Sample Category Title

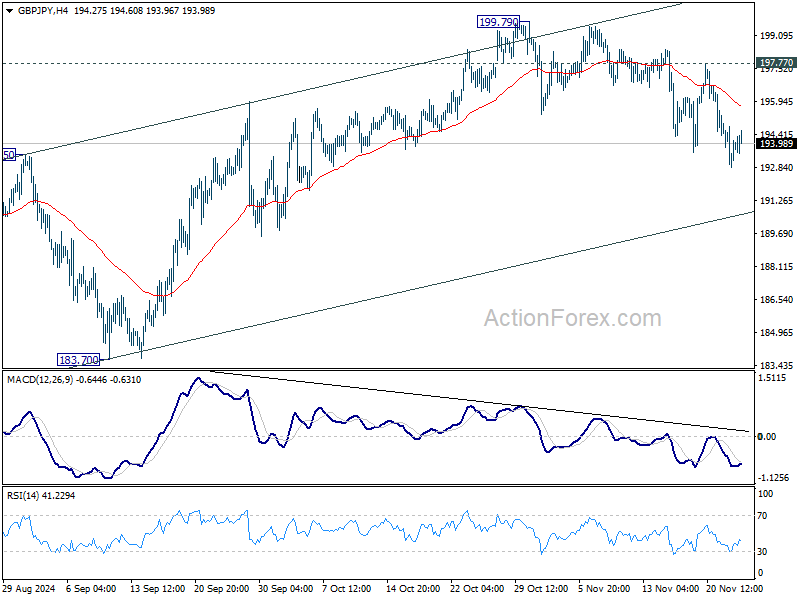

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.90; (P) 193.85; (R1) 194.86; More...

Intraday bias in GBP/JPY remains on the downside for the moment. Current development suggests that corrective rise from 180.00 has completed with three waves up to 199.79. Deeper fall would be seen to 183.70 support. For now, risk will stay on the downside as long as 197.77 resistance holds, in case of recovery.

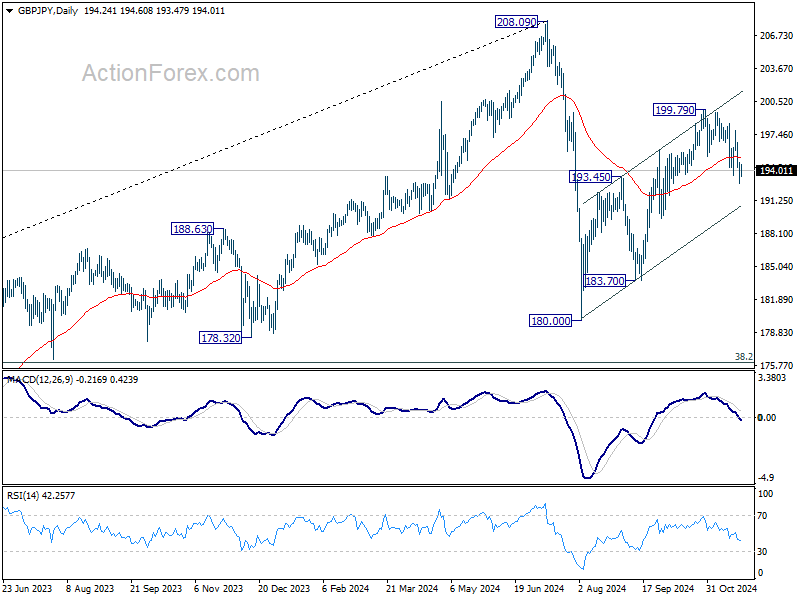

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

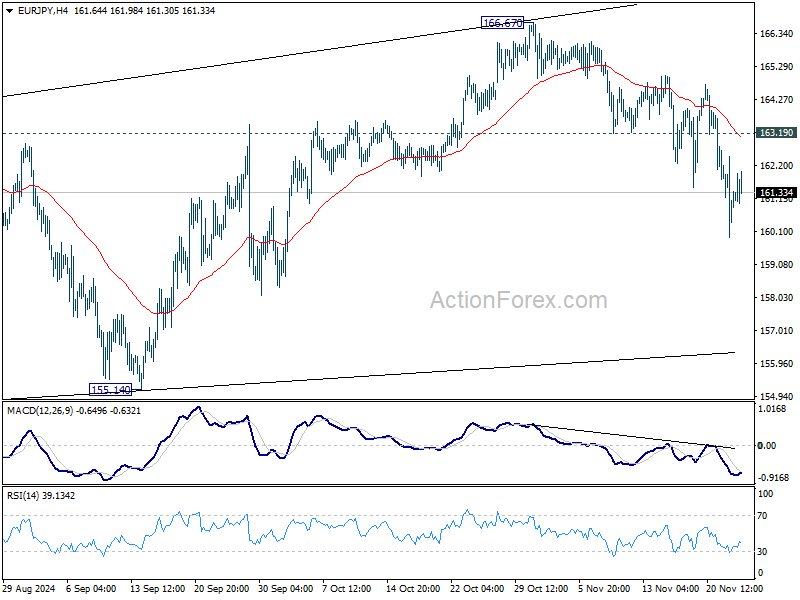

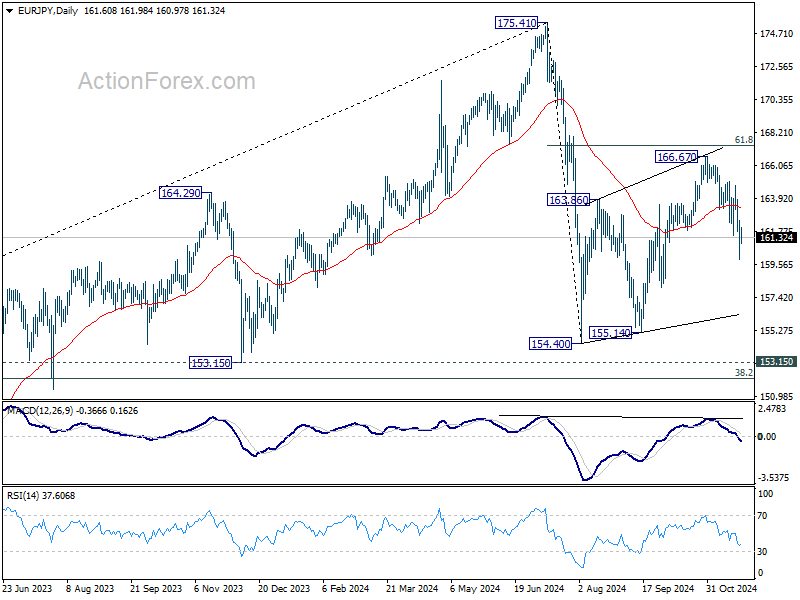

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.94; (P) 161.21; (R1) 162.53; More....

Intraday bias in EUR/JPY remains on the downside for the moment. Current development suggests that corrective rebound from 154.40 has completed with three waves up to 166.67. Deeper fall would be seen to 155.14 support next. For now, risk will stay on the downside as long as 163.19 support turned resistance holds, in case of recovery

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8272; (P) 0.8310; (R1) 0.8351; More...

Range trading continues in EUR/GBP and intraday bias remains neutral. Outlook stays bearish with 0.8446 resistance intact. On the downside, decisive break of 0.8259 will resume larger down trend to 0.8201 key support.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

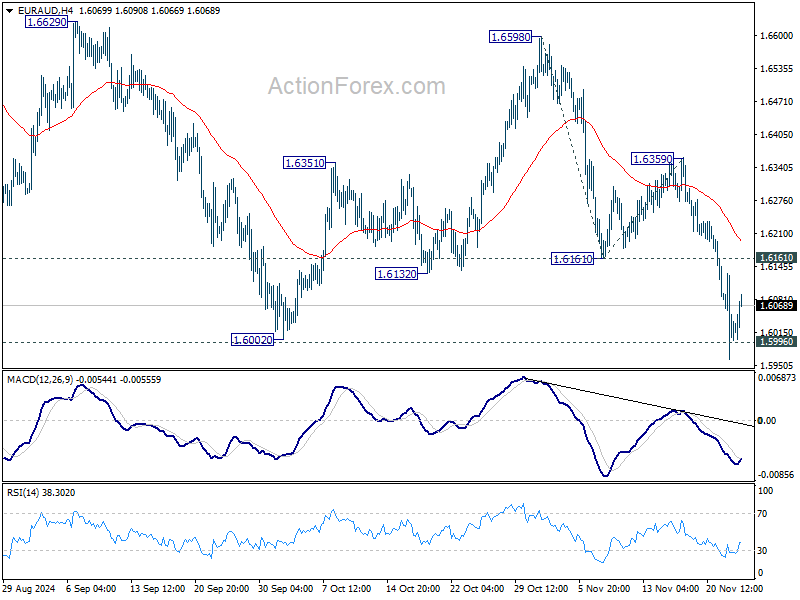

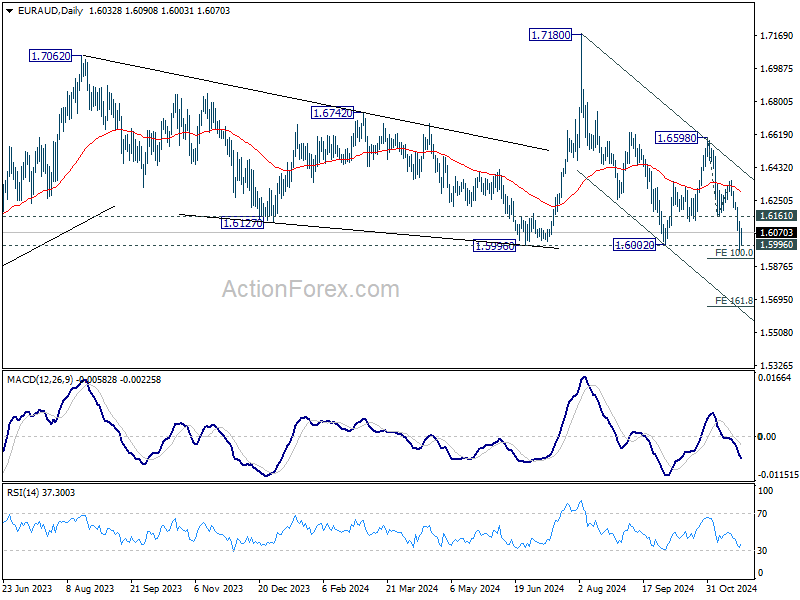

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5948; (P) 1.6041; (R1) 1.6117; More...

Intraday bias in EUR/AUD is turned neutral first with current recovery and some consolidations would be seen. Outlook will stay bearish as long as 1.6161 support turned resistance holds. On the downside, decisive break break of 1.5996 key support will carry larger bearish implications. Next near term target will be 100% projection of 1.6598 to 1.6161 from 1.6359 at 1.5922, and then 161.8% projection at 1.5652.

In the bigger picture, immediate focus is now on 1.5996 key support level. Sustained break there will argue that whole up trend from 1.4281 (2022 low) is already reversing. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction. Nevertheless, strong rebound from current level, followed by break of 1.6359 resistance, will keep medium term outlook neutral at worst.

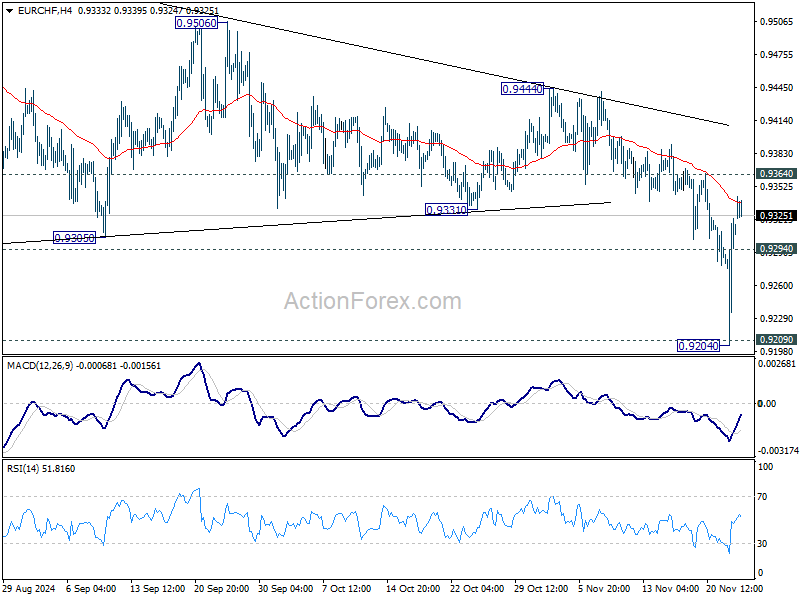

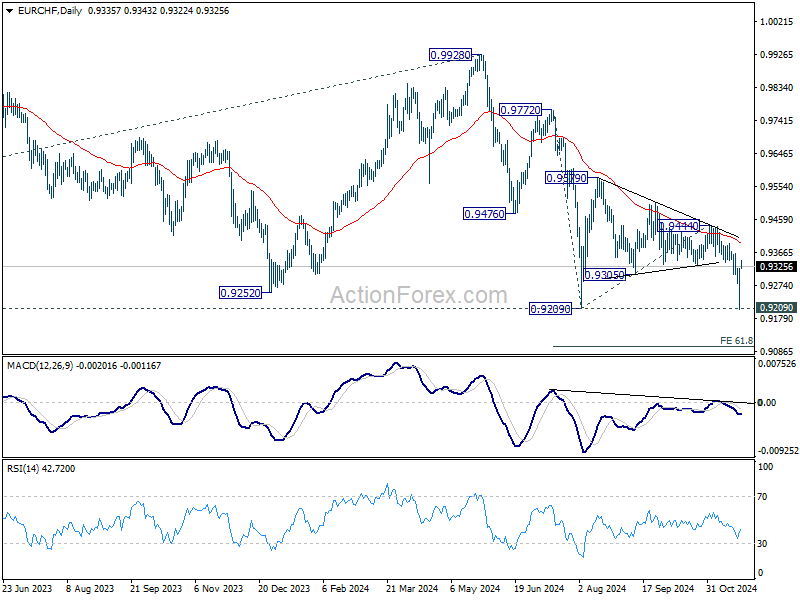

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9241; (P) 0.9283; (R1) 0.9359; More....

Intraday bias in EUR/CHF remains neutral first and more consolidations would be see first. Outlook will stay bearish as long as 0.9364 resistance holds. On the downside, below 0.9294 minor support will bring retest of 0.9204/9 support zone. Decisive break there will indicate larger down trend resumption.

In the bigger picture, outlook will now stay bearish as long as 0.9444 resistance holds. Decisive break of 0.9209 low will resumed long term down trend to 61.8% projection of 0.9772 to 0.9209 from 0.9444 at 0.9096 next.

European Equities are Cheap

Last week was marked by an improved sentiment in the US, but not so much in Europe. The US equities had a strong week: the S&P 500 rallied 1.68% over the week, Nasdaq 100 gained 1.87% - and that despite Nvidia that finally closed the week flat as the earnings disappointment kicked in with a small delay and costed the company a more than 3% retreat on Friday. The Dow Jones rallied nearly 2%, while the small caps rallied jumped nearly 4.5% on further rush to Trump trades. SPDR’s energy and financial ETFs hit a record high, the US dollar index rallied to the highest levels in two years and of course, Bitcoin – the ultimate Trump trade - flirted with the $100’000 psychological mark and consolidated gains slightly below that level during the weekend.

In Europe, things looked much less encouraging. First of all, the Stoxx 600 index tipped a toe below the 500 mark at the start of the week, and even though Friday ended on a positive note, the move was driven by a ‘bad news is good news’ type of motivation.

European equities are cheap, but...

The data released Friday looked all but encouraging. Growth in Germany slowed in the Q3 and the yearly figure printed a faster contraction of 0.3%, versus the expectation of a stable contraction near -0.2%. The PMI figures came in lower than expected: the flashing red French numbers – especially the unexpectedly fast deterioration in the French services sector - pushed the Eurozone services, and composite PMI into the contraction zone. Obviously, the bad set of data boosted the expectation that the European Central Bank (ECB) could opt for a 50bp rate cut in December rather than a moderate 25bp cut in an attempt to catch a falling knife. Today, the European companies trade with a 40% discount on their S&P500 peers in terms of PE valuations. But the ECB alone could hardly give the European businesses a strong basis to thrive in the long term. Europe needs much more than monetary support to get back on its feet.

First, the strictissime regulatory environment in Europe makes it extremely difficult for the European companies to innovate, and that’s something that the ECB can not solve with lower rates.

Second, the luxury goods companies contribute to around 8-10% of the European market capitalization during strong market periods. In France, the luxury stuff makers stand for more than 25% of the CAC 40's market cap, making it one of the most heavily weighted sectors in this index – and this percentage is around 10-12% for MSCI Europe. These companies need a strong demand from EM markets, especially from China. The fact that the Chinese economy is not doing great and the fact that the European policymakers are doing everything in their power to escalate trade tensions with China – by imposing their companies big tariffs – are not encouraging.

The same is true for the zone’s carmakers. Having missed the EV turn, and the escalating tensions with China are not having a good impact on the German carmakers, the industry is facing a massive crisis – the biggest since WW2.

ECB Chief Christine Lagarde said at last Friday’s European Banking Congress that ‘since last year, Europe’s declining innovation position has come more clearly to light,’ and that ‘technology gap between the US and Europe is now unmistakable.’ Her comments echoed Mario Draghi’s call for a 800bn euro innovation fund that the European companies should finance together with supra-sovereign bonds to compete better with the US peers.

So yes, the lower company valuations in Europe and the growing valuation gap with the US companies attract some investors with the prospects of lower ECB rates. Yet, the European economic tissue needs more than just the ECB cuts to get back on its feet. It needs deregulation and international cooperation. And it’s not on the menu du jour.

In Europe, Swiss and UK names are expected to perform better. Swiss, because of the country’s neutral and defensive nature, and stable economic and political environment. And FTSE 100 because its financial, energy and commodity focus is interesting in a period of easing monetary policies, and the big dividends that its big companies pay out are interesting for hedging against a potential uptick in global inflation that could jeopardize the easing monetary policy plans to some extent.

In the FX

The US dollar’s surge last week, combined to the weakness of the European data, sent the EURUSD to a dark hole. The pair tanked to 1.0330 and rebounded strongly after hitting that dip, and consolidating near the 1.0480 level at the time of writing. I expect some consolidation and dip buying near the current levels for tactical longs.

Week ahead

This week will be a holiday-shortened one in the USdue to Thanksgiving, with most news and data packed into the first three days. Highlights include the FOMC minutes on Tuesday, followed by growth, PCE, and jobs data on Wednesday. Meanwhile, European countries will begin releasing their preliminary November inflation figures from Thursday. The fresh CPI figures will either solidify expectations of a 50bp ECB rate cut in December or challenge them, potentially giving the euro a boost. But as mentioned last week, further EUR/USD selloffs may present good buying opportunities below the 1.05 level.

Weak Euro Area PMIs Raise Concerns Over Growth Outlook

In focus today

Today, in Germany we receive the Ifo growth indicator for November. After the decline in German PMIs on Friday, the stage is set for a decrease in Ifo as well. Consensus suggests a decrease to 86 in November compared to 86.5 in October, still suggesting a German economy in weak condition.

ECB's Chief Economist Lane will speak in the afternoon.

This week we look out for FOMC minutes from the November meeting on Tuesday. Markets will look for clues about the policy rate path as markets are divided about whether the Fed will cut rates in December as well. On Wednesday, the Reserve Bank of New Zealand will announce its rate decision, where we expect a 50bp rate cut. We also have PCE data out of the US. On Thursday, we get regional inflation data out of the euro area and on Friday we will get the full euro area flash CPI print. Likewise, Friday we will receive Swedish GDP, Norwegian unemployment and retail sales and Tokyo CPI out of Japan.

Economic and market news

What happened overnight

In China, the Peoples Bank of China injected around USD 124bn into the banking system as one-year policy loans. The measure is intended to help dealing with the liquidity pressure in China's banking system towards the year-end. China has in the past months been stepping up efforts to reduce debt risks and stimulate the struggling economy.

What happened Friday

In the US, PMIs came out strong, where especially services activity growth remains robust (57,0; Oct. 55,0). Notably, services output prices index declines to the lowest level since May 2020. Solid growth and modest price pressures are exactly what the Fed likes to see. Manufacturing new orders data support the diverging picture between the US and rest of the world. Domestic new orders index recovers modestly to 47.9 (from 46.8), but new export orders index collapses to 43.9 (from 49.1).

In the euro area, PMI declined to 48.1 from 50.0 in October indicating the economy has slipped into contractionary territory in the final quarter of the year. Consensus was looking for unchanged PMIs. The decline was due to both services PMI that fell to 49.2 from 51.6 and manufacturing that fell to 45.2 from 46.0. The PMIs today have increased our concerns over the near-term growth outlook for the euro area economy. GDP growth in the final quarter of the year will likely be around 0.0% q/q. The outlook for the first quarters of next year has also turned worse. However, we continue to expect growth to pick up during next year as we look for significant easing by the ECB and as real wage growth is set to increase private consumption since the labour market remain strong.

ECB's Villeroy spoke about monetary policy and said the ECB is not behind the curve and that he expects that the euro area is achieving a soft economic landing after being questioned about the very weak November PMIs. However, he said that they are closely monitoring the risk of undershooting inflation and thereby maintaining a too strict monetary policy. ECB's Nagel spoke about monetary policy as well saying that despite the weak PMIs he will wait for the December ECB economic projection before he is ready to take a stance on the December rate decision. He noted however that more rate cuts are coming in 2025. We expect ECB to deliver a 25bp rate cut at the December meeting.

In the UK, we also got weak PMI figures. Composite at 49.9 (cons: 51.7, prior: 51.8), service at 50.0 (cons: 52.0, prior: 52.0) and manufacturing 48.6. The survey notes a rise in input costs, concerns about the business outlook, a drop in business activity with easing in output price inflation. Note, as previously flagged, there is likely some effect from the Autumn statement (UK fiscal budget) on souring sentiment. While the BoE is set to stay on hold in December, we think this argues for a step up in easing pace in 2025, in line with our forecast. We expect the Bank Rate to end the year at 3.25% in 2025.

In Sweden, Riksbank governor Erik Theddéen spoke at a Danske Bank event. He made it clear that he did not intend to send any new monetary policy signals. However, it was interesting to hear him saying that the Riksbank is not keen on negative interest rates and QE again. Instead, they want to see a better policy mix with, and support from, fiscal policy.

Equities: Global equities were higher on Friday, albeit with a significant sectoral divergence between the US and Europe. This was primarily due to very different outcome of flash PMIs, particularly in the services sector, which drove yields lower in Europe and higher in the US, led by the short end of the curve. Not surprisingly, the most noticeable differences were within the banking sector. In Europe, banks were lower, ranking at the bottom of the performance table, whereas in the US banks were higher and outperformed the S&P 500 index by more than 1 percentage point. Despite the disappointing macroeconomic data out of Europe on Friday the week still ended on a high note, with US yields dominating within styles and lifting the value preferences among investors. Both on Friday and over the last week, small caps performed exceptionally well, with the Russell 2000 up by 4.5% last week. In the US on Friday, Dow +0.97%, S&P 500 +0.4%, Nasdaq +0.2%, and Russell 2000 +1.8%. Asian markets were also solidly in the green this morning, with Chinese stocks bucking the trend. Both European and US futures are showing solid gains this morning.

FI: There was a significant decline in both European and US bond yields on Friday as well as a decent bullish steepening of the yield curves on the back of the weak European PMI data. Given the weak eurozone economy, the divergence between US and Europe continued as seen both the EURUSD as well as 10Y Treasury-Bund spread that has widened from 150bp in mid-September to 210bp-215bp. This morning, we have seen that markets have responded positively to the confirmation of Scott Bessent as new US Treasury secretary as US government bond yields declined in Asian Trading hours. He is seen as a more conventional choice who is expected to give some stability to US economy and focus on reigning in fiscal spending.

FX: The last week in FX markets has been characterised by continued USD performance on the one side and heavy European FX underperformance on the other. Not least the CEEs have been under pressure delivering even larger weekly spot losses than the single currency despite poor PMIs adding pressure on the EUR heading into the weekend. The CAD and AUD continue to do well which might also explain why the NOK has done surprisingly well despite the Norwegian currency's usual closer price action to European FX. CHF, SEK and GBP are all found among the underperformers in Majors' space but are still among those European currencies that have suffered the smallest losses vs the greenback. Finally, the JPY has stabilised after the US rates induced setback post the US election.

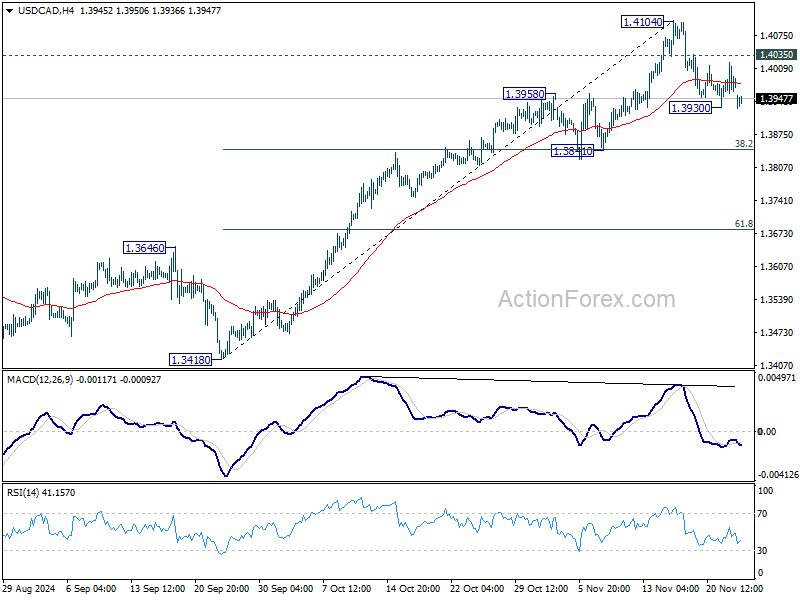

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3952; (P) 1.3986; (R1) 1.4015; More...

USD/CAD is extending the consolidation from 1.4104 and intraday bias remains neutral. On the downside, break of 1.3930 will extend the corrective fall from 1.4104 to 1.3841 cluster support (38.2% retracement of 1.3418 to 1.4104 at 1.3842). Nevertheless, above 1.4035 minor resistance will bring retest of 1.4104 high.

In the bigger picture, up trend from 1.2005 (2021) is resuming with break of 1.3976 key resistance (2022 high). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

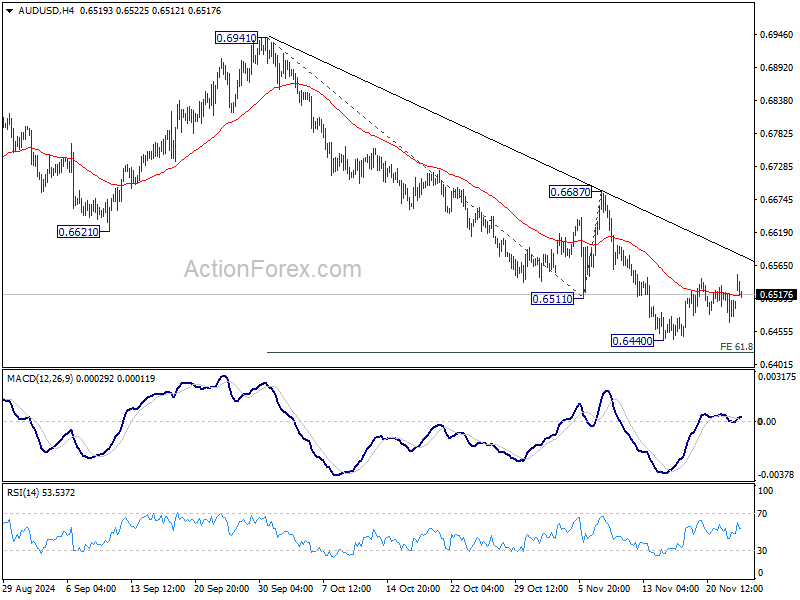

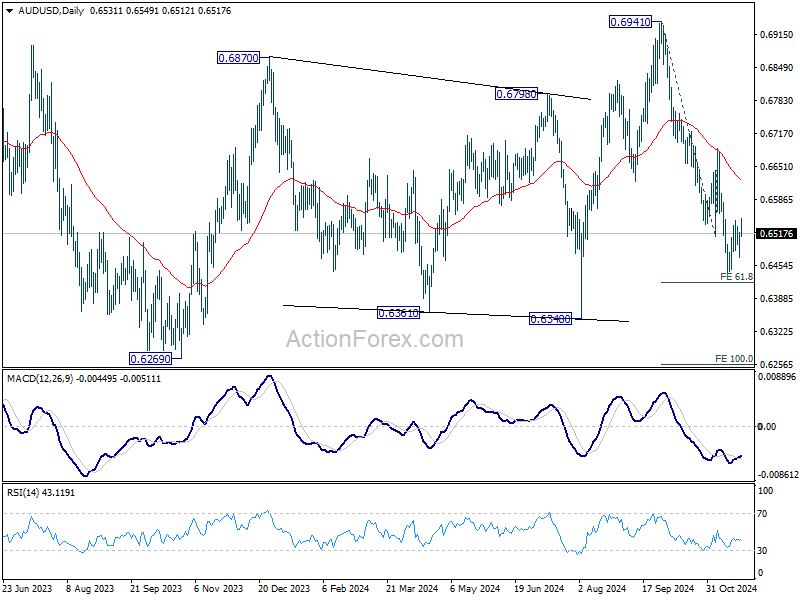

AUD/USD Daily Report

Daily Pivots: (S1) 0.6474; (P) 0.6500; (R1) 0.6529; More...

Intraday bias in AUD/USD remains neutral as consolidation from 0.6440 is extending. Further decline is expected as long as 0.6687 resistance holds. On the downside, decisive break of 61.8% projection of 0.6941 to 0.6511 from 0.6687 at 0.6421 will resume the fall from 0.6941 to 100% projection at 0.6257 next.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

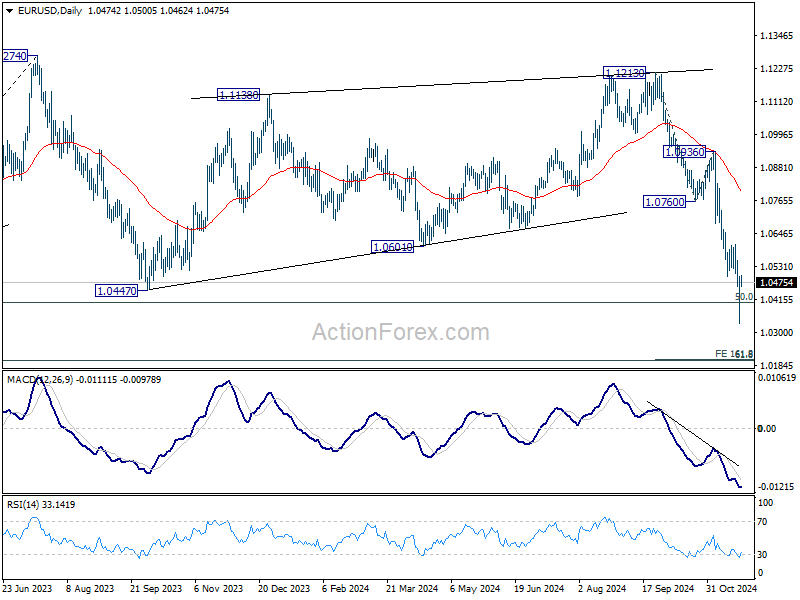

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0335; (P) 1.0416; (R1) 1.0500; More...

Intraday bias in EUR/USD is turned neutral and some consolidations could be seen first. But outlook will remain bearish as long as 1.0609 resistance holds. On the downside, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication and target next level at 161.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0203. Nevertheless, strong rebound from current level, followed by break of 1.0609 resistance, will indicate short term bottoming.

In the bigger picture, immediate focus is now on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.