Sample Category Title

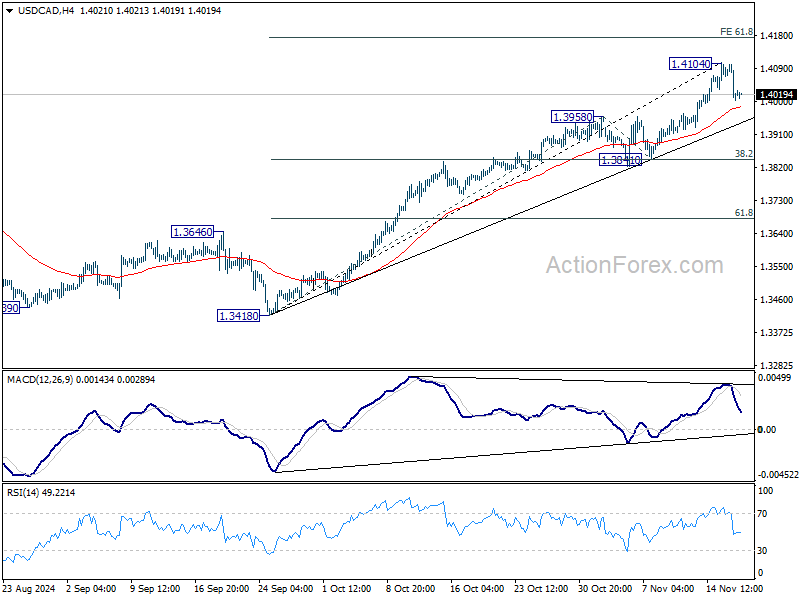

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3978; (P) 1.4041; (R1) 1.4077; More...

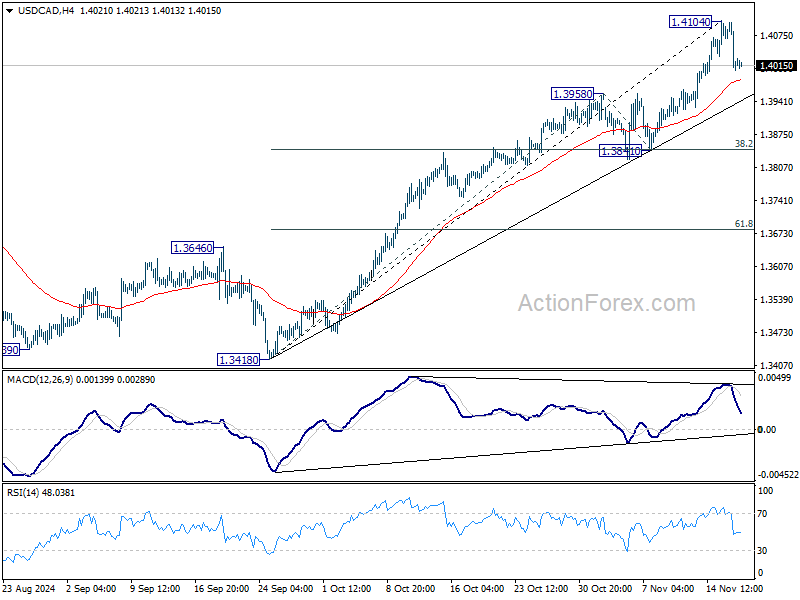

Intraday bias in USD/CAD is turned neutral with current retreat, but consolidations would be brief as long as 1.3958 resistance turned support holds. Above 1.4104 will resume larger up trend to 61.8% projection of 1.3418 to 1.3958 from 1.3841 at 1.4175. Nevertheless, break of 1.3958 will bring lengthier consolidations, bring deeper pull back to 1.3841 cluster support (38.2% retracement of 1.3418 to 1.4104 at 1.3842).

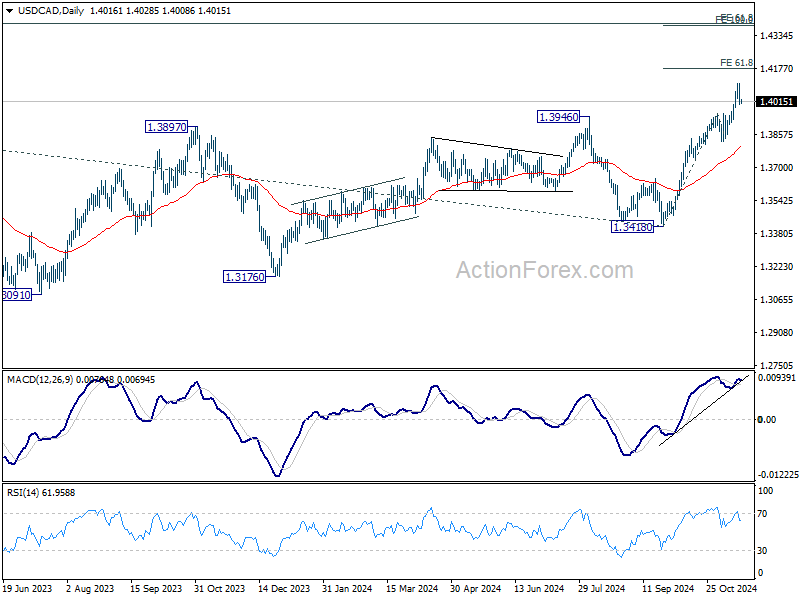

In the bigger picture, up trend from 1.2005 (2021) is resuming with break of 1.3976 key resistance (2022 high). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9347; (P) 0.9358; (R1) 0.9372; More....

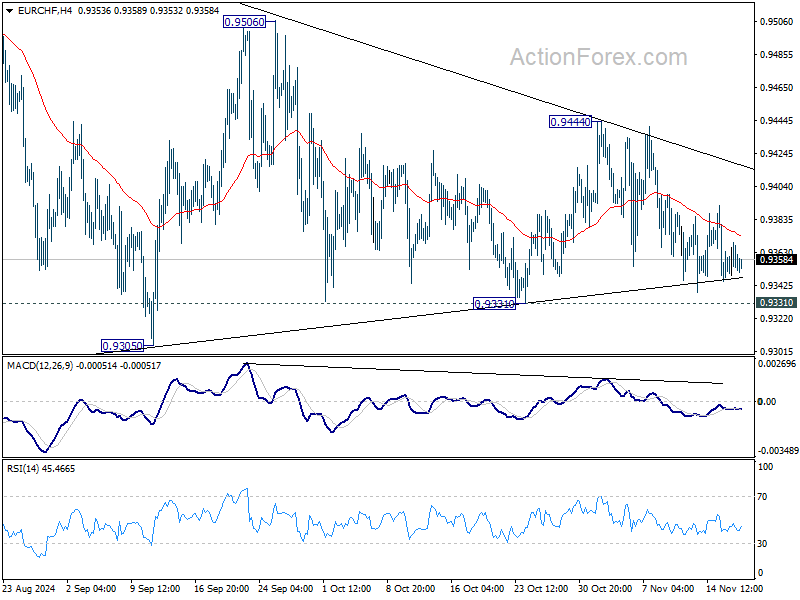

No change in EUR/CHF's outlook as consolidation continues inside converging triangle. Intraday bias remains neutral at this point. On the downside, break of 0.9331 will target 0.9305 support first. Firm break there will bring retest of 0.9209 low. On the upside, break of 0.9444 will bring stronger rally to 0.9506 resistance next.

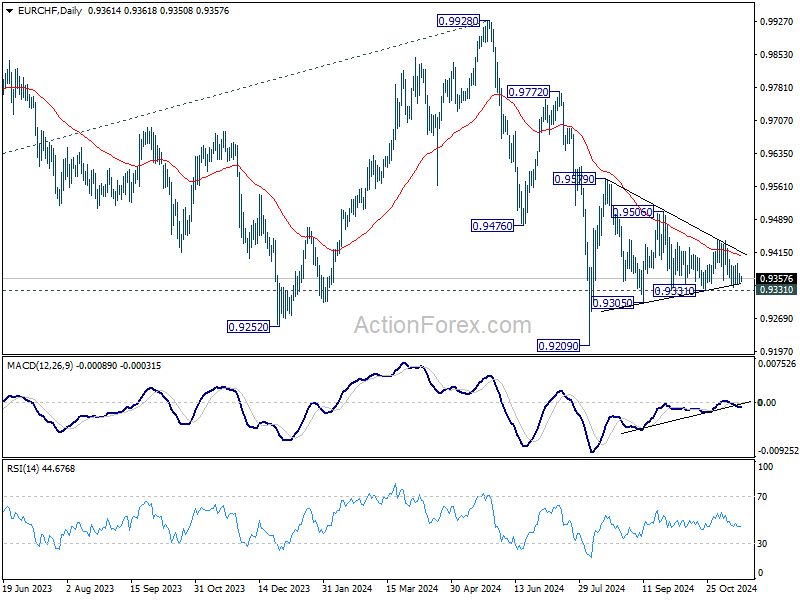

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9410) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming at 0.9209 and bring stronger rebound back towards 0.9928 key resistance.

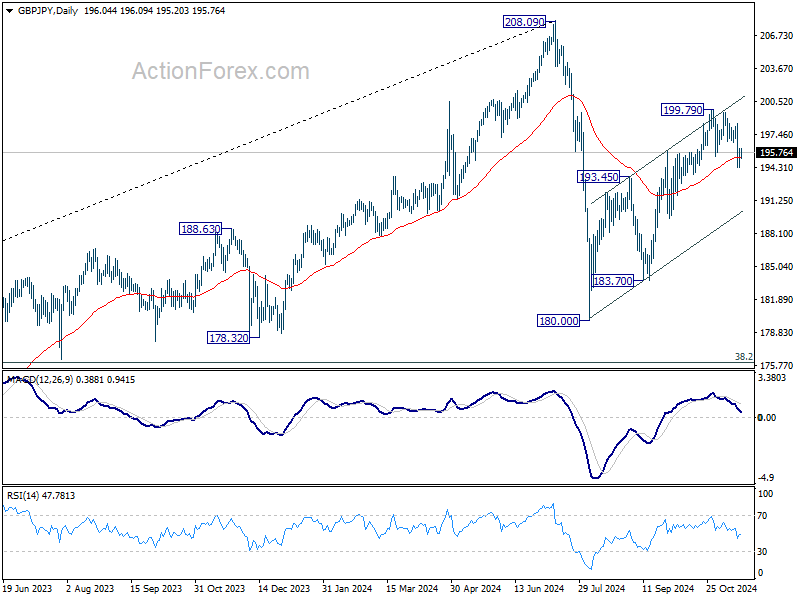

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.93; (P) 195.54; (R1) 196.71; More...

Intraday bias in GBP/JPY is turned neutral first as consolidation from 194.28 extends. But further decline is expected as long as 198.43 resistance holds. Corrective rise from 180.00 could have completed with three waves up to 199.79, after hitting channel resistance. Below 194.28 will target 193.45 resistance turned support. Decisive break there will target 183.70 next. Nevertheless, break of 198.43 will dampen this bearish view and bring retest of 199.79 high instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

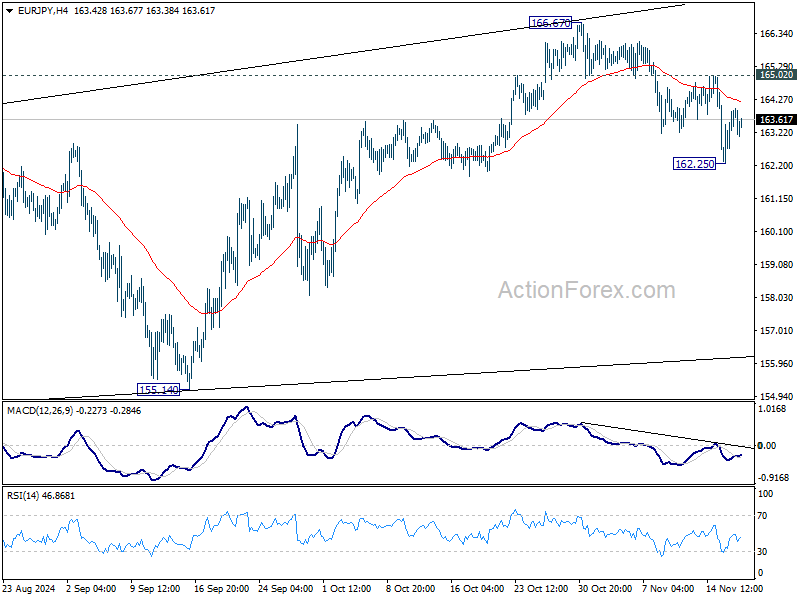

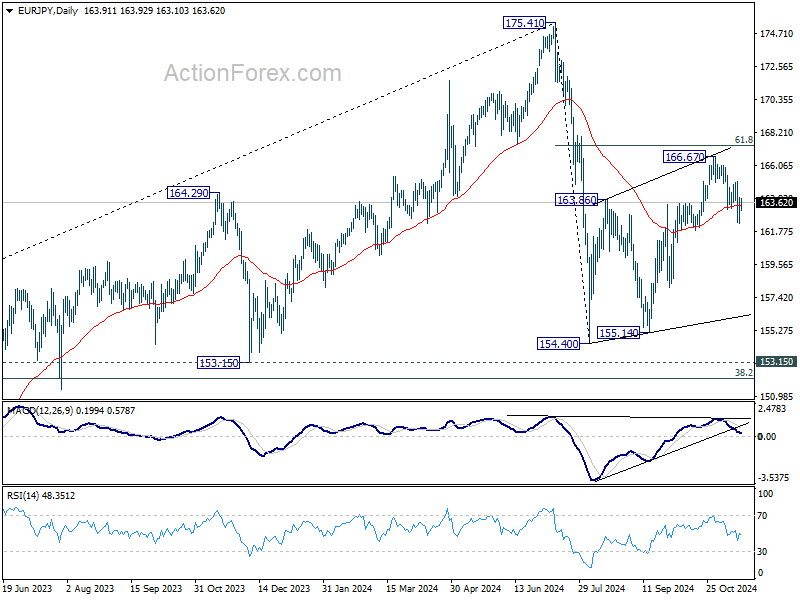

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.81; (P) 163.40; (R1) 164.52; More....

Intraday bias in EUR/JPY is turned neutral first as recovery from 162.25 extends. But further decline is expected as long as 165.02 resistance holds. Corrective rebound from 154.40 could have completed with three waves up to 166.77 already, ahead of 61.8% retracement of 175.41 to 154.40 at 167.38. Below 162.25 will target 155.14 support next. However, firm break of 165.02 will dampen this bearish view and bring retest of 166.67 high instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

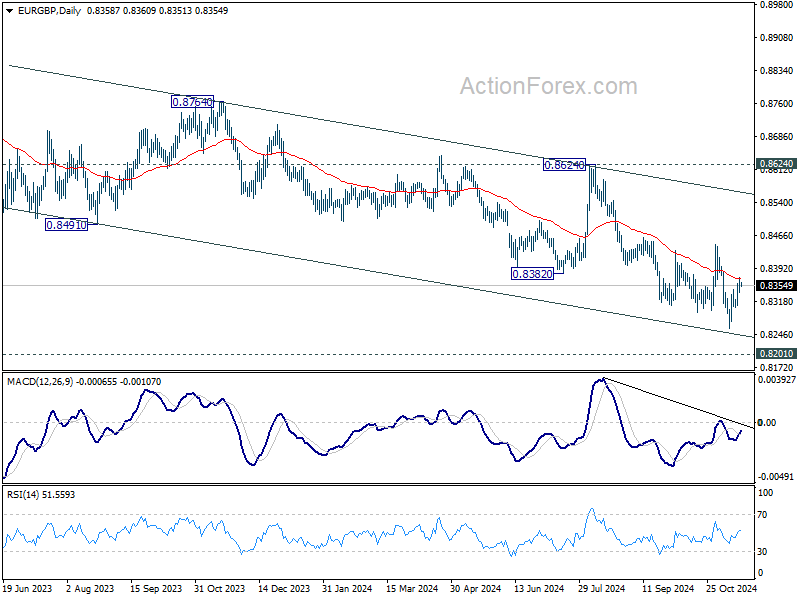

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8342; (P) 0.8358; (R1) 0.8375; More...

Outlook in EUR/GBP is unchanged and intraday bias stays neutral. Further decline is expected as long as 0.8446 resistance holds. On the downside, below 0.8306 minor support will turn bias back to the downside for 0.8259 first, and then 0.8201 key support. Nevertheless, firm break of 0.8446 will confirm short term bottoming.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

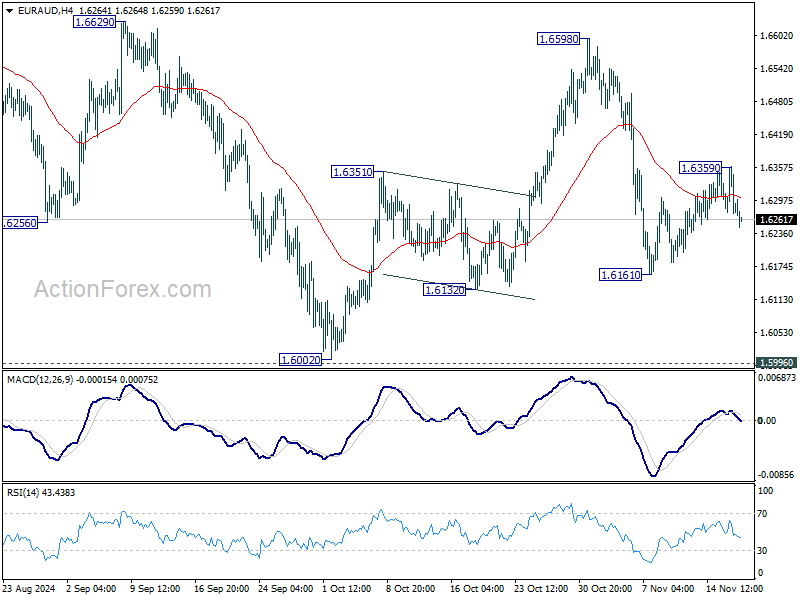

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6253; (P) 1.6307; (R1) 1.6340; More...

EUR/AUD weakens notably after failing to sustain above 55 D EMA, but downside is held well above 1.6161 temporary low. Intraday bias stays neutral and risk remains on the downside for the moment. On the downside, below 1.6161 will target a test on 1.5996/6002 key support zone. Nevertheless, break of 1.6359 will turn bias to the upside for stronger rebound towards 1.6598 resistance instead.

In the bigger picture, as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still expected to resume through 1.7180 at a later stage. However decisive break of 1.5996 will argue that the medium term trend might have reversed. Deeper fall would be seen to 61.8% retracement of 1.4281 (2022 low) to 1.7180 at 1.5388, even as a correction.

Forex Consolidation Continues; Eyes on Canada’s CPI

The forex markets remain subdued in Asian session, with all major pairs and crosses confined within yesterday’s tight ranges, and many still constrained within last week’s bounds. Among the majors, Australian Dollar is showing slight strength supported by hawkish RBA minutes, followed by Swiss Franc and Canadian Dollar. Meanwhile, Japanese Yen lags as the weakest performer, trailed by the Dollar and New Zealand Dollar, with Sterling and Euro positioned in neutral territory. However, the lack of clear directional movement reflects the ongoing consolidative phase.

Today’s primary focus will be on Canada’s inflation data. October’s headline CPI is projected to rise to 1.9%, while CPI common is expected to remain steady at 2.1%. These results would reinforce expectations that the BoC will maintain its swift easing path, likely cutting rates again by 50 bps at its December 11 meeting. October’s BoC rate cut and minutes highlighted the need for aggressive easing due to labor market softness and a requirement to stimulate growth to absorb economic slack. Market participants anticipate this approach to continue.

Technically, a temporary top was formed at 1.4104 in USD/CAD with current retreat. But consolidations should be relatively brief as long as 1.3958 resistance turned support holds. Break of 1.4104 will resume larger up trend to 61.8% projection of 1.3418 to 1.3958 from 1.3841 at 1.4175. However, firm break of 1.3958 will indicate that lengthier consolidation is underway, with risk of deeper pullback to 1.3841 cluster support (38.2% retracement of 1.3418 to 1.4104 at 1.3842).

In Asia, at the time of writing, Nikkei is up 0.36%. Hong Kong HSI is up 0.03%. China Shanghai SSE is down -0.92%. Singapore Strait Times is up 0.73%. Japan 10-year yield is down -0.0055 at 1.071. Overnight, DOW fell -0.13%. S&P 500 rose 0.39%. NASDAQ rose 0.60%. 10-year yield fell -0.014 to 4.414.

RBA minutes highlight need for multiple good quarterly inflation reports before easing

In the minutes from the November meeting, RBA emphasized “minimal tolerance” for a prolonged period of high inflation, acknowledging the already “lengthy period” of elevated prices. They underscored the need to observe "more than one good quarterly inflation outcome" before concluding that a sustainable disinflation trend was underway.

Members discussed various scenarios that could challenge the forecasts, necessitating adjustments in policy.

One critical scenario revolved around weaker consumption. If consumption proved “persistently and materially weaker” than anticipated and threatened to significantly lower inflation, RBA suggested that a rate cut might be warranted. Conversely, stronger recovery in consumption could mean the current monetary stance would need to "remain in place for longer".

The labor market also featured prominently in deliberations. Should employment conditions ease more sharply than expected, resulting in rapid disinflation, the Board acknowledged that looser monetary policy might become appropriate. On the other hand, if the economy’s supply capacity turned out to be “materially more limited” than assumed, a tighter stance could be required.

External risks were also assessed, including potential major shifts in US economic policy following the presidential election, uncertainty around the scope of China’s anticipated stimulus measures, and the broader implications of rising global government debt levels.

BoE’s Greene cautions against aggressive rate cuts amid persistent services inflation and wage growth

BoE MPC member Megan Greene warned during an event overnight that services inflation remains stubbornly high, with wage growth exceeding levels consistent with the 2% inflation target. “There’s some risk that wage growth might be stickier than we would hope,” she said, adding that this could keep both services and overall inflation elevated.

Greene emphasized the importance of a cautious approach, stating that “the risk of cutting too early or too aggressively is a greater risk than going a bit more slowly.”

Feedback from firms suggests wage growth could settle closer to 4%, well above the desired level. Companies may respond to higher costs by increasing prices, reducing employment or hours, investing in productivity-enhancing capital, or absorbing costs into profit margins, she noted.

She also highlighted the UK’s vulnerability to external shocks as an open economy. “Historically speaking, about a third of the moves in our curve in the UK were influenced by things happening outside the UK. Now it’s about half.”

Greene pointed to the outsized influence of the US Treasury curve, describing it as a “drunken dragon” that heavily impacts the UK market, especially amid global geopolitical risks and shifts in US economic policy under the president-elect.

Looking ahead

Eurozone CPI final and Swiss trade balance will be released in European. Canada CPI will take center stage later in the day. US will release building permits and housing starts.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6253; (P) 1.6307; (R1) 1.6340; More...

EUR/AUD weakens notably after failing to sustain above 55 D EMA, but downside is held well above 1.6161 temporary low. Intraday bias stays neutral and risk remains on the downside for the moment. On the downside, below 1.6161 will target a test on 1.5996/6002 key support zone. Nevertheless, break of 1.6359 will turn bias to the upside for stronger rebound towards 1.6598 resistance instead.

In the bigger picture, as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still expected to resume through 1.7180 at a later stage. However decisive break of 1.5996 will argue that the medium term trend might have reversed. Deeper fall would be seen to 61.8% retracement of 1.4281 (2022 low) to 1.7180 at 1.5388, even as a correction.

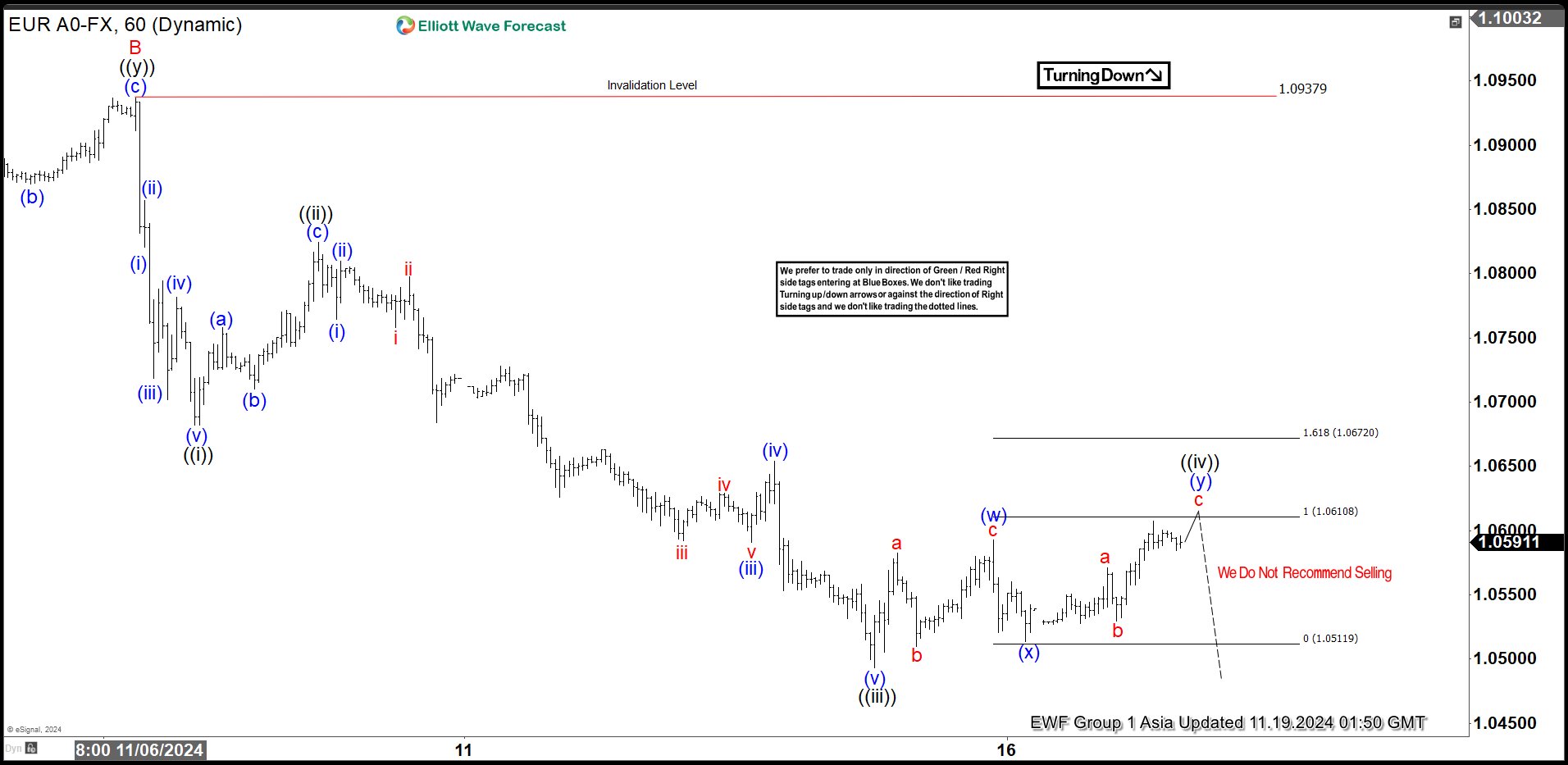

Elliott Wave View Looking Further Downside in EURUSD

Short Term Elliott Wave View in EURUSD suggests cycle from 9.25.2024 high is in progress as a zigzag. Down from 9.25.2024 high, wave A ended at 1.076 and wave B rally ended at 1.09369. Wave C lower is in progress as a 5 waves impulse Elliott Wave structure. Down from 11.6.2024 high, wave (i) ended at 1.082 and wave (ii) rally ended at 1.0857. Wave (iii) lower ended at 1.0718 and wave (iv) ended at 1.078. Wave (v) lower ended at 1.0682 which completed wave ((i)) in higher degree. Rally in wave ((ii)) ended at 1.0825 with internal subdivision as a zigzag.

Pair then turned lower in wave ((iii)). Down from wave ((ii)), wave (i) ended at 1.076 and rally in wave (ii) ended at 1.0809. Pair resumed lower in wave (iii) towards 1.059 and rally in wave (iv) ended at 1.0654. Pair extended lower 1 more time in wave (v) towards 1.0493 which completed wave ((iii)) in higher degree. Wave ((iv)) is in progress as a double three Elliott Wave structure. Up from wave ((iii)), wave (w) ended at 1.0593 and pullback in wave (x) ended at 1.0513. Expect wave (y) higher to complete at 1.061 – 1.067 area and this should complete wave ((iv)) in higher degree. From there, expect the pair to extend lower.

EURUSD 60 Minutes Elliott Wave Chart

EURUSD Elliott Wave Video

https://www.youtube.com/watch?v=rZrMUvzElMY

RBA minutes highlight need for multiple good quarterly inflation reports before easing

In the minutes from the November meeting, RBA emphasized “minimal tolerance” for a prolonged period of high inflation, acknowledging the already “lengthy period” of elevated prices. They underscored the need to observe "more than one good quarterly inflation outcome" before concluding that a sustainable disinflation trend was underway.

Members discussed various scenarios that could challenge the forecasts, necessitating adjustments in policy.

One critical scenario revolved around weaker consumption. If consumption proved “persistently and materially weaker” than anticipated and threatened to significantly lower inflation, RBA suggested that a rate cut might be warranted. Conversely, stronger recovery in consumption could mean the current monetary stance would need to "remain in place for longer".

The labor market also featured prominently in deliberations. Should employment conditions ease more sharply than expected, resulting in rapid disinflation, the Board acknowledged that looser monetary policy might become appropriate. On the other hand, if the economy’s supply capacity turned out to be “materially more limited” than assumed, a tighter stance could be required.

External risks were also assessed, including potential major shifts in US economic policy following the presidential election, uncertainty around the scope of China’s anticipated stimulus measures, and the broader implications of rising global government debt levels.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Hybrid – 4 and 5 November 2024

Members participating

Michele Bullock (Governor and Chair), Andrew Hauser (Deputy Governor), Ian Harper AO, Carolyn Hewson AO, Steven Kennedy PSM, Iain Ross AO, Elana Rubin AM, Carol Schwartz AO, Alison Watkins AM

Others participating

Sarah Hunter (Assistant Governor, Economic), Christopher Kent (Assistant Governor, Financial Markets)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Meredith Beechey Osterholm (Future Hub), Sally Cray (Chief Communications Officer), David Jacobs (Head, Domestic Markets Department), Michael Plumb (Head, Economic Analysis Department), Penelope Smith (Head, International Department)

International economic conditions

Members began their discussion by noting that the central forecast for global economic growth had not changed significantly over the prior three months. Average GDP growth for Australia’s major trading partners was expected to be moderate. Inflation had declined to be close to targets across most advanced economies, and many central banks had reduced the extent of policy restrictiveness as their attention began to shift to downside risks to activity, labour markets and inflation.

Output growth in China had been weak recently, but the outlook had been upgraded following the announcement of a range of policy stimulus measures by Chinese authorities. This stimulus had also reduced some of the downside risks to growth in China, which members had discussed at previous meetings, though other downside risks remained. Financial asset prices in China had increased sharply in response to the announcement of the stimulus package. At the same time, the property market in China and property developers’ balance sheets remained very weak. Along with weaker real income growth, this was weighing on the confidence of households in China and on housing credit growth there.

Members considered various channels through which economic stimulus in China could support the Australian economy. They concluded that the implications for Australia could be more modest than in the past because the capacity of the mining sector to increase Australia’s volume of mineral exports was limited. Moreover, it was unlikely that the sector would invest as heavily to expand this capacity as it had in the past, and the gains from any rise in the terms of trade were expected for the most part to be saved.

Members considered various forward-looking factors that could affect the global economic outlook. One of these was the possibility of a marked change in US economic policy following the US presidential election, the outcome of which would be known after the meeting. Members noted that the effects of the candidates’ policy proposals were difficult to quantify and would also depend significantly on the outcome of the Congressional elections, the extent and speed of implementation, and on how other countries respond. A wide range of alternative outcomes was possible; some scenarios involved significantly lower global growth and increased inflationary pressures, but the implications of others for global growth were more uncertain. The implications for the Australian economy of the scenarios with limited global reaction could ultimately be quite modest because of the potential for trade flows to be redirected, as had been observed in the past. Members noted that, whatever the election outcome, US fiscal deficits were forecast to be large, making sovereign debt markets more sensitive to adverse shocks over time.

Domestic economic conditions

Turning to the domestic economy, members noted that GDP growth had been subdued in the June quarter but looked to have picked up since then. The staff’s medium-term forecast for the level of GDP had been lowered slightly since August. Output growth was expected to pick up gradually to around its potential rate by late 2025.

A range of higher frequency data tentatively suggested that household consumption growth (excluding the effect of energy rebates on measured household expenditure) had increased in the September quarter. However, that projected increase was a little less than forecast in August and followed a surprisingly weak outcome in the June quarter. Members discussed the signal for medium-term consumption outcomes that should be drawn from these indicators, along with insights from liaison on the experience of various retailers and the subdued level of consumer sentiment. The staff forecast was still for a sustained pick-up in household consumption from the second half of 2024, in response to rising real household incomes, but this was expected to occur a little later than had been anticipated in August.

The outlook for services exports had been revised down significantly, reflecting the expected impact of tighter international student visa policies. However, this had not materially affected the staff’s assessment of the gap between aggregate demand and aggregate supply because lower net overseas migration would also reduce the economy’s supply capacity. Members noted the staff’s judgement that the gap between aggregate demand and aggregate supply was still positive but had narrowed. It would become more difficult to have confidence that this gap was positive, however, as the economy and labour market move closer towards balance.

Members assessed that labour market conditions remained tight relative to full employment. While conditions had continued to ease gradually, and the unemployment rate had drifted upwards as expected, employment growth had been strong and a number of indicators – including measures of underemployment, youth unemployment, job advertisements and surveys of labour availability – suggested that the easing in the labour market might have begun to stall or modestly reverse. Members contrasted these indicators with others, such as employment intentions, which had been more subdued. Against this backdrop, members noted that the risks of a rapid deterioration in labour market conditions might have diminished somewhat, though such a scenario could not be ruled out. The forecast was still for the unemployment rate to increase gradually before stabilising around levels consistent with full employment by late 2025.

Members considered the implications of the contrast between subdued growth in output and continued strong growth in employment (which implied weak productivity growth). This disparity may partly have reflected a significant share of growth in employment over the prior year having been in non-market sectors, where the approach to measuring productivity means estimated growth is limited by definition. However, members observed that productivity outcomes in the market sector had also been weak by historical standards, especially in construction and mining. Some part of this was likely to be attributable to a decline in the capital-to-labour ratio, as investment has not kept pace with unexpectedly strong employment growth. Members considered the implications of these outcomes for the staff’s long-run productivity growth assumption. They also discussed the interaction between future productivity outcomes and wages. Growth in wages and labour costs were forecast to moderate further to levels consistent with inflation being at target, but members noted that wages growth would need to slow even further to enable a return to the inflation target if productivity growth does not increase as assumed.

Turning to inflation, headline CPI inflation had fallen sharply in the September quarter because of electricity rebates and declining fuel prices. Underlying inflation – which members agreed provides a better indicator of inflation momentum – had remained high (at 3.5 per cent) and was declining more slowly. Growth in advertised rents had slowed more than expected in preceding months, which would flow through to lower CPI rent inflation over time.

Looking ahead, headline inflation was forecast to remain temporarily within the 2–3 per cent target range until the September quarter 2025, when the scheduled end to energy rebates would see it pick up. Inflation was not expected to return sustainably to the target until 2026, as the level of aggregate demand and aggregate supply move into better balance. Members noted that the outlook for underlying inflation was little changed since the August meeting, with services inflation projected to decline alongside further gradual easing in labour market conditions and an expectation that goods prices would continue to rise at a modest pace.

Annual review of staff forecasts

Members discussed the staff’s annual forecast review and drew a number of lessons.

In line with the forecasts published in the November 2023 Statement on Monetary Policy, underlying inflation and the unemployment rate had evolved largely as expected. However, underlying inflation outcomes over the prior two years had generally been higher than earlier forecasts and quarterly outcomes for underlying inflation since late 2023 had pointed to the relatively slow progress in reducing inflation.

GDP growth had been significantly weaker than forecast a year earlier. That reflected weaker-than-anticipated growth in private demand, partly offset by stronger growth in public demand. Members noted that the staff’s projections for public demand were based on budgeted expenditure by federal and state governments that had been announced at the time the forecasts were prepared.

Taken together, the weaker GDP outcomes, persistence in underlying inflation and the rate of unemployment being broadly as forecast had suggested that the economy’s supply capacity was less than projected a year earlier. This was consistent with weaker-than-expected measured labour productivity and had motivated the staff to revise downwards their assessment of full employment, as set out in the August 2024 Statement on Monetary Policy.

Financial conditions

Members commenced their discussion of financial conditions by noting that central banks in many advanced economies had reduced their policy rates over prior months and that further rate cuts were expected. Central banks had been responding to potential downside risks in labour market conditions and increased confidence that inflation was sustainably returning to central banks’ targets.

Members observed that policy interest rates in most other advanced economies were still assessed to be restrictive relative to those central banks’ published estimates of neutral rates, and more restrictive than monetary policy in Australia. They discussed some of the factors that could cause estimates of neutral nominal interest rates to vary across countries – including differences in inflation targets and potential growth rates – and the weight to place on such estimates in policymaking. Looking ahead, market participants still expected that policy rates in most countries, including Australia, would approach estimated neutral levels by around the end of 2025. However, expectations for the path of policy rates in some advanced economies had shifted upwards since the September meeting, in response to indicators that had allayed concerns emerging in August that economic growth may be turning down sharply, especially for the United States.

Longer term government bond yields in most advanced economies had also increased. This may have been driven in part by market perceptions that a ‘soft landing’ scenario was increasingly likely, coupled with upward pressure on term premia and long-term market-based inflation compensation. Members discussed the extent to which these latter effects may have been associated with geopolitical tensions and the implications of potential changes to economic policies following the US elections. In many economies, yield curves had become upward sloping after a period of being inverted; by contrast, those in Australia and Japan had remained upward sloping over the preceding year.

A range of other measures implied that global financial conditions had eased over prior months, as volatility had subsided and risk premia had declined. Corporate bond yields in the United States and Europe had declined to year-to-date lows, partly reflecting a narrowing of spreads to sovereign bonds. Prices of riskier assets had generally increased in advanced economies since early August. The rise in equity prices had been driven by an increase in expectations of future earnings in the United States and a decline in equity risk premia elsewhere. Members noted the potential for market volatility at some point following the US presidential election.

Members judged that Australian financial conditions remained restrictive overall, although there had been a modest easing in some indicators over preceding months. Housing credit growth had risen further and business credit growth had remained above its long-run average. Members observed that this was somewhat unusual in a period of monetary policy tightness, and that it perhaps reflected banks being well positioned to continue supplying credit to the economy. However, they also noted that credit had not been rising as a share of nominal household disposable income (in the case of housing credit) or nominal GDP (in the case of business credit). Scheduled mortgage and consumer credit payments remained high but were no longer increasing as a share of nominal household disposable income.

Market expectations for the path of the cash rate had risen since the September meeting, in response to signs of persistent strength in the labour market and expectations of somewhat less accommodative monetary policy in the United States. Market pricing suggested that participants now expected the Board to start reducing the cash rate target from around mid-2025, a few months later than at the time of the September meeting. Market economists also expected the first reduction in the cash rate target to occur in the first half of 2025. Members noted that market pricing and economists’ expectations were for a more gradual pace of rate cuts than expected in several other advanced economies.

The Australian dollar trade-weighted index had continued to trade within the range observed since early 2022. An initial appreciation of the exchange rate from its recent low in August had been consistent with a rise in yield differentials between Australia and its major trading partners, and the announcement of a stimulus package in China. However, it was likely that the effect of these factors on the Australian dollar had been offset more recently by the implications of potential policy changes following the US elections, including the possibility that significant tariffs would be imposed on Chinese exports.

Considerations for monetary policy

Turning to considerations for the immediate policy decision, members noted that much of the information received since the September meeting had been consistent with expectations of the Board and staff, which had been broadly true at the time of the September meeting too. As a result, the staff’s updated forecasts were very similar to those published in August. The risks surrounding the forecasts were also still judged to be balanced.

Inflation had been declining over the prior year, driven most recently by lower fuel prices and the expected fall in electricity prices. However, members observed that underlying inflation – as indicated by the ‘trimmed mean’ measure – remained too high and that the staff forecasts did not see inflation returning sustainably to target until 2026. Employment growth had been strong and some of the forward indicators of conditions in the labour market had stabilised or strengthened. However, GDP growth had remained subdued, largely reflecting weakness in private consumption. The staff forecast was for a strengthening in consumption growth to underpin a recovery in GDP growth to around estimates of the potential growth rate over the coming year, and for the unemployment rate to stabilise around the staff’s estimates of full employment from late 2025.

Monetary policy in Australia was assessed to be restrictive. However, the degree to which this was the case remained uncertain and broader financial conditions had eased somewhat over preceding months. Members noted that the staff forecasts were conditioned on a technical assumption – derived from market pricing – that the cash rate target would remain at its current level for a number of months before being lowered several times in 2025 and 2026.

Members agreed that, based on these considerations, it was appropriate to leave the cash rate target unchanged at this meeting. The economy appeared to be evolving in line with earlier expectations, and the staff forecasts were consistent with the Board’s strategy of aiming to return inflation to target within a reasonable timeframe while preserving as many of the gains in the labour market as possible. Members observed that these outcomes were predicated on a technical assumption for the cash rate that did not incorporate any change in the near term. Taken together, these observations suggested that there was no immediate need to change the cash rate target.

At the same time, members recognised it was important to be ready to adjust the future stance of monetary policy as the economic outlook evolves. Members therefore considered the conditions that might warrant either a future change in the cash rate target or a decision to hold it at its present level for a prolonged period. Members agreed that it was important to keep monetary policy sufficiently restrictive until the Board is confident that inflation is moving sustainably towards the target. They noted too that it is important to remain forward looking, avoiding an excessive reliance on backward-looking information that might lead the Board to react too late to a change in economic conditions.

Members discussed a number of potential scenarios in which the key judgements underlying the forecasts proved incorrect, consequently warranting an adjustment in monetary policy.

One set of scenarios centred around the judgement on consumption. Members agreed that if consumption proves to be persistently and materially weaker than the staff forecast, and this was judged likely to lower inflation significantly, a reduction in the cash rate target could be warranted. Members noted various reasons why consumption might be weaker: consumer sentiment, though higher than a year earlier, was still low by historical standards; and data available for the September quarter suggested there had not yet been a significant increase in consumption growth, even as household cash flows had been supported by the Stage 3 tax cuts and energy rebates. At the same time, members highlighted that the current monetary policy setting might need to remain in place for longer than assumed if the recovery in consumption proved sharper than the forecast envisaged. They noted that such an outcome could occur in response to the increase in household wealth over preceding years, the emerging recovery in real household income and nascent signs of an upturn in consumer sentiment. More generally, members noted scenario modelling by staff in which materially stronger-than-expected demand placed greater upward pressure on underlying inflation, requiring the current policy setting to remain in place for an extended period.

Members discussed scenarios in which the judgement about the labour market proved incorrect and conditions eased materially more sharply than expected, in turn lowering inflation more rapidly and warranting a looser monetary policy stance. This could occur if firms are currently hoarding labour and are prompted to unwind this stance in the future. Members recounted instances of firms either laying off staff or intending not to fill vacancies as they arise. Such trends were not yet widely apparent from the RBA’s liaison with firms, but members observed that if forward-looking indicators began to suggest a widespread easing in prospective labour market conditions and a more rapid easing in inflation, the Board might need to consider a policy response.

Members also considered scenarios in which it became evident that the supply capacity of the economy was materially more limited than assumed in the forecasts, necessitating a tighter monetary policy stance. Members observed that this could be the case if the staff’s assessment of the economy’s current potential growth rate was too optimistic or if productivity growth over coming years fell short of that assumed in the forecasts. They noted that persistent weakness in productivity growth would not only erode long-run real income growth but could also boost inflation over the forecast period if wages growth did not adjust in a sufficiently timely manner.

More generally, members noted that, given the already lengthy period in which inflation had been above target, the Board has minimal tolerance to accommodate a more prolonged period of high inflation, even if this occurred because of factors that constrained the economy’s supply capacity. However, there were also scenarios in which inflation declined materially more quickly than currently forecast, perhaps in response to emerging signs that rental housing markets in many cities were moving into better balance or because the energy rebates have a more pervasive effect than factored in (e.g. if they have a broader effect on inflation expectations or price indexation than staff expect). Members noted that this could warrant an easing in the cash rate target, but that they would need to observe more than one good quarterly inflation outcome to be confident that such a decline in inflation was sustainable.

Members also discussed a range of particular risks from abroad that could result in the forecasts being materially wrong and therefore have important implications for monetary policy. These included the potential for major changes in US economic policy following the presidential election, the prospect of the size or composition of the stimulus package foreshadowed by Chinese authorities differing from expectations, and the more general risk of unsustainable growth in global government debt. Members agreed that it was not yet possible to factor in events such as these, given pertinent details were unknown and still largely unpredictable, but that this would need to be done if these risks eventuated.

Finally, members noted that monetary policy might need to be adjusted if the Board formed the view that the stance of policy was not as restrictive as had been judged. They agreed that it was important to pay close attention to potential signs of this, including developments in credit growth, banks’ willingness to lend and growth in asset prices.

In finalising the Board’s statement, members agreed that it was important to convey that the Board remained vigilant to upside risks to inflation. They also affirmed that monetary policy would need to be sufficiently restrictive until members are confident that inflation is moving sustainably towards the target. Based on the information available at the time of the meeting, members agreed that it was not possible to rule anything in or out in relation to future changes in the cash rate target. Members would rely upon the data and the evolving assessment of risks to guide the Board’s future decisions. Returning inflation to target remains the Board’s highest priority and it will do what is necessary to achieve that outcome.

The decision

The Board decided to leave the cash rate target unchanged at 4.35 per cent, and the interest rate on Exchange Settlement balances unchanged at 4.25 per cent.