Sample Category Title

Trade Idea Update: GBP/USD – Sell at 1.2475

GBP/USD - 1.2433

Original strategy :

Sell at 1.2475, Target: 1.2375, Stop: 1.2510

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.2475, Target: 1.2375, Stop: 1.2510

Position : -

Target : -

Stop : -

Cable’s rebound after finding good support around 1.2365-66 has retained our view that further consolidation above this level would be seen and gain to 1.2445-50 cannot be ruled out, however, reckon 1.2475-80 would limit upside and bring another decline later, below said support at 1.2365-66 would extend recent decline from 1.2616 to 1.2350, then towards 1.2325-30 but oversold condition should limit downside and reckon 1.2300 would hold from here.

In view of this, would not chase this fall here and would be prudent to sell cable on further subsequent recovery as 1.2475-80 should limit upside. Only break of resistance at 1.2506 would abort and signal low is formed, bring a stronger rebound to 1.2525-30 first.

Trade Idea Update: EUR/USD – Sell at 1.0665

EUR/USD - 1.0613

Original strategy :

Sell at 1.0665, Target: 1.0565, Stop: 1.0700

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0665, Target: 1.0565, Stop: 1.0700

Position : -

Target : -

Stop : -

As the single currency has continued trading defensively after recent selloff, suggesting recent decline may resume after consolidation, although corrective bounce to 1.0625-35 cannot be ruled out, however, reckon upside would be limited to 1.0667 resistance (Friday’s high) and bring another decline later, below support at 1.0570 would extend the decline from 1.0906 to 1.0550-55 (50% projection of 1.0906-1.0635 measuring from 1.0689), then 1.0525-30 but near term oversold condition should prevent sharp fall below 1.0500, risk from there is seen for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on further recovery as 1.0667 resistance should limit upside. Only a firm break above said resistance at 1.0667 would abort and suggest low is formed instead, risk a stronger rebound to 1.0689, then 1.0702.

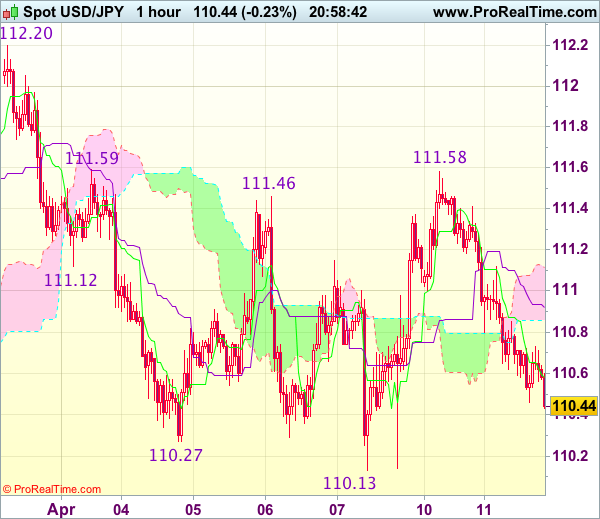

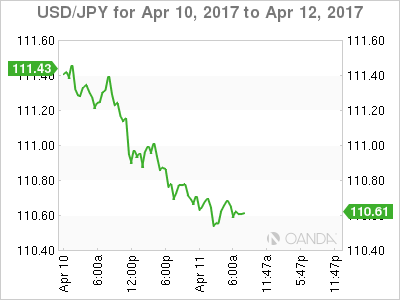

Trade Idea Update: USD/JPY – Hold long entered at 110.60

USD/JPY - 110.43

Original strategy :

Bought at 110.60, Target: 111.60, Stop: 110.25

Position : - Long at 110.60

Target : - 111.60

Stop : - 110.25

New strategy :

Hold long entered at 110.60, Target: 111.60, Stop: 110.25

Position : - Long at 110.60

Target : - 111.60

Stop : - 110.25

Although dollar has remained under pressure after retreating sharp from yesterday’s high of 111.58 and marginal weakness from here cannot be ruled out, reckon 110.25-30 would contain downside and bring another rebound later, above 111.10-15 would suggest the retreat from 111.58 has ended, bring test of 111.58-59 resistance, break there would add credence to our view that further consolidation above recent low at 110.11 would be seen and signal the fall from 112.20 has ended, then a stronger rebound to 111.90-00 would follow but said resistance at 112.20 should hold and choppy trading within 110.11-112.20 would continue.

In view of this, we are holding on to our long position entered at 110.60 but one should exit on such rebound. Below 110.25-30 would risk test of said support at 110.11-13 but only break there would confirm medium term decline has resumed for further subsequent fall to 109.80-85 (1.618 times projection of 112.20-111.12 measuring from 111.59), however, price should hold above 109.50-55 (100% projection of 112.20-110.27 measuring from 111.46).

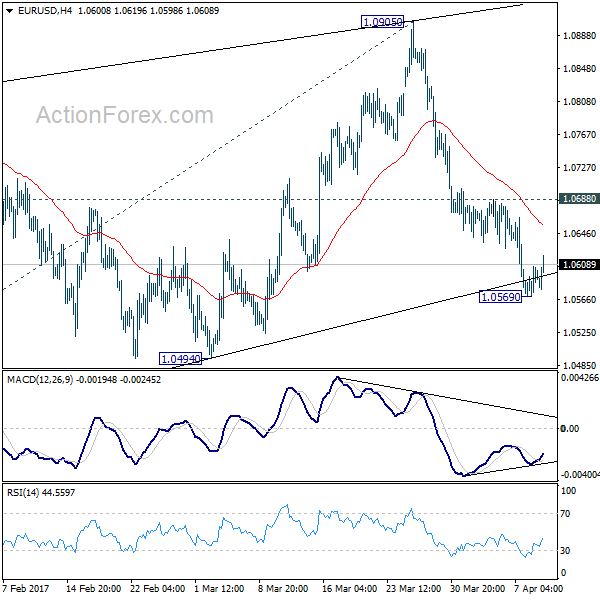

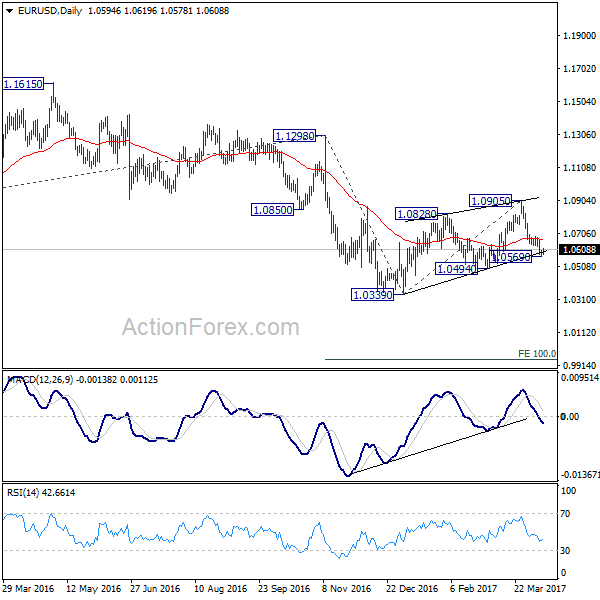

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0574; (P) 1.0590 (R1) 1.0611; More....

A temporary low is in place at 1.0569 as EUR/USD recovers. Intraday bias is turned neutral first. But we'd expect upside of recovery to be limited by 1.0688 resistance and bring fall resumption. As noted before, corrective rise from 1.0339 is likely finished after being rejected by 55 week EMA. And, the larger down trend is ready to resume. Below 1.0569 will turn bias to the downside for 1.0494 support first. Break will confirm this bearish case and send EUR/USD through 1.0339 to 100% projection of 1.1298 to 1.0339 from 1.0905 at 0.9946. On the upside, however, break of 1.0688 resistance will delay the bearish case and turn focus back to 1.0905 resistance instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Euro Recovers by German ZEW, Dollar Softens on Uninspiring Fed Yellen

Euro recovers today as lifted by German investor sentiment data. Meanwhile, Dollar softens broadly after uninspiring comments from Fed chair Janet Yellen. German ZEW economic sentiment rose to 19.5 in April, up from 12.8, beat expectation of 14.8. That's also the highest level since August 2015. Current situation assessment rose to 80.1, up from 77.3, beat expectation of 80.1. ZEW President Achim Wambach said that the "German economic situation has proved fairly robust in the first quarter" And, that was highlighted by "solid figures for growth in industrial production, the construction sector and retail sales from February." Also, "consistently high labour demand has boosted private consumption." Eurozone ZEW economic sentiment rose to 26.3, up from 25.6, beat expectation of 25.0. Also from Eurozone, industrial production dropped -0.3% mom in February versus expectation of 0.1% mom rise.

Yesterday, ECB President Mario Draghi said in the central bank's annual report that 2016 "ended with the economy on its firmest footing since the crisis," even though the year began "shrouded in economic uncertainty". The report noted that the scaling back of asset purchase from EUR 80b per month to EUR 60b "reflected the success of our actions earlier in the year: growing confidence in the euro area economy and disappearing deflation risks". However, overall, the Eurozone economy's recovery is still dependent on massive support from the central bank. And the report also reiterated the calls on governments' effort on fiscal reforms.

UK CPI unchanged at 2.3% yoy

UK CPI was unchanged at 2.3% yoy in March in line with expectation. Core CPI, however, dropped to 1.8% yoy, down from 2.0% yoy and missed expectation of 1.9% yoy. RPI also slowed to 3.1% yoy, down from 3.2% yoy. Headline inflation stayed inside BoE's target rate of 2-3%. Risk to headline inflation should remain on the upside as BoE projects CPI to peak at 2.75% next year. Governor Mark Carney made himself clear that he is willing to tolerate overshooting the target as UK prepares for Brexit. But this view is not shared by all MPC members. Kristin Forbes voted for a rate hike back in March meeting. But for now, at least, inflation outlook is not worsening and Sterling softens a touch against Euro today. PPI input rose 0.4% mom, 17.9% yoy. PPI Output rose 0.4% mom, 3.6% yoy. PPI output core rose 0.3% mom, 2.5% yoy. House price index rose 5.8% yoy in February. BRC retail sales monitor dropped -1.0% yoy in March

Uninspiring comments from Fed chair Yellen

Yellen's comments yesterday were uninspiring. On the job market, the Fed chair indicated that unemployment is now "a bit below" full employment. the March employment report suggested that the unemployment rate surprisingly fell to a post-recession low of 4.5% from 4.7% in February. The participation stayed unchanged at 63%. The number of nonfarm payrolls increased 98K in March, missing expectations of 180K and the downwardly revised 219K in February. On inflation, Yellen noted that it remained "slightly below" the 2% target. With the Fed's focus now turned to sustaining economic growth, Yellen reiterated that "a gradual path of increases in short-term interest rates can get us to where we need to be, but we don't want to wait too long to have that happen".

On a separate note, St. Louis Fed president James Bullard, speaking in Australia, signaled he favored only one rate hike this year, compared with three as suggested in the Fed's median dot plot. Rather, he urged to begin balance sheet reduction this year. As the St. Louis Fed president noted, there is not "much further to go on rates and therefore the next step that would be natural would be to allow the run-off of the balance sheet".

Australia business conditions improved, confidence dropped

Australia NAB business confidence rose 5 pts to 14 in March, hitting the highest level since the global financial crisis. But business confidence dropped 1 pt to 6. NAB noted that "the bounce in business conditions this month came as a bit of a surprise, especially the big improvement in Queensland in light of the likely disruptions from Cyclone Debbie in late March." And, "one possibility is that 'Debbie' is having the unexpected effect of overstating conditions in March given that the cyclone coincided with a lower response rate from firms in Northern Queensland.". But overall, "conditions have improved almost across the board to levels that suggest a strong economy in the near term."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0574; (P) 1.0590 (R1) 1.0611; More....

A temporary low is in place at 1.0569 as EUR/USD recovers. Intraday bias is turned neutral first. But we'd expect upside of recovery to be limited by 1.0688 resistance and bring fall resumption. As noted before, corrective rise from 1.0339 is likely finished after being rejected by 55 week EMA. And, the larger down trend is ready to resume. Below 1.0569 will turn bias to the downside for 1.0494 support first. Break will confirm this bearish case and send EUR/USD through 1.0339 to 100% projection of 1.1298 to 1.0339 from 1.0905 at 0.9946. On the upside, however, break of 1.0688 resistance will delay the bearish case and turn focus back to 1.0905 resistance instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y Mar | -1.00% | -0.50% | -0.40% | |

| 1:30 | AUD | NAB Business Confidence Mar | 6 | 7 | ||

| 6:00 | JPY | Machine Tool Orders Y/Y Mar P | 22.60% | 9.10% | ||

| 8:30 | GBP | CPI M/M Mar | 0.40% | 0.30% | 0.70% | |

| 8:30 | GBP | CPI Y/Y Mar | 2.30% | 2.30% | 2.30% | |

| 8:30 | GBP | Core CPI Y/Y Mar | 1.80% | 1.90% | 2.00% | |

| 8:30 | GBP | RPI M/M Mar | 0.30% | 0.40% | 1.10% | |

| 8:30 | GBP | RPI Y/Y Mar | 3.10% | 3.20% | 3.20% | |

| 8:30 | GBP | PPI Input M/M Mar | 0.40% | -0.10% | -0.40% | -0.10% |

| 8:30 | GBP | PPI Input Y/Y Mar | 17.90% | 17.00% | 19.10% | 19.40% |

| 8:30 | GBP | PPI Output M/M Mar | 0.40% | 0.10% | 0.20% | |

| 8:30 | GBP | PPI Output Y/Y Mar | 3.60% | 3.40% | 3.70% | |

| 8:30 | GBP | PPI Output Core M/M Mar | 0.30% | 0.20% | 0.00% | |

| 8:30 | GBP | PPI Output Core Y/Y Mar | 2.50% | 2.50% | 2.40% | |

| 8:30 | GBP | House Price Index Y/Y Feb | 5.80% | 6.10% | 6.20% | |

| 9:00 | EUR | Eurozone Industrial Production M/M Feb | -0.30% | 0.10% | 0.90% | |

| 9:00 | EUR | German ZEW (Economic Sentiment) Apr | 19.5 | 14.8 | 12.8 | |

| 9:00 | EUR | German ZEW (Current Situation) Apr | 80.1 | 77.5 | 77.3 | |

| 9:00 | EUR | Eurozone ZEW (Economic Sentiment) Apr | 26.3 | 25 | 25.6 |

GBPUSD: Hesitates But Retains Short Term Downside Pressure

GBPUSD: With the pair retaining its downside pressure, more weakness is likely. This view remains valid despite its price hesitation. Support lies at the 1.2350 level where a break will turn attention to the 1.2300 level. Further down, support lies at the 1.2250 level. Below here will set the stage for more weakness towards the 1.2200 level. Conversely, resistance stands at the 1.2450 levels with a turn above here allowing more strength to build up towards the 1.2500 level. Further out, resistance resides at the 1.2550 level followed by the 1.2600 level. On the whole, GBPUSD continues to face downside pressure short term.

British Pound Volatile as UK CPI Holds Steady

Sterling was volatile on Tuesday, with prices oscillating between losses and gains after markets digested the UK's steady 2.3% inflation figure for March, which was the highest level since September 2013. The ongoing currency weakness created by Brexit, coupled with rising oil prices has elevated inflation above the Bank of England's 2% target, with speculation mounting over CPI following its positive trajectory this quarter. Although the immediate market reaction to March's headline CPI reading was noticeably bullish, gains may be relinquished when participants start to re-evaluate the impact it may have on the UK economy. With inflation still above average earning there is a threat of consumer spending taking a hit, which could spark concerns over the longevity of the UK's consumer-fuelled economic growth.

Focusing on the technical outlook, Sterling remains gripped by Brexit woes, with prices pressured on the daily charts. The candlesticks are trading below the daily 20 Simple Moving Averages, while the MACD is in the early stages of crossing to the downside. Weakness below 1.2400 could be the first signs of a steeper decline, with a breakdown below 1.2370 opening a path towards 1.2300.

Euro pressured by political uncertainty

The growing unease and anxiety ahead of the French presidential elections in a few weeks have exposed the Euro to downside risks. Recent polls showing a four-way battle in claiming the French presidency, with Emmanuel Macron and Marine Le Pen on track to winning the first round, have created jitters. With the growing threat of Eurosceptic parties destabilizing the Eurozone's unity weighing heavily on sentiment, the Euro may be in store for further punishment. From a technical standpoint, the EURUSD is bearish on the daily charts. Prices are trading below the daily 20 SMA, while the MACD has crossed to the downside. Weakness below 1.0600 could encourage a further decline lower towards 1.0500.

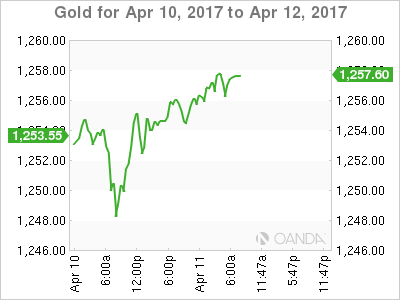

Global stocks subdued by geopolitical tensions

The horrible combination of geopolitical risks and political uncertainty has soured appetite for riskier assets, with investors sprinting to safe-haven investments. Global stocks were vulnerable to losses during trading on Tuesday amid the heightened geopolitical tensions, with the lack of appetite for riskier assets pressuring Asian and European markets. The bearish contagion from Europe could contaminate Wall Street this afternoon, consequently limiting gains as investors turn to Gold for safety.

Commodity spotlight - WTI Oil

WTI Crude was elevated to a fresh five-week high at $53.20 during trading on Tuesday, after the shutdown at Libya's largest oilfield over the weekend eased some oversupply fears. The geopolitical uncertainty in Syria sparked further speculations of a threat to supply complimented the upsurge in oil prices. Although the incredible rebound in oil has somewhat turned prices bullish on the daily charts, the lingering oversupply concerns may cap upside gains in the medium to longer term. From a technical standpoint, for the upside to continue towards $55, a solid breakout and daily close above $53 will be needed.

EUR/USD Bulls Broke 1.0600 Psychological Level

EUR/USD has turned bearish since March 28, as a result of the strengthening of the dollar. It has plunged almost 2% from March 28 to April 10.

However, EUR/USD has rebounded since Monday April 10, after hitting a 1-month low of 1.0568.

This morning, we saw the release of a series of German and Eurozone economic data.

The German ZEW economic sentiment and current situation (Apr), were 19.5 and 80.1 respectively, both surpassing expectations and the previous figures.

The Eurozone ZEW economic sentiment (Apr) was 26.3, better than expectations and the previous figure. The Eurozone industrial production (YoY) was 1.2%, lower than expectations, however, better than the previous figure. Overall, the performance of the data was better than the previous figures.

This morning, the EUR/USD bulls broke the psychological resistance level at 1.0600 after the release of the data.

On the 4-hourly chart, the price has been moving from the lower band to the middle band by the Bollinger Band indicator, suggesting the bearish momentum has waned.

The daily Stochastic Oscillator is around 20, suggesting a rebound.

The resistance level is at 1.0620, followed by 1.0640 and 1.0655.

The support line is at 1.0600, followed by 1.0585 and 1.0570.

Keep an eye on the German CPI (Mar), to be released on Thursday April 13, at 07:00 BST, as well as the US retail sales, to be released on Friday at 13:30 BST. It will likely affect the strength of EUR/USD.

Political Saber Rattling Supports Safe Haven Demand

Tuesday April 11: Five things the markets are talking about

North Korea's saber rattling combined with Russia's role in Syria is spooking investors.

Global stocks are on the back foot; the yen has strengthened along with U.S Treasuries on investor caution about geopolitical risks and the path of U.S interest rates.

In North Korea, Kim Jong has vowed the "toughest" counteraction against President Trump's response to dispatching a U.S naval destroyer to the region over the weekend. While in Syria, there is talk that Russia knew more about Assad's intentions than originally thought.

The question is when, not if? After Friday's weaker-than-expected non-farm payroll (NFP) print, investors are also speculating on the path for U.S interest rates. The Fed is aiming to ease back significantly this year on the level of support the central bank is providing the U.S economy as they close in on their goals of full employment and their +2% inflation target.

Note: Volumes across the various asset classes are down in a week that's shortened in many countries by Easter holidays.

1. Global stocks see red on investor uncertainty

In Japan, the Nikkei fell overnight (-0.3%), as rising geopolitical tensions in the region, a stronger yen (¥110.65) and renewed uncertainty in the French presidential election continues to spook investor sentiment. The broader Topix fell -0.3%, after a two-day advance.

The regional anomaly was in Australia where the S&P/ASX 200 gained +0.3% as energy shares advanced. In South Korea, the Kospi fell -0.4% and extended its selloff to a sixth consecutive session.

In Hong Kong, the Hang Seng lost -0.8% and the Hang Seng China Enterprises Index slid -1.2% amid concern that China may ramp up oversight of financial markets.

Note: The gauge of Chinese shares traded in Hong Kong has dropped -4.8% from its 17-month high reached in March.

In Europe, equity indices are trading generally lower despite the FTSE 100 outperforming and trading positive. Financial stocks are weighing heavily in the major indices.

U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx50 -0.4% at 3,471, FTSE +0.4% at 7,375, DAX -0.2% at 12,181, CAC-40 -0.1% at 5,105, IBEX-35 -0.4% at 10,400, FTSE MIB -0.4% at 20,121, SMI flat at 8,617, S&P 500 Futures -0.1%

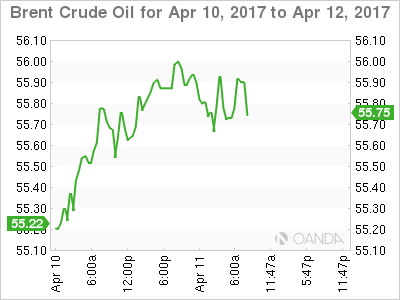

2. Crude oil prices ease on U.S shale production

Oil prices have eased away from their five-week high overnight, as rising U.S shale oil production offsets investor concerns over geopolitical tensions in the Middle East and OPEC output cuts.

Note: Current price levels current prices have attracted shale oil producers in the past.

Brent crude futures are down -20c, or -0.36% from Monday's close at +$55.78 per barrel, while U.S West Texas Intermediate (WTI) have given up -15c, or -0.3%, to +$52.93 a barrel.

In oil supply fundamentals, the global market remains oversupplied, even with efforts led by the OPEC to cut supplies to support global prices.

Brent has risen in each of the previous six sessions, while WTI has gained for the last five-days. U.S data also shows that crude inventories have touched record highs in Cushing, Oklahoma (storage hub), and in the U.S Gulf Coast in recent weeks.

Nervous investors are turning to the safety of gold. Prices (+0.2% to +$1,257.22 an ounce) remain buoyed by the yellow metal's safe-haven status amid rising political tensions over North Korea, Middle East and the upcoming French presidential election.

3. Fixed income enjoys safe haven status

Aside from the safe haven status that U.S Treasury's hold, bond yields have added to their declines in the overnight session after the Fed Chair Janet Yellen confirmed yesterday that the central bank has shifted its focus to "sustaining economic gains from post-crisis healing." Ms. Yellen indicated that its appropriate to gradually raise Fed Funds rate as the U.S economy was now "pretty healthy." Their estimate of "neutral rate was really not that high." The Fed is now trying to "give it some gas, but not so much that we're pushing down hard on the accelerator."

Treasuries have rallied, with the yield on the 10-year note dropping -4 bps to +2.33%, after a -2 bps decline yesterday.

Elsewhere, uncertainty surrounding the French presidential election on April 23 continues to drive investors to sell French government bonds (OAT's) and migrate cash into German government bonds and U.S Treasury debt. The yield on French 10's has backed up to +0.947%, while 10-year Bunds trade atop of their technically critical level of +0.2%.

Down-under, Aussie 10-year yields fell -4 bps to +2.53%.

4. Euro trades nervous on French election

This morning, with a number of Euro-inflation reports coming in below expectations supports the ECB to maintain loose monetary conditions. This has led to EUR cross selling as the predominant FX theme ahead of the U.S open.

The upcoming French election has the single unit (€1.0597) under pressure. Even EUR/JPY (€117.32) is softer as Japan-based entities hold around +12% of all outstanding French sovereign bonds.

Note: A gauge of how much investors are willing to pay to shield them against a sharp move in the EUR hit levels not seen since the height of the eurozone sovereign debt crisis this morning.

Elsewhere, the pound (£1.2436) has edged a tad higher towards the psychological £1.2450 area after U.K Mar CPI inflation (+2.3%) remained above the BoE's +2% target for second consecutive month. This may prompt market talk of the BoE looking to raise interest rates.

5. German Economic Sentiment Beats Forecasts in April

Data this morning showed that German economic sentiment has improved sharply in April, possibly pointing to a pickup in economic growth in the months ahead.

Germany's ZEW headline print for economic expectations rose to 19.5 points from 12.8 points in March - this is the highest level since August 2015.

Note: The ZEW survey signals ongoing optimism among financial analysts and institutional investors.

Fed Chair Janet Yellen Sees Calm Waters ahead

- Yellen sees calm waters ahead

- UK retail sales drop as inflation bites

Comments from Federal Reserve Chair, Janet Yellen, shortly after the US close, failed to move the USD to any great degree. Mrs Yellen sees the US economy growing at or around the Federal Reserve's target level and wants to move slowly on rate hikes to ensure sustainable growth and stable inflation. There is a noticeable lack of US data today, so the Dollar is likely to tread water.

British Retail Consortium sales data overnight reflected a 1.0 percent decline in March, but Sterling was sanguine ahead of this morning's barrage of UK data; giving the Pound scope to strengthen from its flat trading position of the last few days. UK inflation has remained at a stable figure of 2.3 percent, boosting Sterling. The Consumer Prices Index posted a 2.3% 12-month inflation rate in March 2017, showing no change from February.

The annual rate of producer price inflation slowed somewhat for March 2017, with output prices rising to 3.6%, from 3.7% in February 2017, the showing price growth for the ninth year in a row.

The cost of materials and fuels used by UK manufacturers went up 17.9% on the year, a slight drop from February 2017; again, this the ninth consecutive period of annual price growth.

Prices of imported materials and fuels increased 17.1%, growth in inflation for the second month in a row. However, a recent boost for export prices thanks to a weak Pound increased export turnover for motor vehicle manufacturers.

The Sterling-Euro rate was a tad higher overnight, ahead of the UK data. In Europe, we get the Eurozone Industrial Production today, and the German ZEW data showed continue confidence in the German economy, as the ZEW Institute's Economic Sentiment Index posted at 19.5 in April 2017, considerably higher than 12.8 last month, and also beating the 14 that was forecast. This was the highest level for almost two years. In contrast, some of the Eurozone industrial production figures were lower than expected, dropping 0.3 percent in February 2017 - after an increase of 0.3 percent in January 2017 - and a 4.7 percent drop in energy output. A recovery in the Euro's strength is therefore looking unlikely.

It's a short and sweet report today, with few items of real note, but the Donald & Vladimir show could create all sorts of volatility, so hold onto your hats!

Joke

A boy is asked to question a war veteran about their experiences as a project. He finds out that his uncle served in the Falklands War, so he sits down and starts asking him questions about the war, what it was about, what the result was and then he said, "Uncle Joe, did you kill anyone?"

His uncle sighed and said, "Probably. I was a chef, you see."