Sample Category Title

Week Ahead Geopolitics to Cloud Central Bank Outlook

European and Japanese Policy Makers Announce Policy Decisions

Higher political risk in 2017 was forecasted and so far it hasn't disappointed. The calendar of democratic events expanded last week as the United Kingdom announced a snap election that will be held in June. The pound has appreciated above 2 percent since the announcement in the hope it will strengthen the Conservative party's position in parliament and give more latitude for negotiating the British exit from the European Union. The first leg of the French presidential elections will kick off with the second round to take place on May 7.

The Japanese yen is a preferred destination during risk aversion periods which boosted the currency two weeks ago. As risk appetite returned the yen gave back gains and US dollar could continue to advance ahead of the Bank of Japan (BOJ) Outlook Report and monetary policy decisions on early Thursday, April 27. The BOJ will host a press conference at 2:30 am EDT (6:30 am GMT). BOJ Governor Haruhiko Kuroda spoke on Thursday signalling it will continue to keep its monetary policy accommodative with the current pace of asset purchases to remain for some time. Despite growth in the economy the appreciation of the currency could delay inflation reaching the 2 percent goal set by the central bank who could publish a lower target on Thursday.

European Central Bank (ECB) will announce its monetary policy later on the same day. ECB President Mario Draghi is expected to hold the benchmark rate and stimulus programs without any changes. Draghi said on Friday that very substantial accommodation is still necessary in the Euro zone despite the risk of deflation not a going concern. Growth will be on display on Friday, April 28 at 8:30 am EDT when the US releases the first estimate of GDP for the first quarter of 2017, the forecast shows a gain of 1.3 percent that is below the last quarter gain of 2.1 percent. The slowdown of the economy will surely raise questions on what the rate hike path of the Fed when the economy is not gaining momentum and pro-growth policies by the Trump administration are yet to appear.

The EUR/USD gained 0.609 percent in the last five trading days. The single pair is trading at 1.0689 after touching weekly highs of 1.0777 but the US dollar has bounced as French election jitters took its toll on the euro. US President Trump said he would unveil a tax plan next week which got some wind under the greenback sails after his dollar strength comments had sunk the currency.

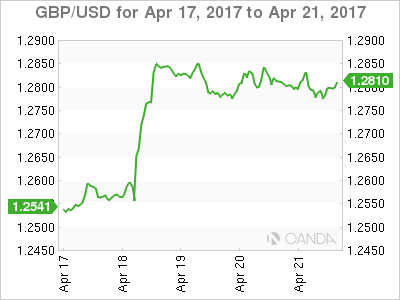

The GBP/USD gained 2.11 percent in the last week. The pair is trading at 1.2796 in a week where British Prime Minister Theresa May announced the decision to call for a snap election in June. The move was ratified by parliament the next day. The market is taking this as a political move to consolidate power in parliament ahead of Brexit negotiations with the European Union.

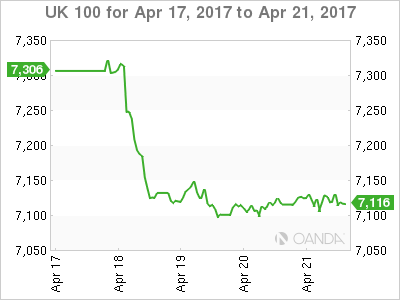

The UK stock market lost 2.56 percent in the last five trading days. The UK100 is trading at 7,119 after UK PM May's shocking decision to call for an early election in June. The rise of the pound as a result of a softer Brexit deal took its toll on the stock market as results were below expectations and the weak UK retail sales data released on Friday. The UK stock market had its worst performance since November.

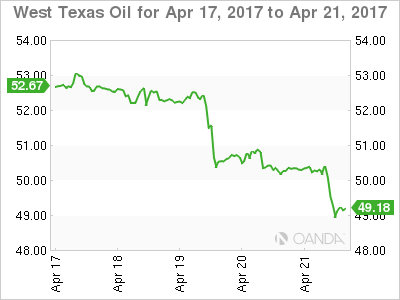

The price of West Texas dropped 7.18 percent in the last week. The energy benchmark is trading at $48.97 as downward pressure from US production has driven the price below $50. The Organization of the Petroleum Exporting Countries (OPEC) production cut deal was able to stabilize prices last year before kicking into effect in 2017, but as it nears the end of its six month term there are doubts on how effective it has really been as there is still ample supply. US oil rig counts rose again for the 14th straight week to a total of 688.

The group will meet in Vienna this weekend with an extension to the production cut deal in the works. Russia has already said that it will meet with OPEC members on late May. Global inflation expectations were based on a higher oil price and if those fail to materialize the reflation trade will have very little to stand on.

Market events to watch this week:

Monday, April 24

- 4:00am EUR German Ifo Business Climate

Tuesday, April 25

- 10:00am USD CB Consumer Confidence

- 9:30pm AUD CPI q/q

Wednesday, April 26

- 8:30am CAD Core Retail Sales m/m

- 10:30am USD Crude Oil Inventories

- 11:50pm JPY Monetary Policy Statement

Thursday, April 27

- Tentative JPY BOJ Outlook Report

- Tentative JPY BOJ Policy Rate

- 2:30am JPY BOJ Press Conference

- 7:45am EUR Minimum Bid Rate

- 8:30am EUR ECB Press Conference

- 8:30am USD Core Durable Goods Orders m/m

- 8:30am USD Unemployment Claims

Friday, April 28

- 4:30am GBP Prelim GDP q/q

- 8:30am CAD GDP m/m

- 8:30am USD Advance GDP q/q

*All times EDT

Weekly Economic and Financial Commentary

U.S. Review

The Expansion Plods Along in a Quiet Data Week

- Housing market data were generally mixed this week, with builder confidence and housing starts declining while existing home sales rose.

- Despite a healthy 0.5 percent increase in industrial production in March, the devil was in the details. The largest surge in utilities output on record masked a decline in manufacturing production.

- The Leading Economic Index (LEI) posted another broadbased gain in March. Our recession forecasting model, which heavily incorporates the LEI, shows a very small chance of a recession in the next six months.

The Expansion Plods Along in a Quiet Data Week

Housing market data released this week were generally mixed but continued to improve on trend. The NAHB/Wells Fargo Housing Market Index fell three points in April from its cycle-high in March. Despite the pullback, confidence remains relatively high; the present sales index has trended above 70 for five consecutive months, signaling strong demand for new homes. Housing starts also dipped, falling 6.8 percent in March, but this decline came on the heels of an unusually strong February reading that was likely boosted by unseasonably warm weather. On balance, the spring construction season got off to a strong start to the year, as starts are up 8.1 percent through the first three months of the year compared to 2016. Further evidence of strength in the housing market could be seen in the existing home sales data released on April 21, which topped expectations. Sales at home improvement stores have also been solid of late and should boost residential construction's contribution to GDP growth in Q1.

The industrial production data for March suggested the factory sector's recovery took a breather last month. On the surface, the strong 0.5 percent gain in industrial production suggests a continued acceleration in activity. However, the largest surge in utilities output on record played an outsized role in the gain. After the second-warmest February on record led to a 5.8 percent decline utilities production, temperatures in the lower 48 returned to more seasonal norms in March. At about 11 percent of the total index, utilities alone boosted the headline by 0.9 percentage points.

Outside of utilities, mining production rose 0.1 percent over the month, with output for oil and gas extraction leading the way with a nearly 8 percent gain. Although far from recovered, the mining sector is headed in the right direction after the steep decline that began in late 2014 (middle chart). Manufacturing output, which comprises about three-fourths of the total index, fell 0.4 percent. Weak auto sales and rising inventories led producers to pullback on motor vehicle and parts production, which declined 3 percent. While the latest data suggest some cooling, we still look for manufacturing output to expand in the coming months. A pause in the dollar's appreciation, more stable commodity prices and a brightening global outlook all bode well for continued improvement in the factory sector.

The Leading Economic Index (LEI) notched a healthy 0.4 percent gain in March. Strong new orders in the ISM Manufacturing Index, robust consumer confidence, rising building permits and additional equity market gains boosted the index and point to steady economic growth ahead. Our primary recession forecasting model uses the LEI as a main component. As illustrated in the bottom chart, the probability of a recession in the next six months has fallen from the brief spike that occurred in early 2016. When the advance release for Q1 real GDP growth comes out next week, we anticipate a soft but positive reading, followed by a pick-up in growth in the subsequent quarter. Thus, for now at least, the economic expansion continues to plod along.

U.S. Outlook

New Home Sales • Tuesday

New home sales rose for the second straight month in February as milder-than-usual weather helped pull activity forward, with the level reaching a seven-month high. Despite the still-elevated level of builder sentiment, sales activity is expected to cool in March as the return to more typical winter weather conditions likely stalled activity. Moreover, since new home sales are registered when the contract is signed, light foot traffic during the seasonally-slow period of the year likely impeded activity. Median home prices fell relative to the previous year in February, while mean prices posted a double-digit gain. Indeed, the gap between the level of median and mean prices was the widest on record as activity was concentrated at the high end of the market. In fact, sales for homes more than $400,000 rose more than 23 percent year over year, while homes priced below the threshold increased just 3 percent. Builders have now turned their sights to lower-priced homes.

Previous: 592K Wells Fargo: 578K Consensus: 588K

Durable Goods • Thursday

Following two straight monthly declines in November and December, orders for durable goods rebounded in January and February. However, much of the headline increase was concentrated in the volatile nondefense aircraft component, which still reflects the surge in orders booked in December. That said, Boeing booked 147 orders (mostly lower priced 737s) in March, which should further lift the headline reading. Similar to the December spike in civilian aircraft orders, we would not be surprised to see headline activity increase over the course of a couple of months. In contrast to strong aircraft orders, vehicle orders will likely be weak. The expected pullback in vehicle orders is consistent with elevated inventories and lackluster production, retail and unit sales. Excluding transportation, the three-month annual rate posted a strong reading in February, suggesting upside risks in the coming months.

Previous: 1.8% Wells Fargo: 1.1% Consensus: 1.5%

First Quarter GDP • Friday

Consistent with the last three first quarter advanced readings, real GDP is expected to register a sub-trend pace of growth. Much of the slower pace will be concentrated in consumer spending due largely to one-off factors like milder-than-usual weather in January and February, which cut utility use and tax refund delays. That said, control-group sales, which exclude food, autos, building materials and gasoline sales, rose at a 4.1 percent three-month annual rate in March suggesting still-solid underlying growth. International trade will also pull the headline lower as the earlier timing of the Chinese New Year led to a surge in imports in January. We also expect state and local government purchases to post a weak reading. On a positive note, business fixed investment should advance as the drag from the earlier collapse in oil prices continues to dissipate. Indeed, nondefense capital goods excluding aircraft shipments rose at an 8.8 percent three-month annual pace in February.

Previous: 2.1% Wells Fargo: 0.8% Consensus: 1.2%

Global Review

It's Official: The Global Economy Is Improving

- The latest IMF global forecast just confirmed what we have been observing for almost half a year: that the global economy was on the mend and that we expect an improvement in economic growth across the world. The IMF's forecast for this year is now 3.5 percent versus 3.1 percent for 2016.

- The Chinese economy grew at a 6.9 percent rate in the first quarter of the year, year over year, a tad higher than what markets were expecting and is the third consecutive improvement in a similar number of quarters.

It's Official: The Global Economy Is Improving

The latest IMF global forecast just confirmed what we have been observing for almost half a year: that the global economy was on the mend and that we expect an improvement in economic growth across the world. The IMF's forecast for this year is now 3.5 percent versus 3.1 percent for 2016.

Of course, this new growth spurt will likely not be similar to the ones we had during the first decade and a half of this century, but it will nevertheless help to lift almost all boats across the globe. Some of the first signs of this recovery have been evident for some time, and while there are still many, many threats that could jeopardize the current growth spurt, we remain confident that the global economy is on the right path.

Again, and even against lots of negative talk regarding trade, especially in the United States, trade is what is actually leading the growth charge across the global economy. And China, while not acting as the behemoth that helped drive growth across the globe during the first decade and a half of this century, is showing that it can still contribute its share to the effort. Case in point was the release of first quarter GDP, which showed an economy growing at a slightly higher clip than what markets were expecting, up 6.9 percent versus market expectations of 6.8 percent. Not much different but it is the third slight improvement in growth in a similar number of quarters.

In our international section last week, we mentioned the strong performance by Chinese trade in March as well as the slight improvement in international reserves during the first quarter of the year and indicated that these were encouraging signs of economic growth solidifying across the world.

Even Brazil seems to have been doing better lately. The Brazilian monthly economic activity index in February posted the strongest month-over-month print, up 1.3 percent, since July 2014 when it grew 1.5 percent. On a year-earlier basis, the economy was still down 0.7 percent, but markets were expecting a decline of 2.3 percent. This release followed the central bank's decision last week to decrease the Selic, benchmark interest rate 100 bps, from 12.25 percent to 11.25 percent, while indicating that it would continue to lower interest rates aggressively during the next several months due to the strong disinflationary path for Brazilian inflation and inflationary expectations. Still, the political corruption situation in Brazil is a potential threat to the recovery in economic activity this year, but the fact that the economy is coming from such a low base will keep the good news coming and will help deliver low but positive growth in 2017.

In the U.K., Prime Minister Theresa May surprised markets with a call for early elections, a strategy that analysts expect to give her administration more power in the negotiations with the European Union on the terms of the U.K. exit from that union. Meanwhile, in Turkey, President Recep Tayyip Erdogan won a contested referendum to reform the country's constitution that many say will enhance his presidential powers and are calling it the beginnings of a dictatorship.

Global Outlook

ECB Policy Meeting • Thursday

The European Central Bank (ECB) holds a regularly scheduled policy meeting on Thursday, and there is very little chance that the Governing Council will change its three main policy rates. Some analysts look for the Governing Council to announce some changes to its quantitative easing program that would take effect in coming months. Although we suspect that the ECB will eventually begin to "taper" its monthly bond purchases, we do not believe that it is quite ready to announce such a step at this policy meeting.

There is also a fair amount of European economic data on the docket next week. In Germany, the Ifo index of business confidence in April is to print on Monday, while retail spending data for March could be released on Friday. The initial estimate of French GDP growth in the first quarter is on the docket on Friday as well. Italian data on business and consumer confidence are slated for release on Friday.

Previous Refi Rate: 0.00% Wells Fargo: 0.00% Consensus: 0.00%

Japan Industrial Production • Friday

The usual end-of-month data barrage in Japan is expected to occur next week, and the data for March should help analysts firm up their GDP growth estimates for the first quarter. The initial official estimate of Q1 GDP growth is to be released by the Japanese government on May 18.

Global economic activity has accelerated a bit in recent months, which has helped to boost Japanese exports and Japanese industrial production (IP). Indeed, Japanese IP is currently growing at its strongest rate since 2014. March data on retail spending, the labor market and CPI inflation will print as well next week. The Bank of Japan (BoJ) also holds a policy meeting next week. But with the current rate of CPI inflation barely above zero percent at present, there is little chance that the BoJ will dial back its degree of monetary accommodation anytime soon, let alone next week.

Previous: 3.2% (Month-over-Month) Consensus: -0.8%

U.K. GDP Growth • Friday

Real GDP growth in the United Kingdom has held up better in the wake of last June's Brexit referendum, better than most analysts, ourselves included, had expected. That said, recent monthly data suggest that the economy decelerated in the first quarter. The rise in inflation in recent months has eroded growth in real income, which has weighed on consumer spending. In that regard, real retail sales in the first quarter fell 1.6 percent on a sequential basis. However, positive growth in the consumption of services likely means that overall consumer spending growth probably continued to grow in the first quarter.

Survey data that are collected from retailers, which are slated for release on Thursday, will give analysts some insights into the state of British consumer spending in April. House price data for April may also print at the end of the week.

Previous: 0.7% (not annualized) Wells Fargo: 0.5% Consensus: 0.4%

Point of View

Interest Rate Watch

Rate Expectations Slip

Benchmark Treasury yields have trended lower since the FOMC's March meeting, while markets have pared back expectations for further rate increases this year.

The lower benchmark rates have followed softer readings of the economic data in recent weeks. First quarter GDP estimates, including our own, continue to track below one percent, while the March payrolls number and downward revisions point to a slowdown in hiring.

While the weak first quarter GDP estimate and March payroll print look to be more noise than signal in our view, more recent data on inflation have likely trimmed market expectations for rate increases since last week. Core CPI unexpectedly fell in March. The decline was mostly due to an unusually large drop in wireless telephone services that is unlikely to be repeated, but it resets the base for inflation and points to a more protracted return to the Fed's target. We expect the year-over-year pace of core PCE inflation to slow to 1.6 percent in March from 1.8 percent in February.

In addition to the latest inflation data hinting that the Fed has a bit more time on its side before raising rates, last week's comments from President Trump may also be weighing on rate expectations. Noting that he likes low rates (rather than critiquing the low-rate environment on the campaign trail), the FOMC looks less likely to suddenly turn hawkish regardless of who is at the helm next February.

Markets continue to put the odds of the FOMC raising rates again in June above 50/50. Whiles expectations fell as low 40 percent early this week, they have since rebounded back to around 60 percent. A stronger-than-expected reading on the index of leading economic indicators and reiteration from a number of Fed officials this week that multiple more rate hikes remain appropriate despite other soft data looks to have helped the turnaround. Still, markets are pricing in only about one more rate hike this year, suggesting FOMC members have more communicating to do before June if a rate hike remains in the offing this quarter.

Credit Market Insights

Beige Book: All Districts See Growth

The underlining tone of the Federal Reserve's recently released Beige Book was one of growth. All 12 Federal Reserve districts reported an increase in overall economic activity with growth in employment, wages and prices. But like with most things, the devil is in the details.

Across the nation, districts reported at least a moderate increase in employment between mid-February and the end of March along with wage growth. However, the tighter labor market is leading to an increase in businesses having trouble filling lower-skilled and higher-skilled positions in addition to higher labor costs and employee retention difficulties. That said, as businesses increase their workforce, we could see a pickup in wages.

In addition to modest wage growth, overall inflation rose modestly in most districts. Districts noted selling prices rising "only slightly" since the previous report. Higher prices weighed on consumers' non-auto retail spending, while warmer weather kept energy prices low. The warmer weather also pulled the home building season forward, which should increase inventory. Moreover, districts saw an increase in lending activity at financial institutions and credit quality remained strong.

The anecdotal information provided by the Fed banks indicates that despite March's slower employment growth, decline in inflation and adverse weather conditions, much of the nation continued to grow at a modest-to-moderate pace.

Topic of the Week

Fiscal Challenges Facing Policymakers

With the release of the Congressional Budget Office's (CBO) latest Long-Term Budget Outlook, the ongoing fiscal policy story of increasing federal deficits and a large and growing stock of federal debt continues.

The CBO projects that deficits are expected to rise from 2.9 percent of GDP today to 9.8 percent of GDP by 2047 if current law remains unchanged. The result of these increasing deficits is the debt-to-GDP ratio rising from 77 percent today to 150 percent of GDP by 2047 (top chart). The three largest categories of spending contributing to annual deficits are Social Security, Medicare and interest on government debt. In fact, by 2047, under current law, federal spending for people age 65 or older who receive benefits from Social Security, Medicare and Medicaid would account for about half of all federal noninterest spending, compared with roughly two-fifths today.

The CBO also presented various alternative scenarios, including one with $2 trillion in additional deficit spending and or/tax cuts over the next 10 years, very roughly the size of our current forecast for tax cuts. With a cumulative increase in the federal budget deficit over the next 10 years of $2 trillion, excluding interest and macroeconomic feedback effects, the net result would be an increase in federal debt to 202 percent of GDP by 2047 compared to 150 percent in the CBO's baseline estimates (bottom chart).

Against this backdrop, Congress and the new administration have ambitious plans to provide fiscal stimulus in the form of tax cuts and perhaps greater federal spending on defense and infrastructure projects. The unchecked costs of some programs in the years ahead create a very challenging environment for this generation of fiscal policymakers and private markets as well.

1st Round of French Elections, ECB & BoJ Meetings, Key Data in Focus

Next week's market movers

- In France, we have the 1st round of the French presidential election. Given that among the leading candidates there are two Eurosceptic, the outcome would have a significant impact in the markets.

- We expect the ECB to offer no changes and maintain a balanced tone, given officials' yield concerns and that the meeting takes place before the second round of the French election.

- We believe that the BoJ will leave policy unchanged, but may revise down its inflation forecasts.

- We also get key economic data from the US, the UK, Eurozone, Japan, and Australia.

On Sunday, we have the 1st round of the French presidential election, but the final outcome is unlikely to be sealed on that day. According to the opinion polls, there is no candidate gaining the absolute majority, so a second round between the two leading candidates is very likely to be held on the 7th of May.

A couple of weeks ago, the leading candidates were three: Emmanuel Macron, Marine Le Pen, and Francois Fillon. Nevertheless, following a strong performance in the TV debates, left-wing candidate Jean-Luc Melenchon enjoyed a stellar rise of support. His program displays a similar Eurosceptic stance to Le Pen's. He advocates for holding a "Frexit" referendum as well. Therefore, a run-off between him and Le Pen seems to be the biggest risk scenario for the financial world.

If something like that takes flesh and bones, we expect the euro to sink as investors will likely price in a much greater risk of European disintegration. A general risk-aversion mood is likely to dominate as well. Safe-havens like the yen are likely to benefit, while equity markets, especially European indices, could take the down road. The other side of the coin is a Macron - Fillon second round. In this case, the opposite market reaction may be observed, as this run-off combination may eliminate the risk for any "Frexit" referendum.

However, at the moment, polls suggest that the most likely outcome is for Macron and Le Pen to make it to the second round, with the former winning by a large margin. In general, Macron is seen as the winner against any other of the candidates. So if Macron makes it on Sunday, this could cause a market relief and the common currency may open Monday with a gap up. In the less likely scenario of him being kicked out, the only combination that could be seen as relatively pro risk is a Fillon - Le Pen run off, given that polls give the final victory to Fillon. In a Fillon - Melenchon race, Melenchon is preferred.

Of course, much will depend on who gets the first place in the aforementioned combinations, and by how much margin.

On Monday, we get Germany's Ifo survey for April. With no forecast available, we see the likelihood for both the current conditions and expectations indices to have risen further. We base our view on the ZEW survey for the month, which showed increased optimism in the German economy. What's more, PMI surveys showed that economic growth remained strong at the start of the second quarter, despite slightly weaker increases in both manufacturing output and services activity.

On Tuesday, the economic calendar is light, with no major events or indicators due to be released.

On Wednesday, Australia's CPI data for Q1 are coming out. Expectations are for both the headline and trimmed mean rates to have risen, with the headline print returning back within the RBA's inflation target range of 2-3%. When they last met, RBA policymakers highlighted the softness in labor market indicators, and that the recently announced supervisory measures with regards to lending could ease financial stability risks. As we already noted, this suggests to us that once these measures take effect, the Bank would be more flexible to cut rates again if needed without being concerned that its actions would amplify risks to the economy. Following the remarkable jobs report for March, released after that meeting, we don't think that the Bank will act at its upcoming gathering on the 2nd of May. A potential acceleration in both the headline and trimmed mean CPIs could decrease further the possibility for any action.

On Thursday, during the Asian morning, BoJ will announce its policy decision. At its latest gathering, the Bank left its expansionary monetary policy program unchanged and maintained a slightly optimistic assessment with regards to the Japanese economy. Since that meeting the nation's core CPI rate ticked up to +0.2% yoy from +0.1% yoy, but the forward-looking Tokyo core CPI rate slid deeper into the negative territory. The data suggest that the Bank may lower somewhat its inflation forecasts when it publishes its quarterly outlook report at its policy meeting next week. However, we don't believe that this will lead to additional stimulus. We don't expect a small revision in projected CPI to alter the BoJ's policy stance. We believe that the focus of the meeting will be once again on the Bank's assessment regarding the Japanese economy.

During the European day, the highlight will be the ECB policy decision, followed by a press conference from President Draghi. At its latest policy meeting, the Bank kept is monetary policy unchanged and in the statement accompanying the decision, it maintained its dovish forward guidance. However, Draghi's press conference had a more hawkish tilt, giving investors the idea that the days of aggressive ECB easing may be behind us. Draghi's remarks were followed by similar speeches from several ECB officials, adding more fuel to expectations that the era of ultra-loose monetary policy is approaching its final stages.

Nevertheless, on the 29th of March, a Reuters report came to appease all this euphoria and to drag investors back down to earth. The report noted that market participants over-interpreted the signals from the ECB's March policy meeting and revealed that ECB officials only wanted to communicate reduced risks and not a step towards a reduction in stimulus. In addition, it was noted that policymakers are now cautious of making any new changes to the April statement, and that they are worried of a potential surge in the bloc's government bond yields.

his suggests that we are unlikely to get any changes from this meeting, especially having in mind that it takes place before the second round of the French election, a political event that could add a risk premium to European bond yields, and consequently enhance the concerns of ECB policymakers with regards to a surge in yields. Therefore, we expect the ECB to maintain a balanced tone, at least until the outcome of the election is sealed.

On the indicators' front, we get Germany's preliminary CPI for April one day ahead of Eurozone's print. The forecast is for the nation's CPI to have accelerated to +1.9% yoy from +1.6% yoy in March, something that could raise speculation that the bloc's rate may also accelerate and meet its forecast of +1.8% yoy.

From the US, we get durable goods orders for March, but no forecast is available yet. Our own view is that the core figure may slow somewhat after rising 0.5% mom in February. We base our expectations on the nation's ISM manufacturing PMI for the month, where the New Orders sub-index slid somewhat.

On Friday, during the Asian morning, we get CPI data for March from Japan. In the absence of any forecast, we see the case for both the headline and core rates to have ticked down. We base our view on the nation's forward-looking Tokyo CPIs for the month, where both the headline and core rates slid further into the negative territory. Something like that combined with a potential downside revision in the Bank's inflation forecasts at Thursday's meeting, could eliminate any speculation left with regards to stimulus reduction, at least for coming months. We continue to expect the Bank to keep its ultra-loose QQE with yield-curve control framework unchanged in the foreseeable future.

During the European day, we get Eurozone's preliminary CPI data for April. The forecast is for the headline rate to have risen to 1.8% yoy from 1.5% yoy in March. The core rate is also expected to have risen to +0.9% yoy from +0.8% yoy. ECB officials have repeatedly noted that they prefer to look through improvements in the headline rate and instead focus on the core print. As such, accelerating core inflation is likely to be pleasant news for them. However, given that the ECB will have already concluded its April policy meeting just the day before, and that the next gathering is scheduled on the 8th of June, we prefer to wait for the preliminary inflation data for May, due out on the 31st of the month, before we arrive to any safe conclusions with regards to what the ECB may communicate when it meets next.

In the UK, we get the first estimate of Q1 GDP. In the absence of a forecast, we see the case for economic activity to have slowed from the robust +0.7 qoq in Q4. Our view is based on the notable slide in retail sales for March, the disappointing industrial production for January and February, and the weak performance in the nation's PMIs compared to that seen at the turn of the year. What's more, the NIESR estimate of UK GDP indicated that the economy grew by 0.5% qoq in the first quarter of 2017. A potential slowdown in GDP combined with the political uncertainty surrounding the nation's future are in line with the current BoE stance. Officials are likely to continue to look through any further upturn in inflation and instead focus on the need to keep policy on hold to support economic growth.

We get the first estimate of Q1 GDP from the US as well. No forecast is available, but the Atlanta Fed GDPNow model suggests a notable slowdown to +0.5% qoq SAAR from +2.1% qoq SAAR in the last quarter of 2016. Such a slowdown is also supported by the disappointing retail sales prints throughout the quarter. After a weaker-than-expected March jobs gain and a surprise monthly drop in consumer prices, the market has started having doubts with regards to whether the Fed will indeed proceed with the three hikes it penciled for the year. According to the Fed funds futures, the market is currently anticipating only 1.2 hikes this year, with the next one fully priced in for November. A weak growth rate could scale further back market expectations and perhaps push the next hike into 2018.

Further GBP Gains Unlikely Before Snap Election

- Falling US Rates Drive Down The Greenback - Arnaud Masset

- Rise In Geopolitical Risk - Peter Rosenstreich

- Sell JPY - Peter Rosenstreich

- Further GBP Gains Unlikely Before Snap Election - Arnaud Masset

Economics - Falling US Rates Drive Down The Greenback

In late March/early April, the US Dollar made a recovery attempt, with the Dollar index rising 2.50% from 98.86 to 101.34, against the backdrop of mounting nervousness about the upcoming French election and Brexit jitters. Those sharp gains were mostly due to a massive debasement of the Euro, which fell more than 3% to 1.0574, while the Japanese Yen was treading water between 110 and 112. Over that period, investors were less focused on developments in the US and particularly the failure of Donald Trump's reform agenda. Investors took their time to send the Dollar back to where it came from as the Dollar capitalised on its status as a safe haven in a troubled environment.

Nevertheless, in the last week of March the wind began to rotate as investors started to call into question the viability of the Trump reflation trade. The equity rally paused as the S&P 500 eased slightly above 2,320 points - down from 2,400 in early March - as traders switched from equity to bonds, sending US 10-year Treasury yields back to 2.20%, compared to 2.62% a month earlier. On the short-end of the curve, the debasement was more acute, with two-year Treasury yields sliding 20bps to 1.17%, as the market slowly realised that the Fed won't deliver three rate hikes this year.

More importantly, the Trump trade, which sent inflation expectations to the moon six months ago, has also started to unwind. Inflation expectations fell substantially since mid-March and dragged down US yields. The two-year breakeven inflation rate (approximation) slid at around 1.60% recently, while on the longer-term, inflation expectations remained stable, so far at least. We think it is just a matter of time before it starts to adjust to the downside as well. Inflation expectations 5y5y is still slightly above 1.90% compared to 1.50% in November last year.

All in all, we believe that is just the beginning and that this basic movement will continue, if not accelerate over the next few months. This re-pricing of inflation expectations will weigh substantially on the USD as treasury yields slid further. In the short-term, we would avoid playing this re-pricing against the Euro and the Pound as the political risk is still quite substantial. However, once the French elections are over, the Euro will be set free (should a pro-business candidate wins the French election). In the higher-yielding currency complex, we would favour long NZD position as speculators will continue to unwind their short positions.

Politics - Rise In Geopolitical Risk

After a long hiatus, geopolitical risk is back in investors' calculations. Geopolitical tensions remained the market focus giving safe haven currencies JPY and CHF a boost. It's likely after the French election results are in, geopolitical risk will continue to drive risk-taking. The US missile strike on Syria on 6th April and the largest non-nuclear bomb ever used in combat on 13th April in Afghanistan highlights President Trump's willingness to use military forces.

While in Asia, China has increased the rhetoric around North Korea's nuclear weapon development, which in turn is stressing warming China/ US relations. There is a current feeling that diplomatic responses may not be enough to lower the risk of further military actions. To emphases this, regarding dealing with North Korea, US Secretary of State Rex Tillerson stated: "Let me be very clear: the policy of strategic patience has ended." History indicates that unilateral missile strikes generally have an immediate negative effect on the markets but quickly recover nearly all loses within five days in most examples. Global stock market indices volatility generally remains elevated, while there is limited effect on gold, USD or bond yields.

In the case of a full blown regime change (executed by NATO in Iraq, Bosnia and Somalia), the stock markets response was mixed although on average there was a gain on the first day then further gains for the next week. Gold and oil prices generally fall after the first day. In Syria, we don't see escalations above localized missile strikes. The decision to strike a single target (this case an airbase) or Syrian surface to air missile sites indicates that the move was not in preparation for a larger campaign. Syrian President Bashar al-Assad was not targeted suggesting that the US was not intending to change the regime or risk provoking the Russians.

A military escalation on the Korean peninsulas would have deeper downside risk. First, N. Korea is military prepared for defensive retaliation (or even first strike). Any action against N. Korea should be considered a total regime change operation. Any action aimed at N. Korea will have profound negative repercussions on financial markets. Japan and South Korea economics account for around 8% of the global GDP (stock markets of South Korea, Japan and China would see negative shocks). The spillover of disruption economic activity into world growth will be real.

The path of least resistance generally defines the path of geopolitics. And despite the erratic behaviour of many of the individuals involved (Trump, Putin, Assad, Kim Jong-un). it's likely that a diplomatic strategy will continue. Already actions (offering for a better trade deal with the US or larger US military presence in the region) by the US have forced China to take a strong stance on N. Korea including new sanctions. While regional military conflict generally has a negative market impact, the mid-term view is that the impact is negligible.

We understand the headlines are scary and force investors to contemplate the unimaginable. However, investors are better served to follow the historical market impact norms and not overreact to geopolitical developments. As we have sated at the start of 2017, fundamentals remain the core driver of asset prices and this will continue barring an extreme event.

FX Market - Sell JPY

Developments in Europe support our short JPY call. We had anticipated a pullback in USD demand but that downwards correction in USDJPY has outpaced our expectations. We anticipate a recovery to resistance at 112.15. The JPY has been supported less by growing inflation expectations but rather weakening in global risk environment. JPY remains the dominant risk aversion trade above gold, USD and CHF (however, we are not seeing significant JPY buying on fluctuations in French polls).

Clearly, rising geopolitical worries have caused investors to rotate out of risky assets and into JPY. We suspect tensions have reached a peak and suspect that the historically customary path of diplomacy will takeover. IMM positioning indicates that the JPY is well overbought suggesting room for readjustments. This week's BoJ meeting will bring no meaningful adjustment to the current strategy as policy board members are likely to shift focus on personal changes rather than monetary policy. Last week the BoJ nominated two very dovish members showing support for aggressive balance sheet expansion to its committee.

For now, the realization is that the BoJ ¥80trn annual balance sheet expansion is unstable, leading to a switch to yields curve control that will dictate strategy. While the ECB inches towards tapering and the Fed contemplates the next 25 bp hike, the BoJ policy continues to be the loosest. This strategy should remain supportive of USDJPY. Yet, it is not the BoJ that will drive USDJPY higher but the reactions of the US economy and interest rate. The US economy seems to have slipped into a period of cyclical softness which should organically pick up in early summer. However, while investors have all but thrown the Trump-reflation trade away, there is still the probability that that the Trump administration gets a pro-growth win (tax reform remains the clearest).

Developments in Europe support our short JPY call. We had anticipated a pullback in USD demand but that downwards correction in USDJPY has outpaced our expectations. We anticipate a recovery to resistance at 112.15. The JPY has been supported less by growing inflation expectations but rather weakening in global risk environment. JPY remains the dominant risk aversion trade above gold, USD and CHF (however, we are not seeing significant JPY buying on fluctuations in French polls).

Economics - Further GBP Gains Unlikely Before Snap Election

Theresa May surprised markets last week as she seeks an early general election on June 8. Looking at GBP's price action, it seems that market participants were quite happy with this decision as the Pound rose more than 2% against the greenback, with GBP/USD hitting 1.2905 on Tuesday afternoon.

This sharp GBP appreciation amid the announcement suggests that PM May's decision is a good thing for the UK economy. We do not share this optimism as we believe it just increases the uncertainty, particularly in relation to the Brexit negotiations and the UK political landscape. Indeed, Theresa May has made a risky but necessary gamble by seeking a direct mandate. On the one hand, it gives her the opportunity to strengthen the Tory majority in the House of Commons, which would heighten her negotiation power in the upcoming Brexit negotiations. In addition, it gives her the opportunity to get rid of the 2015 Tory programme. But on the other hand, it gives a second chance to the British people to speak out about the Brexit referendum and also gives an opportunity to other parties to make a comeback. Therefore, we think that the market overly reacted to the announcement, as the only thing that has increased is the level uncertainty.

In the short-term though, we remain cautious on further Pound gains as investors will act carefully ahead of the election (if it actually takes place). In the longer-term, a strengthening of Conservatives' position would definitely bolster the Pound as it will put the country in a better position to negotiate the terms of its divorce with the EU.

Existing Home Sales Surge in March as Tight Inventories Support Rapid Price Growth

Existing home sales rose by an impressive 4.4% m/m to 5.71 million (annualized) in March, marking a strong rebound from the month prior when sales activity advanced an at slightly downwardly-revised 5.47 million (annualized) pace. The headline print came in significantly higher than market expectations which called for a more moderate rebound to 5.60 million.

The gains were concentrated in the single family segment where transactions rose by 4.3% to 5.08 million. Sales in the smaller and more volatile condo/co-op segment rebounded by 5.0% to 630 thousand.

On a regional basis, sales activity improved across most regions, rising in the Northeast (10.1%), Midwest (9.2%) and South (3.4%), while activity continued to pull back in the West (-1.6%) which posted a second consecutive monthly decline. Still, the sales pace remained higher than year-ago levels across the board.

The number of homes available for sale rose 5.8% on the month but remained low at 1.83 million by historical standards, down 6.6% from year-ago and accounting for just 3.8 months' worth of supply at the current sales pace. The low inventory levels are keeping upward pressure on prices, with the median price advancing 6.8% y/y – a strong print despite a slight deceleration from the 7.6% pace in the prior month.

First time homebuyers accounted for 32% of sales, unchanged from the month prior and up 2pp from year-ago.

Key Implications

Existing home sales activity has been quite volatile since December. The uneven performance can be partly explained by the rapid rise in interest rates immediately following the election which likely swayed buyer behavior and brought forward some contract signing, while unseasonal weather likely also contributed to volatility in the last few reports. Still, seeing through the volatility, the trend is a positive one, with the strong rebound in March to a decade-high a welcome development.

The rise in inventory levels is a very welcome development which helped contribute to the better-than-expected print, but more is needed to sustain the current sales pace. In the near-term, sales activity will likely remain constrained by still-low inventory levels and fast-rising prices which continue to outstrip income growth.

The Fed is poised to hike rates twice more this year, and thrice next year, with long-term borrowing rates likely to increase accordingly. This will further weigh on affordability and could dent demand for homes somewhat. Still, the medium term outlook remains upbeat, as rising employment, wages, and incomes are expected to provide considerable offset.

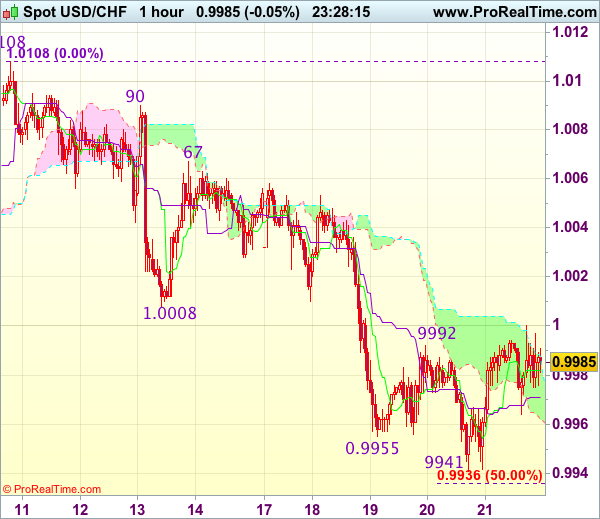

Trade Idea Wrap-up: USD/CHF – Stand aside

USD/CHF - 0.9988

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9982

Kijun-Sen level : 0.9971

Ichimoku cloud top : 1.0088

Ichimoku cloud bottom : 0.9962

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The greenback rebounded after holding above yesterday’s low at 0.9941, suggesting consolidation above this level would be seen and test of previous support at 1.0008 (now resistance) cannot be ruled out, however, break there is needed to signal low is formed and bring retracement of recent decline from 1.0108 to 10030 but resistance at 1.0067 should remain intact.

On the downside, below said support at 0.9941 would extend recent decline to 0.9935-38 (50% projection of 1.0067-0.9955 measuring from 0.9992) and then 0.9926 (61.8% Fibonacci retracement of 0.9813-1.0108) but reckon 0.9900-05 (1.618 times projection of 1.0108-1.0008 measuring from 1.0067) would hold, bring rebound later. As near term outlook is mixed, would be prudent to stand aside for now.

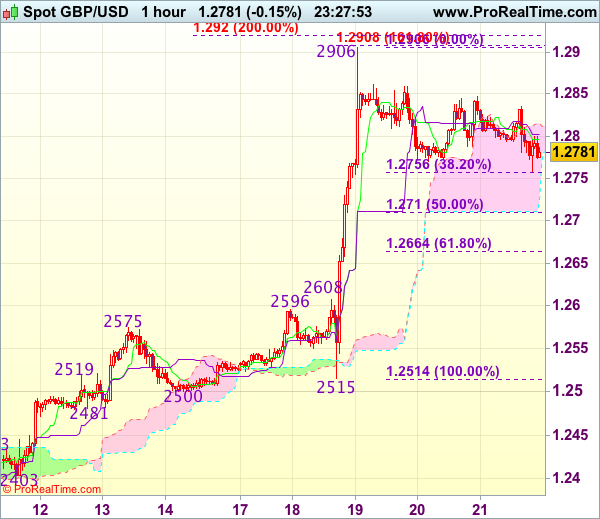

Trade Idea Wrap-up: GBP/USD – Buy at 1.2710

GBP/USD - 1.2770

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2796

Kijun-Sen level : 1.2802

Ichimoku cloud top : 1.2815

Ichimoku cloud bottom : 1.2725

Original strategy :

Buy at 1.2710, Target: 1.2850, Stop: 1.2675

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2710, Target: 1.2850, Stop: 1.2675

Position : -

Target : -

Stop : -

Cable has remained confined within familiar range and further sideways trading is in store, however, downside should be limited to 1.2755-60 (38.2% Fibonacci retracement of 1.2515-1.2906) and reckon 1.2700-10 would hold, bring another rally, break of 1.2755069 would signal the pullback from 1.2906 has ended, bring retest of this level, break there would extend recent upmove to 1.2920-30 (2 times extension of 1.2365-1.2575 measuring from 1.2500), then 1.2950 but loss of near term upward momentum should prevent sharp move beyond 1.2990-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance).

In view of this, would not chase this rise here and would be prudent to buy cable on subsequent pullback as downside should be limited to 1.2710 (50% Fibonacci retracement of 1.2515-1.2906), bring another rise. Below 1.2700 would defer and signal top has been formed, risk correction to 1.2660-65 (61.8% Fibonacci retracement of 1.2515-1.2906) and price should stay well above 1.2608-16 (previous resistance now support).

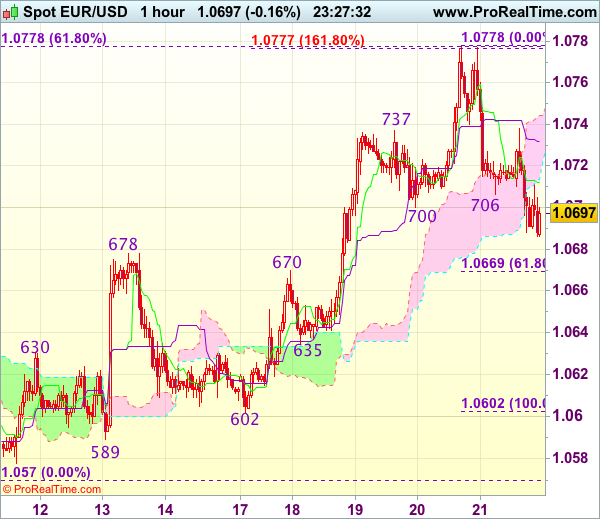

Trade Idea Wrap-up: EUR/USD – Hold long entered at 1.0690

EUR/USD - 1.0696

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0712

Kijun-Sen level : 1.0732

Ichimoku cloud top : 1.0744

Ichimoku cloud bottom : 1.0714

Original strategy :

Bought at 1.0690, Target: 1.0790, Stop: 1.0655

Position : - Long at 1.0690

Target : - 1.0790

Stop : - 1.0655

New strategy :

Hold long entered at 1.0690, Target: 1.0790, Stop: 1.0655

Position : - Long at 1.0690

Target : - 1.0790

Stop : - 1.0665

Euro’s retreat after rising to 1.0778 yesterday suggests a temporary top has been made there and consolidation with mild downside bias is seen for marginal weakness from here, however, reckon downside would be limited and bring another rise later to 1.0783-85 (61.8% projection of 1.0602-1.0737 measuring from 1.0700), then 1.0800-10 but loss of near term upward momentum should prevent sharp move beyond 1.0825-30, risk from there is seen for a retreat to take place later.

In view of this, we are holding on to our long position entered at 1.0690. Only below previous resistance at 1.0670 (now support) would abort and signal top is formed instead, bring correction towards previous support at 1.0635 which is likely to hold from here.

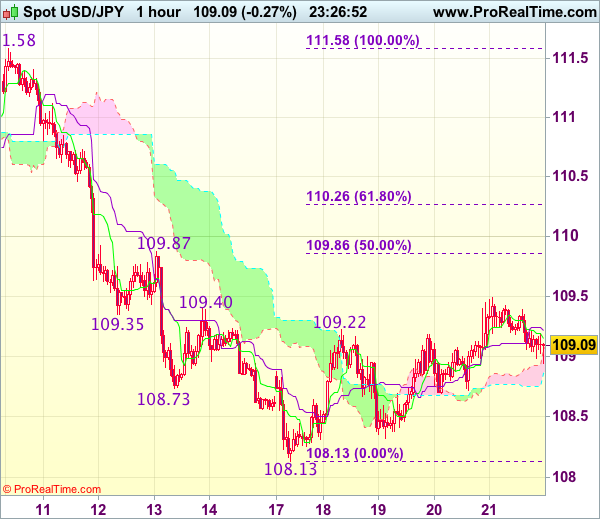

Trade Idea Wrap-up: USD/JPY – Stand aside

USD/JPY - 109.09

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 109.15

Kijun-Sen level : 109.22

Ichimoku cloud top : 109.05

Ichimoku cloud bottom : 108.86

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although yesterday’s anticipated rebound to 109.49 adds credence to our near term bullish view for the erratic rise from 108.13 to bring retracement of recent decline, reckon upside would be limited to 109.86-87 (50% Fibonacci retracement of 111.58-108.13 and previous resistance), however, price should falter below 110.25-30 (61.8% Fibonacci retracement) and bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 108.65-70 would suggest top is formed, bring weakness to 108.30-32, break there would signal the rebound from 108.13 has ended, bring retest of this level first.

Trade Idea: EUR/GBP – Sell at 0.8475

EUR/GBP - 0.8357

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Sell at 0.8475, Target: 0.8325, Stop: 0.8515

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.8475, Target: 0.8325, Stop: 0.8515

Position : -

Target : -

Stop : -

Euro’s rebound after dropping to 0.8312 earlier this week suggests consolidation above this level would be seen and retracement to 0.8440-50 cannot be ruled out, however, reckon 0.8475-80 would limit upside and bring another decline, below 0.8335-40 would bring retest of said support at 0.8312 but break there is needed to signal recent decline from 0.8788 is still in progress and may extend further weakness to 0.8300, then towards 0.8275-80.

In view of this, would not chase this fall here and would be prudent to sell euro on subsequent recovery as 0.8475-80 should limit upside. Only above previous resistance at 0.8512 would abort and signal a temporary low is formed instead, risk a stronger rebound to 0.8545-50 but resistance at 0.8580 should remain intact.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.