Sample Category Title

Sterling: No Firm Direction after Inflation Data

Headlines

European stock markets managed to recover most of the opening losses as risk aversion from Asian trading didn't persist. US stock markets open with small losses as US investors seem to be more afraid about the US' tougher stance against Syria and North-Korea.

British inflation held steady in March due to the later timing of this year's Easter holidays which pushed down airfares, and a dip in global oil prices, but the squeeze on households looks set to resume soon. Consumer prices increased in March by 2.3% Y/Y while core CPI declined from 2% Y/Y to 1.8% Y/Y.

EMU industrial output declined in February (-0.3% M/M), against market expectations of a slight increase (0.1% M/M), largely due a sharp drop of energy production. German ZEW-investor confidence rose more than anticipated in April, as Europe's largest economy continues to gather momentum. The forward looking expectations component also increased further, beating consensus.

US NFIB small business optimism eased off multi-year highs in March, marginally declining in line with expectations from 105.3 to 104.7.

North Korea is "looking for trouble" and the US is prepared to act unilaterally on the issue, with or without China's support, US President Trump said, as the new administration solidifies its much tougher stance on the Asian country.

US Secretary of State Tillerson said it is clear the regime of President Bashar al-Assad in Syria "is coming to an end" and issued a stern warning to Russia as he headed to Moscow for high-level talks on the crisis. The secretary of state also said that "Russia has failed in its commitment to guarantee a Syria free of chemical weapons."

Rates

Technical losses for Bund, but US investors cautious

German Bunds underperformed US Treasuries today. Risk aversion pushed US Treasuries higher during Asian dealings. The Bund opened stronger as well with an immediate test of key support in the German 10-yr yield (0.2%; lower bound 0.2%-0.5% trading range). The test failed, sending German yields higher and Bunds lower. The move's technical importance could be similar to Friday's failed test of key US yields (5y: 1.8% and 10y: 2.3%) if confirmed. European equities managed to recover most of the opening losses and weighed on Bunds as well. Eco data were mixed with disappointing (outdated) industrial production, but a positive surprise from the more important German ZEW investor sentiment. The headline reading hit its highest level in April since the euro crisis, while the forward looking component suggests that strong Q1 growth momentum expands into Q2. The only item on the US eco calendar was NFIB small business optimism, which declined as forecast from 105.3 to 104.7 in March. US Treasuries managed to hold on to most of the overnight gains despite the Bund's downward bias in European trading. Rising geopolitical tensions (Syria, North Korea) still linger in the background of investors' minds (see headlines). As the US trading session gets going, core bonds gain momentum as risk sentiment hits a snag. US stocks deepen losses after the opening and USD/JPY is heading to 110.10 support.

At the time of writing, the German yield curve shifts 0.4 bps lower (2-yr) to 0.7 bps (10-yr) higher. Changes on the US yield curve vary between -3.5 bps (10-yr) and -2.4 bps (2-yr). On intra EMU-bond markets, 10-yr yield spread changes versus Germany widen up to 3 bps (Italy; supply-related) with Greece marginally outperforming (-3 bps).

The Austrian Treasury launched a new 10-yr benchmark via syndication (Apr2027). The bond was priced to yield MS -18 bps, compared to MS -17 bps area guidance. Final books closed in excess of €7.5B, allowing the Treasury to print €4.5B. The Dutch debt agency tapped the on the run DSL (€0.95B 2.5% Jan2033). The amount sold was in the lower half of the €0.75-1.25B on offer, but that's not unusual for Dutch auctions. Tonight, the US Treasury continues its refinancing with a $20B 10-yr Note auction. Currently, the WI trades around 2.34%.

Currencies

Dollar loses ground

The dollar lost ground across the board today. During European trading, EUR/USD recorded the biggest move as the US/EU spread differential narrowed. EUR/USD increased from 1.0580 to an intraday high of 1.0620. The German 10-yr yield bounced off key support (0.2%), pulling the German curve higher. A strong German ZEW investor sentiment might have played a role as well. EMU industrial production (disappointing) and US NFIB small business optimism (spot on consensus) didn't affect trading. Yesterday's French bond/stock underperformance (on rising support for extreme-left candidate Mélenchon) didn't persist and thus didn't weigh on the single currency.

In the US trading session, USD/JPY took over command. Comments by US secretary of state Tillerson (on Russia/Syria) and by US president Trump (on North Korea) confirmed the US' recent tougher stance, stressing geopolitical tensions and creating some new risk aversion. USD/JPY slid from levels around 110.70 to 110.20 currently and is gearing up for a new test of key 110.10 support.

The trade-weighted dollar dropped from 101.10 to 100.80 today, erasing the final post-payrolls gains.

Sterling: No firm direction after inflation data

Overnight, the BRC like for like sales disappointed as they dropped 1% Y/Y while a 0.3% M/M decline was expected. It's a further sign that consumer spending is losing momentum. However, it didn't impact sterling as investors clearly waited for the important inflation data. At their previous policy meeting, the BoE (MPC) showed they saw little room to let inflation move much higher without tightening policy. However, their concerns proved premature as inflation behaved well in March. The headline CPI was stable and in line with expectations at 2.3% Y/Y, while core CPI eased even slightly more than expected to 1.8% Y/Y from 2% Y/Y previously. Input and output PPI eased in March compared to February, even if they surpassed expectations and remain at a fairly high levels. Only core output PPI was a tad higher. There was a knee-jerk reaction pushing sterling stronger versus euro and dollar. However, the absence of follow through sterling buying caught the eye of sterling bulls and bears. Gains were in no time erased. EUR/GBP currently trades around 0.8540, versus the 0.8535 opening. Cable is marginally higher at 1.2434 versus 1.2415 at the open, the modest rise of EUR/USD being the trigger. EMU data were mixed (see dollar section) and the NFIB small business confidence was in line with expectations. Concluding, a session to rapidly forget

GBP/JPY Bullish Wolfe Wave at ATR Pivot

The GBP/JPY has been dropping as suggested in my previous article but at this point it has formed a bullish Wolfe Wave structure straight at ATR pivot point. Boosted by better than expected CPI, the GBP has made a slight recovery but for further upside it needs to break 138.50 with a steady upside momentum. The final target is 138.30 as 1-4 Wolfe Wave target will hardly be reached today (139,80). However, since this Wolfe Wave is not strict as point 3 is below point 1 it might be invalidated. Invalidation will come at the break of double bottom at 137.10. If this happens next target is 136.82 followed by 136.53.

Elliott Wave Analysis: USDCAD Eyeing 1.3180 Region

USDCAD has turned nicely down from 1.3533, clearly with five waves which is a structure of a bearish turn based on the Elliott Wave principle. As such, we now expect even more weakness after recently unfolded three wave bounce from 1.3262 that is pointing lower into wave three. We think that 1.3262 is going to be broken this week from where market may see a drop to 1.3180 short-term objective.

USDCAD, 4H

UK Consumer Spending to be Reined in for Short Term as Inflation Remains on the Up

UK Inflation rose 2.3 percent in March 2017. Although this is unchanged from the rate of growth seen in February, this figure is still above the Bank of England's (BoE) target of 2 percent. As rising cost pressures across the UK economy take their toll, it appears only a matter of time before this figure rises further. All eyes are now on the BoE and whether they will amend interest rates in response.

Ricky Nelson, Head of Corporate Dealing at currency specialists, Halo Financial, commented, "UK Inflation increased 2.3% in March. Although this represents no change from February's figures, food and clothing prices increased sharply, adding to the burden faced by hard-pressed consumers."

"Inflation began to rise following the UK Referendum vote to leave the European Union, which was the catalyst for the rapid fall in the value of the Pound. With inflation now increasing at similar levels to wages, it would suggest that consumer spending will have to be reined in for the short term."

Trade Idea: EUR/GBP – Sell at 0.8620

EUR/GBP - 0.8535

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Sell at 0.8620, Target: 0.8520, Stop: 0.8660

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.8620, Target: 0.8520, Stop: 0.8660

Position : -

Target : -

Stop : -

The single currency has remained confined within near term established range and further sideways trading is in store, however, euro needs to break 0.8500-10 to retain bearishness and signal the rebound from 0.8485 has ended at 0.8592, bring retest of 0.8485, break there would add credence to our view that top has been formed at 0.8788 and bearishness remains for this fall from there to bring retracement of early upmove, hence further weakness to 0.8470 would be seen but oversold condition should prevent sharp fall below 0.8450.

If said support at 0.8500-10 continues to hold, then further choppy trading would take place and risk of another bounce to 0.8592 cannot be ruled out but upside would be limited to 0.8620-25, bring another decline later. In view of this, we are looking to sell euro on subsequent recovery as 0.8620-25 should limit upside. Only above 0.8660-65 would defer and suggest low is possibly formed, risk rebound to 0.8680, then 0.8700 but price should falter below said resistance at 0.8735, bring further choppy trading later.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Stand aside

USD/CAD - 1.3315

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

New strategy :

Stand aside

Position: -

Target: -

Stop:-

As the greenback has remained under pressure after meeting renewed selling interest at 1.3427, initial downside bias remains for test of 1.3277 support, however, a break below this level is needed to signal another leg of decline from 1.3535 top is underway for test of 1.3264, below there would add credence to this view and extend weakness to 1.3235-40 (61.8% Fibonacci retracement of 1.3056-1.3535) and then 1.3200-10.

In view of this, would not chase this fall here and would be prudent to stand aside for now. Above 1.3380-85 would bring test of 1.3430-35 but break there is needed to revive bullishness and bring retest of 1.3456 resistance, break there would add credence to our view that the correction from 1.3535 has ended and bring further gain to 1.3495-00 but break there is needed to signal upmove has resumed for retest of 1.3535, once this level is penetrated, this would extend recent recent upmove from 1.2969 to 1.3575-80 but previous chart resistance at 1.3599 should hold on first testing.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

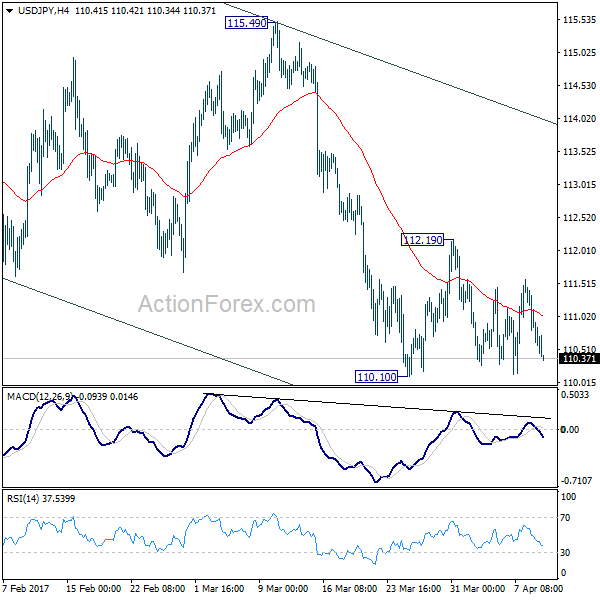

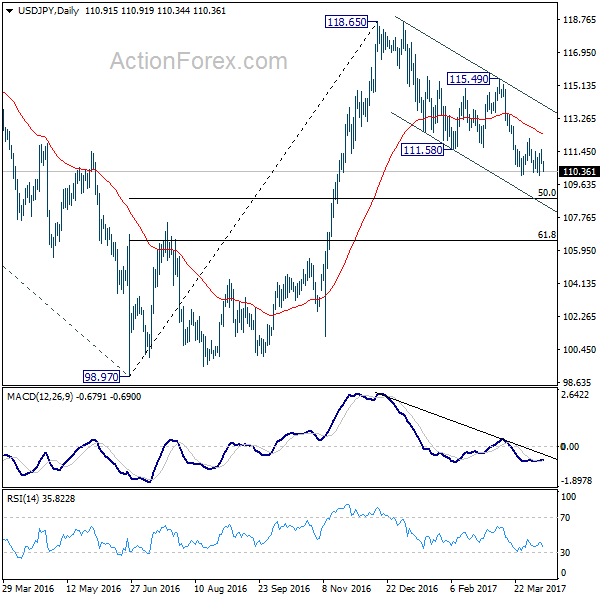

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.62; (P) 111.10; (R1) 111.40; More....

Intraday bias in USD/JPY remains as range trading continues in 110.10/112.19. The pair is staying in the near term falling channel and the correction from 118.65 could extend lower. Below 110.10 will turn intraday bias to the downside for 50% retracement of 98.97 to 118.65 at 108.81. On the upside, however, break of 112.19 resistance will indicate short term reversal and turn bias back to the upside for 115.49 resistance.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.15) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

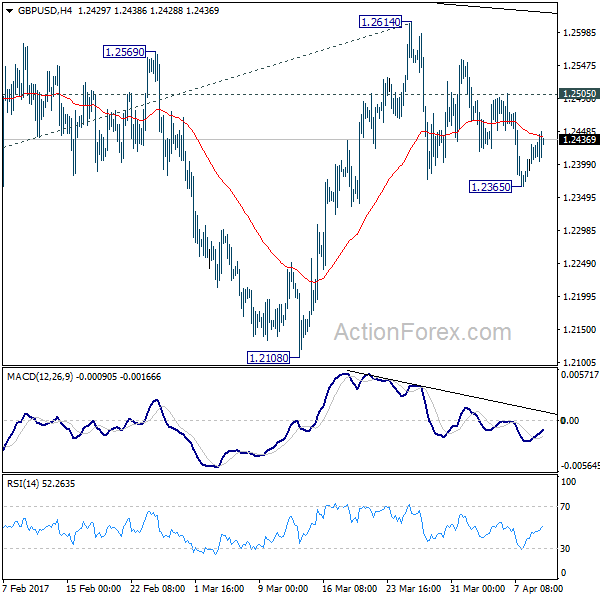

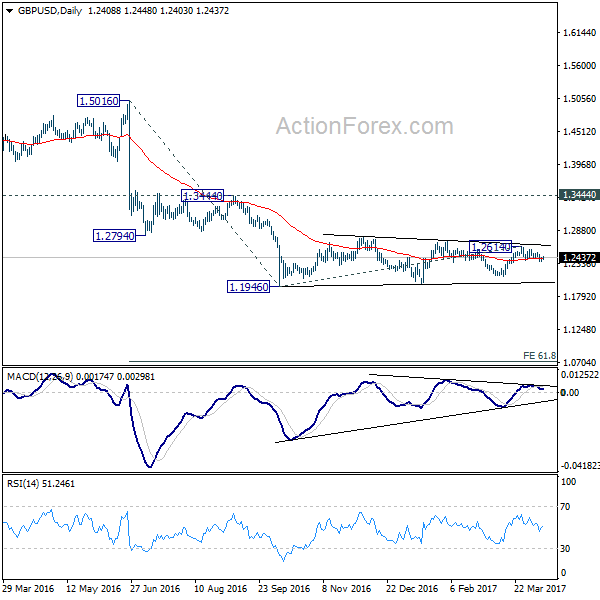

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2377; (P) 1.2402; (R1) 1.2441; More...

Intraday bias in GBP/USD is turned neutral with current recovery. But deeper decline is still expected with 1.2505 resistance intact. As noted before, triangle pattern from 1.1946 could be finished with five waves to 1.2614. Below 1.2365 will target 1.2108 support first. Decisive break there will argue that medium term down trend is resuming. In that case, GBP/USD should take out 1.1946/1986 support zone to 61.8% projection of 1.5016 to 1.1946 from 1.2614 at 1.0717. On the upside, however, break of 1.2505 resistance will invalidate this immediately bearish case. Then, it will turn bias back to the upside for 1.2614 resistance instead.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

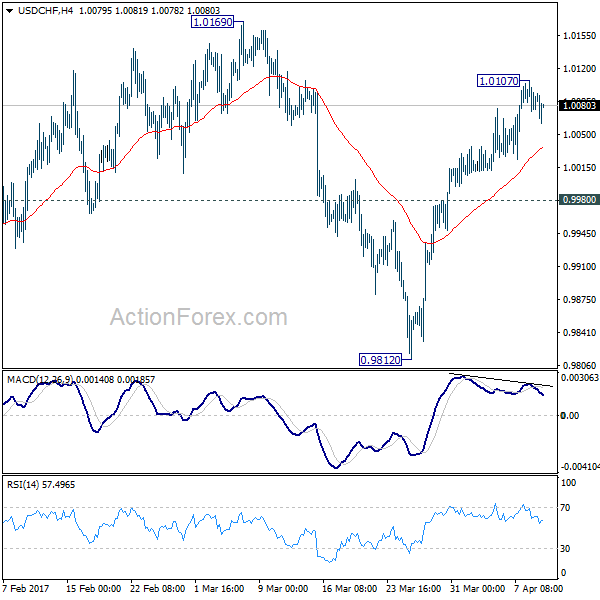

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0071; (P) 1.0089; (R1) 1.0104; More.....

A temporary top is in place at 1.0107 as USD/CHF retreats. Intraday bias is turned neutral for consolidation. Outlook is unchanged that corrective fall from 1.0342 should have finished with three waves down to 0.9812. Hence, downside of retreat should be contained by 0.9980 support and bring rally resumption. Above 1.0107 will target 1.0169 resistance. Decisive break there will confirm this bullish case and target 1.0342 key resistance next. However, below 0.9980 will dampen this bullish case and turn bias back to the downside for 0.9812 low.

In the bigger picture, we're still maintain that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the cross. However, the corrective nature of the fall from 1.0342 to 0.9812 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

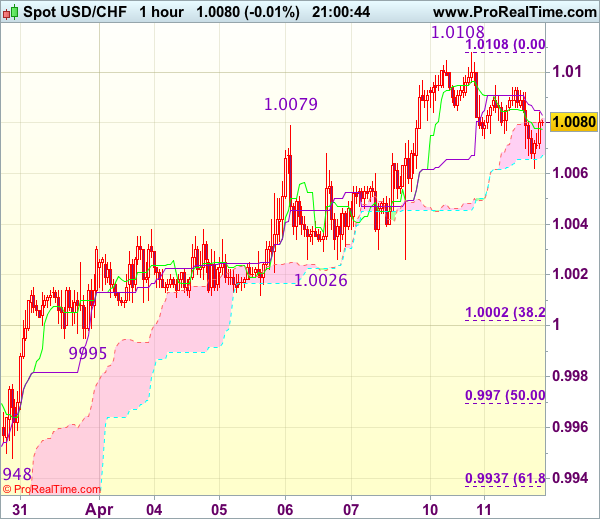

Trade Idea Update: USD/CHF – Buy at 1.0000

USD/CHF - 1.0080

Original strategy :

Buy at 1.0000, Target: 1.0100, Stop: 0.9965

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0000, Target: 1.0100, Stop: 0.9965

Position : -

Target : -

Stop : -

As the greenback has retreated after rising to 1.0108 yesterday, suggesting consolidation below this level would be seen and initial downside risk is for pullback to 1.0050, then towards support at 1.0026, however, reckon 0.9995 support would contain weakness and bring another rise later, above indicated resistance at 1.0108-09 would extend recent upmove from 0.9813 towards 1.0140-45 but loss of upward momentum should prevent sharp move beyond another previous resistance at 1.0171, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent pullback as support at 0.9995 should limit downside. Below 0.9970 (50% Fibonacci retracement of 0.9831-1.0108) would abort and signal top is formed instead, bring correction to support at 0.9948.