Sample Category Title

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9954; (P) 0.9971; (R1) 1.0001; More.....

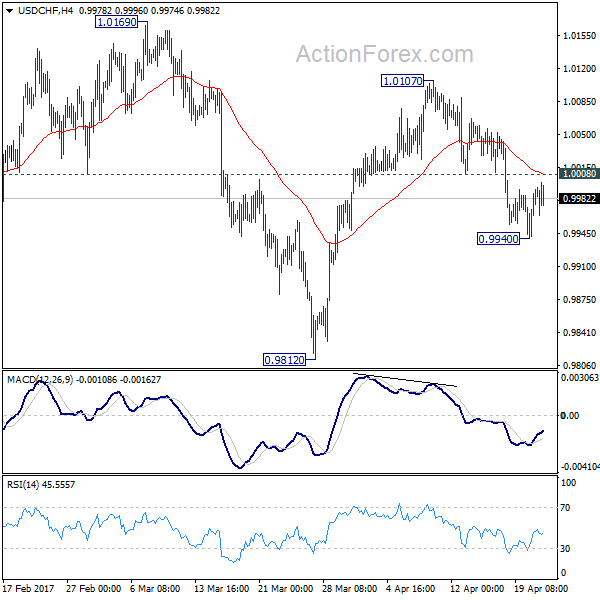

Intraday bias in USD/CHF remains neutral for consolidation above 0.9940 temporary low. Another decline is in favor as long as 1.0008 minor resistance holds. Below 0.9940 will target 0.9812 and below. Fall from 1.0342 is seen as a correction. Hence, we'll look for bottoming signal below 0.9812. Meanwhile, on the upside, above 1.0008 minor resistance will turn bias back to the upside for 1.0107 resistance instead.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the cross. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

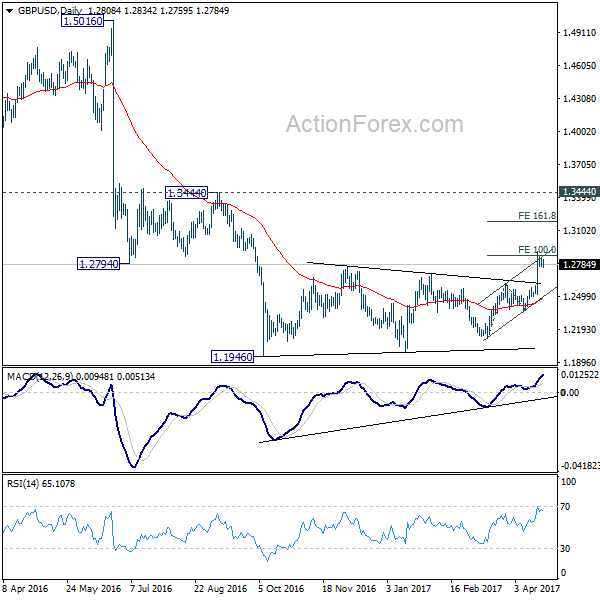

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2772; (P) 1.2809; (R1) 1.2847; More...

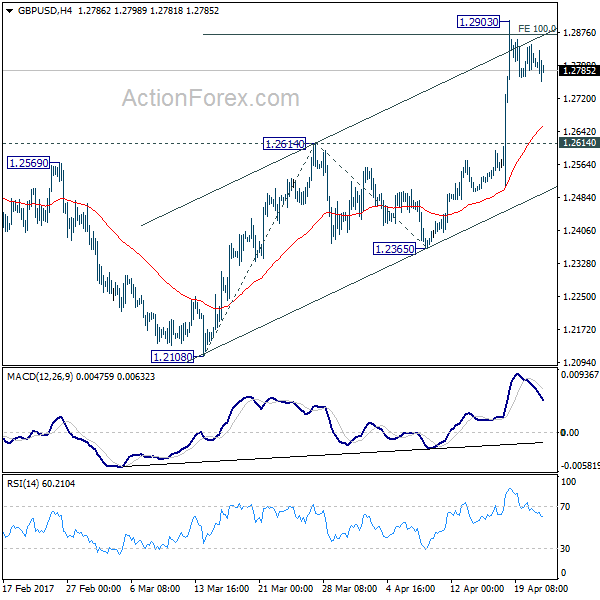

Intraday bias in GBP/USD remains neutral for the moment. With 1.2614 resistance turned support holds, near term outlook remains bullish for further rise. Firm break of 100% projection of 1.2108 to 1.2614 from 1.2365 at 1.2871 will target 161.8% retracement at 1.3184. Still, price actions from 1.1946 are seen as a correction. Hence we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2614 resistance turned support will turn bias back to the downside for 1.2365 support first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 0.9990

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The greenback rebounded after holding above yesterday’s low at 0.9941, suggesting consolidation above this level would be seen and test of previous support at 1.0008 (now resistance) cannot be ruled out, however, break there is needed to signal low is formed and bring retracement of recent decline from 1.0108 to 10030 but resistance at 1.0067 should remain intact.

On the downside, below said support at 0.9941 would extend recent decline to 0.9935-38 (50% projection of 1.0067-0.9955 measuring from 0.9992) and then 0.9926 (61.8% Fibonacci retracement of 0.9813-1.0108) but reckon 0.9900-05 (1.618 times projection of 1.0108-1.0008 measuring from 1.0067) would hold, bring rebound later. As near term outlook is mixed, would be prudent to stand aside for now.

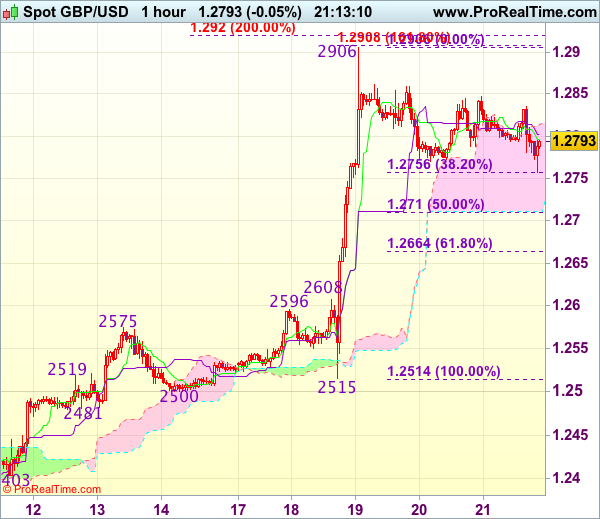

Trade Idea Update: GBP/USD – Buy at 1.2710

GBP/USD - 1.2788

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2814

Kijun-Sen level : 1.2817

Ichimoku cloud top : 1.2810

Ichimoku cloud bottom : 1.2711

Original strategy :

Buy at 1.2710, Target: 1.2850, Stop: 1.2675

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2710, Target: 1.2850, Stop: 1.2675

Position : -

Target : -

Stop : -

Cable has remained confined within familiar range and further sideways trading is in store, however, downside should be limited to 1.2755-60 (38.2% Fibonacci retracement of 1.2515-1.2906) and reckon 1.2700-10 would hold, bring another rally, break of 1.2755069 would signal the pullback from 1.2906 has ended, bring retest of this level, break there would extend recent upmove to 1.2920-30 (2 times extension of 1.2365-1.2575 measuring from 1.2500), then 1.2950 but loss of near term upward momentum should prevent sharp move beyond 1.2990-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance).

In view of this, would not chase this rise here and would be prudent to buy cable on subsequent pullback as downside should be limited to 1.2710 (50% Fibonacci retracement of 1.2515-1.2906), bring another rise. Below 1.2700 would defer and signal top has been formed, risk correction to 1.2660-65 (61.8% Fibonacci retracement of 1.2515-1.2906) and price should stay well above 1.2608-16 (previous resistance now support).

Trade Idea Update: EUR/USD – Hold long entered at 1.0690

EUR/USD - 1.0700

Original strategy :

Bought at 1.0690, Target: 1.0790, Stop: 1.0655

Position : - Long at 1.0690

Target : - 1.0790

Stop : - 1.0655

New strategy :

Hold long entered at 1.0690, Target: 1.0790, Stop: 1.0655

Position : - Long at 1.0690

Target : - 1.0790

Stop : - 1.0665

Euro’s retreat after rising to 1.0778 yesterday suggests a temporary top has been made there and consolidation with mild downside bias is seen for marginal weakness from here, however, reckon downside would be limited and bring another rise later to 1.0783-85 (61.8% projection of 1.0602-1.0737 measuring from 1.0700), then 1.0800-10 but loss of near term upward momentum should prevent sharp move beyond 1.0825-30, risk from there is seen for a retreat to take place later.

In view of this, we are holding on to our long position entered at 1.0690. Only below previous resistance at 1.0670 (now support) would abort and signal top is formed instead, bring correction towards previous support at 1.0635 which is likely to hold from here.

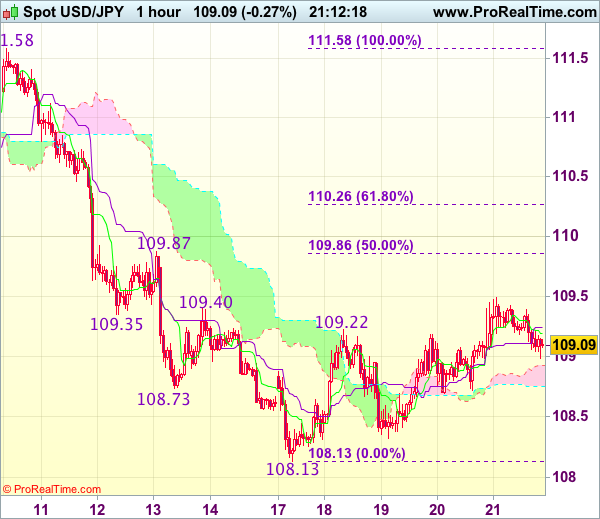

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 109.10

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although yesterday’s anticipated rebound to 109.49 adds credence to our near term bullish view for the erratic rise from 108.13 to bring retracement of recent decline, reckon upside would be limited to 109.86-87 (50% Fibonacci retracement of 111.58-108.13 and previous resistance), however, price should falter below 110.25-30 (61.8% Fibonacci retracement) and bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 108.65-70 would suggest top is formed, bring weakness to 108.30-32, break there would signal the rebound from 108.13 has ended, bring retest of this level first.

CAC Quiet as Investors Cautious Ahead of French Vote

The CAC is showing little change on Friday, following strong gains in the Thursday session. Currently the CAC is trading at 5073.50. On the release front, French and Eurozone Manufacturing PMIs both beat their estimates, and the Eurozone current account surplus easily beat expectations. On Saturday, US Treasury Secretary Robert Mnuchin will speak at the International Monetary Fund meeting in Washington. On Sunday, France goes to the polls for the first round of the presidential election.

European investors are holding their breath, as France goes to the polls on Sunday, in the first round of the presidential election. The election campaign has been divisive and turbulent, in one of the tightest elections in years. The four front-runners (in a crowded field of 11) are all within a few percentage points of one another. Given the tightness and unpredictability of the race, final opinion polls have become market-movers. The CEC posted strong gains on Thursday, following an opinion poll which showed Emmanuel Macron opening a slight lead with 25% of the vote, just ahead of far-right candidate Marie Le Pen with 22%. Le Pen's platform includes sharp curbs on immigration and a referendum on France's membership in the European Union. If Le Pen does better than predicted, investor sentiment could send the stock markets lower. A shooting in Paris on Thursday which killed a policeman and a tourist have stretched taut nerves even further, as security and the terrorism threat remain one of the key issues in the campaign. The markets are expecting more volatility ahead of and following the election, and French banks will be staffed throughout Sunday night in order to respond quickly to the election results. Traders should be prepared for volatility from the CEC in the Monday session.

The eurozone economy continues to expand, and this was underscored by strong PMIs out of Europe. Eurozone, French and German PMIs all pointed to expansion in the services and manufacturing sectors. Manufacturing data was particularly encouraging, as Eurozone and French Manufacturing PMIs beat expectations. However, these strong readings failed to move the CAC, as investors are keeping low ahead of the French election on Sunday. There was more positive news as the eurozone's current account surplus jumped to EUR 37.9 billion, well above the estimate of EUR 26.3 billion.

With the US economy in good shape, the markets are expecting interest rates to continue rising in 2017. The Fed has broadly hinted that it will gradually raise rates this year, but it's unclear how many times Janet Yellen will press the rate trigger. Most analysts are expecting two more moves this year, but there have been calls from some Fed policymakers for three more hikes. However, soft retail sales and CPI numbers in March are likely to make the Fed more dovish, and on Tuesday, the Atlanta and New York Federal Reserve lowered their outlook for US economic growth for the first quarter. The Fed can point to a labor market that is close to capacity as well as strong consumer confidence, but surprisingly, this has not translated into stronger consumer spending, a key driver of economic growth. The Fed is unlikely to make a move in May, but June is a strong possibility. However, the odds of a June move are showing a surprising amount of volatility, and the latest CME Group reading shows the likelihood a 1/4 point hike have jumped to 58%, up from 51% earlier this week.

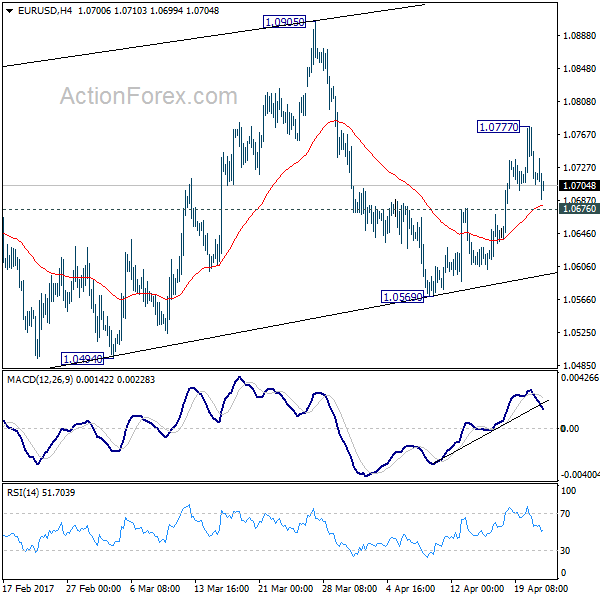

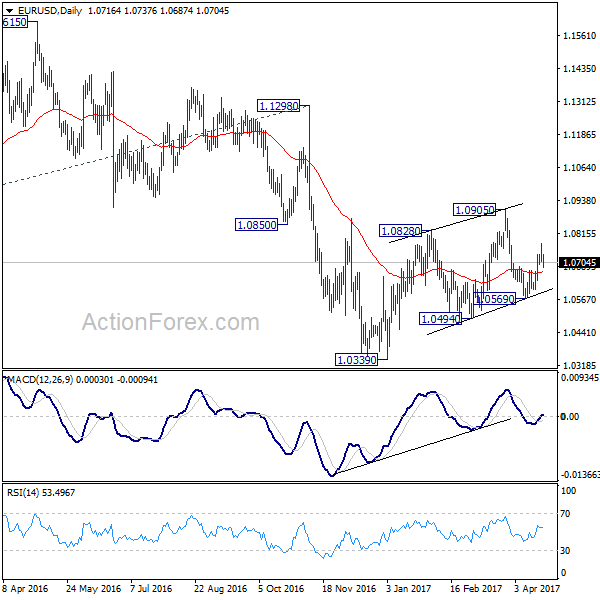

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0688; (P) 1.0733 (R1) 1.0759; More....

EUR/USD's retreat from 1.0777 extends lower today but it's still staying above 1.0676 minor support. Intraday bias remains neutral and another rise is still in favor. Above 1.0777 will target 1.0905 and above. But still, choppy rise from 1.0339 is still seen as a correction. Hence, we'll pay attention to topping signal above 1.0905 again, as we'd expect larger down trend to resume later. On the downside, break of 1.0676 minor support will turn intraday bias back to the downside for 1.0569 instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Euro Weakens Further as French Presidential Elections Looms

Euro dips further today as markets are lighting up positions ahead of the first round of French presidential election this Sunday. Far right Marine Le Pen and centrist Emmanuel Macron are still tipped to come out as winners and head to the run-off on May 7. But yesterday's terrorist attack in Paris could stir up some uncertainties. In particular, far left leader Jean-Luc Melenchon has rather strong momentum in the past two weeks and emerged as a real contender. Euro would very likely suffer if Melenchon could slip into the run-off and take Macron's place. Both Le Pen and Melenchon are euro-sceptic, just at two different extremes. But the common currency could have a relieve rally next week if the election delivers no surprise.

Eurozone PMIs came in strong

Eurozone PMI manufacturing rose to 56.8 in April, up from 56.2, and beat expectation of 56.1. Eurozone PMI services Rose to 56.2, up from 56.0 and beat expectation of 56.0. Germany PMI manufacturing dropped to 58.2, down from 58.3 but beat expectation of 58.1. Germany PMI services dropped to 54.7, down from 55.6 and missed expectation of 55.5. France PMI manufacturing surged to 55.1, up from 53.3 and beat expectation of 53.2. France PMI services rose to 57.7, up from 57.5 and beat expectation of 57.2. Markit noted that "there is a good outlook for the year - it looks like the upturn has legs. With numbers like these, people are going to start edging up their forecasts."

EU Brexit negotiation document leaked

According to a leaked draft EU Brexit negotiation document, UK will be required to pay off the obligations after Brexit, remain subject to EU court and, be required to let relatives of European immigrants settle in UK. And the keys of the negotiation would be about protecting rights of three million EU citizens living in UK. Meanwhile, EU will insist on having ECJ jurisdiction to enforce the rules during the transition period. And that would be in direct conflict with UK as Prime Minister Theresa May would seen to end that ECJ jurisdiction in UK. While EU might consider alternative dispute system for the treaty, it would be under the condition on equivalence to the ECJ.

Finnish RM Orpo: No one will want to follow Brexit

Finland's Finance Minister Petteri Orpo said that UK's "divorce" with EU is "inevitably going to be so painful that no one will want to feel it for themselves." And it's going to be a "precedent no one will want to follow." Meanwhile Orpro is confident that "there should be no slowdown in developing the EU because of Brexit." Instead, the member states should "push even harder". Separatrly, EU Brexit negotiator Michel Barnier said that the so called EUR 60b "Brexit bill" is not "revenge" no punishment" and he emphasized that "we don't want to ask the Brits to pay a single euro more than" their legal obligations.

On the data front...

Canada CPI slowed to 1.6% yoy in March, below expectation of 1.8% yoy. CPI core-trim slowed to 1.4% yoy, CPI core-medium slowed to 1.7% yoy, CPI core-common was unchanged at 1.3% yoy. UK retail sales dropped -1.8% mom in March. Japan PMI manufacturing rose to 52.8 in April, up from 52.4 and beat expectation of 52.5. Also from Japan, tertiary industry index rose 0.2% mom in February.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0688; (P) 1.0733 (R1) 1.0759; More....

EUR/USD's retreat from 1.0777 extends lower today but it's still staying above 1.0676 minor support. Intraday bias remains neutral and another rise is still in favor. Above 1.0777 will target 1.0905 and above. But still, choppy rise from 1.0339 is still seen as a correction. Hence, we'll pay attention to topping signal above 1.0905 again, as we'd expect larger down trend to resume later. On the downside, break of 1.0676 minor support will turn intraday bias back to the downside for 1.0569 instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | PMI Manufacturing Apr P | 52.8 | 52.5 | 52.4 | |

| 04:30 | JPY | Tertiary Industry Index M/M Feb | 0.20% | 0.30% | 0.00% | -0.20% |

| 07:00 | EUR | France Manufacturing PMI Apr P | 55.1 | 53.2 | 53.3 | |

| 07:00 | EUR | France Services PMI Apr P | 57.7 | 57.2 | 57.5 | |

| 07:30 | EUR | Germany Manufacturing PMI Apr P | 58.2 | 58.1 | 58.3 | |

| 07:30 | EUR | Germany Services PMI Apr P | 54.7 | 55.5 | 55.6 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr P | 56.8 | 56.1 | 56.2 | |

| 08:00 | EUR | Eurozone Services PMI Apr P | 56.2 | 56 | 56 | |

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | 37.9B | 26.3B | 24.1B | |

| 08:30 | GBP | Retail Sales M/M Mar | -1.80% | -0.30% | 1.40% | |

| 12:30 | CAD | CPI M/M Mar | 0.20% | 0.40% | 0.20% | |

| 12:30 | CAD | CPI Y/Y Mar | 1.60% | 1.80% | 2.00% | |

| 12:30 | CAD | CPI Core - Trim Y/Y Mar | 1.40% | 1.60% | ||

| 12:30 | CAD | CPI Core - Median Y/Y Mar | 1.70% | 1.90% | ||

| 12:30 | CAD | CPI Core - Common Y/Y Mar | 1.30% | 1.30% | ||

| 13:45 | USD | Manufacturing PMI Apr P | 53.9 | 53.3 | ||

| 13:45 | USD | Services PMI Apr P | 53.7 | 52.8 | ||

| 14:00 | USD | Existing Home Sales Mar | 5.61M | 5.48M |

French Election Monitor: Markets Hold Their Breath as First Election Round Draws Near

As election day for the first round of France's presidential election approaches on Sunday, the result remains unpredictable, with the four leading candidates Marine Le Pen, Emmanuel Macron, François Fillon and Jean-Luc Mélenchon head to head in the polls. Around 30% of voters are still undecided, as outlined in French Election Monitor #2, 18 April. The market reaction afterwards will depend largely on the candidate combination in the second round and we see three broad risk scenarios, depending on the chances of an EU sceptic proceeding to the second round and subsequently winning the presidency (see below). While a run-off between Fillon and Macron would be the lowest risk scenario, with no EU sceptic reaching the second round, we see a face-off between the two EU sceptics Le Pen and Mélenchon as the highest risk scenario, with the biggest adverse market reaction. A 'surprise' scenario where we see, for example, Le Pen significantly outperforming the polls, gaining some 30-49% of the vote in the first round, should also be considered a high-risk scenario, as, in this case, the predictive power of second round polls would also be highly questionable, even if her contender is Macron.

Voting stations will open at 08:00 CEST on Sunday and close at 19:00 in small towns and 20:00 in big cities. Voting in the French overseas constituencies will take place on Saturday, to ensure that voting takes place before any preliminary results are published. Exit polls by the main TV and radio channels are due to be published at 20:00 on Sunday and have been relatively accurate in the past. Keep an eye out for voter turnout estimations released during the day. Lower participation, as suggested by the polls, would be likely to boost Le Pen's chances of winning, as her supporters remain the most certain of their choice.

Official election results will be released by the Ministry of the Interior over the course of the night and updated continually as new results come in district by district. Due to France's overseas territories, the final result will probably be released on Monday around midday. However, unless the race is very tight, the votes from the overseas territories should not move the result much and we should have a good indication of the outcome around midnight or in the early hours of Monday morning.