Sample Category Title

BoE’s Greene cautions against aggressive rate cuts amid persistent services inflation and wage growth

BoE MPC member Megan Greene warned during an event overnight that services inflation remains stubbornly high, with wage growth exceeding levels consistent with the 2% inflation target. “There’s some risk that wage growth might be stickier than we would hope,” she said, adding that this could keep both services and overall inflation elevated.

Greene emphasized the importance of a cautious approach, stating that “the risk of cutting too early or too aggressively is a greater risk than going a bit more slowly.”

Feedback from firms suggests wage growth could settle closer to 4%, well above the desired level. Companies may respond to higher costs by increasing prices, reducing employment or hours, investing in productivity-enhancing capital, or absorbing costs into profit margins, she noted.

She also highlighted the UK’s vulnerability to external shocks as an open economy. “Historically speaking, about a third of the moves in our curve in the UK were influenced by things happening outside the UK. Now it’s about half.”

Greene pointed to the outsized influence of the US Treasury curve, describing it as a “drunken dragon” that heavily impacts the UK market, especially amid global geopolitical risks and shifts in US economic policy under the president-elect.

GBP/USD Struggles Ahead: Will It Break Through Key Levels?

Key Highlights

- GBP/USD extended losses and tested the 1.2600 support.

- A connecting bearish trend line is forming with resistance at 1.2700 on the 4-hour chart.

- Bitcoin started a consolidation phase near the $90,000 zone.

- Oil is correcting losses and trading near the $69.50 zone.

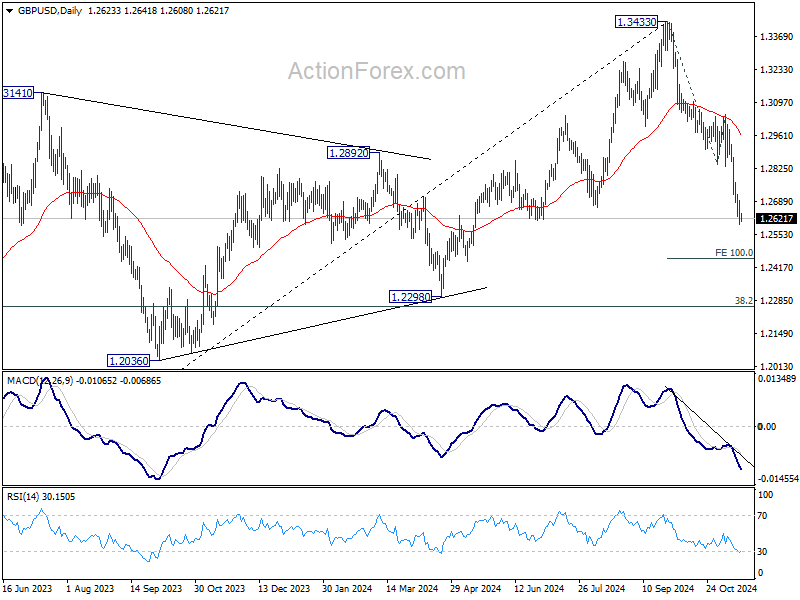

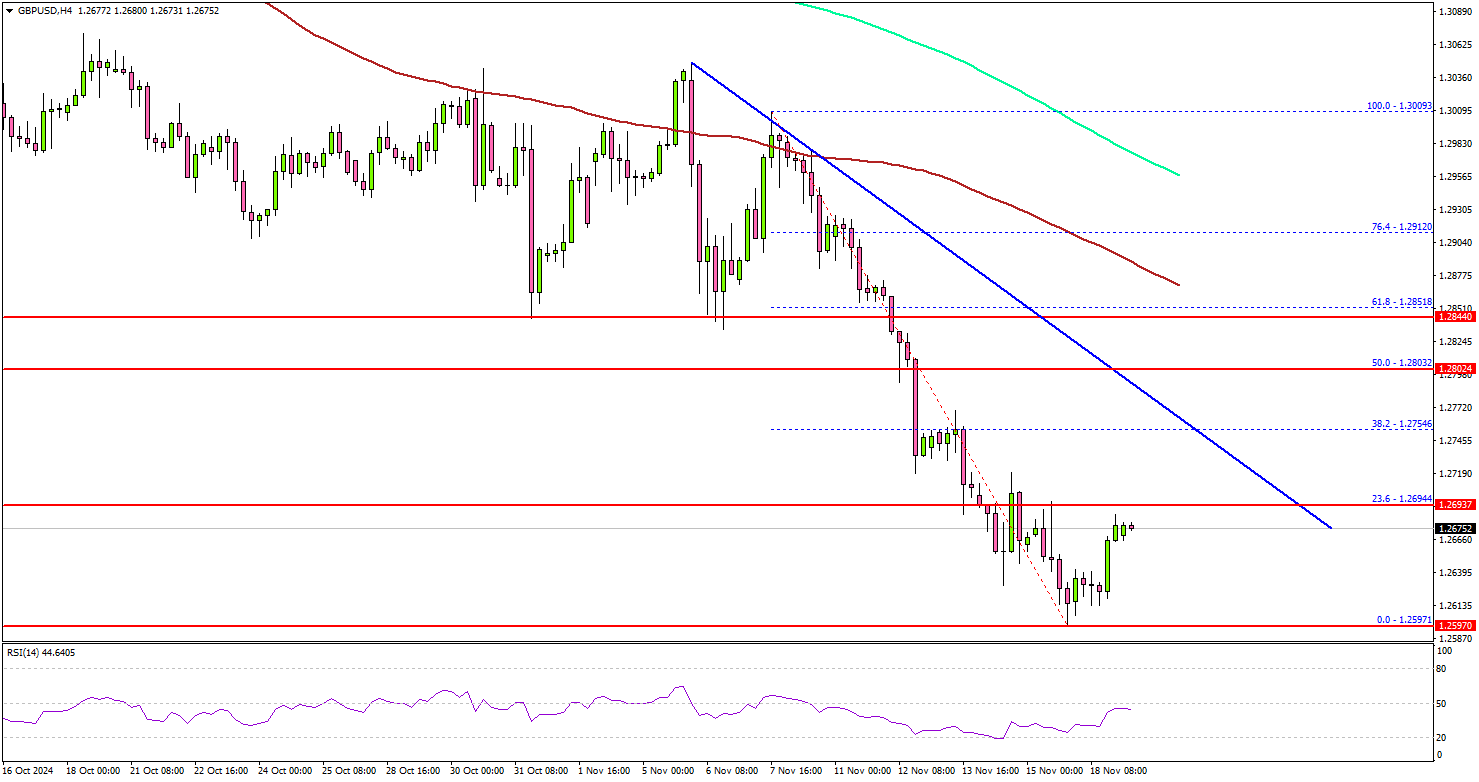

GBP/USD Technical Analysis

The British Pound started a fresh decline below the 1.2800 support against the US Dollar. GBP/USD traded below 1.2720 to move into a negative zone.

Looking at the 4-hour chart, the pair settled below the 1.2700 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). Finally, the bulls appeared near the 1.2600 support zone.

A low was formed at 1.2597 and the pair is now attempting to recover. On the upside, the pair could face resistance near the 1.2700 level. There is also a connecting bearish trend line forming with resistance at 1.2700 on the same chart.

The trend line is close to the 23.6% Fib retracement level of the downward move from the 1.3009 swing high to the 1.2597 low. The first key resistance is near the 1.2750 level.

A close above the 1.2750 level could set the tone for another increase. The next major resistance could be 1.2800, above which the price could climb higher toward the 1.2850 resistance. It is near the 61.8% Fib retracement level of the downward move from the 1.3009 swing high to the 1.2597 low.

On the downside, immediate support sits near the 1.2640 level. The next key support sits near the 1.2600 level. Any more losses could send the pair toward the 1.2550 level or even 1.2500 in the near term.

Overall, GBP/USD is attempting to recover but it might face many hurdles near 1.2700 or 1.2750 in the near term.

Looking at Bitcoin, the price gained traction for a new all-time high above $92,000 and is currently consolidating gains.

Upcoming Economic Events:

- US Housing Starts for Oct 2024 (MoM) – Forecast 1.34M, versus 1.354M previous.

- US Building Permits for Oct 2024 (MoM) – Forecast 1.430M, versus 1.425M previous.

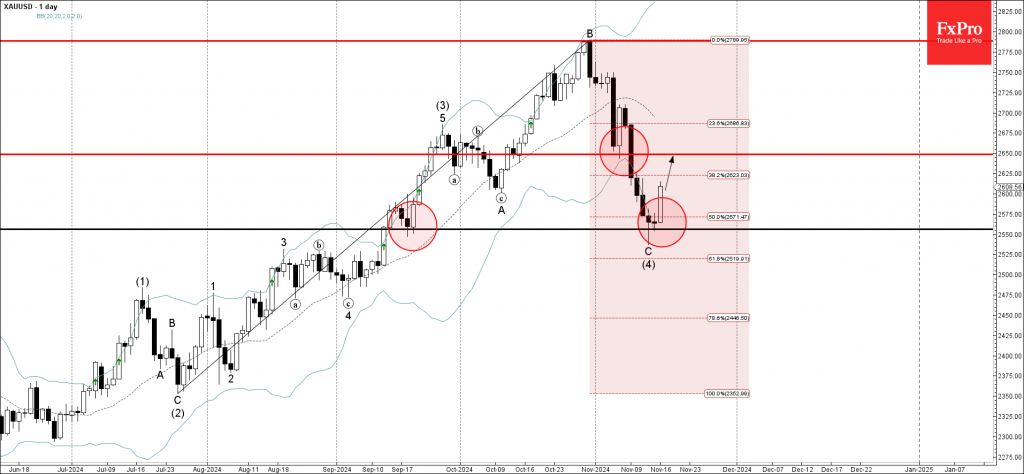

Gold Wave Analysis

- Gold reversed from key support level 2550.00

- Likely to rise to resistance level 2650.00

Gold recently reversed up from the support zone located between the key support level 2550.00 (which also reversed the price in the middle of September), standing close to the lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from July.

The upward reversal from the support level 2550.00 stopped the previous intermediate ABC correction (4) from the end of September.

Given the clear daily uptrend, Gold can be expected to rise to the next resistance level 2650.00 (former support from the start of November).

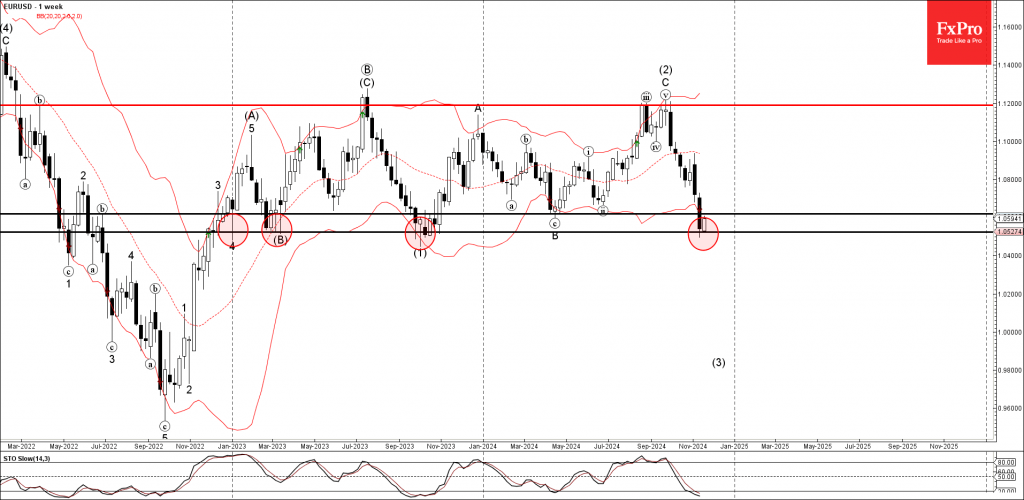

EURUSD Wave Analysis

- EURUSD reversed from long-term support level 1.0500

- Likely to rise to resistance level 1.0620

EURUSD currency pair recently reversed up from the major long-term support level 1.0500 (which has been steadily reversing the price from the start of 2023, as can be seen below), standing close to the lower daily Bollinger Band.

The support level 1.0500 level was further strengthened by the lower daily Bollinger Band.

Given the strength of the support level 1.0500, oversold weekly Stochastic and the strong US dollar bearishness seen today, EURUSD currency pair can be expected to rise to the next resistance level 1.06200, former support from the start of this year.

Sunset Market Commentary

Markets

The week started off with some Bund underperformance, both vs US Treasuries and UK gilts. With the front end adding up to 7 bps, European money markets are slightly paring bets on ECB rate cuts. The terminal rate in the recent repricing was brought down to less than 2%. Such a supportive monetary policy stance isn’t something we consider necessary based on the current economic data, even if the picture isn’t particularly rosy. This week’s (German) PMI’s (on Friday) serve as a reality check and will be watched closely for signs of the economy further bottoming out. Greek Governing Council member Stournaras said in any case ”there’s going to be a number of cuts” and advocated going in steps of 25 bps, the next one all but certain to happen in December. Stournaras said borrowing costs could be close to 2% toward the end of next year. The UK curve joined the bear flattening move in Europe but the US parted ways. US rates were flat (3-yr) to 4 bps (30-yr) higher in a steepening move. Stocks trade on the backfoot in Europe and open mixed on Wall Street. The Nasdaq ekes out a small gain. Tech-heavyweights Tesla and Nvidia more or less cancel each other out with the former rising on speculation president-elect Trump will ease self-driven car rules. The latter slides over an overheating problem with its most recent chip ahead of Wednesday’s earnings release. Currency markets are uninspired. The Japanese yen underperforms on a speech by Ueda. The Bank of Japan governor kept the cards close to his chest, not offering any particular hint on a potential rate hike at the December meeting. USD/JPY recoups some of Friday’s gains but remains sub 155. The euro is generally better bid after a horrible two first weeks in November, though we remain cautious on its upside potential. EUR/USD rises to 1.057. EUR/GBP builds on Friday’s momentum to trade around 0.837 ahead of UK inflation numbers on Wednesday and retail sales and PMI’s on Friday. The greenback on a trade-weighted basis is on track for a back-to-back loss to 106.5. The crypto market captured some headlines with Bitcoin trading back above the 90k barrier. Gas prices on commodity markets hit a new one-year high as supply concerns add to higher demand. Oil prices rebounded the recent lows just north of $70/b (Brent) as well.

News & Views

Greek Prime Minister Mitsotakis said at a Bloomberg event that Athens is planning to repay next year at least €5bn of debt outstanding under the Greek loan facility with maturities ranging from 2033 to 2043. Before year-end the Greek government will still conclude a €7.9bn repayment of floating rate debt (also under GLF) which matures in 2026, 2027 and 2028. Greece has already paid back loans worth €5.3bn in December 2023 and €2.65bn in December 2022 thanks to good growth and the high primary surpluses it is running. The Greek debt ratio is on a downward path since peaking at 207% of GDP in 2020. Next year, it is expected to drop below 150% of GDP. Improving public finances helped the country regain its investment grade status at S&P and Fitch at the end of last year after losing it at the start of the EMU sovereign debt crisis.

The Czech National Bank published remarks on a panel discussion in which CNB governor Michl took part last Thursday. He reiterated his view that we are now entering a phase of higher inflation volatility around central bank targets, with an upside risk. Some degree of restriction is necessary to ensure low core inflation. Looking ahead, core inflation may need to be slightly below 2%. Since this is not reflected in the CNB’s current outlook, they are already discussing the appropriate time to pause rate cuts, likely at the next, December, policy meeting. The CNB cut its policy rate by 25 bps to 4% in November with neutral rates estimated to be at least 3.5%. EUR/CZK trades a tad weaker today, at 25.30.

ECB’s Stournaras: December 25bps cut optimal

Greek ECB Governing Council member Yannis Stournaras told Bloomberg today that a 25 bps rate cut at the upcoming December meeting would represent “an optimal reduction".

He acknowledged that interest rates remain firmly in restrictive territory, emphasizing that even with continued cuts to reach the neutral rate, "it’s still a long way to go,” indicating multiple reductions are likely ahead.

Stournaras also highlighted the optimistic revision in inflation expectations. "The baseline is that now, inflation falls more rapidly than we thought in our September forecasts,” he noted, adding that ECB could meet its 2% inflation target on a sustainable basis by early to mid-2025 rather than by the end of the year.

Will Fed-ECB Policy Gap Sink Euro? EUR/USD Analysis

- EUR/USD faces pressure due to a strong US Dollar and concerns about the ECB’s policy direction.

- The US election and potential trade war concerns are weighing on the Euro.

- The interest rate differential between the Fed and ECB is a key factor to watch.

The US Dollar bulls continue to hold firm at the start of the week following signs that some weakness may materialize. So far this has proven to be false, as Asian session declines were immediately wiped out following the European.

ECB Policymakers Send Mixed Signals

The US election has raised concerns for the EU regarding a potential trade war, and its impact on the Euro Area. Mixed messaging from ECB policymakers this morning has kept EUR/USD under pressure following an attempted rally at the start of the European session. Markets will no doubt be eyeing a speech by ECB President Christine Lagarede this evening in Paris for clues as to how the ECB views the potential impact of a Trump Presidency.

Earlier in the day, ECB Vice President Luis de Guindos said that the main worry has moved from high inflation to concerns about economic growth. A trade conflict between the Eurozone and the US could start after Trump said in his campaign that the Eurozone would face serious consequences for not purchasing enough American goods.

Rate Differential Concerns Grow

Following another bout of strong US data last week and an uptick in US PPI numbers, markets continue to price in less cuts from the Federal Reserve. This has kept the USD underpinned at a time when the ECB is dealing with disappointing growth and the possibility of more aggressive rate cuts.

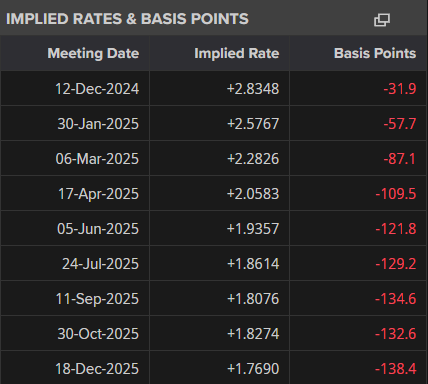

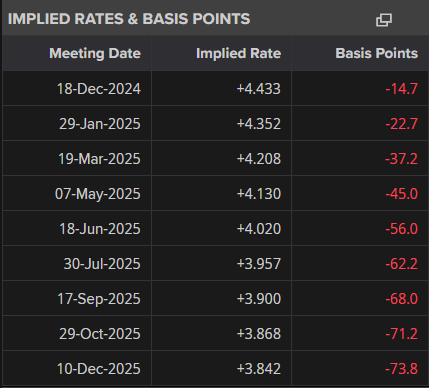

As things stand, the ECB is scheduled to cut rates as much as 140+ bps through December 2025, the Fed are only expected to cut around 70+ bps. This is a massive discrepancy and if this gap continues to grow, the chances of further losses for EUR/USD will rise.

ECB and Federal Reserve Implied Rates – December 2025

ECB

FED

Source: LSEG

Looking ahead to the rest of the week, US and EU PMI data will be key. For the Euro Area more so than the US as concerns linger around growth moving forward. A disappointing PMI print for the EU will keep the Euro on the back foot.

The US PMI data will have markets focused on performance as well, largely to see if the US economy is as strong as recent data suggests. Job creation in the sector might also be of interest given the up and down payroll figures and downgrades in the US.

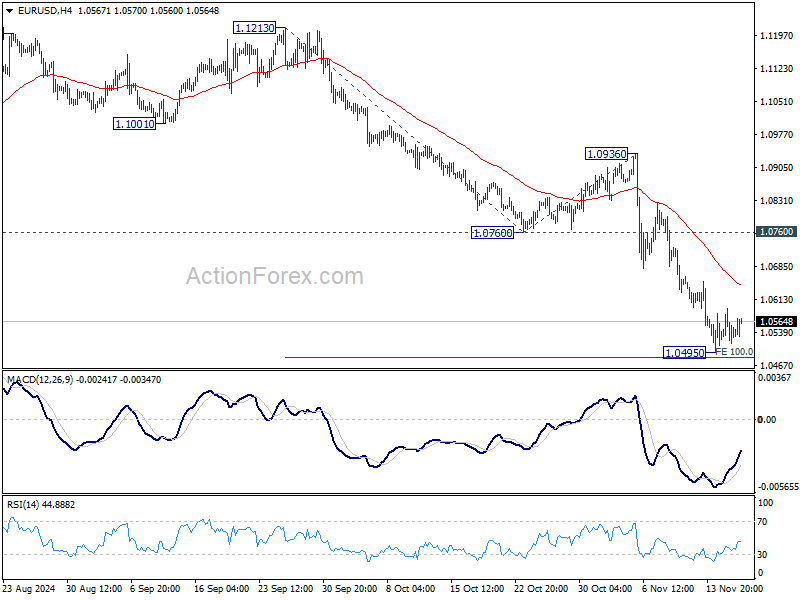

Technical Analysis of EUR/USD

From a technical standpoint, EUR/USD is holding above the key psychological handle at 1.0500. An inverse hammer candle close on Friday hinted at further upside today, but there remains significant downward pressure on the pair.

This is evidenced by the failure of the pair to hold onto gains with early European session largely wiped out already in a similar vain to Friday.

The positive is that EUR/USD continues to hover around oversold territory on the RSI period 14. This of course not a guarantee of a move higher but a sign that attention should be paid for a potential reversal.

Immediate resistance rests at the 1.0600 and 1.0700 handles respectively before a potential retest of the descending trendline around the 1.0755 handle comes into focus.

A move lower here and a break of the 1.0500 handle faces support at 1.0450 before support at 1.0366 becomes a possibility.

EUR/USD Daily Chart, November 18, 2024

Source: TradingView.com

Support

- 1.0500

- 1.0450

- 1.0366

Resistance

- 1.0600

- 1.0700

- 1.0755

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0506; (P) 1.0549; (R1) 1.0583; More...

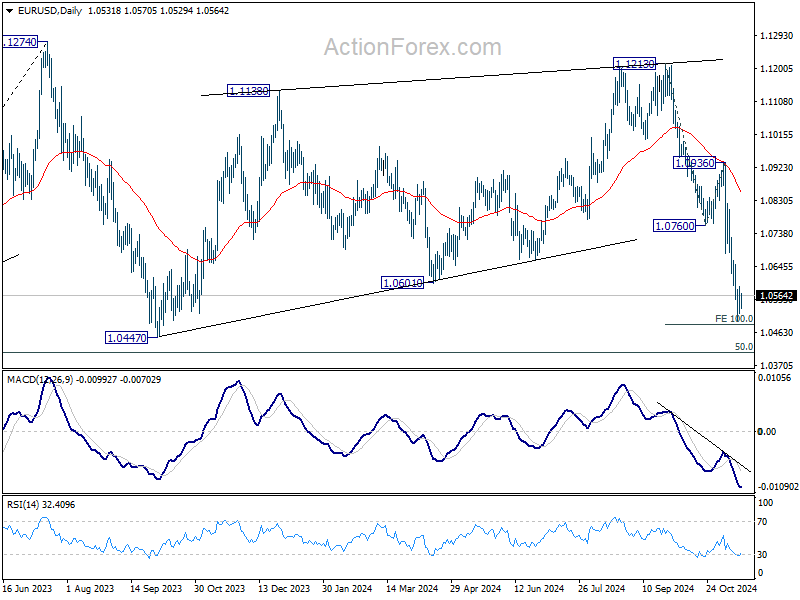

EUR/USD is staying in consolidation above 1.0495 temporary low and intraday bias stays neutral. Outlook will stay bearish as long as 1.0760 support turned resistance holds. On the downside, firm break of 1.0495 will resume the fall from 1.1213 to 1.0447 support and then 1.0404 key fibonacci level next.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage. However, firm break of 1.0404 will raise the chance of reversal and target 61.8% retracement at 1.0199.

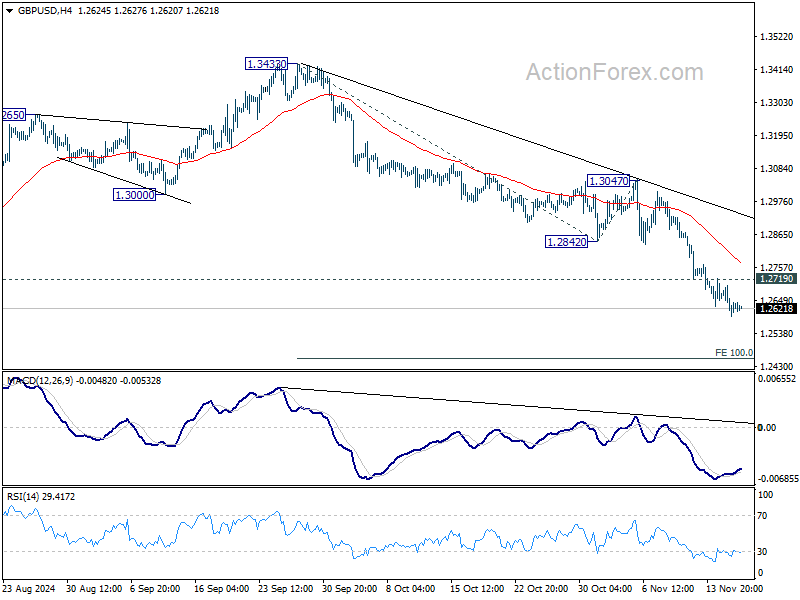

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2580; (P) 1.2638; (R1) 1.2680; More...

GBP/USD's fall from 1.3433 is in progress and intraday bias stays on the downside. Next target is 100% projection of 1.3433 to 1.2842 to 1.3047 at 1.2456. On the upside, above 1.2719 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 1.2842 support turned resistance holds, in case of recovery.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2977) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.