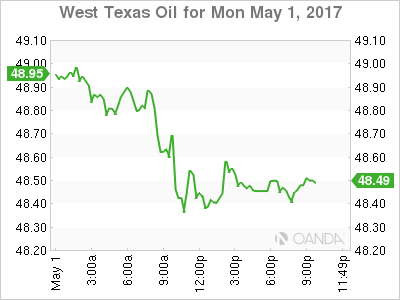

WTI

Oil prices declined overnight, hobbled by a report of high Libya oil production and from fallout from Friday's Baker Hughes report of another increase in drilling rigs. Supply concerns continue to weigh negatively.

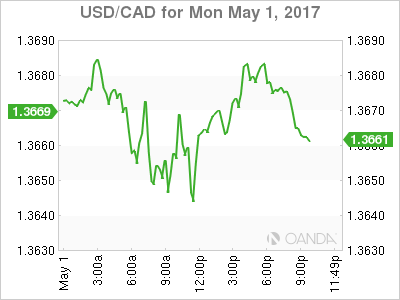

USD/CAD Canadian Dollar Stable On May Day Trading Session

The Canadian dollar continues trading at 1.3666 (14 month low) on a low volume trading session due to the May Day holiday. The price of oil is keeping the loonie lower against the greenback despite a solid performance from the Canadian manufacturing sector. The manufacturing purchasing Managers Index (PMI) reported on Monday is the highest in six years (55.9) a gain from last month’s 55.5.

US data on Monday was mostly negative. The US manufacturing PMI disappointed with a 54.8 level below the forecast of 56.6. Construction spending contracted by 0.2 percent in March. Despite the optimistic comments from US Treasury Secretary Steven Mnuchin about the economy, the USD was mixed as U.S. President Donald Trump issued comments on financial regulations that spooked the markets.

Soon after Canadian authorities in Ontario passed a 15 percent tax on housing by foreign buyers the news hit that Home Capital Group, the largest non-bank mortgage lender asked of for a $2 million Canadian dollar line of credit to offset the exiting of saving account deposits. The company will report first quarter results later this week.

The USD/CAD gained 0.1 percent in the last 24 hours. The currency is trading on a thin volume trading day due to the May holiday in some major markets. The US economy posted a disappointing 0.7 percent GDP growth in the first quarter. The forecast called for a 1.3 percent reading which was already pointing to a slowdown form the last quarter of 2016. This morning the Institute for Supply Management published the US purchasing managers index (PMI) at a 54.8 reading. It was a miss on the expectations of 56.6. A reading above 50 is considering an expansion, but there is no denying that the economic health of the United States has slowed as per the views of purchasing managers.

West Texas lost 1.05 percent at the beginning of the week. The price of WTI is $48.38 as US shale drillers add more oil rigs driving supply up despite the efforts of the Organization of the Petroleum Exporting Countries (OPEC) deal to reduce production with members and other major producers. The official manufacturing PMI from China released over the weekend pointed to a slower than expected growth which will put downward pressure in commodities.

The OPEC and other producers will meet on May 25 to discuss an extension to the production cut agreement. The deal was almost a year in the making as members were at odds on who was expected to participate.

Gold lost 0.962 percent in the last 24 hours. The precious metal is trading at $1,256 after a deal reached by the White House will avoid a government shutdown. The news drove down the price from the daily high of $1,271 to the current price level. There has been movement to the upside as Donald Trump has issued some comments on the regulation of Big Banks which caused anxiety in the stock market.

The metal is range bound ahead of the two-day Federal Open Market Committee (FOMC) meeting that is not expected to end in a rate hike announcement on Wednesday morning. Gold has been bid as a safe haven during turbulent times but as the Fed signals a stronger willingness to raise interest rates it will put downward pressure on the yellow metal. Softer US economic data has kept optimism in check ahead of the central bank’s statement.

Market events to watch this week:

Tuesday, May 2

12:30am AUD Cash Rate

AUD RBA Rate Statement

4:30am GBP Manufacturing PMI

6:45pm NZD Employment Change q/q

Wednesday, May 3

4:30am GBP Construction PMI

8:15am USD ADP Non-Farm Employment Change

10:00am USD ISM Non-Manufacturing PMI

10:30am USD Crude Oil Inventories

2:00pm USD FOMC Statement

USD Federal Funds Rate

9:30pm AUD Trade Balance

11:10pm AUD RBA Gov Lowe Speaks

Thursday, May 4

4:30am GBP Services PMI

8:30am CAD Trade Balance

USD Unemployment Claims

4:25pm CAD BOC Gov Poloz Speaks

9:30pm AUD RBA Monetary Policy Statement

11:00pm NZD Inflation Expectations q/q

Friday. May 5

8:30am CAD Employment Change

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change

The Great Catch-Down

The ISM manufacturing index on Monday was another sign that soft US economic data is catching down to consistently mediocre hard data. The New Zealand dollar was the top performer on the day while the pound lagged. The RBA decision is next. The Premium video on the existing and future trades will be released ahead of the Tuesday European session.

The April ISM manufacturing index slid to 54.8 compared to 56.5 expected. It's another sentiment survey that's fading after an early-year climb on election optimism. At the same time, hard data continues to show a middling economy. Personal spending was flat in March, missing the +0.2% consensus.

Given the lack of progress on substantive legislation or stimulus in the US, the arc of the sentiment numbers isn't a surprise. The moderation is likely to continue until the administration proves it can turn its rhetoric into action.

Another factor is that the uncertainty on taxes could be encouraging firms to hold off on investments until they have a better idea of the landscape. So even if tax reform comes later this year, it may result in a drag until then.

For all the negative data Monday, the US dollar proved to be resilient. A 30 pip fall in USD/JPY was erased later in the day. That's in part because of rising bond yields after the Treasury said it would increase borrowing.

Up next, we look to the Caixin China manufacturing index at 0145 GMT. The risks are skewed towards a lower number after the decline in the data released on the weekend.

The main event comes at 0430 GMT with the RBA decision. No change from the 1.50% rate is expected and the central bank could moderate its tone given the recent correction in iron ore prices. But for the most part it will be a wait-and-see type statement.

Gold Drops as Congress Avoids Federal Shutdown

Gold has posted losses in the Monday session. In North American trade, spot gold is trading at $1254.88 an ounce. On the release front, US numbers started the week on a soft note. ISM Manufacturing PMI dropped to 54.8, short of the estimate of 56.6 points. This marked a 4-month low. US Personal Spending dipped to 0.0%, shy of the forecast of 0.2%. US Treasury Secretary Steven Mnuchin will deliver remarks at the Milken Conference in Los Angeles.

The US economy appears to have hit some turbulence, as underscored by a disappointing Advance GDP for the first quarter. The economy expanded at just 0.7%, well below the forecast of 1.3%. Consumer indicators have also been softer than expected. On Friday, Revised UoM Consumer Sentiment came in at 97.0, short of the estimate of 98.1 points. This echoed the CB Consumer Confidence report earlier in the week, which also missed expectations. Consumer spending is also raising concerns, and Personal Spending dipped to 0.0% in March, the first time the indicator hasn't posted a gain since July 2016. Key employment data, highlighted by Nonfarm Payrolls, will be released on Friday. If these indicators miss expectations, investor jitters could push gold to higher levels.

President Trump has managed to avert a partial government shutdown, as lawmakers reached an agreement on the weekend. The short-term spending deal, which has bipartisan support, provides funding for government services until September 30th. The deal does not include any funding for a border wall with Mexico, marking a clear concession on the part of President Trump. Still, after a rocky 100 days in office, Trump could ill afford the embarrassment of the federal government running out of funds so early on his watch.

ISM: Sugar High Is Wearing Off

The manufacturing ISM came in at 54.8 for April-well below expectations as the gap gets smaller between once-soaring soft economic data, like surveys, and generally weak output measures, or hard data.

Soft Serve with a Dip

Since the start of 2017, one of the top questions we get from clients has to do with the gap between hard and soft data. Our take then and now is that the euphoria reflected in the soft data overstates the health of the economy and that without big gains in productivity or labor force participation, the speed-limit for real GDP growth is just a bit faster than 2 percent.

Many purchasing manager surveys and measures of consumer and business confidence have jumped to multi-year highs since the start of this year. In the case of the NFIB's measure of small business confidence, the level reached in January was the highest in 13 years. Yet, actual hard measures like industrial production and factory orders have been weaker. Last week we learned that GDP, the most widely-followed measure of output, posted growth of just 0.7 percent at an annualized rate in the first quarter.

Today's print for the ISM of 54.8 was the third consecutive monthly decline and was lower than consensus expectations for a print of 56.5. To be clear, 54.8 is still a solid number and consistent with our outlook for gradual firming in the manufacturing sector. The multi-year high of 57.7 reached in February would be consistent with a much-stronger rate of growth than we have been forecasting, so the return to a more sustainable pace of expansion suggested in this report for April is consistent with our forecast.

The most pronounced move among the various subcomponents was the 7.0 point swing lower for orders to 57.5 from 64.5 previously. Although 57.5 is still consistent with steady growth in factory orders, the momentum shift is disconcerting-particularly after the tepid 0.2 percent monthly gain in core capital goods orders in last week's durable goods report for March.

The dip in the employment component was almost as large, as it fell 6.9 points to just 52.0. The employment index is now at its lowest level since before the election. The weakness there might suggest some downside risk for Friday's jobs report. As of this writing, our forecast of 190K net new jobs remains intact, but we'll be watching the ISM non-manufacturing report on Wednesday to see if this slower employment growth trend is also evident in the service sector.

Not All Bad News

For a report that fell well short of expectations, particularly in the key orders and employment components, it was not all bad news. The comments were almost universally positive, but perhaps more qualified than a few months ago. One respondent, for example, noted that "world/political headlines cause personal anxiety, business conditions remain solid."

To sum up, the weakening trend in soft data like the ISM is not particularly troubling and is consistent with our forecast for only modest GDP growth.

Pound Subdued in Holiday-Thinned Trade

GBP/USD is showing little movement at the start of the week. In Monday's North American session, the pair is trading at 1.2920. On the release front, British banks are closed for the May 1 holiday. In the US, ISM Manufacturing PMI dropped to 54.8, short of the estimate of 56.6 points. This marked a 4-month low. US Personal Spending dipped to 0.0%, shy of the forecast of 0.2%. US Treasury Secretary Steven Mnuchin will deliver remarks at the Milken Conference in Los Angeles. On Tuesday, the UK kicks off this week's PMIs releases with Manufacturing PMI, with an estimate of 54.0 points.

The British economy has weathered the Brexit storm better than expected, but market concerns are again rising ahead of the start of negotiations between Britain and the European Union. The EU has toughened its stance in recent weeks, and on Monday, the German media reported that a meeting last week between May and Jean Claude Juncker, President of the EU had gone very badly. Although 10 Downing Street claims the talks were 'constructive', the EU attacked May on Monday, bluntly stating that it was "more likely than not" that Brexit talks would fail in light of the May-Juncker fiasco. If the two sides remain at loggerheads, market jitters could send the pound downwards.

The US economy appears to have hit some turbulence, as underscored by a disappointing Advance GDP for the first quarter. The economy expanded at just 0.7%, well below the forecast of 1.3%. Consumer indicators have also been softer than expected. On Friday, Revised UoM Consumer Sentiment came in at 97.0, short of the estimate of 98.1 points. This echoed the CB Consumer Confidence report earlier in the week, which also missed expectations. Consumer spending is also raising concerns, and Personal Spending dipped to 0.0% in March, the first time the indicator hasn't posted a gain since July 2016. Key employment data, highlighted by Nonfarm Payrolls, will be released on Friday. If these indicators miss expectations, the US dollar could suffer broad losses.

The lights will stay on in Washington after all. Following a week of intense negotiations on Capitol Hill, Lawmakers reached an agreement which averts a partial government shutdown. The short-term spending deal, which has bipartisan support, provides funding for government services until September 30th. The deal does not include any funding for a border wall with Mexico, marking a clear concession on the part of President Trump. Still, after a rocky 100 days in office, Trump could ill afford the embarrassment of the federal government running out of funds so early on his watch.

U.S. Manufacturing Activity Loses Momentum in April

The Institute for Supply Management (ISM) manufacturing index declined by 2.4 points in April to 54.8 - weaker than the consensus expectation of a decline to 56.5 from 57.2 in March. Still, the U.S. manufacturing sector continued to expand for the eighth consecutive month.

Moves in the subcomponents of the index were mixed, with four of the ten subcomponents rising in the month. Some of the biggest moves lower included new orders (-7.0 to 57.5), employment (-6.9 to 52.0) and prices (-2.0 to 68.5). The four subcomponents that recorded an increase include inventories (+2.0 to 51.0), imports (+2.0 to 55.5), production (+1.0 to 58.6), and new export orders (+0.5 to 59.5).

As a result of the large decline in new orders and the small increase in inventories, the spread between the two - useful as a leading indicator of activity - narrowed in April to 6.5 from 15.5 in March. This suggests that manufacturing activity is likely to expand at a more gradual pace in upcoming months.

Of eighteen manufacturing industries, sixteen reported growth in April. Electrical equipment appliances and components, textile mills, and nonmetallic mineral products all registered the strongest rates of expansion in the month. The only industry reporting contraction in April was apparel, leather and allied products.

Key Implications

The softer reading on the manufacturing sector this morning suggests that growth or sentiment in the sector is coming back down to earth after peaking this past February. Although all subcomponents (with the exception of customers' inventories) remain firmly in expansionary territory, the large decline in new orders and employment will likely reduce expectations of a similar strong performance in the sector in the second quarter as was observed in the first. Still, comments by survey respondents remained broadly positive, with some citing increased prices being passed on by suppliers and price pressures firming on commodities.

Although the U.S. manufacturing sector is still expanding, it will likely continue to face a number of challenges this year. Most important is the elevated level of policy uncertainty both globally and domestically, particularly concerning any upcoming changes to the U.S. trade pact with its NAFTA partners. Given U.S. manufacturers strong integration in global value chains, any material changes to U.S. trade policies could destabilize and do more harm than good as far as domestic industries are concerned in the short to medium term. A strong dollar should also continue to dampen the export competitiveness of U.S. firms, despite attempts by the new administration to talk down its strength.

Overall, the manufacturing sector is off to a good start thus far for 2017, and its strength and resilience highlights how anomalous the first release of first quarter GDP is. The good news is that this morning's data on personal consumption expenditure suggests that consumer spending should see a lift in momentum at the start of the second quarter, albeit due to a rebound in utilities rather than the broad boost to spending that was hoped for. Still, both producer and consumer prices have lost momentum in recent months, which is likely to warrant some caution from the Federal Reserve, and if this persists it could make the path of interest rate normalization more gradual.

Real Personal Spending and Income End First Quarter Strong

Negative inflation in the last month of the quarter helped personal income and spending recover after very weak readings in the first two months of 2017. Real personal consumption increased 0.3 percent in March.

Inflation Takes the Pressure Off the U.S. Consumer in March

Higher inflation kept the U.S. consumer in check during the first two months of the quarter as real personal consumption expenditures dropped 0.3 percent and 0.1 percent. However, the easing of inflation in the third month of the year helped personal consumption expenditures (PCE) to come in positive during the quarter as we saw last week with the release of first quarter results. Personal consumption expenditures, while flat in nominal terms in March, rose 0.3 percent in real terms after accounting for inflation. The PCE deflator was down 0.2 percent during the last month of the first quarter, while the core PCE was down 0.1 percent.

Still, goods consumption was very weak in March while services consumption was strong. Durable goods consumption was down $19.6 billion, while non-durable goods consumption was down $8.7 billion. However, services consumption was very strong, increasing $34.0 billion in March and helping overall PCE during the month. Services consumption was very weak during the first two months of the quarter, increasing only $8.3 billion and $3.2 billion in January and February, respectively.

The 0.3 percent increase in real PCE was due to a 0.1 percent drop in goods consumption, which was caused by a 0.7 percent decline in durable goods consumption. Meanwhile, services consumption improved by a strong 0.4 percent after declining 0.1 percent and 0.2 percent in January and February, respectively.

Personal Income Mixed in March

Although consumption remained weak during the first quarter of the year income continued to advance. Nominal personal income increased 0.2 percent during the last month of the quarter after a 0.4 percent increase in January and a 0.3 percent increase in February. Nominal disposable personal income also increased 0.2 percent in the last month of the quarter. However, real disposable personal income surged 0.5 percent in March due to the weak inflation print for the month.

However, compensation of employees weakened considerably in March compared to the previous months. Compensation of employees increased only $8.1 billion in March, compared to an increase of $42.5 billion and $45.9 billion in January and February, respectively.

Better Times Ahead for Consumption

The March numbers may be pointing to an improvement in the second quarter of the year for the U.S. economy, especially from the consumer side. If that is the case, consumer demand will be more in tune with the improvement in consumer confidence data we have seen since the presidential election last November.