Sample Category Title

Higher Front-End US Yields Served Dollar Well Recently

Markets

Volatility remains high in the US Treasury market. We believed that Wednesday’s in-line with consensus CPI inflation report could be the start of a consolidation process on the sell-off which started mid-September. Fed Chair Powell’s comments on Thursday (“not in a hurry”) and retail sales on Friday twice ended the tentative correction higher before it even started. Headline retail sales were somewhat stronger than expected (+0.4% M/M) while slight disappointment in core gauges (+0.1% M/M) and for the retail control group (-0.1% M/M) were completely erased by a huge upward revision to already good September data (control group +1.2% M/M from +0.7% M/M). On both occasions, US Treasuries tested the sell-off lows but failed to break lower. Daily changes on the US yield curve ranged between -4.2 bps (2-yr) and +3.1 bps (30-yr). It strengthens our view that the time is there for some rebound action higher. Especially given deteriorating risk sentiment. Main US equity indices lost 0.7% (Dow) to 2.25% (Nasdaq) in what was the S&P’s worst week in more than two months. The vacuum on the US calendar comes in handy as well. Fed Powell’s comments minify the potential market impact of this week’s avalanche of Fed speakers. If any, they could even prompt a new increase of watered-down market bets on a December Fed rate cut (65%). From a data point of view, it will be a waiting game into Friday’s November PMI business surveys.

Higher front-end US yields served the dollar well recently. The same combo Powell-retail sales twice triggered a tentative move to reach for EUR/USD 1.05, but again without conviction. A correction in US Treasuries could in theory provide some breathing space in the pair, but the risk-off climate, rising gas prices (see below) and market conviction on a stimulative ECB monetary policy in 2025 to help the EMU economy all suggest that the rebound potential remains low. Just like in the US, we have a lot of ECB speeches this week. Apart from PMI’s, we also keep a close eye on Q3 wage data which are published on Wednesday.

Attention went to Japan this morning where Bank of Japan governor Ueda gave a final major speech ahead of the December 19 policy meeting. He kept close to recent comments, reiterating that “the actual timing of the adjustments (in the policy rate) will continue to depend on developments in economic activity and prices as well as financial conditions going forward”. That way he didn’t drop a hint that a next hike could be around a corner. There was some speculation that recent JPY weakness in combination with sticky inflation could trigger such frontrunning. JPY is a tad weaker this morning around USD/JPY 154.60.

News & Views

Dutch natural gas prices spiked to the highest in a year over the last couple of days. The surge towards €46/MWh and more are the result of supply concerns. Russia’s Gazprom warned Austria’s biggest oil and gas company that it would halt deliveries in response to the Austrian company seeking to reclaim hundreds of millions of euros over past contract violations by Gazprom. Russia made good on the threat over the weekend. With Ukraine’s transit deal with Moscow to supply Slovakia scheduled to run out at the end of this year, there could be an additional crunch in the midst of the heating season. The supply worries coincide with European countries dipping into their reserves earlier than usual amid chilly weather and slumping energy production from renewable sources.

UK’s Rightmove said that asking prices for British homes fell by 1.4% m/m in November to 1.2% y/y. The property portal noted it was an unusually big dip for the time of the year, which is typically something around 0.8%. The survey was squeezed in between the release of finance minister Reeves’ October 30 budget and the Bank of England policy meeting (Nov 7). When publishing new forecasts for 2025 it said that "The big picture of market activity remains positive when compared to the quieter market at this time last year. This sets us up for what we predict will be a stronger 2025 in both prices and number of homes sold." Rightmove expects house prices to rise by 4% new year, its highest prediction since 2021.

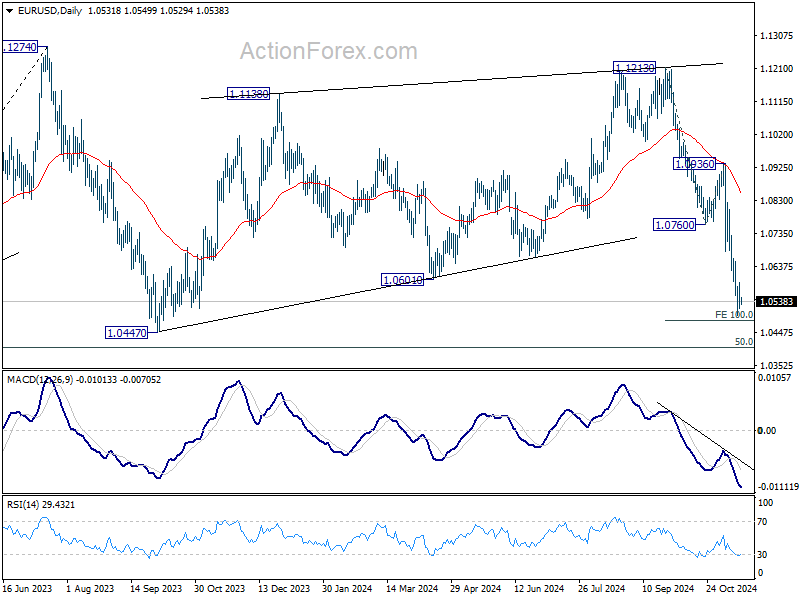

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0506; (P) 1.0549; (R1) 1.0583; More...

Intraday bias in EUR/USD remains neutral and more consolidations could be seen. But outlook will stay bearish as long as 1.0760 support turned resistance holds. On the downside, firm break of 1.0495 will resume the fall from 1.1213 to 1.0447 support and then 1.0404 key fibonacci level next.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage. However, firm break of 1.0404 will raise the chance of reversal and target 61.8% retracement at 1.0199.

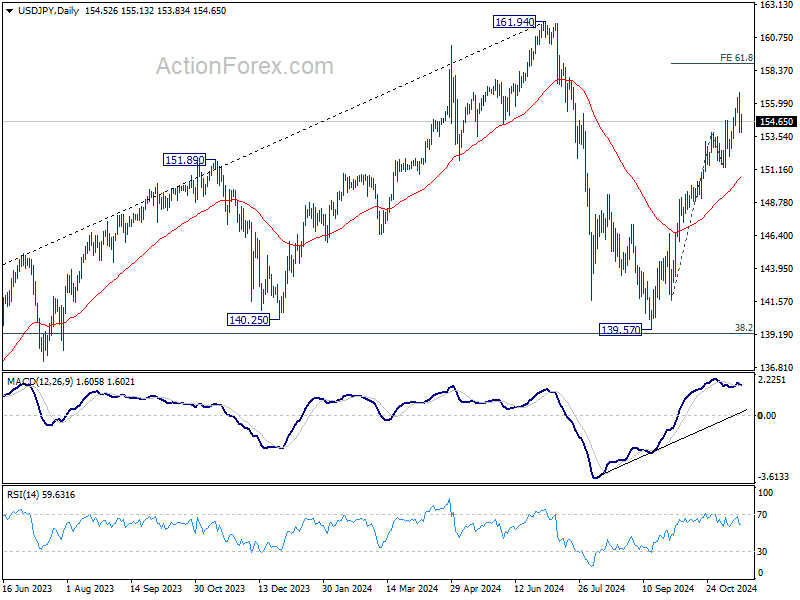

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.18; (P) 154.97; (R1) 156.07; More...

Intraday bias in USD/JPY remains neutral and more consolidations would be seen below 156.74. Further rally is expected as long as 151.27 support holds. Above 156.74 will target 61.8% projection of 141.63 to 153.87 from 151.27 at 158.83.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

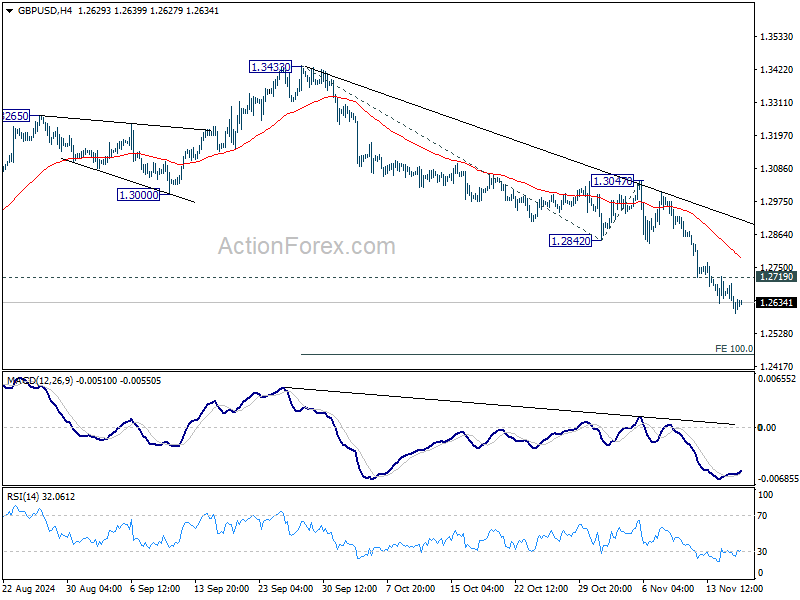

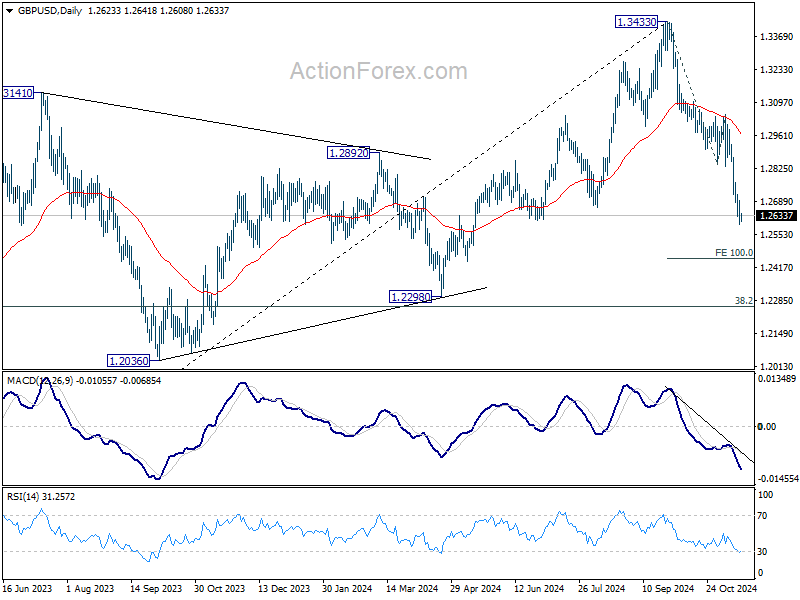

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2580; (P) 1.2638; (R1) 1.2680; More...

Intraday bias in GBP/USD remains on the downside for the moment. Fall from 1.3433 is in progress for 100% projection of 1.3433 to 1.2842 to 1.3047 at 1.2456. On the upside, above 1.2719 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 1.2842 support turned resistance holds, in case of recovery.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2977) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

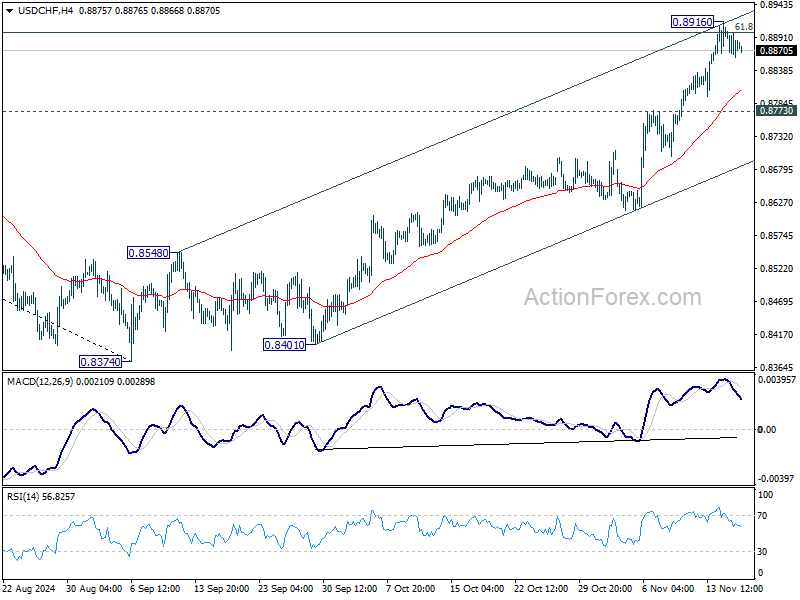

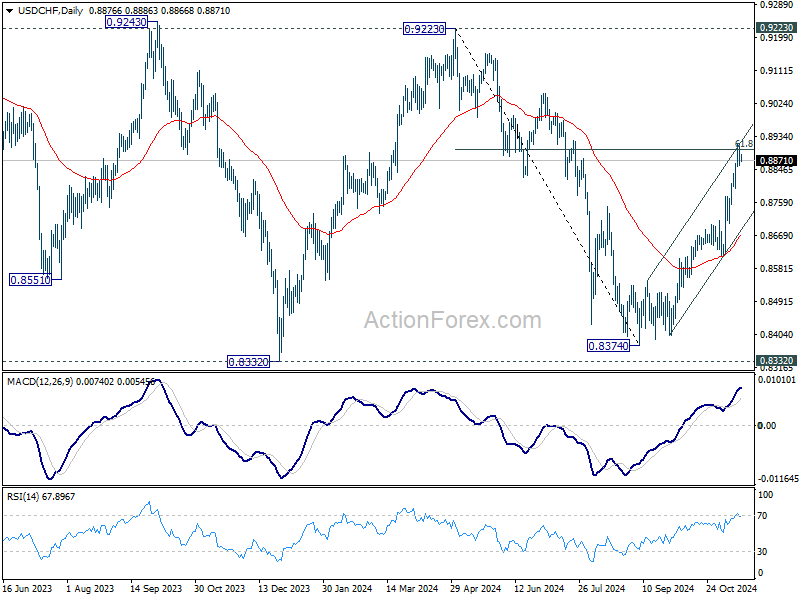

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8857; (P) 0.8883; (R1) 0.8906; More…

Intraday bias in USD/CHF remains neutral for consolidations below 0.8916. Outlook will stay bullish as long as 0.8773 resistance turned support holds. On the upside, break of 0.8916 and sustained trading above 61.8% retracement of 0.9223 to 0.8374 at 0.8899 will pave the way back to 0.9223 key resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

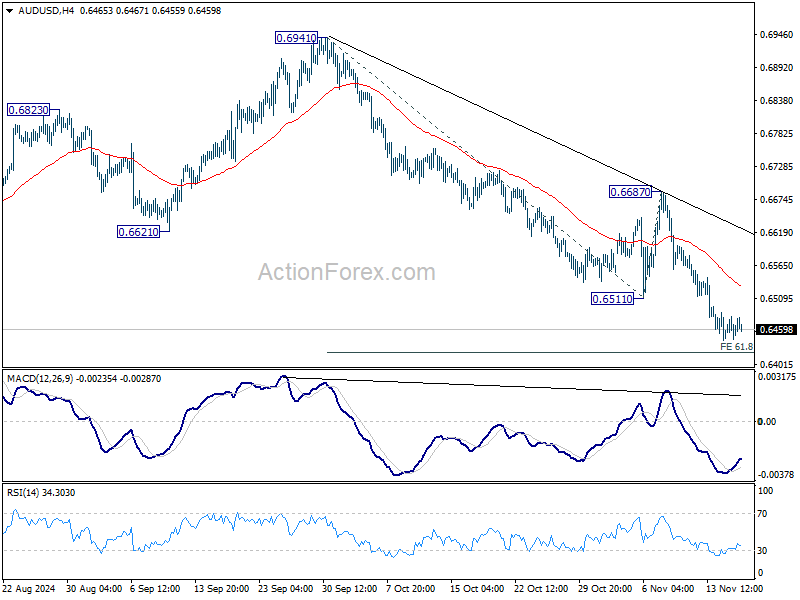

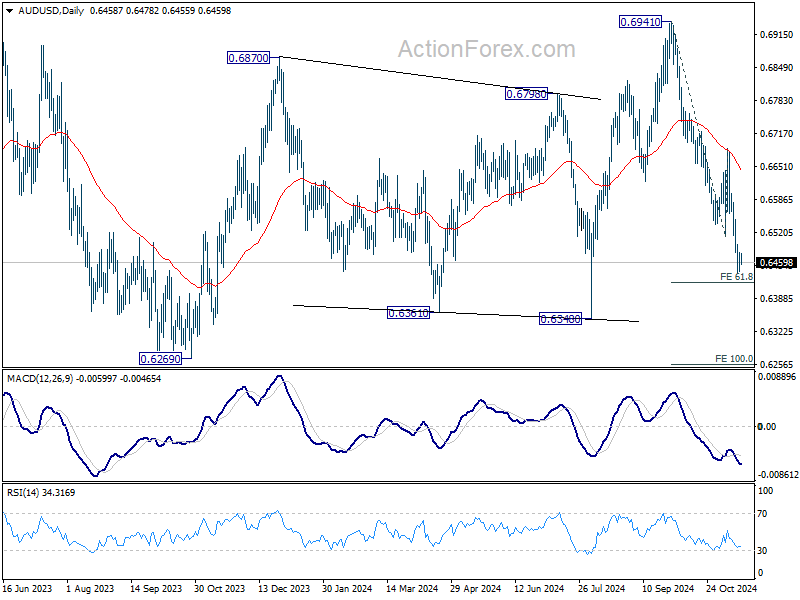

AUD/USD Daily Report

Daily Pivots: (S1) 0.6443; (P) 0.6463; (R1) 0.6482; More...

Intraday bias in AUD/USD is turned neutral first with 4H MACD crossed above signal line. Some consolidations would be seen but outlook will stay bearish as long as 0.6687 resistance holds. On the downside, decisive break of 61.8% projection of 0.6941 to 0.6511 from 0.6687 at 0.6421 will resume the fall from 0.6941 to 100% projection at 0.6257 next.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

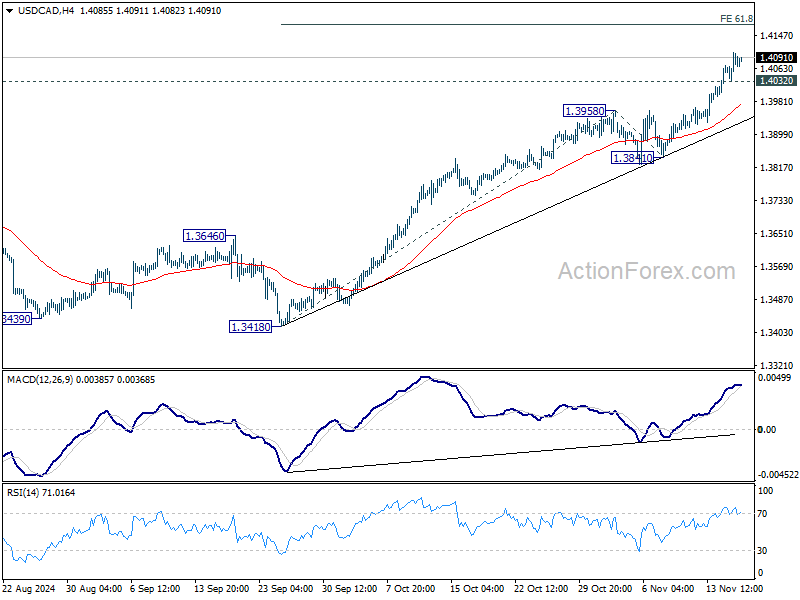

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4046; (P) 1.4075; (R1) 1.4118; More...

Intraday bias in USD/CAD remains on the upside at this point. Current rally should target 61.8% projection of 1.3418 to 1.3958 from 1.3841 at 1.4175. On the downside, below 1.4032 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 1.3841 support holds, in case of retreat.

In the bigger picture, up trend from 1.2005 (2021) is resuming with break of 1.3976 key resistance (2022 high). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

Heavy Euro Area Data Release This Week

In focus today

Today, in China, PBOC will set the Medium Lending Facility rates, but they are widely expected to keep rates unchanged due to the recent sharp depreciation on the CNY, aiming to avoid to further downward pressure on the currency.

Today, in the euro area, we have a string of ECB speeches including Lagarde, Lane and Nagel. The market will be looking for comments on monetary policy.

This week is heavy on euro area releases. On Tuesday, we receive the final euro area October HICP inflation. Wednesday, we receive the ECB's indicator of negotiated wage growth in Q3. Thursday, data on euro area consumer confidence for November is released. Finally on Friday the data highlight of the week is released in form of the November euro area PMIs and US PMIs.

Economic and market news

What happened overnight

Russia-Ukraine, the Biden administration has permitted Ukraine to deploy US-made weapons to strike deep into Russa, escalating tensions. This comes following an air strike by Russia on Sunday where the target was Ukraine's energy infrastructure, which damaged power systems further ahead of winter. Subsequently, oil prices increased due to heightened tensions between Russia and Ukraine over the weekend.

What happened over the weekend

In the US, October retail sales released on Friday initially seemed weak, with control group sales declining by 0.1% m/m SA (cons. +0.3%). However, in non-seasonally adjusted terms, annual growth rate picked up with growth to a solid 5.2% y/y. This might have contributed to the dip in EUR/USD following the data release. Despite fluctuations in monthly data, it looks like the US consumer overall remains on a solid footing. Friday, we also received industrial production, which followed consensus of -0.3% m/m (prior: -0.3% m/m).

In the euro area, the EU commission published their new economic projections for 2025 and 2026. The commission expects GDP growth at 1.3% y/y in 2025 (prior: 1.4%) and 1.6% in 2026. Inflation is expected to decline to average of 2.1% y/y in 2025 and 1.9% in 2026. The projections for 2025 have been revised slightly down due to increased downside risks, while inflation remains unchanged. The Commission anticipates that growth next year will stem from domestic demand, with net trade expected to be unchanged.

In Japan, Comments from BoJ's Ueda over the weekend send the JPY modestly weaker against the USD and EUR this morning, as he stated that the next move in Japanese policy rate was dependent on the economic data such as inflation and did not give a clear signal that BoJ would raise rates at the next BoJ meeting in December 18-19.

Equities: Global equities were lower on Friday and for the week overall. The US led the decline, which should be viewed in the context of its significant outperformance in the days following the US election results. Additionally, when examining both Friday and the past week, it is difficult to attribute the negative equity markets to macroeconomic data. We received robust data, with economic surprise indices reaching new highs after the summer's decline.

In the technology sector, there was a notable downturn on Friday and throughout the week, whereas financials, energy, and utilities sectors all registered gains last week. Health care also saw a sharp decline last week, leading to defensive stocks underperforming cyclicals.

Friday indicated a bit more uncertainty coming into the markets, with the VIX index ticking higher. In the US on Friday, the Dow closed down by 0.7%, the S&P 500 by 1.3%, the Nasdaq by 2.2%, and the Russell 2000 by 1.4%.

This morning in Asia, performance is mixed, with most indices lower, while South Korea is up almost 2%. European futures are marginally higher this morning, while US futures are mixed, with the technology-heavy indices outperforming.

FI: Friday's price action was without a clear catalyst resulting in the tight trading range through the day in the 10y point. The front end, ended marginally higher, thus leading to a bearish flattening of the curves. On Friday Ireland was placed on positive outlook by S&P bringing them closer to regaining AAA-status.

FX: JPY rallied on Friday followed by CHF and NOK, while GBP, CAD and SEK lost ground. The intraday move in EUR/USD was relatively large, but the pair remained below the 1.06 level. The rally in USD/JPY came to an end and the pair dropped to 154. EUR/SEK held steady just below the 11.60 level, while EUR/NOK dropped 11.70.

Let’s Take a Break from Politics

US Retail Sales and the inflation data came in higher than expected last week, and the Federal Reserve (Fed) Chair Jerome Powell said that the US economy is strong enough and that there is no urge for rushing to rate cuts. The US 2-year yield consolidated between the 4.30 and 4.40% level, the 10-year yield shortly spiked to 4.50% and the US dollar index traded at the highest levels in more than a year. The US yields and the dollar are softer this morning. Yet activity on Fed funds futures still gives around 65% chance for a 25bp cut in December, hinting that there is room for a further hawkish adjustment for December bets. Even if the next jobs data disappoints, rising US inflation expectations will likely tame the expectation of further rate cuts. This is especially true with Trump’s pro-growth policies and hefty tariffs threatening to give an additional boost to inflationary pressures.

The week’s economic data is light, investors will find a window to digest and breath after hectic weeks since the US election. We could see consolidation and correction in both US treasuries and the dollar. The EURUSD, which tested the 1.05 psychological support last week, could recover from the oversold territory, and the USDJPY could form resistance near the 155 level, but the rising risk for US inflation will remain the key market narrative and should limit the appreciation potential of major peers against the US dollar.

In energy, investors repeatedly knock crude oil back down each time it tries to recover. The barrel of US crude tumbled more than 2% on Friday and tipped a toe below the $67pb level. Higher global supply versus weak demand outlook keeps the bears in charge of the market. The price rallies serve to strengthen the bearish positions in expectation of a deeper selloff to $65pb. A solid support is seen for Brent crude approaching the $70pb level. Unless the macroeconomic narrative changes to stronger China, and lower oil output (in case the geopolitical tensions escalate), the bears will likely dominate the field.

In equities, last week ended on a sour note. The European equities were already bearing the brunt of US tariff threats and the Stoxx 600 remained downbeat despite the rising dovish expectations for the ECB. But the major US indices were also hit by a selloff last week on the back of a hawkish shift in Fed expectations. The Dow Jones retreated 1.24% last week, the S&P500 slipped more than 2%, Nasdaq 100 dropped around 3.40% while Russell 2000 lost 4%.

This week, attention shifts from politics and economic data to earnings. Big names like Walmart, Target and, yes, Nvidia will be reporting their Q3 earnings this week. The big retailers will shed light on the health of U.S. consumers, while Nvidia is expected to deliver a strong beat and an upbeat outlook, fueled by ‘insane demand’ for its Blackwell chips. That said, with such high expectations already baked into its stock, surprising Nvidia investors is becoming increasingly challenging with each passing quarter.

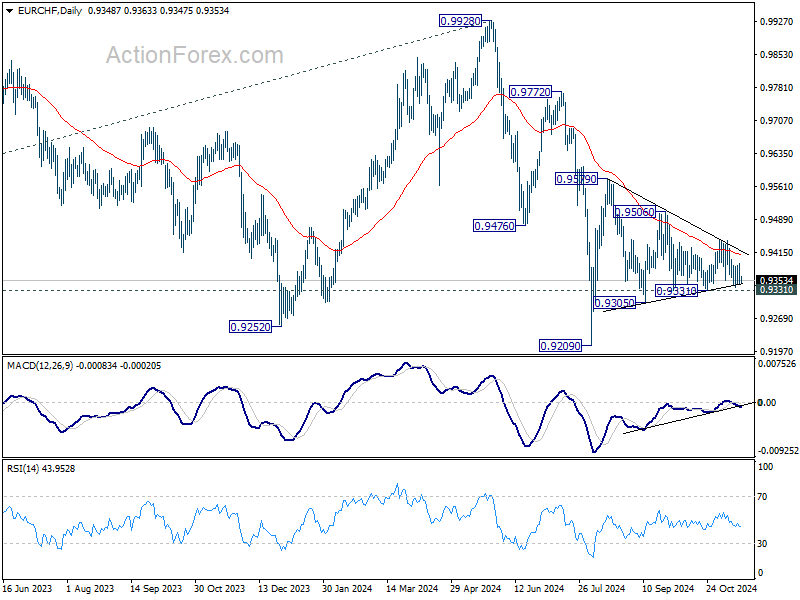

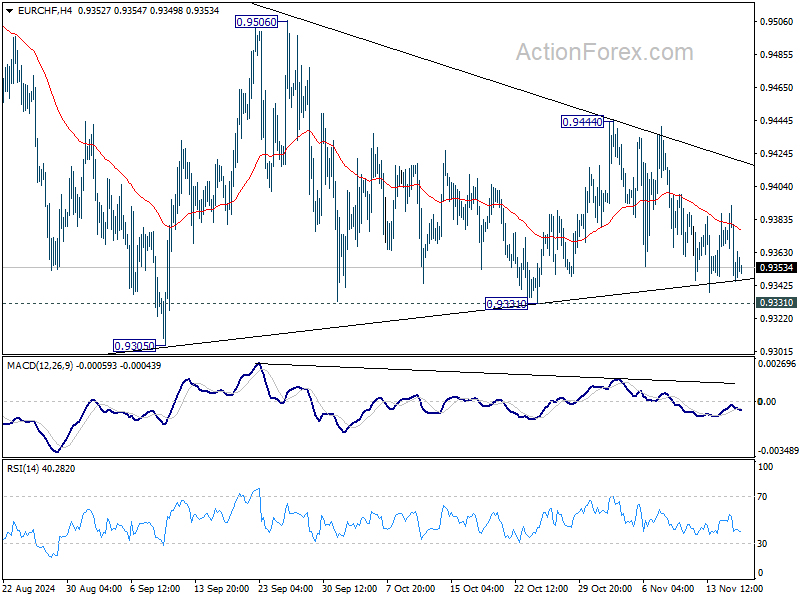

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9339; (P) 0.9367; (R1) 0.9388; More....

Intraday bias in EUR/CHF remains neutral as it's still bounded in converging triangle. On the downside, break of 0.9331 will target 0.9305 support first. Firm break there will bring retest of 0.9209 low. On the upside, break of 0.9444 will bring stronger rally to 0.9506 resistance next.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9410) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming at 0.9209 and bring stronger rebound back towards 0.9928 key resistance.