Sample Category Title

UK Headline Inflation Accelerated Slightly More than Expected

Markets

Markets were on an emotional rollercoaster yesterday. The first Ukrainian use of US-made long range ATACMS missiles pushed Russian President Putin into signing off a revised nuclear doctrine. It now includes a possibility of a nuclear response to aggression by non-nuclear states that are supported by other nuclear powers. European stocks lost around 1.5% and hit an intraday bottom (-2%) after Russian minister of foreign affairs Lavrov called it a “signal of escalation”. European stock markets eventually recovered to closing losses of somewhat less than 1% after that same minister tried to calm worries over a nuclear escalation. “We are strongly in favor of doing everything not to allow nuclear war to happen. A nuclear weapon is first and foremost a weapon to prevent any nuclear war.” Haven assets mirrored the intraday sell-off/recovery from equities. German yields ended around 3.5 bps lower across the curve but traded with losses of up to 10 bps. US yields lost up to 2.8 bps in a bull flattening move. EUR/USD closed unchanged just below 1.06, but set an intraday bottom around 1.0530. US stock markets turned starting losses into closing gains (S&P & Nasdaq), mainly thanks to a near 5% increase in Nvidia shares going into tonight earnings from the company. The outcome will influence general market/risk sentiment and could set the tone going into year-end.

EMU Q3 negotiated wage data are today’s economic highlight. Annualized wage growth remained between 4.3% and 4.7% from Q1 2023 to Q1 2024. Last quarter’s decline to 3.5% was welcomed by the ECB in its inflation fight, but remains way above the central bank’s 2% inflation target. ECB Lagarde indicated that forward-looking wage trackers point to a an easing of pay growth in 2025 which she hopes to see reflected in today’s numbers. While a further deceleration is likely, we don’t think they will give sufficient confidence for the ECB to accelerate from 25 bps rate cuts to a 50 bps move in December. It could extend the short term bottoming-out process in EUR rates given that EMU money market still attach a small probability to such a scenario.

UK headline inflation accelerated slightly more than expected in October, by 0.6% M/M to 2.3% Y/Y. Core CPI remained stronger as well, rising by 0.4% M/M to 3.3% Y/Y (from 3.2%). Services CPI ticked up from 4.9% Y/Y to 5%. Today’s figures add strength to the Bank of England’s “not too many, not too much” rhetoric. Sterling strengthens marginally in a first reaction, from EUR/GBP 0.8350 to 0.8330.

News & Views

Hungary’s central bank (MNB) kept the policy rate unchanged at 6.5% yesterday. One dissenter voted for a rate decrease, potentially inspired by disappointing Q3 growth and the recent sharper-than-expected inflation decline. The MNB noted that this indicates lower inflation in the short term. But the “exchange rate depreciation seen in the past months as well as changes to the system of excise duties are likely to have inflationary effects in the next year.” The Monetary Council said the increase in risk aversion towards emerging markets was driven by geopolitics and changing growth and central bank expectations of developed economies. The MNB said these developments pose an upside risk to domestic inflation and considered a pause in the cutting cycle appropriate. “Looking ahead, a careful and patient approach to monetary policy is still warranted.”, the statement still says. Its deputy governor in the press conference afterwards stressed the importance of anchoring inflation expectations, which for households are “significantly” above the central bank’s 3% target range. He stuck to earlier guidance of maintaining the current policy rate for a “sustained period”. The Hungarian forint ended yesterday lower against the euro. EUR/HUF closed at 408.3. Hungarian swap yields dropped some 5 bps across the curve, be it in a pre-meeting move.

Austria is expected to give Romania and Bulgaria full accession to Europe’s Schengen zone, the FT reported. Air and maritime checks were already abandoned since end-March but Austria insisted on land border controls because of concerns over irregular migration. It is now ready to drop its veto after Romania and Bulgaria increased security checks, resulting in lower asylum applications and irregular migration. Barring a change-of-mind of the Dutch government, which gave green light in 2023 but now has the far-right Freedom party in the coalition, the matter can be formalized at the next EU home affairs meeting Dec 12. All restrictions may then be lifted at the start of 2025.

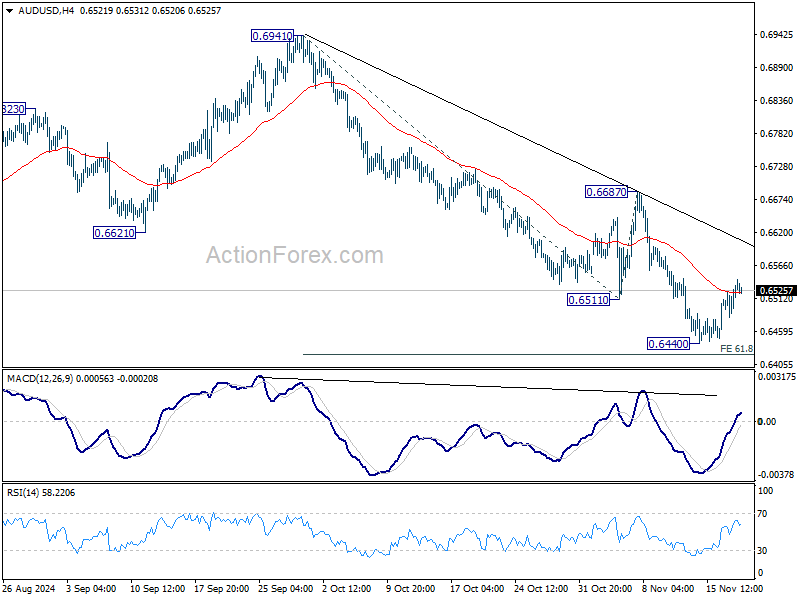

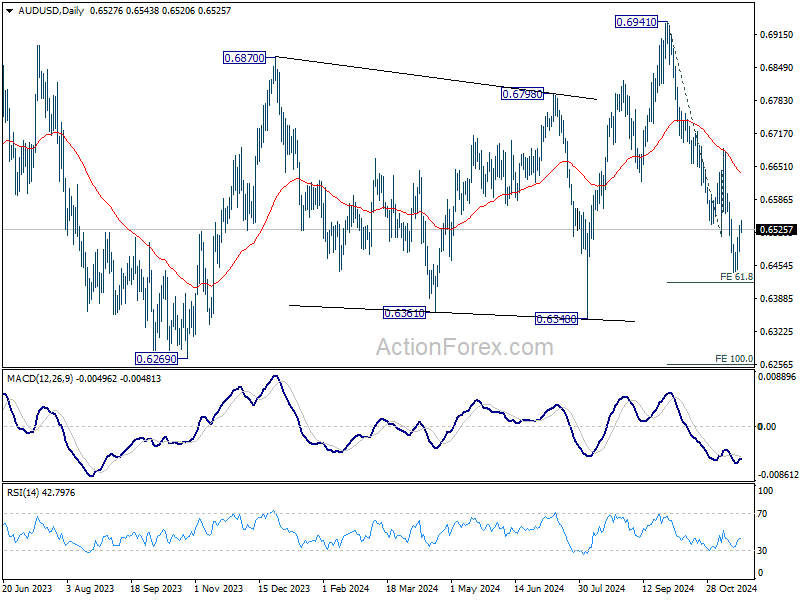

AUD/USD Daily Report

Daily Pivots: (S1) 0.6498; (P) 0.6516; (R1) 0.6551; More...

AUD/USD is extending consolidations from 0.6440 and intraday bias remains neutral. Outlook will stay bearish as long as 0.6687 resistance holds. On the downside, decisive break of 61.8% projection of 0.6941 to 0.6511 from 0.6687 at 0.6421 will resume the fall from 0.6941 to 100% projection at 0.6257 next.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

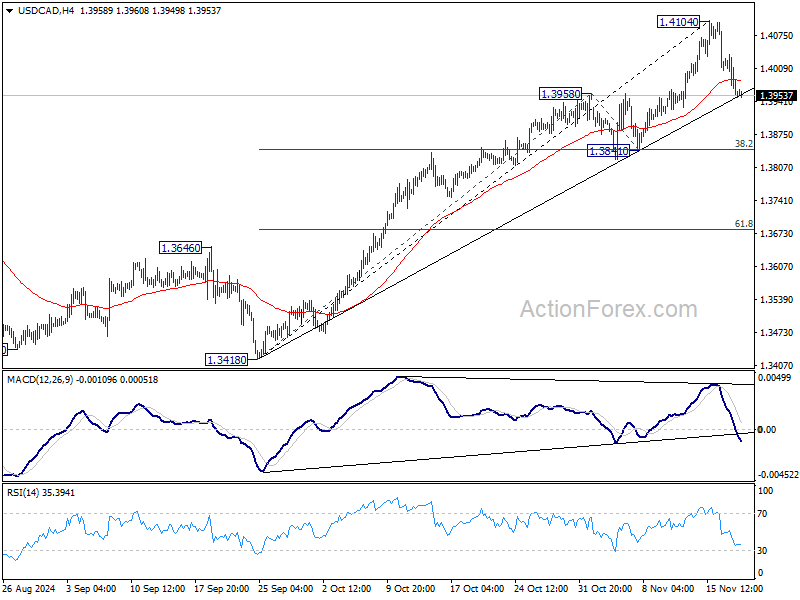

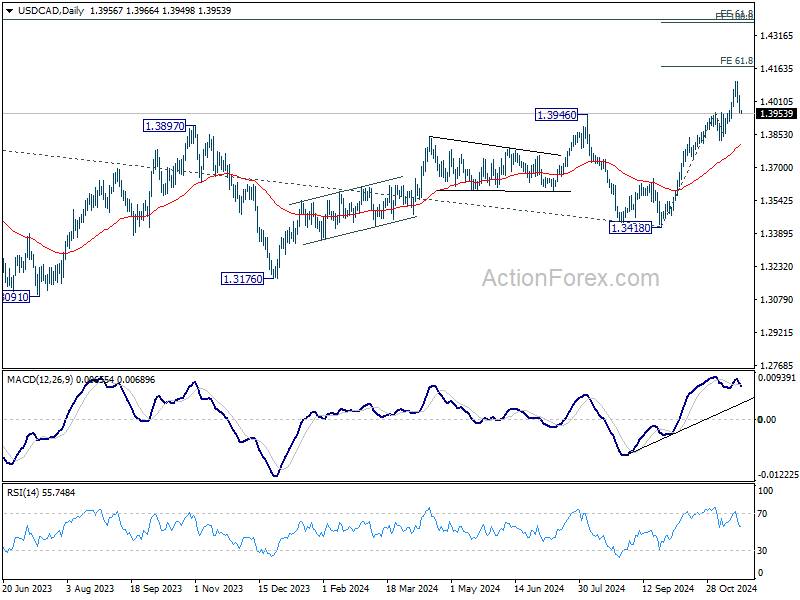

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3929; (P) 1.3983; (R1) 1.4010; More...

Intraday bias in USD/CAD remains neutral for the moment. Consolidations from 1.4104 should be brief as long as 1.3958 resistance turned support holds. Above 1.4104 will resume larger up trend to 61.8% projection of 1.3418 to 1.3958 from 1.3841 at 1.4175. Nevertheless, break of 1.3958 will bring lengthier consolidations, and risk deeper pull back to 1.3841 cluster support (38.2% retracement of 1.3418 to 1.4104 at 1.3842).

In the bigger picture, up trend from 1.2005 (2021) is resuming with break of 1.3976 key resistance (2022 high). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

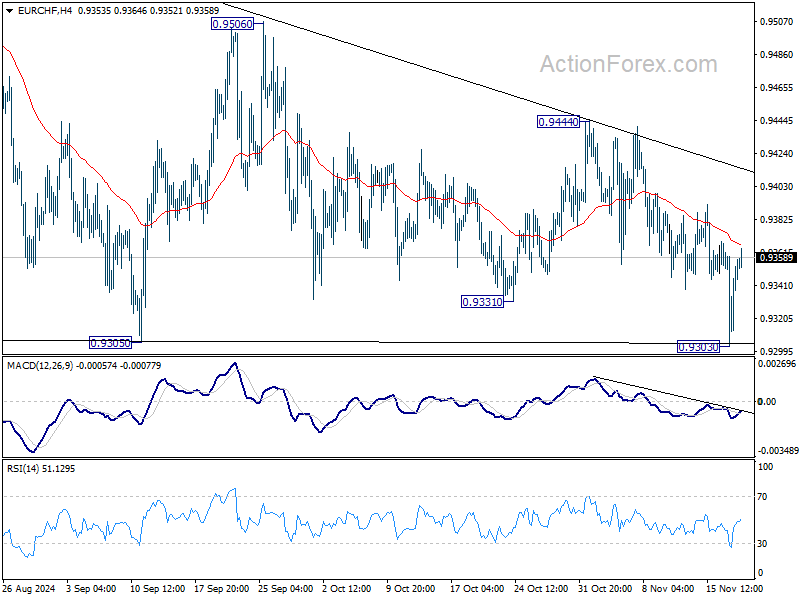

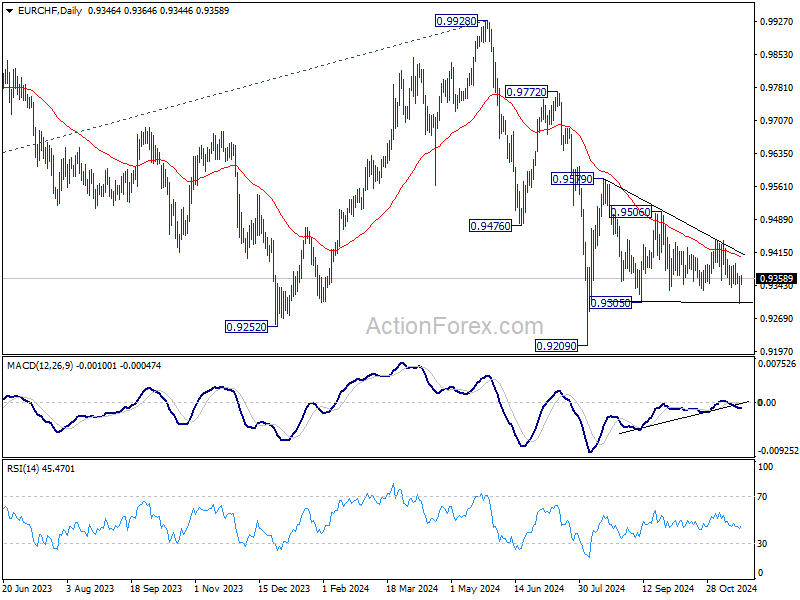

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9314; (P) 0.9341; (R1) 0.9376; More....

EUR/CHF rebounded after breaching 0.9305 support briefly and the development dampened the original bearish view. Intraday bias is turned neutral again. But still, risk will stay on the downside as long as 0.9444 resistance holds. Below 0.9303 will target a retest on 0.9209 low.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9408) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming at 0.9209 and bring stronger rebound back towards 0.9928 key resistance.

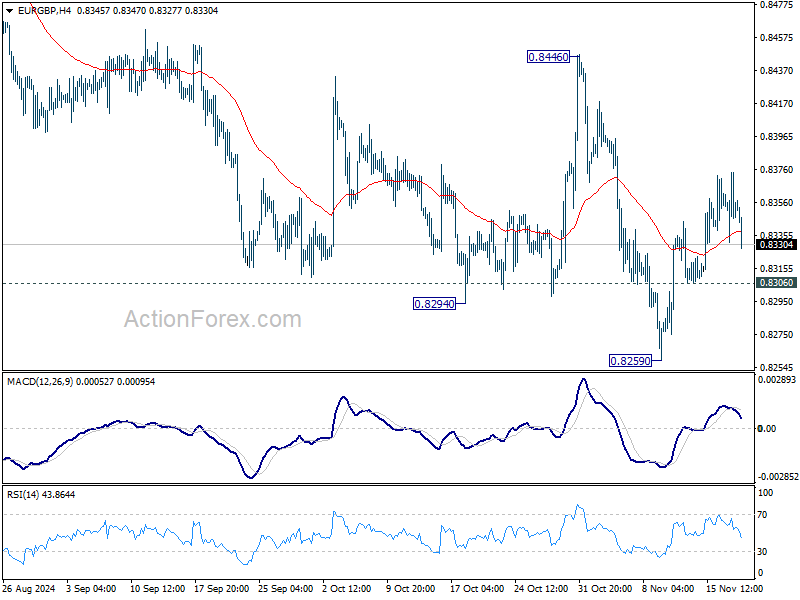

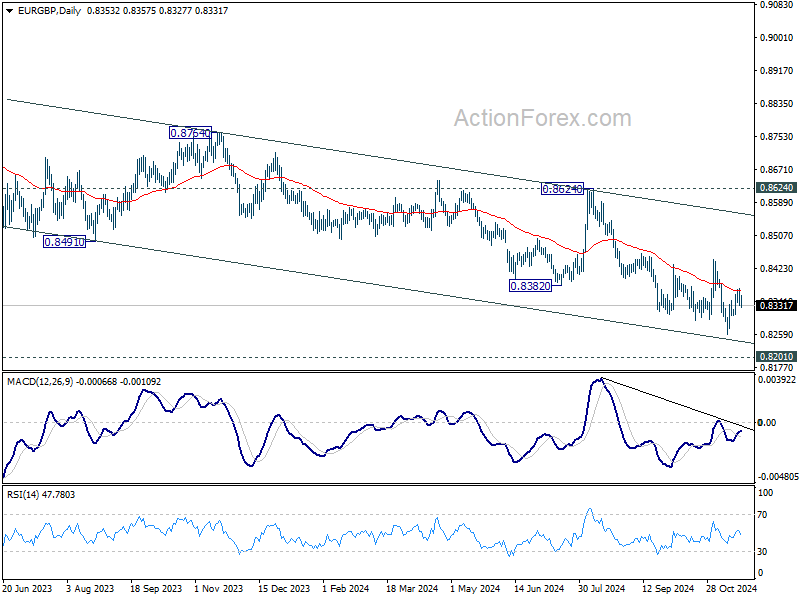

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8333; (P) 0.8354; (R1) 0.8377; More...

Intraday bias in EUR/GBP remains neutral and outlook stays bearish with 0.8446 resistance intact. On the downside, below 0.8306 minor support will turn bias back to the downside for 0.8259 first, and then 0.8201 key support. Nevertheless, firm break of 0.8446 will confirm short term bottoming.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

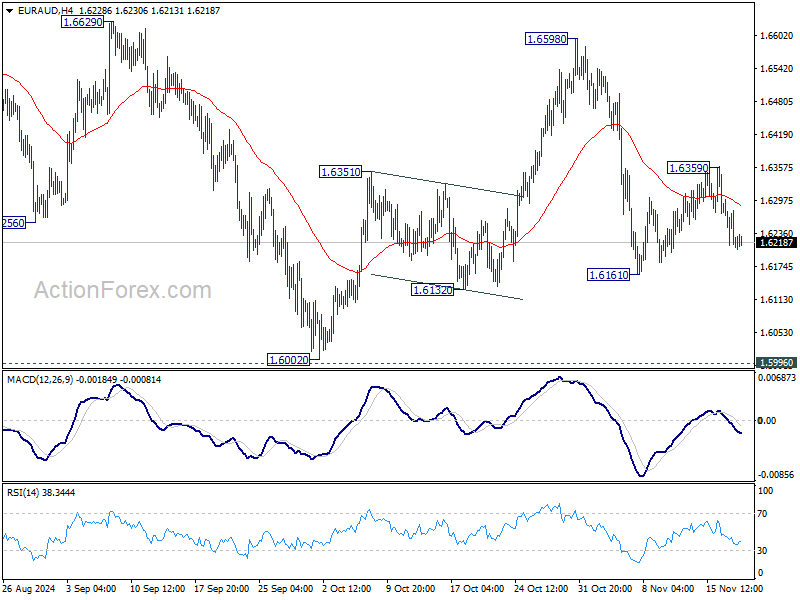

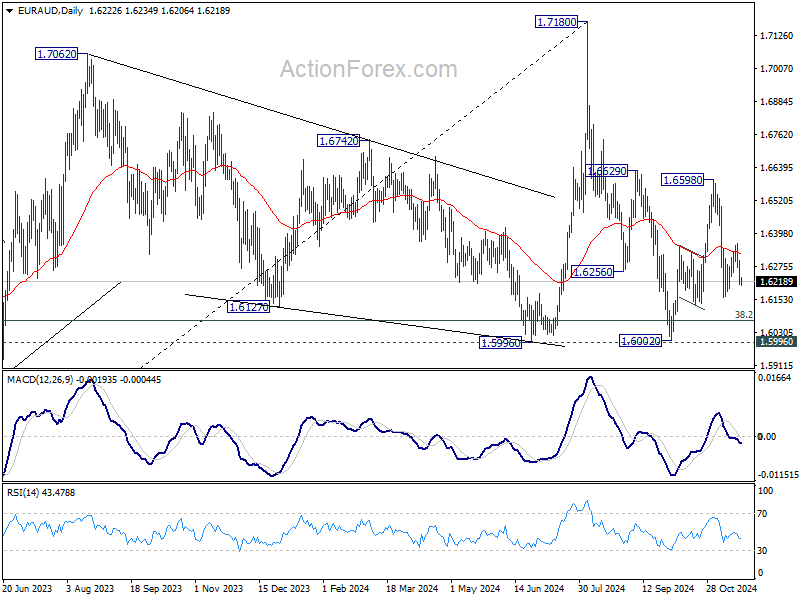

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6189; (P) 1.6245; (R1) 1.6278; More...

Intraday bias in EUR/AUD remains neutral and further decline is expected Break of 1.6161 will resume the fall from 1.6598 for retesting 1.5996/6002 key support zone. Nevertheless, break of 1.6359 will turn bias to the upside for stronger rebound towards 1.6598 resistance instead.

In the bigger picture, as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still expected to resume through 1.7180 at a later stage. However decisive break of 1.5996 will argue that the medium term trend might have reversed. Deeper fall would be seen to 61.8% retracement of 1.4281 (2022 low) to 1.7180 at 1.5388, even as a correction.

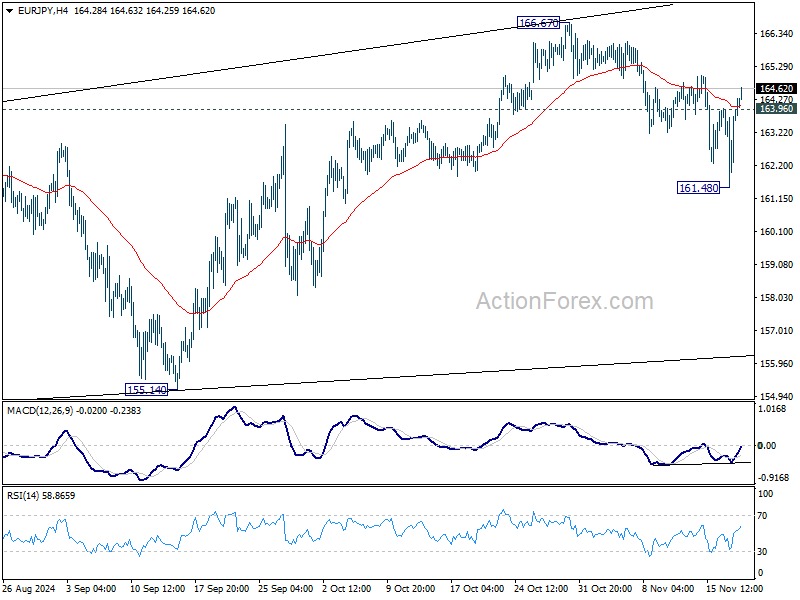

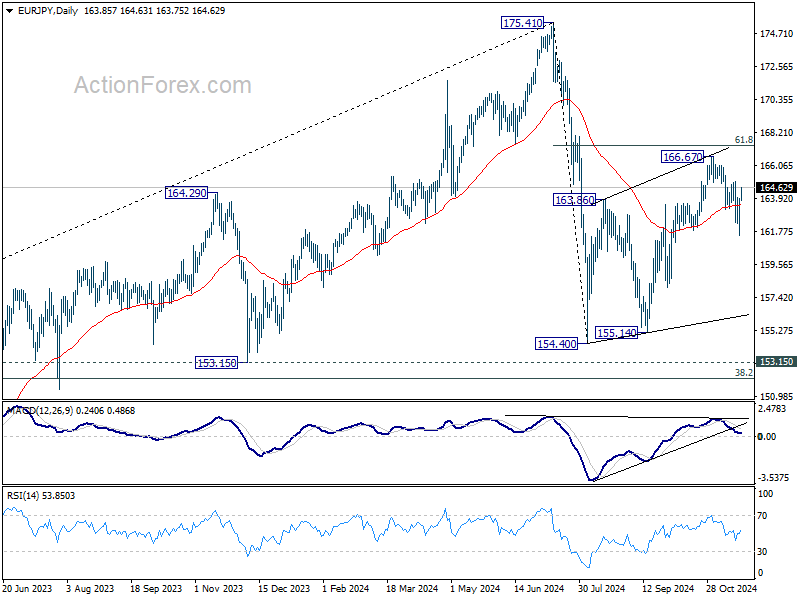

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.25; (P) 163.12; (R1) 164.75; More....

EUR/JPY's strong rebound from 161.48 and break of 163.96 minor resistance suggests that pullback from 166.67 has completed. The development also revives near term bullishness. Intraday bias is back on the upside for 166.67 resistance first. Firm break there will resume whole rebound from 154.40.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

UK CPI jumps to 2.3% in Oct, core CPI rises to 3.3%

UK CPI reaccelerated from 1.7% yoy to 2.3% yoy, above expectation of 2.2% yoy. Core CPI (excluding energy, food, alcohol and tobacco) rose by 3.3% yoy, ticked up from prior month's 3.2% yoy and above expectation of 3.1% yoy.

CPI goods annual rate rose from -1.4% yoy to -0.3% yoy, while the CPI services annual rate rose from 4.9% yoy to 5.0% yoy.

On a monthly basis, CPI rose by 0.6% mom, above expectation of 0.5% mom.

Geopolitical Tensions Spike amid Russia-Ukraine Escalation

In focus today

Today, in euro area we receive ECB's indicator of negotiated wage growth in the third quarter. The indicator declined significantly in Q2 to 3.5% y/y from 4.8% y/y, and we expect a rebound in Q3 as the decline in the second quarter was due seasonality of the payments especially in Germany. Hence, we do not put too much weight on the expected increase as most recent wage negotiations for the next year point to significantly lower wage growth going forward, which is the most important for the ECB.

We have several central bank speeches from both ECB and Federal Reserve during the day, where the market will look for clues on monetary policy.

There is significant focus on Nvidia as they are publishing earnings announcement today. A strong result is expected to support the equity markets.

Economic and market news

What happened over night

In China, Loan Prime Rates were as expected kept unchanged with 1Y 3.1% and 5Y at 3.6%. Part of the reason is the recent sharp depreciation pressure on the CNY which will likely keep PBOC sidelined for now on rates to not add to the downward pressure on the currency. Last week they again set the daily USD/CNY fixing stronger than the spot rate, indicating efforts to slow the depreciation.

What happened yesterday

In the euro area, October inflation was reported at 2.0% y/y (0.3% m/m). Core inflation was confirmed at 2.7% y/y despise service inflation being revised slightly up to 4.0% from 3.9%. The domestic inflation measure (LIMI) held steady at 4.2%, indicating persistent price pressure. However, the momentum declined again signalling a continued downward trend, which we expect will continue as wage growth declines. Overall, the downward trend in underlying inflationary pressures remains on track, which allows the ECB to continue lowering rates.

In Germany, negotiated wages surged significantly to 8.8% y/y in Q3 from 3.1% y/y in Q2. Even excluding special payments, wages rose 5.6%, indicating substantial increases. For the ECB, the most important is the wage growth outlook and as such the previous developments. The German Bundesbank anticipates future wage negotiations to moderate due to economic weakness and lower inflation. However, current high wage growth suggests that services inflation might remain sticky in the short term, influencing ECB's policy decisions amid uncertainties about the pace of wage growth slowdown.

In Russia-Ukraine, Ukraine hit a military target inside Russia using long-range US-made missiles, marking the first use since restrictions were lifted. As a response, Russia lowered threshold for a nuclear strike. The market reacted to the resurgence of geopolitical tensions, by a decline in European stocks and the euro as investors rushed to safe-haven assets such as government bonds and gold.

Equities: Global equities were higher yesterday, although this was not a day of uniform global performance. Europe, and particularly Eastern Europe, underperformed due to escalating geopolitical tensions and the Ukraine-Russia war. Examining the sector rotation reveals significant differences across the Atlantic; cyclicals underperformed in Europe while outperforming in the US. It is important to note that we did not receive any significant macroeconomic data yesterday. Thus, the explanation for market movements appears to lie in the weaponised escalation. In the US yesterday, the Dow closed down 0.3%, the S&P 500 was up 0.4%, the Nasdaq rose by 1.0%, and the Russell 2000 increased by 0.8%. Most markets in Asia are in the red this morning, while both European and US futures are trending higher.

FI: The rising tensions between Russia, Ukraine and NATO provided some tailwinds to the EGB market yesterday with the 10Y Bund yield declining almost 11p before noon. However, most of the move faded through the second half of the session as Russian foreign minister Lavrov tried to dampen fears of a nuclear escalation. The Bund ASW-spread rose by 4bp throughout the day - the largest 1D move since June - with the level now back in positive territory (1.7bp).

FX: It was a steady day for the global FX market yesterday with little big news to drive the market and mixed risk sentiment. G10 currencies posted small gains versus the USD with commodity currencies, NZD, AUD, CAD and NOK once again leading the way. EUR/USD traded in a tight range below 1.06, EUR/SEK around 11.60 and EUR/NOK dropped towards 11.60.

Happy Nvidia Earnings Day

Geopolitical tensions were on the headlines yesterday after Ukraine fired its first US missile to Russia after having received the green light from the White House following a two-year wait to do so. And Kremlin relaxed rules that would allow them to use nuclear weapons in case of an attack on its soil. Consequently, the session was marked by a swift flight to safety. Gold and treasuries gained, the Swiss franc tipped a toe below the 200-DMA, and crude oil was better bid. The barrel of US crude remained short of testing the $70pb offers however, as the geopolitical-led rally brought the top sellers back to the market. The fact that most Western economies have cut their exposure to Russian oil, and the weak demand outlook from China – which buys around half of the Russia oil today - keeps the bears in a dominant position below the $70pb level.

European indices fell and major US indices kicked off yesterday on a bad mood, but the geopolitical worries gradually left their place to optimism in the US after Walmart rallied to a fresh record on higher-than-expected sales and strong outlook for the holiday season, and on hope that Nvidia would do the same today, after bell.

Risk sentiment is improved today. US and European futures hint at a positive start and demand for safe haven assets has slowed.

Nvidia

One of the most highly anticipated days of the earnings season, if not the most, the Nvidia earnings day, is finally here. Nvidia is expected to have sold for $33bn of chips last quarter: it is 10% higher than the revenue the company announced last quarter, it is more than 80% of the amount they made during the same time last year and more than five times the amount they used to make before the AI craze began at the beginning of last year. The strong AI demand, particularly the insane demand for Nvidia’s next generation Blackwell chips - as says CEO Jensen Huang, and the robust results from TSM – that builds Nvidia’s chips – hint that the results will probably meet and hopefully beat these expectations. Nvidia closed yesterday’s trading session at $147 per share – a touch below its ATH level, and will either extend its rally to a fresh ATH, or decline on some profit taking. The implied volatility for Nvidia shares, based on at-the-money options pricing, stood at approximately 58% for a 30-day period as of November 18 hinting at a potential move of approximately 8-10% in the share price immediately after earnings. That implies a potential move around 1-2% in S&P500, to the upside or to the downside.

But it’s hard to say that good results will lead to a good market reaction. Last quarter, the blowout results and solid outlook weren’t necessarily enough to boost the share price after the earnings announcement. Over time, and at the current valuations, investors have become harder to satisfy and increasingly worried about what could go wrong.

Blackwell delays are the most obvious thing that could go wrong. But the company had successfully tamed worries regarding the Blackwell chips at last quarter’s results. And I believe, they will do the same this time around; they will probably play down the delays that could happen for this type of technology releases and focus on the insanity of the demand. If the company could convince investors that they are making progress to meet this insane demand, the reaction will likely be positive.

Other risks involve the rising competition and a slower future demand for AI from the Big Tech. The AI demand will not die out, even if it slows. Capital continues to flow into AI startups, especially in the US, many sectors, public or private, consider AI projects to improve their productivity levels. But demand outside the Big Tech will be more granular, and the new AI customers will certainly be looking for more affordable chips than Nvidia’s expensive, premium ones. That said, Nvidia has an important card to play now, and it’s called Balckwell. Some expect the company to ship up to 100’000 of these chips in the current quarter: that would be a $7mio addition to sales revenue...

Looking at political risks, the expectation that the new Trump administration could further revive the chip war with China is not a major worry anymore, because Nvidia has a significantly smaller exposure to China today than it did before. In 2021, the company made 25% of its revenue from China. Last quarter, the revenue from China was no more than 12%. But if tariffs go beyond China, it could be an issue for Nvidia that made almost two thirds of its revenue from abroad last quarter.