Sample Category Title

Trade Idea Wrap-up: USD/JPY – Stand aside

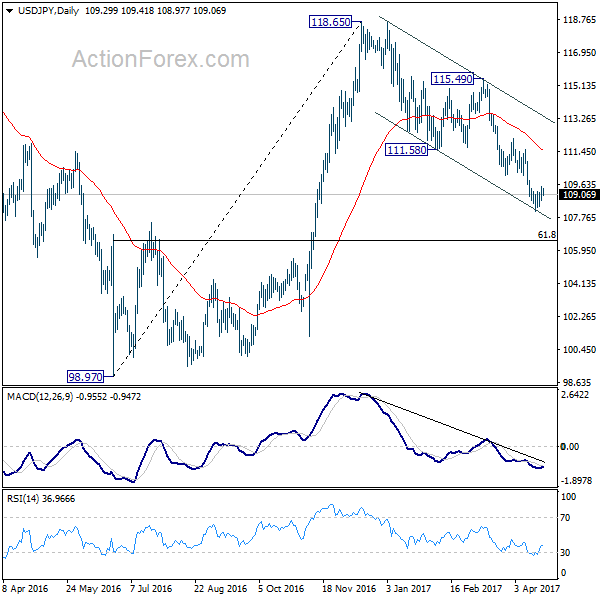

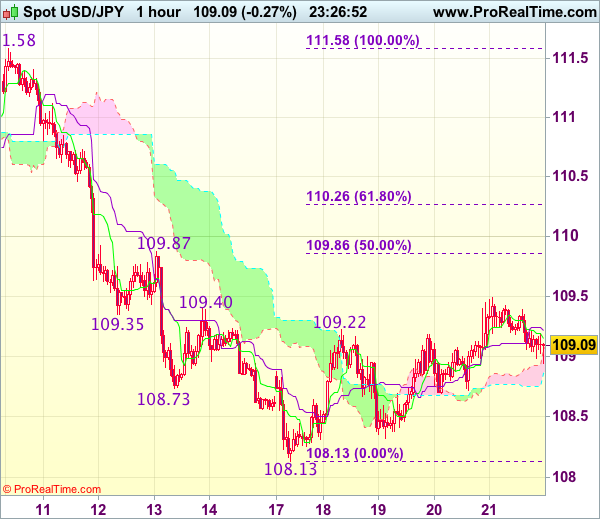

USD/JPY - 109.09

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 109.15

Kijun-Sen level : 109.22

Ichimoku cloud top : 109.05

Ichimoku cloud bottom : 108.86

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although yesterday’s anticipated rebound to 109.49 adds credence to our near term bullish view for the erratic rise from 108.13 to bring retracement of recent decline, reckon upside would be limited to 109.86-87 (50% Fibonacci retracement of 111.58-108.13 and previous resistance), however, price should falter below 110.25-30 (61.8% Fibonacci retracement) and bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 108.65-70 would suggest top is formed, bring weakness to 108.30-32, break there would signal the rebound from 108.13 has ended, bring retest of this level first.

Trade Idea: EUR/GBP – Sell at 0.8475

EUR/GBP - 0.8357

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Sell at 0.8475, Target: 0.8325, Stop: 0.8515

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.8475, Target: 0.8325, Stop: 0.8515

Position : -

Target : -

Stop : -

Euro’s rebound after dropping to 0.8312 earlier this week suggests consolidation above this level would be seen and retracement to 0.8440-50 cannot be ruled out, however, reckon 0.8475-80 would limit upside and bring another decline, below 0.8335-40 would bring retest of said support at 0.8312 but break there is needed to signal recent decline from 0.8788 is still in progress and may extend further weakness to 0.8300, then towards 0.8275-80.

In view of this, would not chase this fall here and would be prudent to sell euro on subsequent recovery as 0.8475-80 should limit upside. Only above previous resistance at 0.8512 would abort and signal a temporary low is formed instead, risk a stronger rebound to 0.8545-50 but resistance at 0.8580 should remain intact.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

EUR/GBP Tests Major Support Ahead of the French Election

EUR/GBP has retraced since March 13.

Tuesday April 18, EUR/GBP hit the lowest level of 0.8312 since December 5, due to the UK early general election shock.

However, the downtrend was held above the significant mid-term major support level at 0.8300 since then.

The first-round voting of the French presidential election will be held this Sunday April 23.

The consensus is that the Centrist Macron and the far-right wing Le Pen would likely get into the second round, then Macron would likely win the final vote.

If result of the first-round turns out to be the far-right wing Le Pen's share of votes surpasses Macron's, or both the far-right wing Le Pen and the far-left wing Melenchon get into the second round. We will likely see a falling Euro.

In this situation, EUR/GBP will likely test the support level at 0.8300 again. If it is broken, then we will likely see an extension of the downtrend.

Conversely, if the result of the first-round turns out to be Macron 's share of votes notably surpasses Le Pen's, or both Macron and Fillion get into the second round. Then we will likely see the Euro rally as market concerns over the collapse of the EU would be relieved.

In this situation, EUR/GBP will likely see a rebound.

The resistance level is at 0.8385, followed by 0.8400 and 0.8415.

The support line is at 0.8350, followed by 0.8330 and 0.8300.

Be aware that the Euro and Euro crosses will likely be volatile before and after the release of the result.

Weekly Focus: Elections Set the Agenda in Europe

Market movers ahead

- There are no clear favourites in the first round of the French presidential elections, in which several candidates are EU sceptics.

- The ECB meets during the week and will probably take the opportunity to dampen the expectations of higher rates that came in the wake of the March meeting.

- Euro-area inflation will probably rise slightly in April, but nowhere near enough for the ECB to start tightening monetary policy.

- Confidence indicators have been pointing to strong growth in the US in 2017, but hard data have been more subdued, so there is strong interest in the GDP numbers for Q1.

- In Sweden, the Riksbank is expected to announce that it will not be extending its asset purchase programme even though inflation remains low.

Global macro and market themes

- Elections in Europe come against the backdrop of the global business cycle looking to lose momentum.

- First round of French presidential elections too close to call.

- Relief rally expected if mainstream candidates go to second round.

- A run-off between Marine Le Pen and Jean-Luc Mélenchon cannot be precluded and could set off a major market correction.

- The UK election is likely to strengthen Theresa May's hand in the upcoming Brexit negotiations.

Currencies: No Further Euro Gains ahead of French Election

Headlines

European equities initially slid lower, but the losses were easily recouped after which sideways trading followed. US stock markets opened little changed.

The euro zone defied expectations of slowing growth in April, expanding for another month, according to Markit PMI business sentiment. Its closely-watched measure of economic activity climbed to a fresh post-euro zone crisis high of 56.7 in April from 56.4, beating forecasts, to hit its highest level since April 2011.

UK retail sales fell back more than predicted in March to cap off the first quarterly decline since 2013 in the latest sign that rising inflation is beginning to weigh on economic growth. Retail sales excluding auto fuel fell by 1.5% compared to February, bringing the year on year growth rate down to 2.6%, from 4.1% the previous month.

BOE policy maker Michael Saunders sees risks that the weaker pound will boost near-term inflation more than officials projected in February. "I would not be surprised if CPI inflation reaches 3% later this year or early next".

Federal Reserve staff, widening their outreach to investors in anticipation of a critical turning point in monetary policy, are seeking bond fund manager feedback on how the central bank should tailor and communicate its exit from record holdings of Treasuries and mortgage-backed securities.

Belgium's 2016 budget deficit widens to EU11.1b, or 2.6% of GDP, from EU10.3b, or 2.5% of GDP in 2015. Gross public debt rises to EU446.8b, or 105.9% of GDP, from EU434.8b, or 106.0% of GDP in 2015. EU Commission anticipated a 2016 deficit of 2.9% of GDP, debt-to-GDP ratio of 106.8% at year-end for Belgium

Rates

Core bonds take day off ahead of French election

Core bonds showed no appetite to choose direction today and stayed near yesterday's closing levels. The April EMU PMI rose unexpectedly for the sixth consecutive month to a 6 year high, suggesting that the strong economic momentum isn't hindered by political uncertainty. Even the Italian economy is gaining momentum, as evidenced by iron-strong industrial sales and orders figures. For the bond markets, it was worth one long yawn. Some punters anticipated a continuation of the past two days selling spree at the start of the Bund trading. They tried to push the Bund lower, but once equities opened, the losses were recouped. Traders understood that it would be a wait-and-see session ahead of the French election. The Bund sleep-walked around in a 20 ticks range. US traders had even less appetite than their European peers and Treasuries remained range-bound too as the US market calendar was unenticing.

At the time of writing, the German yield curve bull steepens marginally with yields 0.7 bps (2-yr) to 0.1 bp (30-yr) lower. Changes on the US yield curve ranged between -0.4 bps (2-yr) and +0.4 bps (30-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany narrowed up to 4 bps for France. Core spreads widened 1 bp.

Currencies

No further euro gains ahead of French election

Yesterday's pro-Europe/France repositioning didn't continue. EUR/USD and USD/JPY held tight ranges respectively in the 1.07 and the 109 area. Investors kept a wait-and-see modus going into the first round of the French presidential election. The EMU PMI was strong, but had also no impact on the euro.

This morning, Asian markets to some extent joined the risk rally from the US yesterday evening. However, contrary to what happened yesterday, the move had no big impact on the dollar. EUR/USD stabilised in the low 1.07 area. USD/JPY traded near the 109.25 level.

At the start in Europe, investors retried yesterday's tactics. Both EUR/USD and USD/JPY gained a few ticks. The move had no strong legs and all the gains evaporated very soon. The EMU PMI's (in particular the French ones) were strong, indicating ongoing good growth in EMU at the start of the second quarter. However, it didn't help a resumption of yesterday's risk-on trade. On the contrary, the topside of European equities was blocked and core bond yields stabilized. Both EUR/USD and USD/JPY lost a few ticks, returning to the 1.07 and 109 big figures. Yesterday's terrorist attack in Paris maybe made investors a bit reluctant to adopt positions further to a market-friendly outcome of Sunday's vote in the first round. The was no additional news this afternoon in the US to spice USD trading., leaving EUR/USD and USD/JPY in directionless trading.

Poor UK retail sales have limited impact on sterling

UK investors focused on the retail sales today. Of late, there were tentative signs that price rises were eroding consumers' purchasing power and that this would affect spending. UK March retail sales declined more than expected -1.8% M/M). A more modest decline of -0.5M/M after a strong February report was expected. The damage for sterling was limited. Cable was well bid going into the publication of the report (intraday top of 1.2835) but returned to the big figure after the report. EUR/GBP jumped up and down in the 0.8375 area as sterling's 'decline' was counterbalanced by a decline of EUR/USD more or less at the same time. So, for now, soft UK data still have only a modest impact on sterling. Later in the session, there were some hawkish comments from BoE 's Saunders as he indicated that the BoE doesn't need to delay a rate hike because of Brexit if growth and inflation are stronger than expected. The reaction of sterling was again close to non-existent. EUR/GBP trades currently in the 0.8365/70 area. Cable hovers around 1.28.

Elliott Wave Analysis: GBPJPY Trading In A Temporary Correction

GBPJPY may be trading at the beginning of a three wave correction, now in wave a. As such after wave a finds bottom a new bounce into wave b may follow. Later the mentioned wave b may see limited upside around the 139.90 level, from where a new drop into the following wave c may follow. Support for the whole corrective retracement may later be around the 138.29 level.

GBPJPY, 1H

Canadian CPI Growth Moderated Further in March

Highlights:

- The year-over-year rate of headline CPI inflation edged down to 1.6% (below expectations for a 1.8% reading) from 2.0% in February 2.1% in January.

- The rate of energy price inflation eased to 8.5% (on a year-over-year basis) from 12.3% in February but food price weakness eased to –1.9% from the 46-year low –2.3% in the earlier month.

- Excluding food and energy, price growth dropped to 1.7% from 2.0% in February and 2.2% in January.

- Of the Bank of Canada's three preferred 'core' measures, the 'CPI-Median' and 'CPI-Trim' measures both moderated, to 1.7% from 1.8% and 1.4% to 1.5%, respectively, while the 'CPI-Common' held at historically low levels (1.3%).

Our Take:

The dip in the headline CPI year-over-year rate of growth to 1.6% from 2.0% in February provides little evidence that stronger recent economic growth is generating greater underlying inflation pressures. The latest monthly dip in part reflected a moderation in energy price growth (which moderated to 8.5% on a year-over-year basis from 12.3% in February); however, the larger factor was a moderation in the pace of growth excluding the energy and food components to a 1.7% year-over-year pace from 2.0% in February and 2.2% in January. Of the Bank of Canada's three preferred 'core' measures, the 'trim' (1.4% in March) and 'median' (1.7%) both edged lower from modestly downwardly revised levels in earlier months while 'CPI-Common' held at 1.3%, matching its lowest level since the mid-1990s. The monthly price data can be volatile and we continue to expect the underlying trend rate of price growth is just under a 2% rate; however, alongside continued modest wage growth to-date in 2017, today's report will provide further ammunition to the Bank of Canada's argument that the economy continues to run materially below its long-run production capacity.

Canada: Inflation Mellows in March

Consumer price inflation decelerated to 1.6% (year-on-year) in March from 2.0% in February. Most categories experienced a slower rate of price growth in March, with decelerating energy prices leading the way. The broader, transportation price growth slowed to 4.6% from 6.6% in February.

Declining food prices (-1.9% y/y) and clothing and footwear prices (-0.9% y/y) weighed on the headline.

The Bank of Canada's core measures softened, with CPI-median edging down to 1.7% (from 1.8%), and CPI-trim to 1.4% (from 1.5%), and CPI-common unchanged at a feeble 1.3%.

Key Implications

Economic data has turned up in Canada in recent months, but softening inflation gives the Bank of Canada scope to fade some of that strength and await confirmation that it will be sustained. The deceleration in the core measures in particular means the Bank of Canada will be in no rush to remove accommodation.

Soft inflation and wage growth is the best evidence that the Canadian economy continues to operate under its potential. With faster economic growth, the output gap will eventually close and begin to exert upward pressure on inflation. However, this is likely to be more of a 2018 story than a 2017 one.

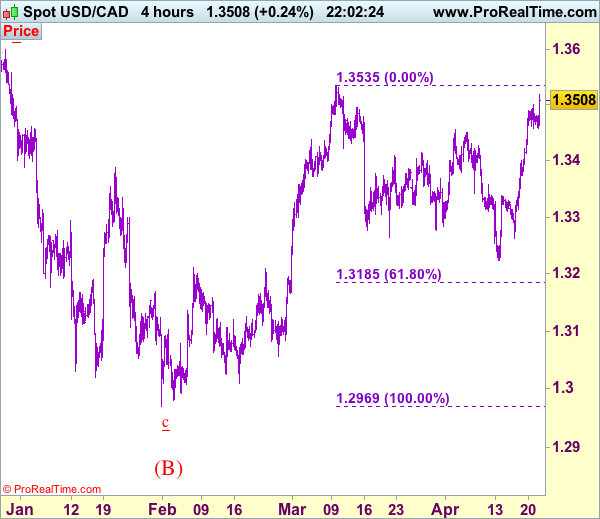

Trade Idea: USD/CAD – Buy at 1.3430

USD/CAD - 1.3510

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Buy at 1.3400, Target: 1.3580, Stop: 1.3340

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.3430, Target: 1.3590, Stop: 1.3370

Position: -

Target: -

Stop:-

As the greenback has risen again after brief pullback, adding credence to our view that the correction from 1.3535 has ended and upside bias remains for the rise from 1.3223 to extend gain to previous resistance at 1.3535, once this level is penetrated, this would confirm early upmove has resumed and extend headway towards previous chart resistance at 1.3599 later which is likely to hold from here.

In view of this, would not chase this rise here and would be prudent to buy on subsequent pullback as 1.3430 should limit downside. Only below previous resistance at 1.3337 would abort and suggest top is possibly formed, risk weakness to 1.3300-10 but indicated support at 1.3262 should remain intact.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.85; (P) 109.17; (R1) 109.63; More....

Intraday bias in USD/JPY remains neutral for consolidation above 108.12. With 110.10 resistance intact, near term outlook remains bearish. Rise from 98.97 is finished at 118.65 and fall from there would extend. On the downside, break of 108.12 will target 61.8% retracement of 98.97 to 118.65 at 106.48. Sustained break there will pave the way back to 98.97 low. Nonetheless, break of 110.10 will be the first sign of near term bottoming and turn bias back to the upside for 112.19 resistance instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. Current development suggests that it's not completed yet and is extending. In case of deeper decline, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Rise from 75.56 is still expected to resume later after the correction from 125.85 completes.