Sample Category Title

USD/CHF Finding Demand, USD/CAD Sharp Rejection, AUD/USD Pause In Bearish Pressure.

USD/CHF Finding demand.

USD/CHF is consolidating below new high at 1.0107. Hourly support is given at 1.0039 (07/04/2017 base low) then 0.9814 (27/03/2017 low). Key resistance can be found at a distance at 1.0171 (07/03/2017) then 1.0344 (15/12/2016 high). Expected to show another leg higher.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Sharp rejection.

USD/CAD short-term bullish technical pattern has quickly reversed, indicating further downside pressure. Key support is given at 1.3265 (21/03/2016 low) is in focus then 1.2969 (31/01/2017 low). Resistance can be located at 1.3427 (10/04/2017 high) then 1.3456 (04/04/2017 range high).

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Pause in bearish pressure.

AUD/USD bounce near the support has thus far unimpressive failed to find momentum, confirming persistent selling pressures. Next meaningful support is located at 0.7449 (13/01/2017 low). Resistance can be located at 0.7515 (intraday high and downtrend channel top).

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Bearish Pause, GBP/USD Marginal Bounce, USD/JPY Turning Downwards Within Range.

EUR/USD Bearish pause.

EUR/USD is boucing after breaking support implied by short term base. Hourly support can be found at 1.0570 (intraday low). Stronger support can be found at 1.0494 (22/02/2017 low). Resistance can be located at a distant 1.0658 (07/07/2017 reaction high). Expected to see further short-term weakness.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Marginal bounce.

GBP/USD remains weak despite bounce near the support at 1.2334, indicating persistent selling pressures. Hourly resistance is located at 1.2469 (07/04/2017 high).

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Turning downwards within range.

USD/JPY is trading sideways below resistance at 112.20 (31/03/2017 high) and 110.11 support. Stronger resistance can be located at 113.57 (16/03/2017 high) while support is given at 110.11 (27/03/2017 low).

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

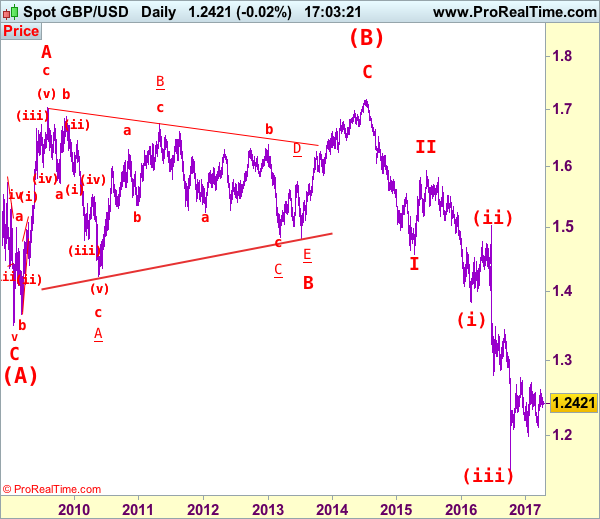

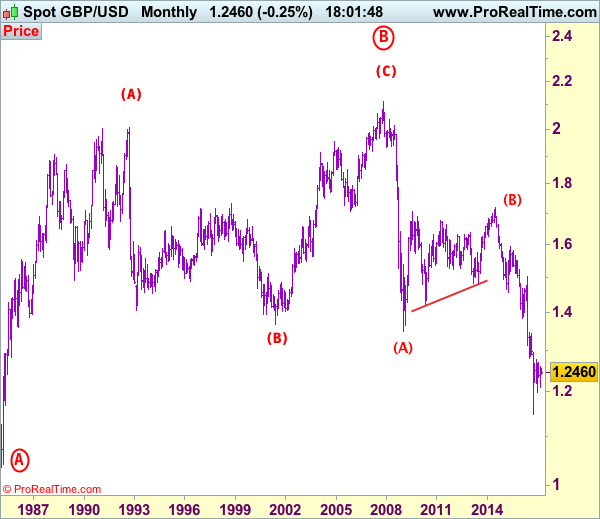

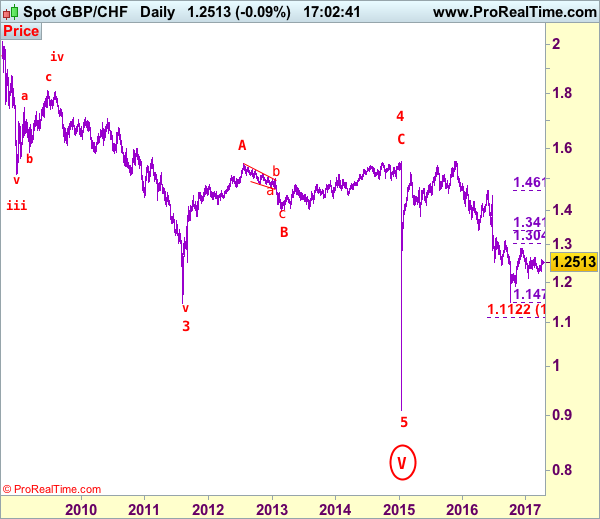

GBP/USD Elliott Wave Analysis

GBP/USD – 1.2418

GBP/USD – Wave 4 is unfolding as an (A)-(B)-(C) and could have ended at 1.7192

Although cable slipped again last week and near term downside risk remains for the erratic fall from last month’s high of 1.2616 to bring retracement of the rise from 1.2109, reckon downside would be limited to support at 1.2335 and bring another rebound later, above 1.2505-10 would bring test of resistance at 1.2559, break there would signal the retreat from 1.2616 has ended, bring retest of this level, break there would extend the rebound from 1.2109 to previous resistance at 1.2706 but break there is needed to signal another leg of corrective upmove from 1.1986 low is underway for further gain to 1.2800 and then 1.2900, having said that, psychological resistance at 1.3000 would remain intact.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has possibly ended at 1.7192, below support at 1.4232 would add credence to this count, then further fall to 1.4000 level would follow but reckon downside would be limited to 1.3655 support and price should stay above previous support at 1.3500.

On the downside, whilst initial pullback to 1.2360-65 cannot be ruled out, reckon downside would be limited to 1.2335 support and bring another rise later. A daily close below support at 1.2335 would dampen this bullish view and bring weakness to 1.2290-00 but reckon 1.2240-50 would hold, bring another rebound. A drop below 1.2240-50 would suggest the rebound from 1.2109 has ended instead, bring further fall to 1.2200 and then 1.2150-60 but said support at 1.2109 should remain intact.

Recommendation: Buy at 1.2335 for 1.2550 with stop above 1.2235.

Longer term - Cable's rise from 1.0520 (Feb 1985) to 2.0100 (September 1992) is seen as [A], the decline to 1.3682 is labeled as (B) and (C) wave rally has ended at 2.1162 (9 Nov, 2007) which is also the top of larger degree wave B with circle. The selloff from there is a 5-waver with wave (A) ended at 1.3500 (23 Jan 2009), wave (B) itself is labeled as A: 1.6733, triangle wave B: 1.4813 and wave C as well as top of wave (B) ended at 1.7192 (2014), hence the selloff from there is an impulsive wave (C) with wave I : 1.4566, wave II 1.5930, an extended wave III is unfolding and already exceeded our downside target at 1.3500 and 1.3000, hence weakness to 1.2500 and possibly 1.2000 cannot be ruled out, however, price should stay well above psychological level at 1.0000.

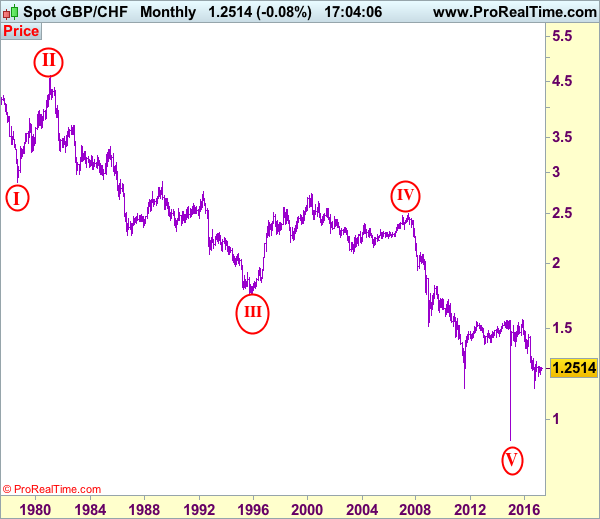

GBP/CHF Elliott Wave Analysis

GBP/CHF – 1.2507

GBP/CHF – Circle wave v ended at 0.9106 and major correction has commenced for subsequent gain to 1.5547.

As sterling found decent demand at 1.2285 and has staged a stronger-than-expected rebound, dampening our bearishness and suggesting the fall from 1.2660 has ended at 1.2215 last month, hence upside risk is seen for test of resistance at 1.2596 (last month’s high) but reckon said resistance at 1.2660 would hold from here, bring further choppy trading within early established range. Only a break of 1.2660 would shift risk back to the upside for the rebound from 1.2102 to extend further gain to 1.2745-55, above there would signal the retreat from 1.2915 has ended at 1.2102 and encourage for subsequent rise to 1.2800-10 first.

To recap the larger degree count, the selloff from 2.4965 (July 2007) is the beginning of wave V with circle and is labeled as 1: 2.3760, 2: 2.4425, wave 3 extension ended at 1.1470, followed by wave 4 at 1.5547, the quick rebound from 0.9106 suggests wave 5 as well as entire circle wave V could have ended there, hence consolidation with mild upside bias is seen for major correction to take place, bring initial test of 1.5547 (previous 4th of a lesser degree).

On the downside, whilst initial pullback to 1.2460-65 cannot be ruled out, reckon support at 1.2440-45 would limit downside and bring another rise later. Below 1.2355-60 would defer and risk test of said support at 1.2285 but only break there would revive bearishness and suggest the rebound from 1.2215 has ended instead, bring retest of this support first. A break of 1.2215 would signal the erratic fall from 1.2915 has resumed and extend weakness to previous support at 1.2102 which is likely to hold on first testing. Looking ahead, only a break below this level would extend the fall from 1.2915 to 1.2000-10 and later towards previous support at 1.1962 but reckon key support at 1.1899 would contain downside.

Recommendation: Stand aside for this week.

On the Monthly chart, the longer-term count is that major downtrend is under way with circle wave I at 2.8645 (Sep 1.978), then wave II with circle at 4.6175 (Feb 1981), the wave III with circle ended at 1.7425 (Nov 1995) and followed by wave IV with circle at 2.4965 (July 2007 with a short wave C) and wave V with circle has possibly ended at 0.9106. A monthly close above 1.5547 would add credence to this view, bring major correction to 1.7000, then towards psychological level at 2.0000.

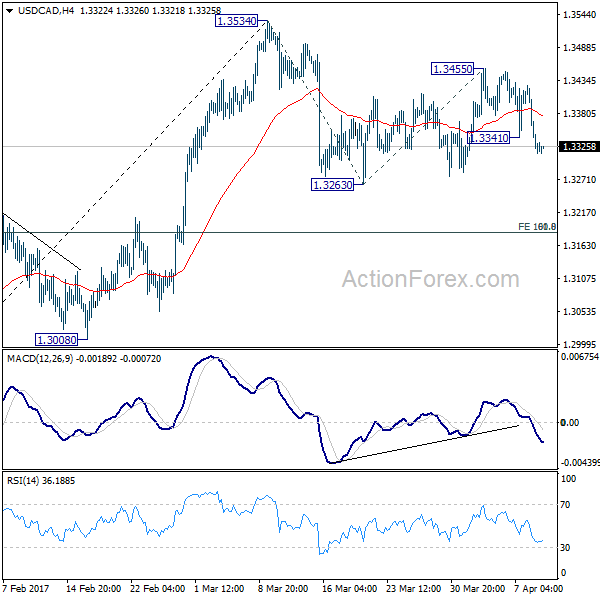

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3290; (P) 1.3357; (R1) 1.3393; More....

Intraday bias in USD/CAD is back on the downside after taking out 1.3341 minor support. Correction fall from 1.3534 is resuming for 1.3263 and below. In that case, we'd expect strong support from 1.3184 cluster level (61.8% retracement of 1.2968 to 1.3534 at 1.3184, 100% projection of 1.3534 to 1.3263 from 1.3455 at 1.3814 too) to contain downside and bring rebound. On the upside, break of 1.3455 will turn bias back to the upside for 1.3534 resistance.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. However, break of 1.2968 will argue that the third leg has already started and should at least bring a retest of 1.2460 low. Meanwhile, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

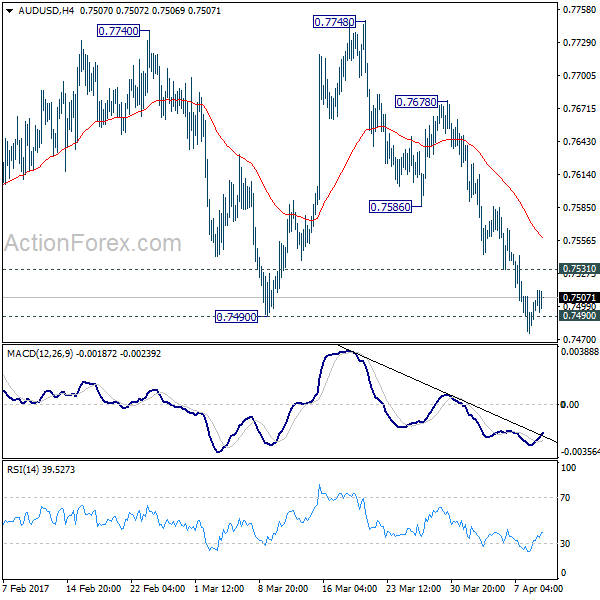

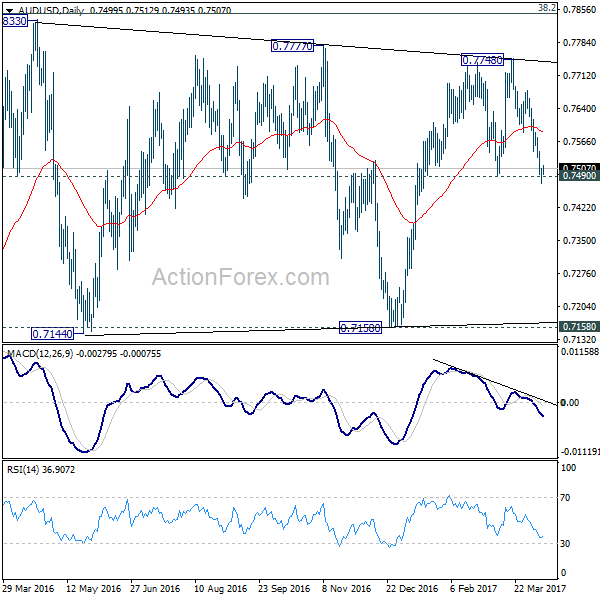

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7483; (P) 0.7495; (R1) 0.7515; More...

Intraday bias stays on the downside with 0.7531 minor resistance intact. Rise from 0.7158 is already completed at 0.7748. And, near term trend has reversed. Deeper fall should be seen back to support zone next. On the upside, above 0.7351 minor resistance will turn bias neutral and bring recovery. But upside should be limited by 0.7586 support turned resistance to bring fall resumption.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8142) and above.

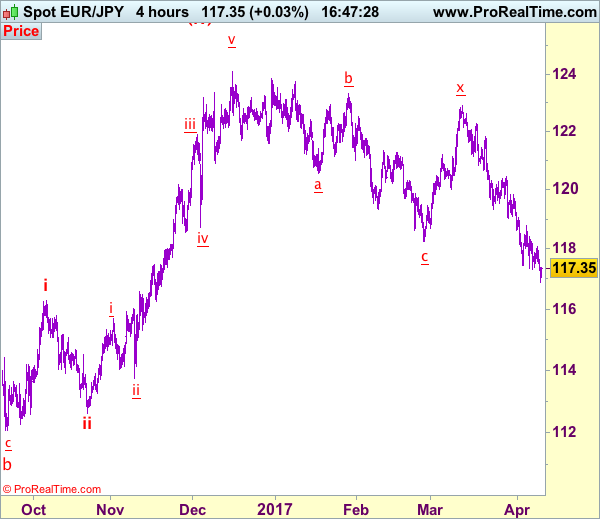

Trade Idea: EUR/JPY – Sell at 119.00

EUR/JPY - 117.35

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term down

Original strategy:

Sell at 119.00, Target: 117.00, Stop: 119.60

Position: -

Target: -

Stop: -

New strategy :

Sell at 119.00, Target: 117.00, Stop: 119.60

Position: -

Target: -

Stop:-

Although the single currency has remained under pressure, loss of near term downward momentum should prevent sharp fall below 116.50-60 and risk has increased for a rebound later, above 118.05-10 would bring recovery to 118.40-45 but upside should be limited to 118.90-00 and bring another decline later, bearishness is seen for recent erratic decline from 124.10 top (2016 high) to extend weakness to 116.50-60 but oversold condition should prevent sharp fall below 116.15-20 and reckon 116.00 would hold from here.

In view of this, would not chase this fall here and would be prudent to sell euro on subsequent rebound as 118.90-00 should limit upside. Above 119.06 resistance would defer and suggest a temporary low is possibly formed, risk rebound to 119.40-50 but price should falter below resistance at 119.85, bring another selloff.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Trade Idea: AUD/USD – Hold long entered at 0.7525

AUD/USD – 0.7509

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term down

Original strategy :

Bought at 0.7525, Target: 0.7680, Stop: 0.7465

Position: - Long at 0.7525

Target: - 0.7680

Stop: - 0.7465

New strategy :

Hold long entered at 0.7525, Target: 0.7680, Stop: 0.7465

Position: - Long at 0.7525

Target: - 0.7680

Stop:- 0.7465

As aussie has remained week after recent selloff, marginal weakness from here cannot be ruled out, however, loss of near term downward momentum should prevent sharp fall from there and bring rebound later, above 0.7550 would bring test of indicated resistance at 0.7588, break there would suggest a temporary low is possibly formed, bring rebound to 0.7625-30 and later towards resistance at 0.7680-85.

In view of this, we are holding on to our long position entered at 0.7525. Below indicated support at 0.7465-70 would signal the fall from 0.7750 is still in progress for further weakness to 0.7450-55 (50% Fibonacci retracement of 0.7158-0.7750), however, oversold condition should limit downside to 0.7380-85 (61.8% Fibonacci retracement), risk from there is seen for a rebound later.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

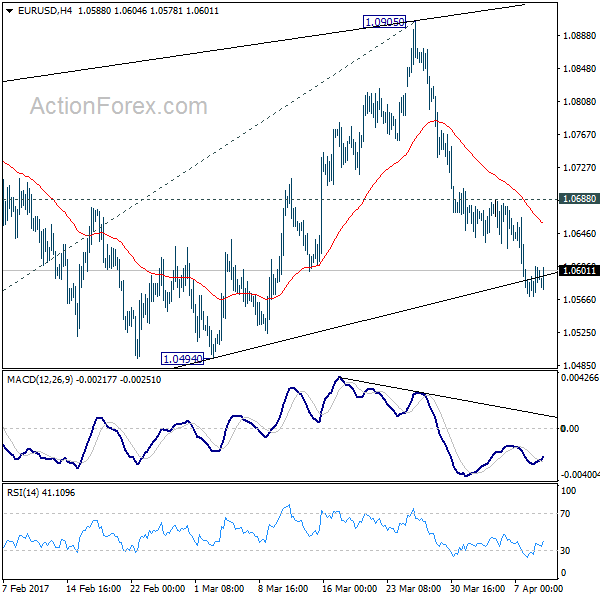

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0574; (P) 1.0590 (R1) 1.0611; More....

With 1.0688 resistance intact, deeper fall is still expected in EUR/USD to 1.0494 support. As noted before, corrective rise from 1.0339 is likely finished after being rejected by 55 week EMA. And, the larger down trend is ready to resume. Decisive break of 1.0494 support will confirm this bearish case and target 1.0339 low. Break of 1.0339 will confirm down trend resumption and target 100% projection of 1.1298 to 1.0339 from 1.0905 at 0.9946. On the upside, however, break of 1.0688 resistance will delay the bearish case and turn focus back to 1.0905 resistance instead.

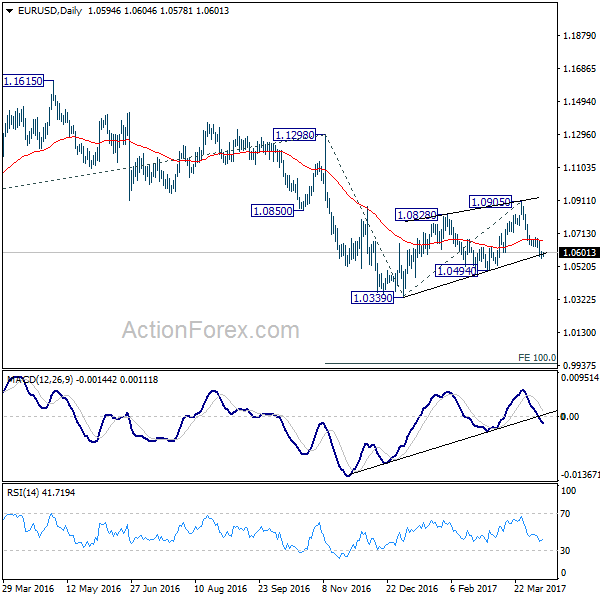

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

How Will Labour Market And UK Inflation Data Affect GBP ?

This morning at 09:30 BST will see the release of a series of UK inflation data for March including; CPI, core CPI, PPI and core PPI. It will likely cause volatility for GBP and GBP crosses. GBP/USD is currently trading above the psychological level at 1.2400.

The German ZEW economic sentiment and current situation (Apr), and Eurozone industrial production (Feb), at 10:00 BST, will likely affect the strength of the Euro and the trend of the DAX index.

UK CPI has seen an uptrend since the end of 2015, helped by a weakening Sterling rising food and fuel prices. CPI and the core CPI for February both reached above the Bank of England’s 2% target for the first time since January and July 2014 respectively.

UK inflation uptrend is likely to continue; however, the economic prospect seems to be uncertain due to Brexit uncertainty. The Bank of England is likely to keep rates on hold for the near future.

Wednesday April 12, at 09:30 BST, will see the release of UK labour market data (Mar), including average earnings (from Dec to Feb). If the pace of wage growth is slower than the pace of inflations rise then it will likely result in the weakening of household spending and purchasing power, which will lead to the slowdown of economic growth.

To adapt to rising inflation the UK government is increasing the minimum wage from £7.20 to £7.50 this month and has frozen tax on petrol and diesel for the seventh year.

Monday morning, during the early European session, the dollar index hit its highest level of 101.24 since March 15. However, it retraced and is now trading below the resistance level at 101.00. Fed Chair Yellen made a speech yesterday at the University of Michigan. She stated that “the US economy is healthy and growing at a moderate pace with the Fed close to achieving its goals on employment and inflation, neutral monetary policy and that a gradual rate hike would be appropriate”.

FOMC voting member, Neel Kashkari, will make a speech at 18:45 BST this evening.

There are only two weeks ahead until the first round voting of the French presidential election. Polls conducted by BVA-SALES FORCE showed a tightening race: Macron, Le Pen and Fillion are 23%, 23%, and 19% respectively. Macron and Le Pen got a lower share of the vote compared to 25% from a previous poll. Surprisingly, the far-left candidate Jean-Luc Melenchon, has slipped to third position, with 19% of voters, which is equal to Fillion, which poses more uncertainty to the election.