Sample Category Title

Temporary Dollar Dip or Intrinsic Euro Strength?

The Dollar Index is retreating from Thursday’s highs, moving against the logic of fundamental forces. This behaviour begs the question: either the Dollar Index has reached the limits of its range, or this is an extended shake-out of positions after a prolonged rally.

The DXY rallied to 106.99 last Thursday, almost repeating the October 2023 highs of 107.04. The recent highs were slightly above the April peak this year, making 107 a serious resistance area. There is a significant battle going on here in the dollar between the bulls and bears, the outcome of which could determine the trend for weeks or months to come.

The resistance is so significant that it goes against the major trends of recent days. At the end of last week, Fed Chairman Powell said that the central bank was in no hurry to cut interest rates. As a result, interest rate futures are already pricing in more than a 40% chance of no change, whereas there was no doubt at the beginning of October. The pullback in equity indices also clearly showed how much the markets took the central bank chief’s words to heart.

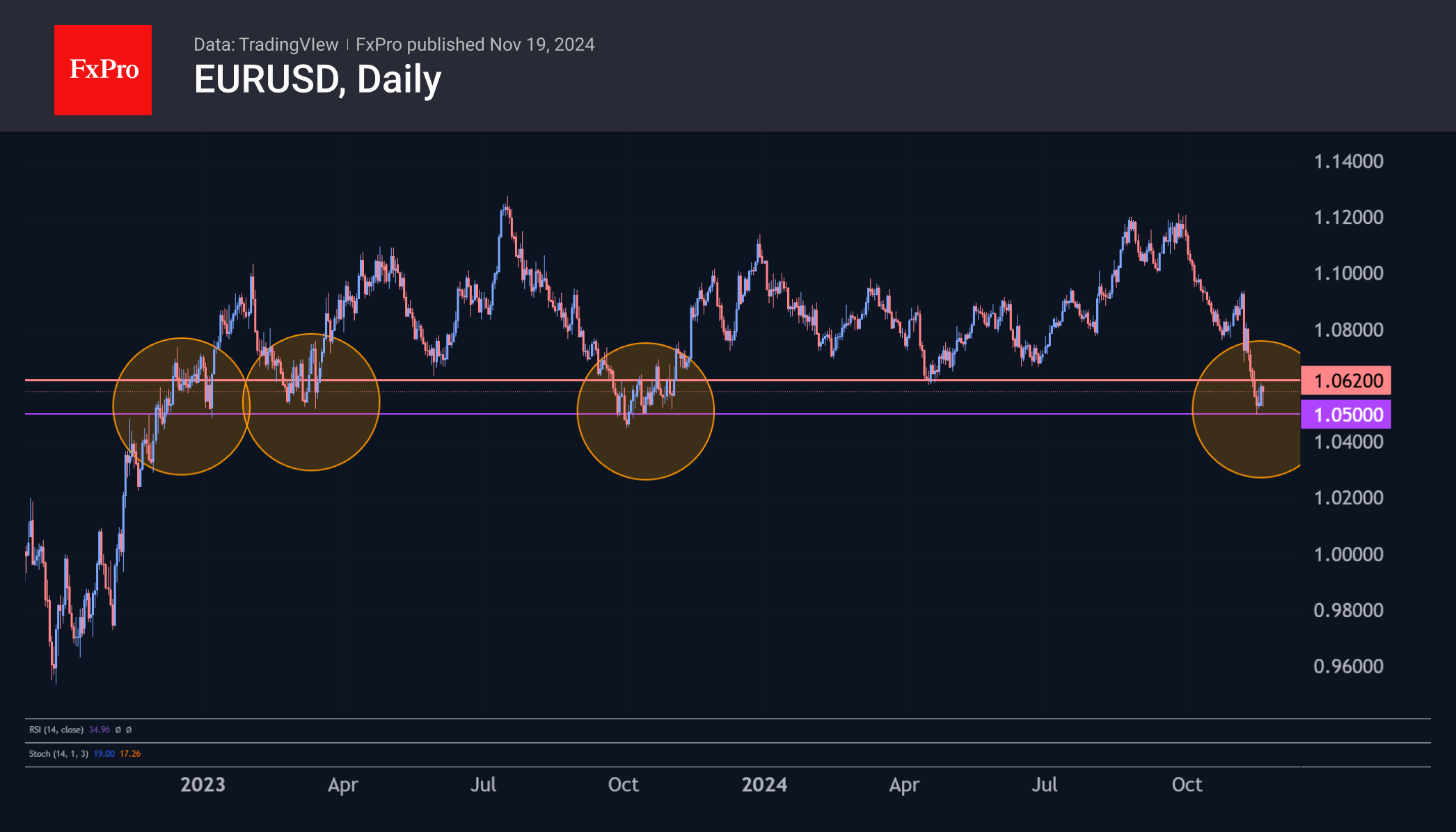

The authorisation of US missile strikes deep into Russia, and the retaliatory escalation of rhetoric also led to a pullback in defensive assets, helping gold and the yen, but not the dollar, which has not fallen below 1.05 in EURUSD terms. However, in the current geopolitical environment and amid expectations of tariff wars with the US, it isn’t easy to see the euro as a safe-haven.

In our view, EURUSD holding above 1.05 looks like a technical correction and a liquidity pick-up after a 6% fall since early October. As the odds of no change in US interest rates continue to rise, the dollar can build up potential that is still constrained by the local overbought condition of the US currency.

However, the ball is now in Europe’s court. On Wednesday, it is worth listening to Lagarde and the ECB’s biannual assessment of financial stability. On Friday, it is also worth paying attention to another speech by Lagarde entitled ‘Out of the Comfort Zone…’ and the preliminary PMI estimates for November, which have often been the driving force behind the euro’s movement and could now indicate either a light at the end of the tunnel or a further plunge.

Sunset Market Commentary

Markets

Geopolitics rattled markets otherwise on track for an uninspired trading session. Russian president Putin signed off a revised nuclear doctrine, expanding the conditions for the use of atomic weapons. Russia could now retaliate in case of a (conventional) attack on its soil. Making good on the pledge made by Putin back in September, Russia will view aggression against itself or its allies by a non-nuclear state backed by a nuclear power as a joint attack. The revision doesn’t come out of the blue: it follows the outgoing US Biden administration giving Ukraine green light for the limited use of American-made long-range ATACMS missiles. This was in turn a response to North Korea’s agreement to deploy its forces in support of Russia and to increased Russian missile and drone attacks on Ukraine. Less than an hour after the updated doctrine, reports rolled in of Ukraine conducting such a first ATACMS strike. Russian minister of foreign affairs called it “a signal of escalation”. Risk-off rolled over markets. Both US Treasuries and German bunds rallied, the former outperforming. Both trade well off the intraday highs, though. US yields drop between 3.4-4.7 bps. German yields lose 2.5-3.4 bps across the curve compared to initial losses of <10 bps. European stocks take a 1.7% hit (EuroStoxx50) while Wall Street opens about 0.50% lower. The Japanese yen and Swiss franc take the lead on the G10 currency scoreboard. USD/JPY fills bids around 153.6. JPY gains against the euro are slightly bigger, bringing down the EUR/JPY pair to its 50dMA around 162.4. EUR/CHF came close to the 0.93 but without really testing the big figure. It is nevertheless on track for the lowest close since the August market meltdown. Natural gas prices (Dutch TTF) temporarily jumped to a new one-year high before easing a bit later in the session. Gold prices printed the first back-to-back rise since end-October. The precious metal is currently being sold for over $2635 per ounce. While geopolitics usually have a limited shelf-life, the topic may continue to draw market attention during the economic, political and monetary vacuum the coming days/weeks. Bank of England governor Bailey during his testimony before the UK parliament stuck to a “gradual” approach to rate cuts. Inflation returned faster than expected to target (temporarily though, red.) and there’s evidence of a loosening in the labor market, Bailey said. But he also saw risks of “lingering persistence” of wage pressures. The latter take center stage in Europe tomorrow, with the negotiated wage indicator (Q3) due. The Bundesbank already today disclosed German wages in Q3 having grown at the fastest pace in more than three decades (8.8%).

News & Views

The Riksbank’s first deputy Governor Anna Breman in a speech said that ‘inflation has fallen, and that conditions are good for inflation to remain close to the target even in the medium term.’ At the same time, Breman assesses that economic activity is not yet showing clear signs of strengthening. This combination justified accelerating the pace of rate cuts to 50 bps bringing the policy rate to 2.75%. On the recent inflation development (CPIF 1.5%; CPIF ex energy 2.1%) Breman said that “Energy prices are still contributing to CPIF inflation being below two per cent. At the same time, food prices have risen in in recent months. This is important to monitor, not least when a weak krona risks pushing up the price of imported food.” Still, Breman assesses that recent inflation data don’t change the view that inflation will remain low and stable in the medium term. If the outlook for inflation and activity remains the same, she sees the policy rate being cut further in December and during the first half of 2025. Markets currently more or less discount a 25 bps step in December and a policy rate being reduced to 2.0% by Q1 2025. The Swedish krone recently stabilized at weak levels (EUR/SEK 11.58).

Inflation in Canada in October rebounded more than expected. Headline CPI printed at 0.3% M/M and 2.0% Y/Y, to be compared to -0.4% M/M and 1.6% Y/Y in September, as gasoline prices fell less in October compared to September. CPI ex-gasoline was unchanged at 2.2%. Price of goods rose 0.1% Y/Y up from -1.0% Y/Y in September. On the other hand, services inflation decelerated to 3.6%, the smallest yearly rise since January 2022. The Bank of Canada’s preferred core measures increased to 2.5% (from 2.3%) and 2.6% from 2.4%. Markets reduced the chance of an additional 50 bps rate cut to about 30% from +40% at the start of the session. The BoC meets December 11. Gains of the Loonie against the US dollar look unconvincing. USD/CAD is hovering near the 1.40 barrier.

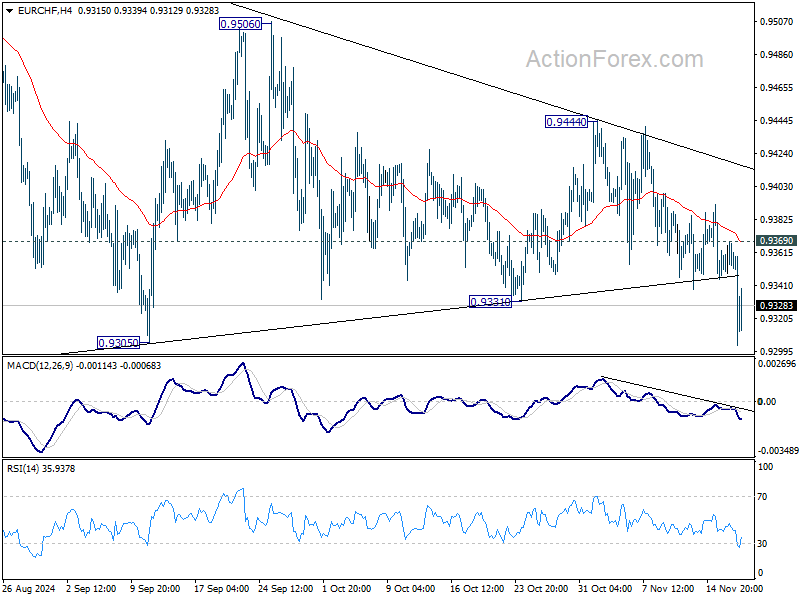

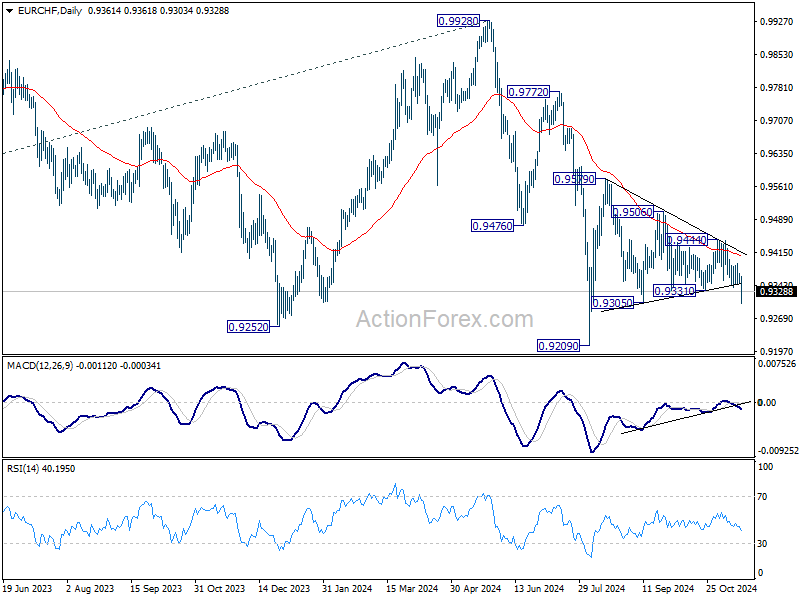

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9347; (P) 0.9358; (R1) 0.9372; More....

EUR/CHF's break of 0.9331 support suggests that triangle consolidation pattern from 0.9209 has completed. Intraday bias is now on the downside. Break of 0.9305 will target 0.9209 low next. On the upside, above 0.9369 minor resistance will dampen this view, and turn intraday bias neutral again.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9410) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming at 0.9209 and bring stronger rebound back towards 0.9928 key resistance.

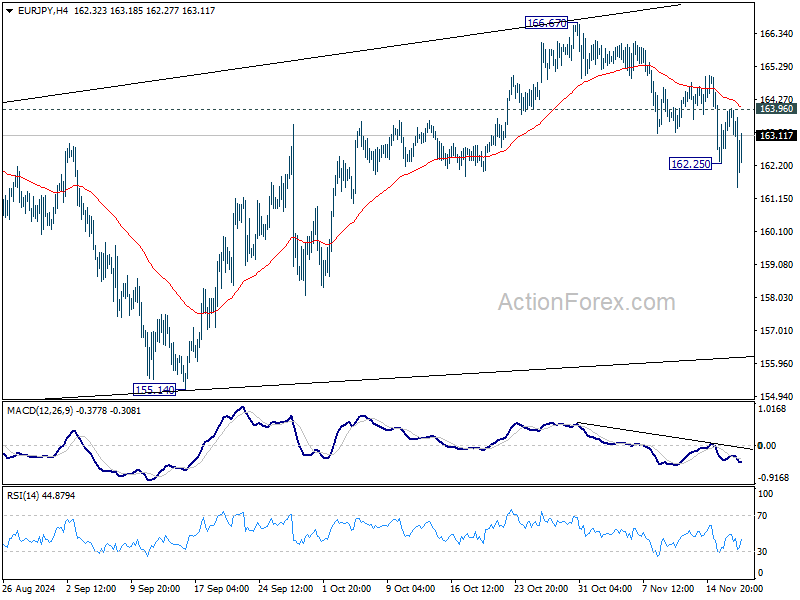

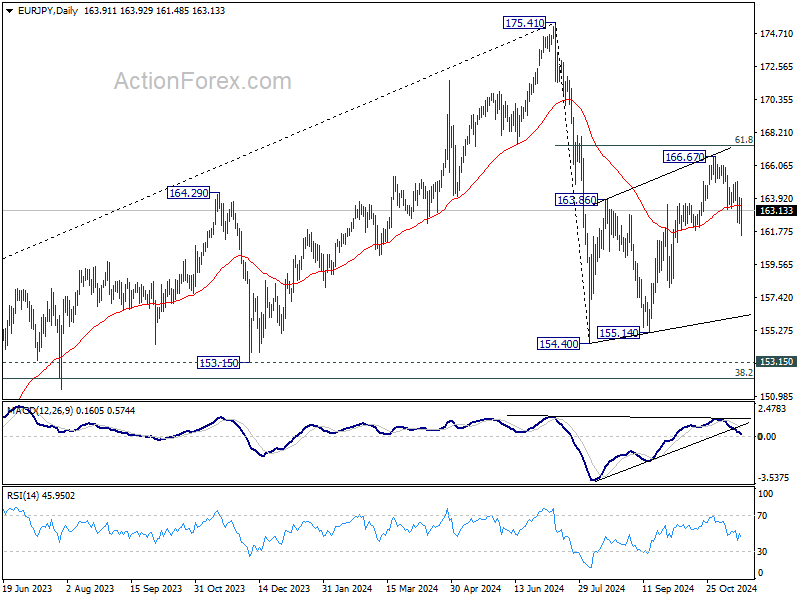

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 162.81; (P) 163.40; (R1) 164.52; More....

EUR/JPY's fall from 166.67 resumed after brief consolidations, and intraday bias is back on the downside. As noted before, corrective rebound from 154.40 could have completed with three waves up to 166.77 already, ahead of 61.8% retracement of 175.41 to 154.40 at 167.38. Deeper decline would be seen to 155.14 support next. On the upside, above 163.96 minor resistance will turn intraday bias neutral again.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

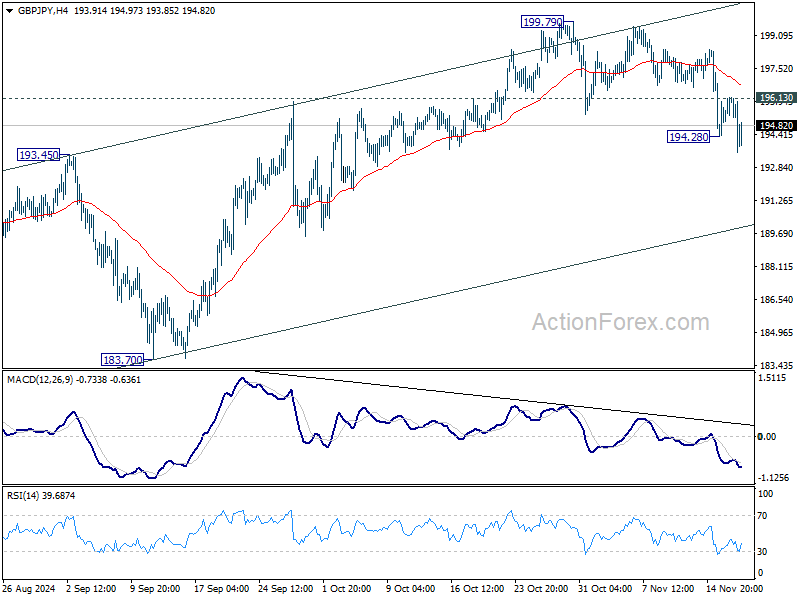

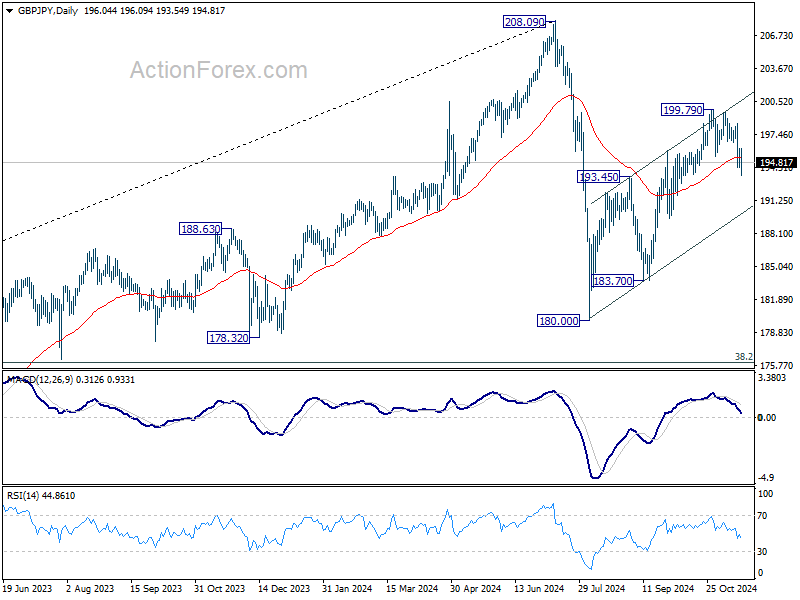

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 194.93; (P) 195.54; (R1) 196.71; More...

GBP/JPY's fall from 199.79 resumed after brief consolidations and intraday bias is back on the downside. As noted before, corrective rise from 180.00 could have completed with three waves up to 199.79, after hitting channel resistance. Break of 193.45 resistance turned support will target 183.70 next. On the upside, above 196.13 minor resistance will turn intraday bias neutral again.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

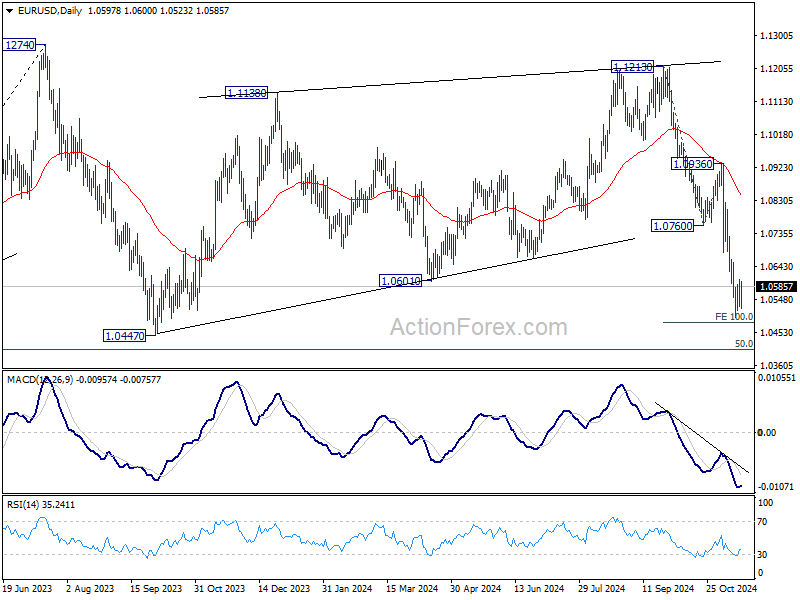

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0550; (P) 1.0578; (R1) 1.0627; More...

EUR/USD is staying in consolidation above 1.0495 temporary low and intraday bias remains neutral. Outlook will stay bearish as long as 1.0760 support turned resistance holds. On the downside, firm break of 1.0495 will resume the fall from 1.1213 to 1.0447 support and then 1.0404 key fibonacci level next.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage. However, firm break of 1.0404 will raise the chance of reversal and target 61.8% retracement at 1.0199.

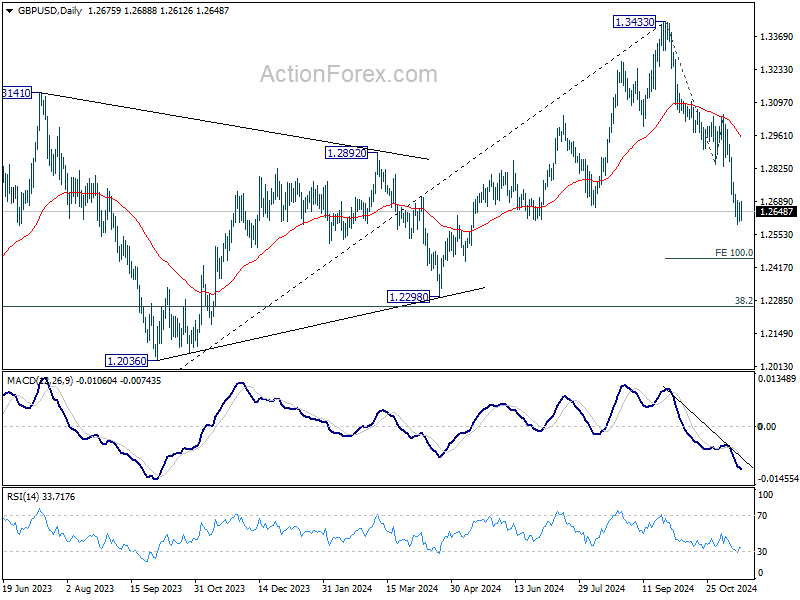

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2629; (P) 1.2658; (R1) 1.2707; More...

GBP/USD is staying in consolidations above 1.2596 temporary low and intraday bias remains neutral. Outlook will stay bearish as long as 12.842 support turned resistance holds. Break of 1.2596 will resume the fall from 1.3433 to 100% projection of 1.3433 to 1.2842 to 1.3047 at 1.2456.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2977) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

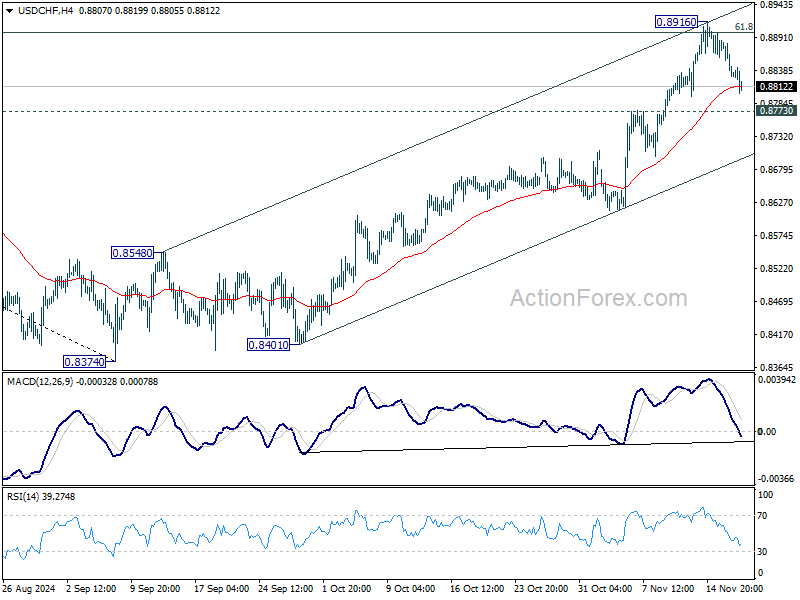

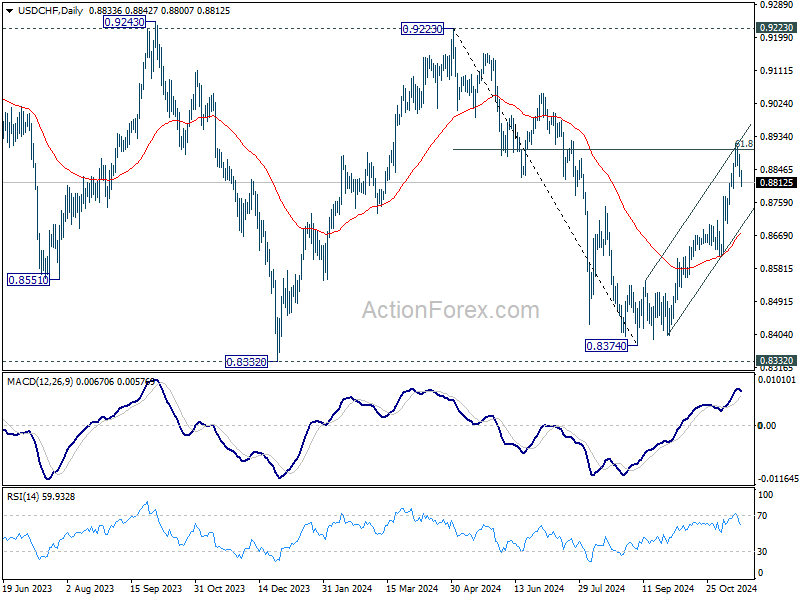

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8811; (P) 0.8850; (R1) 0.8871; More…

USD/CHF's retreat from 0.8916 extends lower today but stays above 0.8773 resistance turned support. Intraday bias remains neutral first and further rally is in favor. On the upside, break of 0.8916 and sustained trading above 61.8% retracement of 0.9223 to 0.8374 at 0.8899 will pave the way back to 0.9223 key resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

Canadian Inflation Jumps Higher in October

Headline CPI inflation increased in October to 2.0% year-on-year (y/y), above expectations for a 1.9% y/y print and up from the 1.6% y/y reading from September.

The acceleration was due to base-year effects on gasoline prices (the impact of price changes from a year ago falling out of the data), which were down 4.0% y/y, compared to down 10.7% y/y in September. Also pushing prices higher were food costs (2.7% y/y), which have been rising faster than overall inflation for three straight months.

Encouragingly, inflation in services has continued to ease (3.6% y/y from 4.0% y/y in September). Shelter costs have been a big driver of services inflation, but with lower interest rates, mortgage interest cost inflation has decelerated (14.7% y/y from 16.7% y/y in September), while rent inflation is also easing (7.3% y/y from 8.2% y/y in September).

The Bank of Canada's preferred "core" inflation measures increased to 2.6% y/y on average, from 2.4% y/y in September.

Key Implications

Today's data reinforced the message that the Bank of Canda's (BoC) goal of stabilizing inflation won't be a smooth path. While the increase in headline inflation was expected, the move higher in core inflation was discouraging. Even worse, on a three-month basis, core inflation moved from just above the BoC's target, at 2.1%, to 2.8%. That was a big move and points to core inflation remaining above the BoC's target in the coming months. High inflation for shelter, food, and health care were behind this, and aren't looking likely to go away any time soon.

The BoC is likely to view today's data release as a minor setback. Inflation had become a background worry, and while it isn't raising any red flags yet, today's data is a reminder that getting price growth to settle at 2% will take time. The BoC will also be getting a reading on Q3 GDP growth next week. That release will do a lot to help guide the central bank in deciding whether it will cut by 25 or 50 bps in December. We think that a 25 bp cut remains the most likely outcome, especially given the resilience that the economy has demonstrated over the last few months.

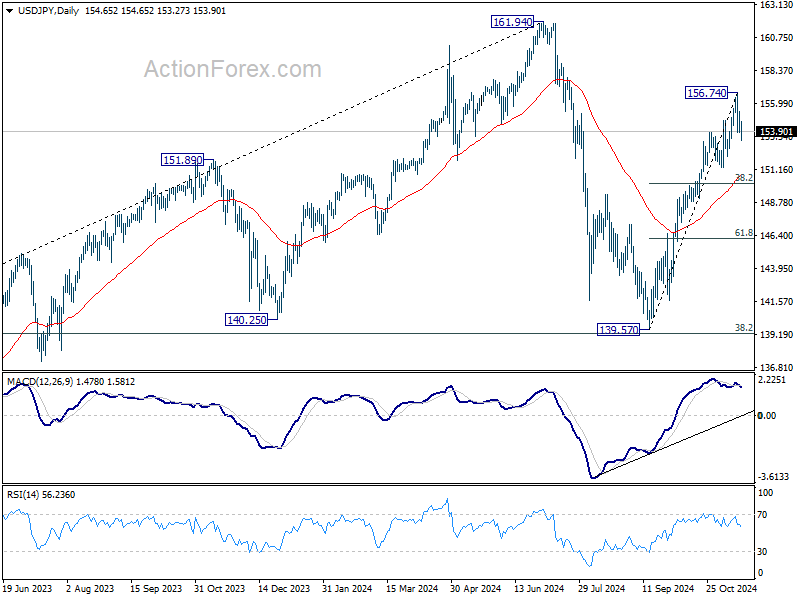

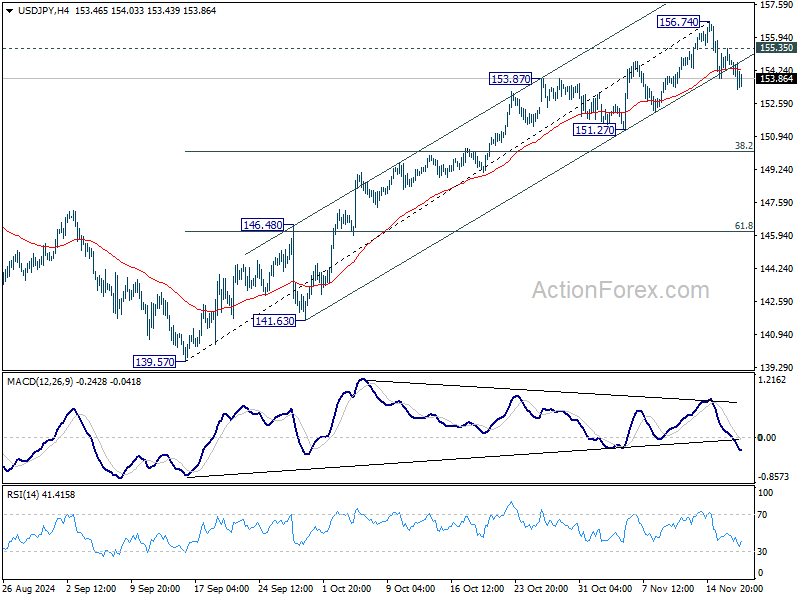

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 153.89; (P) 154.63; (R1) 155.41; More...

USD/JPY's break of 153.87 resistance turned support and rising channel suggest short term topping at 156.74. Intraday is back on the downside for pull back to 151.27, and possibly below. But strong support should emerge at 38.2% retracement of 139.57 to 156.74 at 150.18 to contain downside. On the upside, above 155.35 minor resistance will bring retest of 156.74 high instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.