Sample Category Title

Inflation Softens in March, But Spending Volumes Rebound

Personal income rose 0.2% in March, below the median consensus forecast of 0.3%. Still, it was a good month for real income growth - controlling for inflation and removing taxes, real disposable personal income was up a robust 0.5%.

Personal spending was flat in nominal terms, below the consensus call for a 0.2% gain. In real terms, spending rose 0.3%, led by services, which rebounded 0.4% (after two months of declines). Goods consumption fell slightly (-0.1%) as gains in non-durable goods (+0.3%) were offset by declining spending on durables (-0.7%).

Consumer prices fell 0.2% in March, bringing the year-on-year inflation rate to 1.8% (from 2.1% in February). Core prices (excluding food & energy) fell 0.1% month-on-month - bringing year-on-year price growth to 1.6% (from 1.8% previously).

The personal saving rate rose to 5.9% in March from 5.7% in February.

Key Implications

The good news is that personal spending gained momentum through the soft first quarter. Still, there is little here to get excited about. The strong growth in services spending reflects a normalization in utilities consumption after two months of warm weather-induced weakness. Meanwhile, the pullback in durable spending (already telegraphed in falling auto sales) provides a high hurdle for spending growth in April and May in order to assuage fears that the slowdown is more than a first quarter blip. The saving grace is the strong gain in real incomes. As long as job growth holds up and inflation remains modest, real income growth should provide the impetus for spending growth to accelerate in the months ahead.

The weakness in inflation, especially in the core measure, has to induce some caution as far as the Federal Reserve deliberations this week. The momentum of the past few months was completely unwound in March. This is more than enough for the Fed to pause at its meeting later this week. Should it continue, it may also jeopardize plans for any additional rate hikes later in the year.

US Consumer Spending Volumes Higher in March

Highlights:

- US personal consumption expenditures (PCE) were unchanged for a second consecutive month in nominal terms in March but the volume of spending (real PCE) rose 0.3%.

- Personal incomes rose 0.2% and the monthly saving rate rose to 5.9% from 5.7% in February and up from 5.2% at the end of last year.

- PCE inflation declined 0.2% with core (ex-food and energy) prices also slipping 0.1%. The dip in the core price measure was the first decline since 2001 (led by weaker telecom services) although on a year-over-year basis, prices were still up 1.6%.

Our Take:

Nominal consumer spending was flat in March but largely due to falling prices, flagged in the earlier-released March CPI numbers. A 0.3% tick increase in spending in volume terms provides the first sign that spending is bouncing back after a weak 0.3% (annualized) increase in all of Q1 (already reported in last Friday's advance Q1 GDP report) that looks decidedly out of line with underlying strength in labour markets, rising consumer confidence, and still extremely low interest rates. Part of the Q1 disappointment was related to weak spending on utilities as warmer-than-usual temperatures reduced the need for home heating (a good thing for consumers) and the reversal as temperatures returned to normal will also support stronger spending growth in Q2. We continue to view the fundamental backdrop for consumer spending as solid, supported by ongoing improvement in labour markets (including rising wages) and the stimulative stance of monetary policy. Today's report is in line with our monitoring that consumer spending growth will bounce back to a 2.8% rate in the second quarter which, along with continued growth in business and residential investment is consistent with a 2.9% rise in GDP after the weaker-than-expected 0.7% Q1 gain.

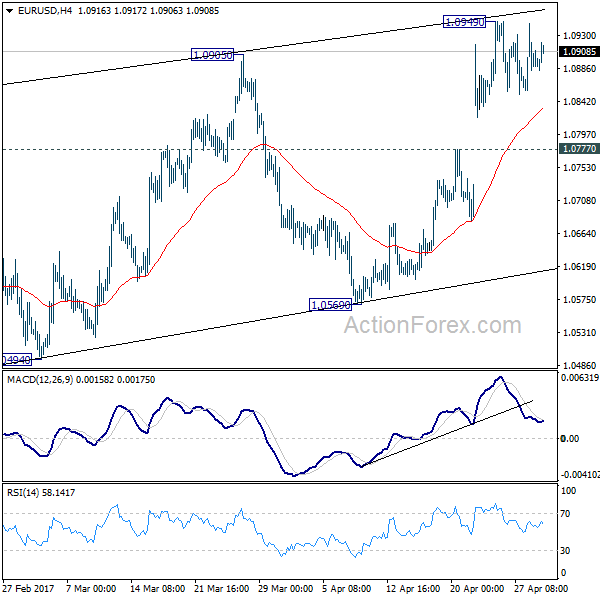

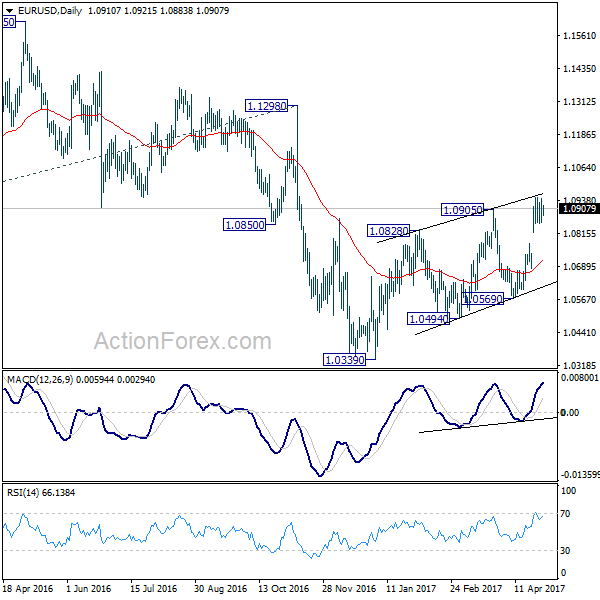

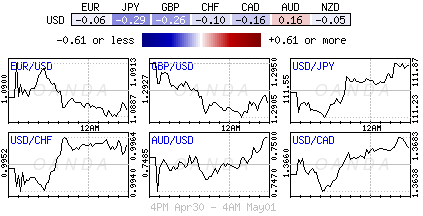

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0850; (P) 1.0898 (R1) 1.0941; More....

EUR/USD is staying in consolidation below 1.0949 temporary top and intraday bias remains neutral at this point. Another rise is expected as long as 1.0777 support holds. But still, choppy rebound from 1.0339 is seen as a correction. Hence we'd look for topping again on next rise. Meanwhile, on the downside, break of 1.0777 will turn turn bias to the downside for 1.0569 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. This would also be supported by sustained trading above 55 week EMA.

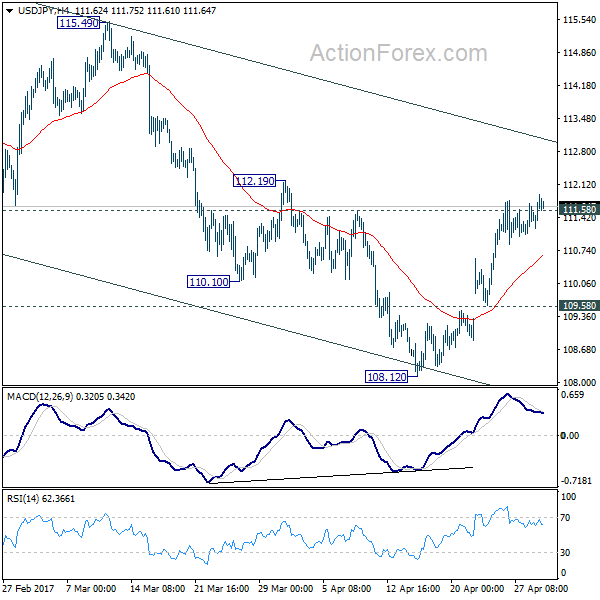

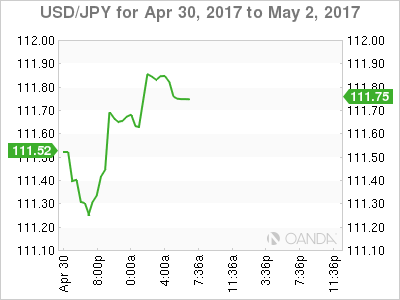

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.13; (P) 111.42; (R1) 111.79; More....

No change in USD/JPY's outlook. We're favoring the case that corrective fall from 118.65 has completed with three waves down to 108.12. Sustained break of 111.58 support turned resistance will confirm this bullish view and target 115.49 resistance and above. However, break of 109.58 will argue that fall from 118.65 is still in progress and will turn bias to the downside for 108.12 and below.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

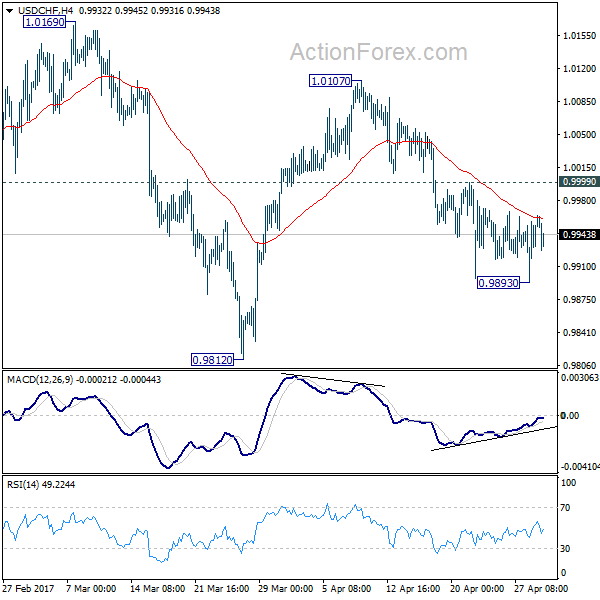

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9908; (P) 0.9932; (R1) 0.9972; More.....

USD/CHF is staying in consolidation above 0.9893 temporary low. Intraday bias stays neutral at this point. With 0.9999 minor resistance intact, deeper decline is mildly in favor. Below 0.9893 will target 0.9812 and below to extend the correction from 1.0342. But break of 0.9812 should be brief and we will look for bottoming signal below there. On the upside, above 0.9999 minor resistance argues that fall from 1.0107 is finished, with bullish convergence condition in 4 hour MACD. In that case, intraday bias will be flipped back to the upside for 1.0107 resistance first.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

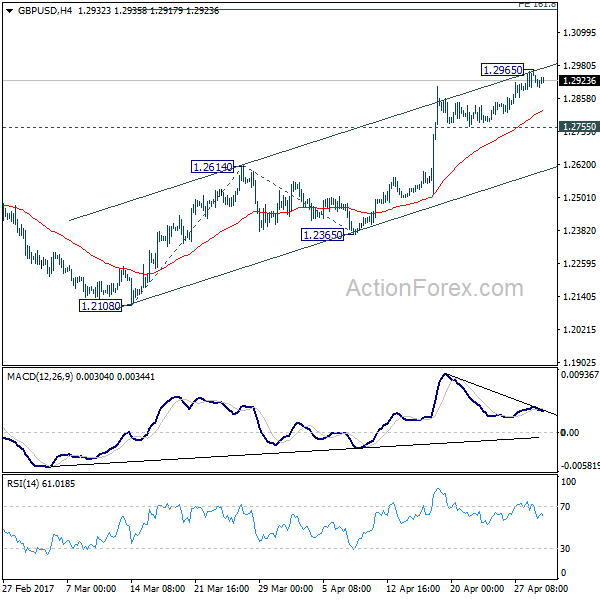

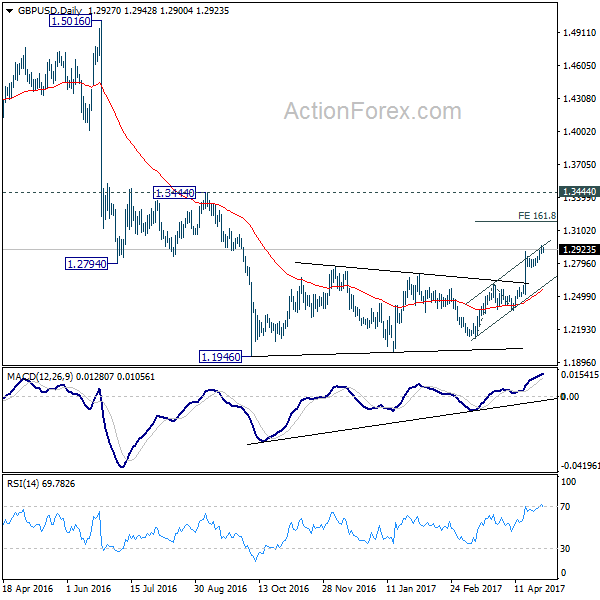

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2899; (P) 1.2932; (R1) 1.2975; More...

Intraday bias in GBP/USD remains neutral for consolidation below 1.2965 temporary top. Further rally is expected as long as 1.2755 minor support holds. Break of 1.2965 will target 161.8% projection of 1.2108 to 1.2614 from 1.2365 at 1.3184. At this point, price actions from 1.1946 are still interpreted as a correction pattern. Therefore, we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2755 minor support will turn bias to the downside. Further break of 1.2614 resistance turned support will now indicate near term reversal.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Dollar Trades Mixed after as Inflation Slowed, Traders Calm ahead of Key Events

Dollar turns mixed in early US session after weaker than expected economic data. Personal income rose 0.2% in March versus consensus of 0.3%. Personal spending rose 0.0% versus consensus of 0.2%. Headline CPI slowed to 1.8% yoy, down from 2.1% yoy. Core PCE slowed to 1.6% yoy down from 1.8% yoy. Dollar traders will look into the string of key events this week for guidance. Fed is widely expected to keep policies unchanged on Wednesday. But at this point, Fed fund futures are pricing in over 60% of a June hike. Markets would be eager to get some hints for that in this week's FOMC statement. Meanwhile, ISM indices and non-farm payroll would shed some lights on how the US economy would rebound after a weak Q1.

Quick update: ISM manufacturing index dropped to 54.8 in April, below expectation of 56.7. Employment component also dropped sharply to 52.0, down from 58.9.

Macron talks tough on EU

Ahead of the French Election on May 9, front-runner pro-EU centrist Emmanuel Macron warned that EU must reform or face the risk of Frexit. Macron said that "I'm a pro-European, I defended constantly during this election the European idea and European policies because I believe it's extremely important for French people and for the place of our country in globalization." Be he also emphasized that "we have to face the situation, to listen to our people, and to listen to the fact that they are extremely angry today, impatient and the dysfunction of the EU is no more sustainable." And he considers his mandate to "reform in depth the European Union and our European project" after winning the election.

Le Pen softens her stance

On the other hand, far-right euro-sceptic Marine Le Pen softened her stance on Euro. She still insisted of leaving Euro and repeated that the Euro is "dead", isn't "viable" and "everyone has been saying it for years. But, she now noted that "the transition from the single currency to the European common currency is not a pre-requisite of all economic policy, the timetable will adapt to the immediate priorities and challenges facing the French government". And, "everything will be done to ensure an orderly transition ... and the coordinated construction of the right for each country to control its own currency and its central bank."

Blair to be back in politics

In UK, former Prime Minister Tony Blair announced his return to politics as "this Brexit thing has given me a direct motivation to get more involved". He criticized that the Conservatives are keen to deliver "Brexit no matter what the cost". But he used a football metaphor and said that "the single market put us in the Champions League of trading agreements". A free trade agreement is like "League One" and "we are relegating ourselves". But after all, polls suggest that Blair's Labour Party will be beaten heavily in the upcoming election in June.

May sells strong leadership

Current Prime Minister Theresa May responded to the approval of EU's guidelines on Brexit negotiation. She emphasized that "what matters sitting around that table is a strong Prime Minister of the United Kingdom, with a strong mandate from the people of the United Kingdom which will strengthen our negotiating hand to ensure we get that possible deal."

EU leaders showed unity during the weekend and approved the Brexit negotiation guidelines unanimously. EU will insist on the approach that the exit deal should be completed before trade negotiations. It's reported that UK will be required to "respect the obligation resulting from the whole period" of the membership and pay the agreed seven-year budget that concludes in 2020. The sum is estimated to be between EUR 40b and EUR 60b.

The European Commission will come up with a more detailed proposal for governments to approve on May 22. Formal negotiation will start after election in UK on June 8.

RBA watched in upcoming Asian session

RBA rate decision will be another focus this week. The central bank is widely expected to keep the cash rate unchanged at 1.50%. Rate has been staying at this record low since last August. Also, RBA would likely continue to adopt a neutral stance even though inflation has returned to target band of 2-3% in Q1. Meanwhile, one of the keys to shape the policy path this year would be the government budget to be unveiled on May 9.

China PMIs point to slowing growth

Released yesterday, the official China PMI manufacturing dropped to 51.2 in April, down from 51.8, and below expectation of 51.7. PMI non-manufacturing dropped to 54.0, down from 55.1. The data suggests that growth in China would slow after the unexpected pickup in first quarter. In particular, the employment component dipped into contraction region at 49.2 while output also dropped 0.4 pt to 53.8. There are also expectations that the government's policy would turn into a more cautious approach ahead. Nonetheless, the economy in China will likely remain robust.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2899; (P) 1.2932; (R1) 1.2975; More...

Intraday bias in GBP/USD remains neutral for consolidation below 1.2965 temporary top. Further rally is expected as long as 1.2755 minor support holds. Break of 1.2965 will target 161.8% projection of 1.2108 to 1.2614 from 1.2365 at 1.3184. At this point, price actions from 1.1946 are still interpreted as a correction pattern. Therefore, we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2755 minor support will turn bias to the downside. Further break of 1.2614 resistance turned support will now indicate near term reversal.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Apr F | 52.7 | 52.8 | 52.8 | |

| 01:00 | AUD | TD Securities Inflation M/M Apr | 0.50% | 0.10% | ||

| 07:15 | CHF | Retail Sales (Real) Y/Y Mar | 2.10% | 0.50% | 0.60% | 0.70% |

| 12:30 | USD | Personal Income Mar | 0.20% | 0.30% | 0.40% | 0.30% |

| 12:30 | USD | Personal Spending Mar | 0.00% | 0.20% | 0.10% | 0.00% |

| 12:30 | USD | PCE Deflator M/M Mar | -0.20% | 0.10% | ||

| 12:30 | USD | PCE Deflator Y/Y Mar | 1.80% | 2.10% | ||

| 12:30 | USD | PCE Core M/M Mar | -0.10% | -0.10% | 0.20% | |

| 12:30 | USD | PCE Core Y/Y Mar | 1.60% | 1.80% | ||

| 14:00 | USD | ISM Manufacturing Apr | 54.8 | 56.7 | 57.2 | |

| 14:00 | USD | ISM Prices Paid Apr | 68.5 | 66.5 | 70.5 | |

| 14:00 | USD | Construction Spending M/M Mar | 0.40% | 0.80% | ||

| 23:50 | JPY | BOJ Minutes of March 15-16 Meeting | ||||

| 23:50 | JPY | Monetary Base Y/Y Apr | 21.20% | 20.30% |

CAC Unchanged as French Stock Market Closed for Holiday

The CAC is unchanged in the Monday session, as the Paris stock exchanged is closed for the May 1 holiday. Currently, the index is trading at 5,267.33. There are no French or Eurozone indicators on Monday. On Tuesday, the Eurozone and France release Manufacturing PMIs, as we'll get a look at as the Eurozone Unemployment Rate.

It's week two of the second round of the French presidential campaign, with voters choosing between centrist Emmanuel Macron and far-right candidate Marie Le Pen. The markets have priced in a victory by Macron, which is why we didn't see significant movement in European stock markets last week. The opinion polls ahead of the first round were on the money, correctly forecasting that Macron would win 24% of the vote and Le Pen 22%, with both advancing to the May 7 runoff. The markets are relying on the polls ahead of the second round, which continue to show Macron with a comfortable lead of 60-40. Macron should prevail, but Brexit and Trump are fresh reminders that polls can be off the mark and surprises in politics can always happen. Still, unless polls shift dramatically this week, the election campaign is unlikely to have much impact on European stock markets.

The ECB has implemented an ultra-loose monetary policy since 2008, in an attempt to kick-start the eurozone economy and raise inflation levels. With growth and inflation pointing upwards in the first quarter, will we see a tightening of policy? The ECB appears in no rush to make any changes, even though inflation levels have improved. The estimate for CPI in April improved 1.9% in April, up from 1.5% in March. Still, Mario Draghi stated on Thursday that the ECB was not changing its inflation forecast. The ECB held rates at a flat 0.00%, and the rate statement and comments from Mario Draghi were more dovish than the markets would have liked. The current ultra-loose policy, which includes a quantitative easing program of EUR 60 billion/mth, has been in place since 2008. Draghi acknowledged that the eurozone is in better shape, noting that economic conditions had improved and downside risks had decreased. The ECB holds its next meeting in June, and if growth and inflation data continue to point upwards, the markets will again be looking for some tightening from the central bank.

May Day, May Day, Thin Trading Ahead

The yen has weakened; global yields have rallied, while equities have climbed as a tentative deal by U.S Congress to avert a government shutdown overshadows weaker economic data from China and the U.S.

The U.S House and Senate seems to have reached a bipartisan agreement yesterday on a +$1.1T bill to keep the government open through the end of September, ahead of a busy week for macro-economic events and data.

Tomorrow, the RBA announces its monetary policy decision followed by the FOMC Wednesday – no policy changes are expected.

Global manufacturing and composite PMI's begin Tuesday, while Canada releases its March merchandise trade data.

On Friday, its the 'crème de la crème' of North American economic data, both the U.S and Canada will update their employment data for last month.

Elsewhere, the second round of the French presidential election takes place on May 7 and the market is also weighing the possibility of escalating tension between the U.S and North Korea.

1. Stocks little fussed in holiday trading

In Japan, the Nikkei hit a six-week high (+0.2%) as tech shares jump on earnings. The broader Topix index rose +0.5% to the highest level since March 29, after capping its biggest weekly gain of the year on Friday.

Down-under, Australia's S&P/ASX 200 Index gained +0.6%, climbing for a seventh consecutive session for the longest winning streak in 10-months. However, volumes were down in thin trading from the 30-day average. In New Zealand, the S&P/NZX 50 Index advanced less than +0.1%.

In Europe, markets are closed for the May Day holiday.

U.S stocks are expected to open little changed (+0.1%).

Note: On Friday, the S&P 500 Index posted a +1.5% advance to close out the final week of April.

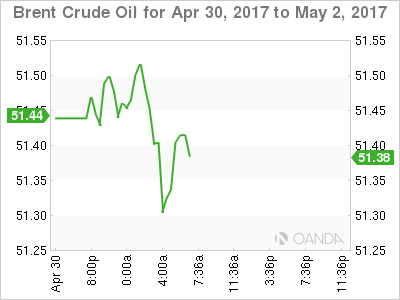

2. Crude oil under pressure from production increases, gold down

Oil prices are starting the week on the back foot as rising crude output and drilling in the U.S offsets OPEC-led production cuts aimed at clearing a global supply glut.

Brent crude for July is down -33c at +$51.72 a barrel, while U.S light crude (WTI) is down -27c at +$49.06 a barrel.

Note: Data on Friday's from Baker Hughes showed that U.S drillers added more oilrigs in the week to April 28 – 870 vs. 857-w/w, +1.5%.

Prices have also come under pressure after an official survey showed yesterday that growth in Chinese manufacturing (see below) slowed faster than expected this month, potentially weighing on the outlook for oil demand.

OPEC and participating non-OPEC countries meet on May 25 to discuss whether to extend last November's reduction agreement. Consensus believes that given that inventories remain high, they expect OPEC to support prolonging the curbs in H2.

Gold prices fell overnight amid thin trading as the 'mighty' dollar firmed. The yellow metal price fell -0.4% to +$1,262.51 per ounce.

3. Fed to dominate proceedings

The FOMC is not expected to change its monetary policy when it concludes its two-day meeting Wednesday, although uncertainty about the prospect of a June rate rise continues to remain. Officials are expected drill down into details about “when and how” to reduce their large holdings of mortgage and Treasury securities.

Note: U.S futures are pricing in a +63% probability on a Fed rate increase by June.

Several Fed officials have indicated they expect to lift rates around two more times this year. Last Friday's weaker Q1 GDP print (+0.7% vs. +1.1%) may not be enough to prevent the Fed from raising rates in June.

The challenge in their post-meeting policy statement will be to acknowledge the handful of disappointing economic growth indicators since officials last gathered in mid-March without suggesting they are ready to veer from the policy path they have sketched out at recent meetings.

The yield on 10-year Treasuries has backed up +2 bps to +2.30%, after dropping for three consecutive sessions.

4. May Day sees thin trading

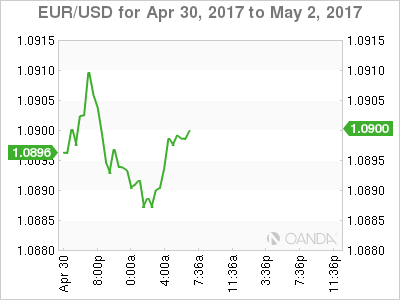

The FX market has started this data laden week relatively quite due to the number of markets closed in both the Far East and Europe for the May Day celebrations.

The dollar bulls will be expecting their currency to try and find firmer footing after last week's disappoint performance. The EUR (€1.0897) starts the week off trading just below the psychological €1.09 handle. Last week, the 'single' unit put in a strong shift on the back of the first round election results (Macron and Le Pen square off this weekend, May 7), and on a no-move from the ECB.

Note: Solid Euro inflation data is supporting the currency and could prompt the ECB to take a more 'hawkish' tone in its June statement.

USD/JPY (¥111.80) continues to edge towards the €112 handle. However, expect the market to remain 'fleet of foot' on any developments re-North Korea that would bring more safe-haven flows back into the yen.

5. China official PMI's slow to six-month lows, while Japan's rise

Following weaker-than-expected U.S growth data for Q1 on Friday, China data over the weekend showed a decline in manufacturing and services sectors.

Last month's official manufacturing and non-manufacturing PMI's both hit six-month low on lower prices and lower demand. New export orders and employment components slumped to a three-month low, while input prices are at a ten-month low.

China April Manufacturing PMI Govt. Official: 51.2 (six-month low) vs. 51.6E; non-manufacturing PMI: 54.0 (six-month low) vs. 55.1 prior.

In Japan, April manufacturing PMI (52.7 vs. 52.8 prelim.) was confirmed at an eight-month high, supported by strengthening overall demand across the South East Asia region with exports seen as a key driver of growth.

Down-under, Aussie inflation also trended hotter (+0.5% vs. +0.1% – three-month high), while manufacturing expanded for the eight consecutive month (59.2 vs. 57.5 prior).

DAX Subdued As German Stock Market Closed For May 1 Holiday

It's a quiet start to the week for the DAX, as the Frankfurt stock exchange is closed for the May 1 holiday. The index has ticked higher in the Monday session, and is trading at 12,438.00 points. There are no German or Eurozone indicators on Monday. On Tuesday, we'll get a look at Eurozone and German Manufacturing PMIs, as well as the Eurozone Unemployment Rate.

Eurozone consumer inflation climbed considerably in April. The Eurostat flash estimate indicated that CPI will climb to 1.9% in April, compared to 1.5% in March. Although this figure is close to the ECB inflation target of about 2 percent, the markets are not expecting Mario Draghi & Co. to make any monetary moves just yet. Last week, the ECB held rates at a flat 0.0%, and Draghi sent a dovish message out to the markets, saying that the ECB's inflation forecast remained unchanged. The current ultra-loose policy, which includes a quantitative easing program of EUR 60 billion/mth, has been in place since 2008. Draghi acknowledged that the eurozone is in better shape, noting that economic conditions had improved and downside risks had decreased. There had been speculation that the ECB might taper or bring forward its asset-purchase program, which runs until December. The ECB holds its next meeting in June, and the markets will again be looking for some tightening from the ECB.

The French presidential campaign continues this week, with voters choosing between Emmanuel Macron and Marie Le Pen. The markets have priced in a victory by Macron, which is why we didn't see significant movement in European stock markets last week. The opinion polls ahead the first round were fairly accurate, correctly forecasting that Macron would win 24% of the vote and Le Pen 22%, with both advancing to the May 7 runoff. The markets are thus relying on the polls for the second round, which continue to show Macron with a comfortable lead of 60-40. Le Pen is a heavy underdog, compounded by the fact that some candidates from the first round as well as former President Francois Hollande have publicly called for voters to support Macron. At the same time, traders should keep an eye on the polls, as any shift in the numbers could quickly translate into some volatility from the stock markets.