Sample Category Title

Natural Gas Prices Reach Yearly Highs

According to the XNG/USD chart, natural gas prices have risen by approximately 13% since early November and this week hit a new 2024 high.

Factors Driving Bullish Sentiment (as reported by Reuters):

→ A sharp increase in global gas prices.

→ Forecasts of colder weather and higher heating demand in the United States.

Will Natural Gas Prices Continue to Rise?

From a fundamental perspective, the Energy Information Administration (EIA) forecast on 13 November predicts natural gas prices could peak in January 2025.

From a technical analysis standpoint of the XNG/USD chart, the $3.200 level is a critical resistance, having previously triggered price reversals in October (B) and June (not shown on the chart). Price movements since early August have formed a trend channel (shown in blue).

Bullish Arguments:

→ The $2.7 level serves as support, aligned with Fibonacci retracement levels, as the B→C pullback is at 50% of the A→B rise.

→ The $2.93 level has flipped from resistance to support (indicated by arrows).

Bearish Arguments:

→ Prices reversed sharply downward earlier this week from the $3.200 level, showing seller activity.

→ Reports indicate utilities are injecting gas into storage at faster-than-expected rates, suggesting stockpiles could meet increased cold-weather demand.

Bulls may attempt to keep prices within the blue channel and make further attempts to breach the $3.200 level. However, XNG/USD signals show that bears are ready to push back.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

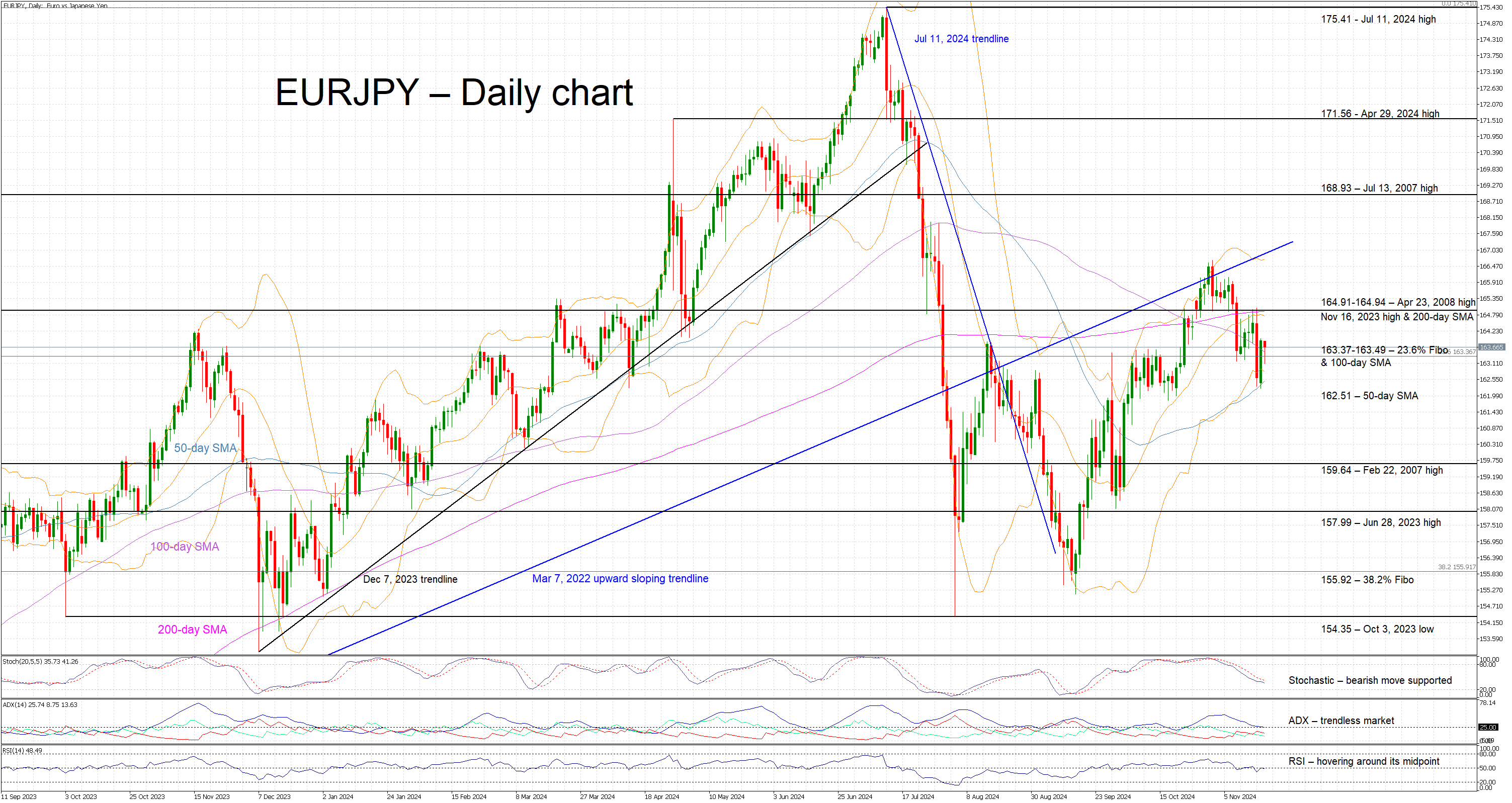

EURJPY Correction Halts at Key Support Area

- EURJPY is hovering around the 100-day SMA

- EURJPY bears have probably regained the upper hand

- Momentum indicators are mostly mixed at this stage

EURJPY is edging lower today, testing the support set by the 100-day simple moving average (SMA) and the 163.37-163.49 area. The rally from the mid-September low stopped at the March 7, 2022 upward trendline, with the 200-day SMA also proving strong resistance. A plethora of verbal interventions from Japanese government officials, which were triggered by the recent robust rally in EURJPY, and the strong details of the preliminary GDP report for the third quarter of 2024 have allowed EURJPY bears to reclaim the upper hand.

Meanwhile, momentum indicators are mostly directionless at this stage. Specifically, the RSI is hovering around its midpoint, without showing any appetite for a forceful move. Similarly, the Average Directional Movement Index (ADX) is trading lower, signaling the absence of a clear trend in EURJPY. On the flip side, the stochastic oscillator continues its downward trend, parallel to its moving average (MA), and thus revealing decent bearish pressure. A possible move above its MA could potentially signal the end of the current bearish move in EURJPY.

Should the bears remain confident, they would try to push EURJPY below the 163.37-163.49 area, which is populated by the 23.6% Fibonacci retracement level of March 7, 2022 – July 11, 2024 downtrend and 100-day SMA. The 50-day SMA is probably the last obstacle ahead of a more protracted selloff towards the February 22, 2007 high at 159.64.

On the other hand, the bulls could make another effort to retake the market reins and keep EURJPY above the 163.37-163.49 region. If successful, they could test the resistance set by the 164.91-164.94 area, which is defined by the April 23, 2008 and November 16, 2023 highs, and the 200-day SMA. Then, the March 7, 2022 trendline could be the most crucial test of the bulls' drive on their way higher.

To sum up, EURJPY bears have regained the upper hand, but they must overcome some key support levels in order to feel comfortably in control.

San Francisco Fed Economists Said US Labor Market Still Adding to Inflationary Pressures

Markets

US Treasuries followed last week’s recipe. Testing the recent low (area; depending on the maturity), but eventually rebounding higher. This time without strong trigger though like Thursday’s Powell speech or Friday’s retail sales. The move seemed more erratic in nature. Timing didn’t fit with the release of second-tier, but consensus-beating US figures. NY Fed services business activity rose from -2.2 to -0.5 in November, with details showing strength in business activity and employment. Both in the current and 6-month forward looking subindex. The NAHB housing index recorded a third consecutive increases to a 7-month high, from 43 to 46. The 6-monht sales outlook reached the highest level since April 2022 on hope on looser regulation and more construction during president Trump’s second tenure. Yesterday’s price action strengthens our short term consolidation call as dust settles over the US presidential elections, in absence of important eco data and with the Fed not in a hurry. Intraday changes on the US yield curve ranged between -0.7 bps and -3.3 bps with the belly of the curve outperforming the wings. German Bunds underperformed US Treasuries (GE 2y: +5.4 bps) in what could be the start of an opposite (to US Treasuries) consolidation phase. EUR/USD profited from relative yield dynamics with the pair being squeezed from 1.0531 to 1.0598. Dovish Greek ECB member Stournaras labelled a December 25 bps rate cut a done deal and added that it’s an optimal reduction. That way, he dented more aggressive market bets calling on a 50 bps move (25% probability). This week’s eco data have the potential to completely close the door obviously depending on their outcome. The ECB built her recent reaction function on what her president Lagarde calls “the three criteria”: the inflation outlook, the dynamics of underlying inflation and the strength of monetary transmission. Tomorrow, we receive important info on the second pillar via Q3 negotiated wage data. Annualized wage growth remained between 4.3% and 4.7% from Q1 2023 to Q1 2024. Last quarter’s decline to 3.5% was welcomed by the ECB in its inflation fight, but remains way above the central bank’s 2% inflation target. ECB Lagarde indicated that forward-looking wage trackers point to a an easing of pay growth in 2025 which she hopes to see reflected in tomorrow’s numbers. On Friday, EMU November PMI’s are expected to paint a similar, dire, picture as in October (50 for composite). Recall though that there was a serious discrepancy between weak Q3 soft data and hard data (+0.4 Q/Q EMU GDP growth).

News & Views

ECB chair Lagarde in yesterday’s “The economic and human challenges of a transforming era” speech again called for a(n effective) single market for both goods and capital in order to reverse progressively slowing productivity. “By acting as a union to raise our productivity growth, and by pooling our resources in areas where we have a tight convergence of priorities – like defense and the green transition – we can both deliver the outcomes we want and be efficient in our management of public spending.” Lagarde stressed the need for such changes given the two megatrends that are challenging the bloc’s economic model. The first is a new geopolitical landscape. An increasingly inward-looking global environment is a hazard to the open European economy. The second is Europe falling behind in emerging technologies, specializing mostly in technology developed the last century. Lagarde said the innovation and financing ecosystems are not suited to develop new advanced technologies, noting that about a third of EU savings sit in cash and bank deposits compared to around one-tenth in the US. She floated an amount of up to €8tn that could be redirected into long-term investments if EU households were given better opportunities to invest their savings. The still-existing trade barriers within the EU’s single market for goods and capital are estimated to represent a shortfall of around 10% of the EU’s economic potential.

San Francisco Fed economists in research published yesterday said that the US labor market is still adding to inflationary pressures, be it less than in 2022 and 2023. "Declines in excess demand pushed inflation down almost three-quarters of a percentage point over the past two years. However, elevated demand continued to contribute 0.3 to 0.4 percentage point to inflation as of September 2024." The findings offer some counterweight to Fed chair Powell’s observation back in the summer, when he said that the job market is no longer a source of significant inflationary pressures.

US Crude Rallies Continue to Face Stiff Resistance

The week kicked off on a bullish note, as the recovery in US treasuries, and the retreat in US yields help boost appetite in major US indices. The S&P500 rebounded 0.39%, while Nasdaq added 0.71%, supported by a more than 5.5% jump in Tesla shares on rumours that Trump administration wants to make a federal framework for fully self-driving vehicles one of the Department of Transport’s priorities. And remember, Elon Musk’s robotaxis is one of the company’s priorities for the future development and had helped – earlier this year – revive appetite for Tesla despite the slowing sales of EV sales. So yes, the news couldn’t come at a better time for Tesla. News were not as good on the Nvidia front though, as Nvidia’s Blackwell chips – you know the next generation chips that see an insane demand according to the CEO Jensen Huang – reportedly overheat, requiring redesign and delay for deliveries. Of course, you can argue that this type of adjustments are standard for such large-scale tech releases, and they should not have a material impact in the long run, but the delay in the short run mean that the big customers like Meta, Google and Microsoft won’t have their chips on time, the latter will extend the payoff period on their investments at a time investors can’t wait to see these investments bear fruit. Nvidia retreated 1.30% yesterday, as the news that the company is now working with Google to design its next generation quantum computing devices helped countering the negative vibes of the overheating Blackwell chips. The Blackwell news triggered a 3% rally in AMD that also sells high capacity chips for AI applications. ‘The MI325X is expected to begin production by late 2024, while the MI350 series aims for up to 35 times better inference performance compared to its predecessors and is set to launch in 2025’, according to ChatGPT. Any misstep from Nvidia could help AMD gain market share. For now, investors are focused on the next earnings report from Nvidia that will land on Wednesday, after the closing bell, and will hopefully put a number on how insane the demand for these Blackwell chips, whether they are overheating or not.

Beyond tech, the Dow Jones index was not cheery, yesterday, the index closed the session slightly lower, while small caps were slightly up on lower yields, but the direction of the yields are not encouraging the small cap investors given that these companies have smaller margin to deal with higher borrowing costs. As such, the buyers are seen more crowded in big caps, and even the most bearish of the bears on the Wall Street are busy lifting up their PT for the S&P500. The 6500 is increasingly pronounced for the S&P500, while gold is also among the top picks at Goldman Sachs, apparently, which sees the precious metal top the $3000 per ounce next year. In the short-run, the retreat in the US yields helped throw a floor under the gold’s retreat. We see a beautiful support forming near the minor 23.6% Fibonacci retracement and the 100-DMA – that’s around $2550 level.

In Europe, the Stoxx 600 index was flat, the Chinese stocks are lower as the Chinese authorities gather in Hong Kong to discuss the latest developments in China’s financial sector, while the Japanese Nikkei is under the pressure of a rebound in the Japanese yen against the US dollar, on the back of a broadly softer US dollar – a move that I believe is just a correction of the past few week’s rally on political developments and the hawkish shift in Federal Reserve (Fed) expectations.

The EURUSD tested the 1.06 psychological resistance yesterday, supported by the weak dollar and also the news that Greece will repay 5 billion euros of long-term debt before time. But outlook for the EURUSD remains negative on divergence between the European Central Bank (ECB) and the Fed, Hence, price rallies in the EURUSD will soon create interesting opportunities for the euro bears to come back in and give an other try to breaking the 1.05 offers’ back.

In energy, US crude posted a 3% rally yesterday, but the bulls could find the $70pb offers hard to clear, as the amply global supply / weak global demand outlook remains supportive of the bears. The short-end of the market shifted into contango, another signal that investors price in an oversupplied oil market, which could cap the upside potential of short-term price rallies. Solid resistance is seen between $70/72pb range. The key resistance to the actual negative trend – that has been building since summer – stands at the $72.85pb level – which is the major 38.2% Fibonacci retracement on summer decline.

Focus on Euro Area HICP Inflation

In focus today

Today, in euro area we receive final October HICP inflation data. This will show drivers of inflation and allow us to calculate the "LIMI" indicator of domestic inflation, which has received great attention from the ECB lately.

In Sweden, the day begins with a speech from Riksbank's Anna Breman at 8.15 CET, focusing on "Current monetary policy and the economic situation". This follows several notable events since the 6 November decision, such as US election, higher-than-expected inflation for October, and significantly higher electricity prices, presenting various discussion points. At 10.00 CET, the Swedish National Financial Management Authority will present new forecasts on the economy and public finances.

Today, we also have a few ECB speeches as well as some BoE speeches including BoE Governor Baily.

Economic and market news

What happened yesterday

In the euro area, ECBs Lagarde highlighted the critical need for Europe to reverse declining growth to sustain its welfare provisions, increase defence spending and address climate change. Lagarde emphasized the necessity for bold economic policies to generate the required wealth for these purposes. She also focused on the urgency of adapting to a changing geopolitical landscape and regaining competitiveness and innovation. Lagarde also pointed out Europe's vulnerability to trade wars due to its heavy reliance on trade, which makes up more than half of its economic output.

Equities: Global equities were higher yesterday, with European markets lagging behind the rest. We observed some elements of the Trump trade, though not nearly to the extent we witnessed in the immediate aftermath of the elections. Health care continued to underperform, while the materials sector experienced a slight recovery after several challenging weeks for the China-linked sector.

The VIX was marginally lower and appears to have stabilised around the 15 level, aligning with expectations given the current macroeconomic backdrop.

In the US yesterday, Dow -0.1%, S&P 500 +0.4%, Nasdaq +0.6%, and Russell 2000 +0.1%.

Asian markets were broadly higher, while South Korea underperformed for the second consecutive day. US and European futures are higher this morning.

FI: The EUR swap curve saw some bearish flattening through the Monday session, which was characterized by being very limited on market moving news. The 2Y tenor was up some 5bp throughout the session, while the 10Y point rose 3bp. The Bund ASW-spread at -2.5bp was roughly unchanged, similar to peripheral and EUR credit spreads.

FX: USD sold off against all currencies but the JPY to start the week. Commodity currencies, NOK, AUD and CAD gained the most on Monday. EUR/USD rose towards 1.06, EUR/SEK traded around 11.60 and EUR/NOK around 11.70.

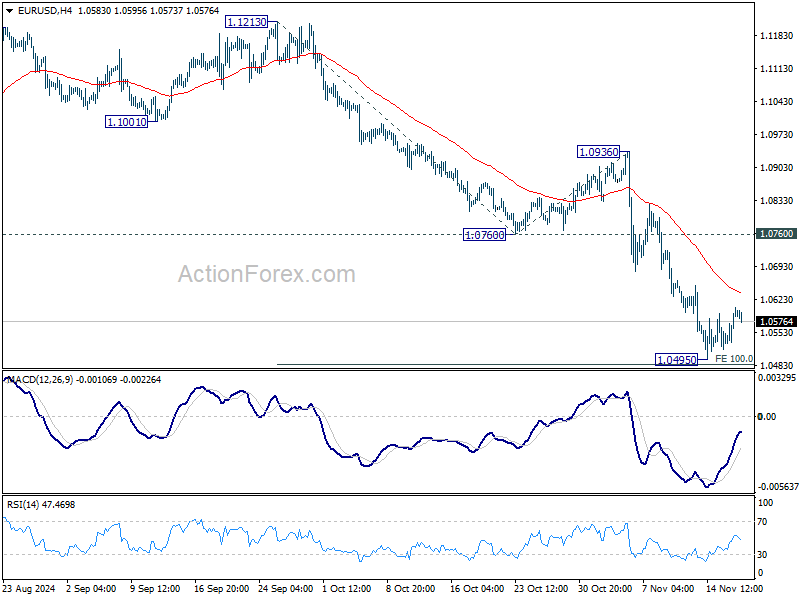

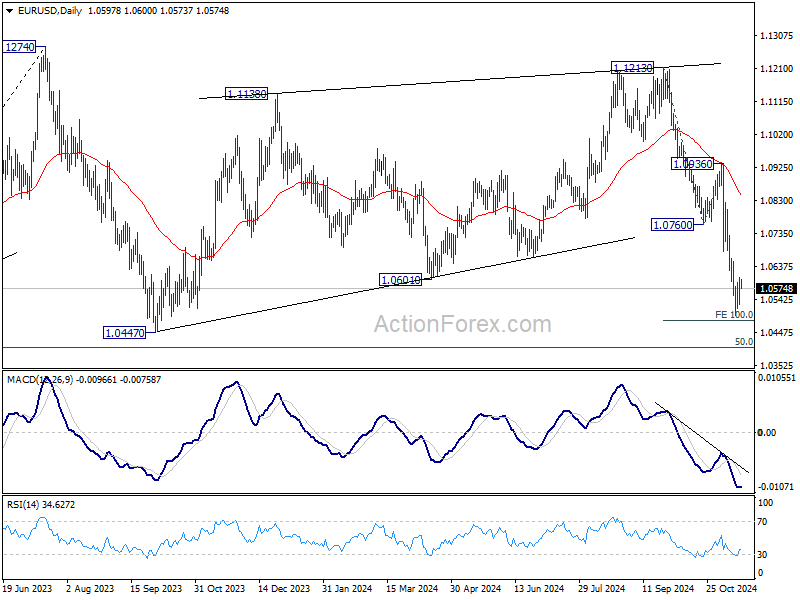

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0550; (P) 1.0578; (R1) 1.0627; More...

Intraday bias in EUR/USD remains neutral as consolidations continue above 1.0495 temporary low. Outlook will stay bearish as long as 1.0760 support turned resistance holds. On the downside, firm break of 1.0495 will resume the fall from 1.1213 to 1.0447 support and then 1.0404 key fibonacci level next.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage. However, firm break of 1.0404 will raise the chance of reversal and target 61.8% retracement at 1.0199.

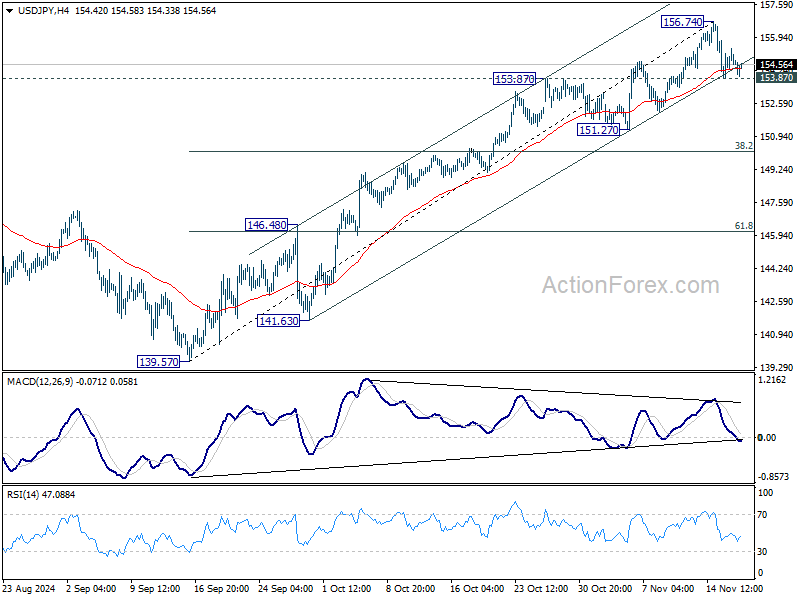

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.89; (P) 154.63; (R1) 155.41; More...

Intraday bias in USD/JPY stays neutral and further rally is in favor as long as 153.87 resistance turned support holds. Break of 156.74 will resume the rally from 139.57 towards 161.91 high. However, firm break of 153.87 and the near term rising channel would confirm short term topping. In this case, intraday bias will turn back to the downside for 151.27 support, or even further to 38.2% retracement of 139.57 to 156.74 at 150.18.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

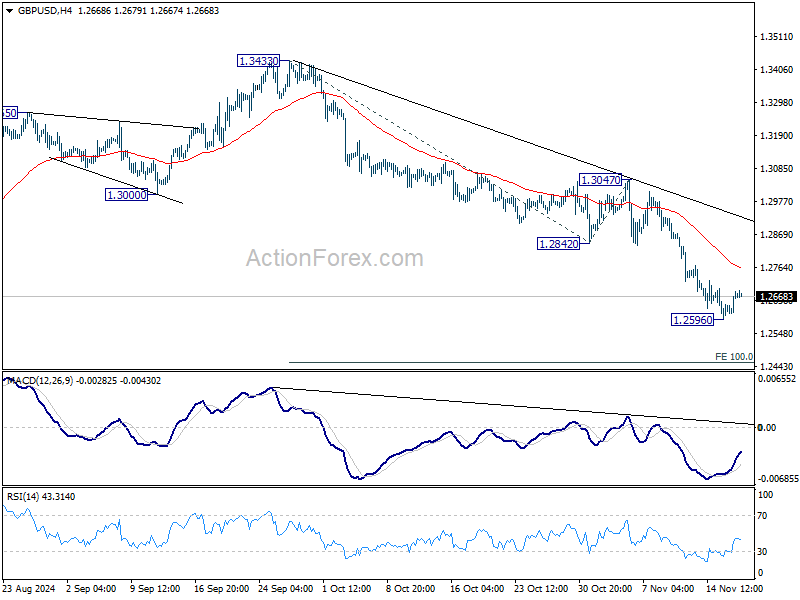

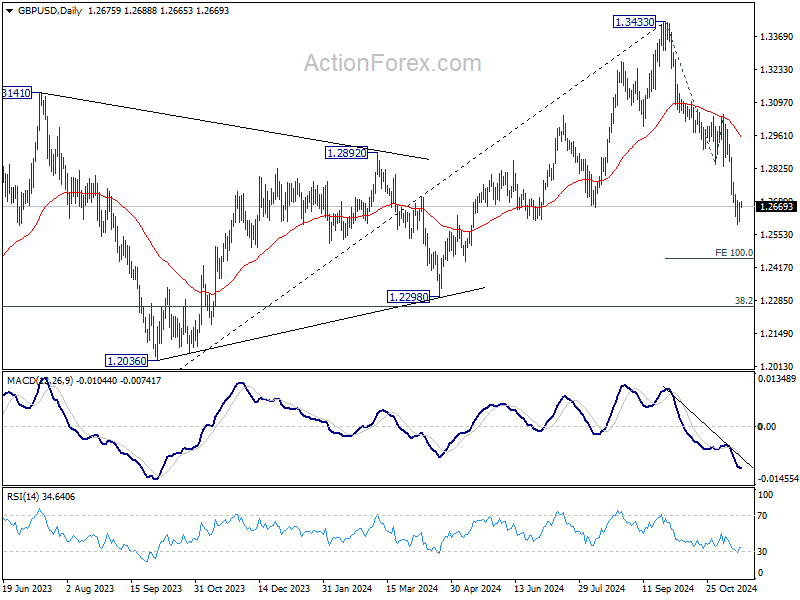

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2629; (P) 1.2658; (R1) 1.2707; More...

Intraday bias in GBP/USD is turned neutral as consolidation from 1.2596 extends. Outlook will stay bearish as long as 12.842 support turned resistance holds. Break of 1.2596 will resume the fall from 1.3433 to 100% projection of 1.3433 to 1.2842 to 1.3047 at 1.2456.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2977) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

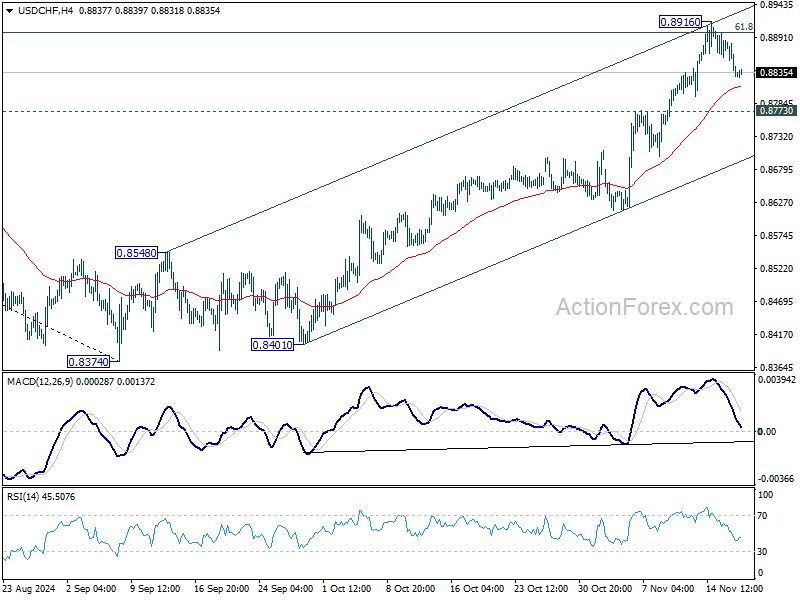

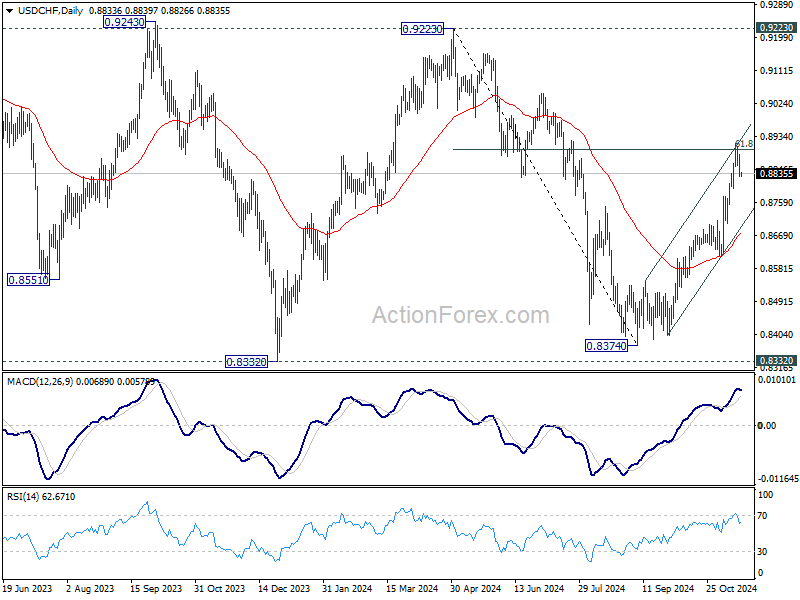

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8811; (P) 0.8850; (R1) 0.8871; More…

Intraday bias in USD/CHF remains neutral as consolidation from 0.8916 is still extending. Outlook remains bullish as long as 0.8773 resistance turned support holds. On the upside, break of 0.8916 and sustained trading above 61.8% retracement of 0.9223 to 0.8374 at 0.8899 will pave the way back to 0.9223 key resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

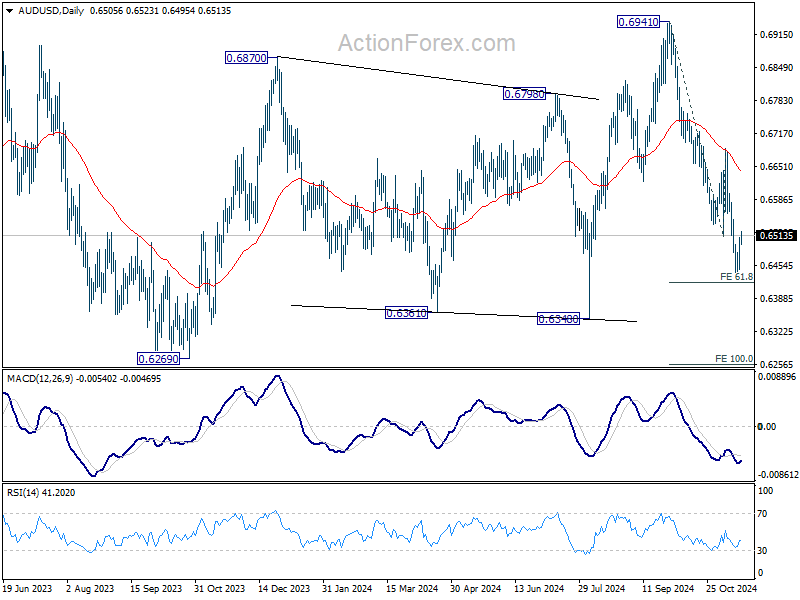

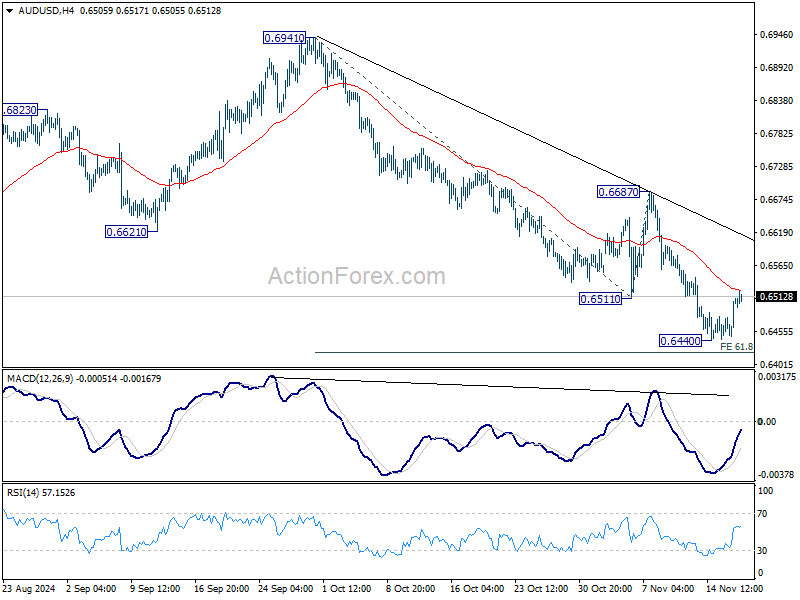

AUD/USD Daily Report

Daily Pivots: (S1) 0.6467; (P) 0.6489; (R1) 0.6530; More...

Intraday bias in AUD/USD stays neutral and some more consolidations would be seen above 0.6440 temporary low. But outlook will stay bearish as long as 0.6687 resistance holds. On the downside, decisive break of 61.8% projection of 0.6941 to 0.6511 from 0.6687 at 0.6421 will resume the fall from 0.6941 to 100% projection at 0.6257 next.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.