Sample Category Title

Hiring Demand to Weigh on Canadian Jobs Data, U.S. Fed to Cut Again

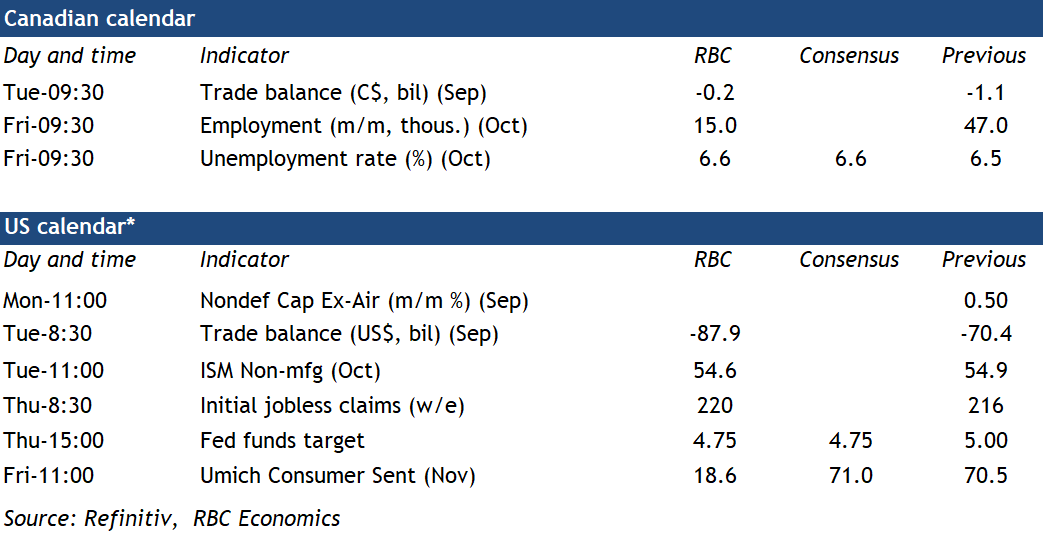

We think Friday’s Canadian employment report should tell a familiar story—that the labour market has continued to weaken in October amid slowing hiring demand. Employment is still expected to increase, but not by much. We expect 15,000 jobs were added, but that would again undershoot growth in the labour force and population, and push the unemployment rate back up to 6.6% after a tick lower to 6.5% in September.

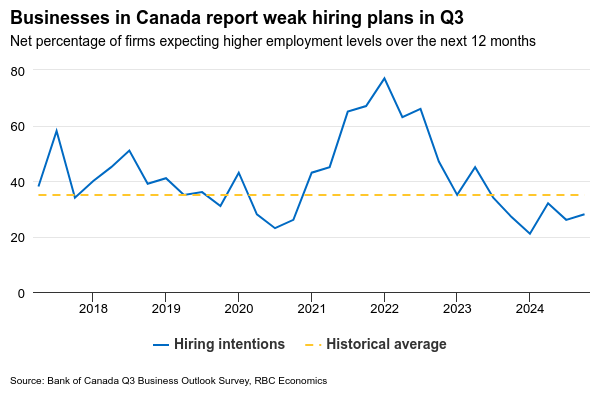

Leading indicators for employment conditions in Canada are still sending weak signals. Job openings have already dropped below pre-pandemic levels, and are still plunging. Business hiring intentions, according to the Bank of Canada’s latest Business Outlook Survey, have remained soft in Q3 driven by a subdued sales outlook over the next 12 months. Looking forward, we think unemployment will continue to rise in Canada to 7% by early 2025 before trending lower on a recovery in hiring demand.

The U.S. economic backdrop ahead of the Federal Reserve’s interest rate decision on Wednesday is very different, and much stronger.

Another solid increase in Q3 gross domestic product last Thursday extended a string of resilient U.S. economic data compared to other advanced economies. Still, labour markets have shown signs of cooling. The unemployment rate has inched higher, but very gradually, which is consistent with a normalization from overheated levels rather than faltering. An unusually large government budget deficit—which would likely increase under campaign pledges from both major presidential candidates in the week’s elections—will keep a floor under the economy and inflation in the year ahead.

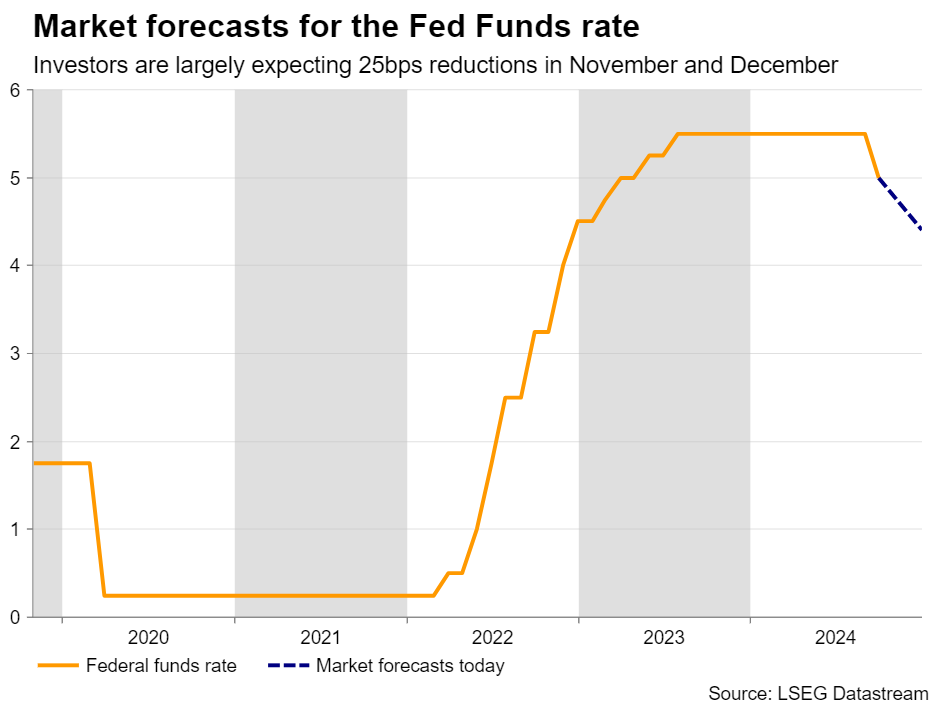

Interest rates are still likely higher than they need to be for inflation to return fully back to the Fed’s 2% inflation target. We expect the Fed to cut interest rates by another 25 basis points on Wednesday. Beyond that, we expect a 25-bps cut at each of the next two policy decisions in December and January before a pause. That leaves the Fed funds range at 4% to 4.25% for the rest of 2025.

Week ahead data watch

We look for Canadian trade deficit to narrow to $200 million in September, led by lower imports and higher exports. Oil prices were down significantly by 8.3% in September, lowering the energy trade balance. Rail activities were disrupted by the strike in August, but that decline should reverse in September, boosting exports.

The U.S. trade deficit likely widened to US$87.9 billion in September. According to the advance indicators, goods deficits were up US$14 billion from August, mainly due to falling exports (-2%), and higher imports (3.8%) during the month.

RBA in Wait-and-See Mode Despite Drop in Inflation

-

- RBA to stand pat at 4.35%

- Aussie may not be affected from this meeting

- Decision due on Tuesday at 3:30 GMT

RBA policy to remain unchanged

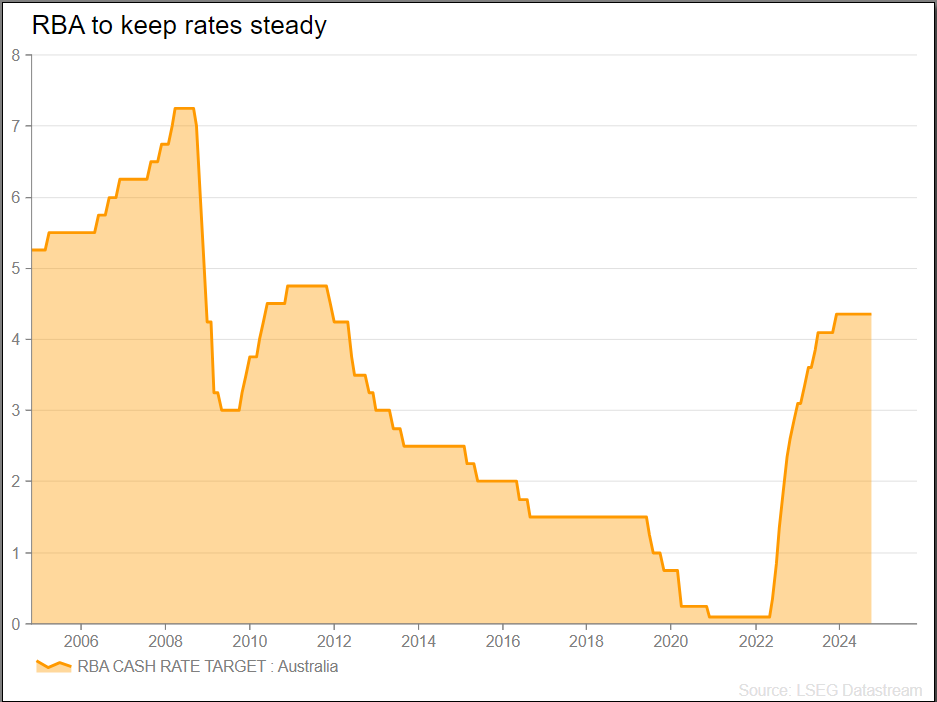

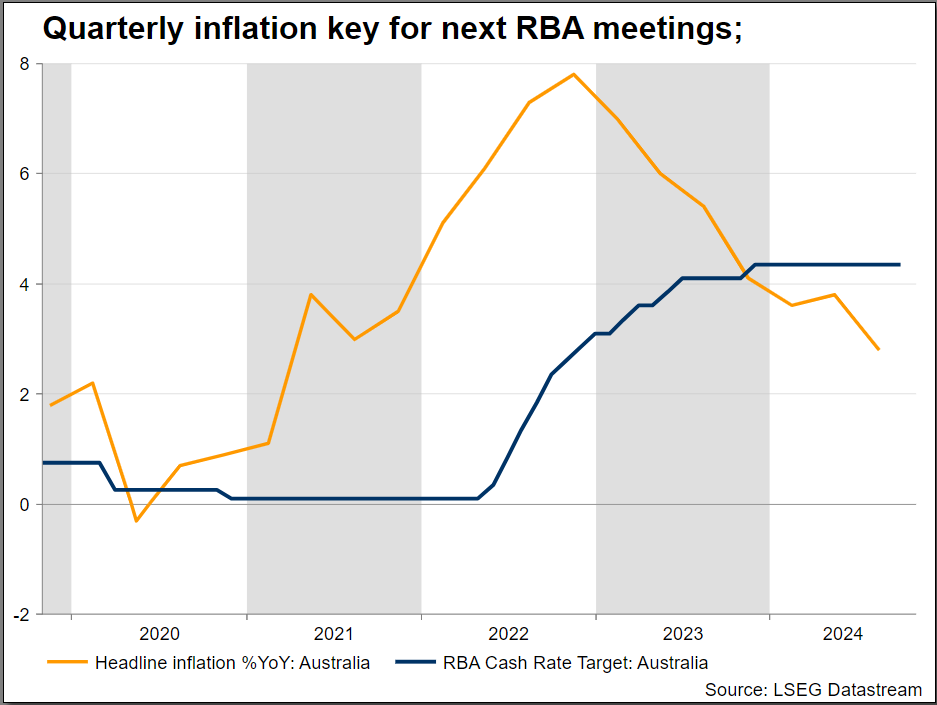

The upcoming Reserve Bank of Australia (RBA) policy meeting on November 5 is highly anticipated, with the bank adopting a wait-and-see approach and holding the cash rate steady while monitoring economic developments. The focus will be on ensuring that inflation continues to decline and that the economy remains on a stable growth path, with potential rate cuts anticipated in early 2025 if conditions improve.

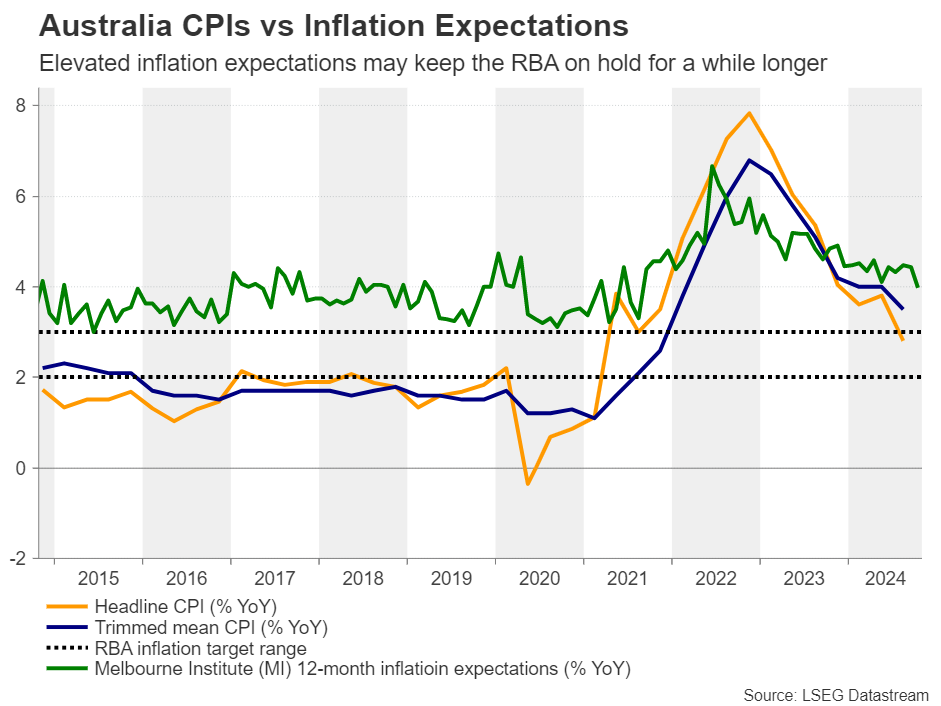

Inflation ticks down within target

Recent inflation figures show a mixed but overall encouraging pattern. In the September quarter, the headline inflation rate dropped to 2.8%, the lowest level in three and a half years. Significant drops in fuel and electricity prices, aided by government rebates, drove this decline. However, underlying inflation, measured by the trimmed mean, remains above the RBA’s target band at 3.5%. This persistent core inflation suggests that the RBA may need to maintain a cautious stance as service sector inflation, particularly in rents, insurance, and childcare, continues to exert upward pressure.

GDP and economic growth

The development of Australia's GDP has been modest. The June quarter of 2024 saw a 0.2% q/q increase in economic growth, which is consistent with the ongoing trend of gradual but consistent expansion. The weakest annual growth since the early 1990s, with the exception of the pandemic period, was 1.5% in the 2023–24 fiscal year. Although government expenditure has provided some support, this lethargic growth is a result of subdued household consumption and a decline in discretionary spending.

Various factors, including international economic conditions, domestic inflation patterns, and labor market robustness, will influence the RBA's decision. The recent decrease in headline inflation is promising; however, the RBA remains vigilant about the stickiness in underlying inflation and its possible effects on the economy. The GDP data underscore the necessity for ongoing support to foster economic growth and tackle the difficulties confronting households and companies.

Aussie stands near critical area

Investors will closely scrutinize the language and tone of the RBA's statement, even though the immediate decision to hold rates might not cause significant movement. Investors will look for clues about future monetary policy direction, which will influence the Aussie’s trajectory in the coming months.

Aussie/dollar rebounded off the 0.6535 support level, which overlaps with the medium-term uptrend line, with the next strong resistance coming from the 200-day simple moving average (SMA) near 0.6620. However, a tumble beneath the diagonal line could open the way for a test of the bearish spike of 0.6360, achieved on August 5.

Week Ahead – US Election Draws All Eyes, Fed, RBA and BoE Meet

- Traders lock gaze on Tuesday’s US election

- Trump and Harris battle neck and neck in final stretch

- Fed to decide whether to cut interest rates

- RBA and BoE decisions are also on next week’s agenda

The US dollar flexed its muscles lately on the back of upbeat data suggesting that there is no need for the Fed to deliver another bold 50bps rate cut at the remaining gatherings of the year, but also due to increasing market bets that Donald Trump will return to the White House.

It’s US election time!

The day when US citizens will decide whether this will be the case or not has come. While some Americans have already casted their vote, the official election day is on Tuesday, with candidates Donald Trump and Kamala Harris battling neck and neck for the Oval Office. Although Harris entered the race with a decent lead, the gap narrowed significantly over the past days, with the outcome hinging on battleground states.

Trump has pledged to cut taxes and impose import tariffs, especially on Chinese goods, policies that are seen as inflationary. Therefore, a Trump victory may raise speculation for even slower rate reductions by the Fed and thereby drive Treasury yields and the US dollar even higher.

The question is how the stock market will perform. Tax cuts and deregulation may be positive developments for Wall Street, but tariffs and slower rate cuts are not. Thus, even if stocks trade north just after a potential Trump win, a pullback may be on the cards in the not-too-distant future.

With the dollar and Wall Street gaining on increasing bets of a Trump win, a potential Harris victory may have the opposite market impact as her plans do not include massive tax cuts as Trump is promising. Having said that though, whether any policies will be implemented will depend on the composition of the Congress.

What will the Fed do after the election?

We may get a first idea on how the election outcome may affect the thinking within the Fed just two days later as on Thursday, the Committee announces its monetary policy decision. With the latest US data pointing to improvement and no need for a back-to-back bold rate cut, investors are now penciling in 25bps reductions at both this and the December gatherings.

That said, a 25bps reduction next week may not be a done deal as a hot NFP report later today and a Trump victory on Tuesday could convince more policymakers to agree with Atlanta Fed President Raphael Bostic who said a few weeks ago that he is totally comfortable with skipping a meeting. They could skip it next week or deliver the expected reduction in order not to catch investors off guard and hint at a December pause. After all, according to Fed funds futures, there is a 30% chance for a pause in December if a cut is delivered next week.

Taking into account the current market pricing, both cases argue for further gains in the US dollar. For the greenback to come under strong selling interest, Fed policymakers need to sound worrisome about the state of the US economy and signal that aggressive easing is needed for the months to come. Such a scenario seems unlikely though.

RBA and BoE also on next week’s agenda

The Fed gathering is not the only monetary policy decision on next week’s agenda. The ball will get rolling during the Asian session on Tuesday morning with the RBA, while on Thursday, ahead of the Fed, it will be the BoE’s turn to decide on interest rates.

RBA could remain on hold for a while longer

At their latest decision in September, RBA officials kept interest rates untouched, noting that underlying inflation remains too high and that their projections show that it will be some time before it is sustainably within the Bank’s target range. The Board noted that they will continue to rely on data and that they will do whatever is necessary to achieve price stability.

With the Melbourne Institute (MI) still suggesting that inflation will hover around 4.0% in 12 months, it is hard to envision an RBA policy strategy like other major central banks, which have already begun slashing rates. Indeed, market participants are pencilling only a 20% chance of a 25bps reduction by the end of the year, while such a move is fully priced in for May.

So, investors will dig into the statement to see whether they are correct in predicting that this Bank will remain on hold for a while longer. If their views are confirmed, the aussie may instantly gain some ground, but its latest downtrend against the almighty US dollar is unlikely to be reversed, at least not until investors get convinced that China will proceed with meaningful measures to shore up its economy.

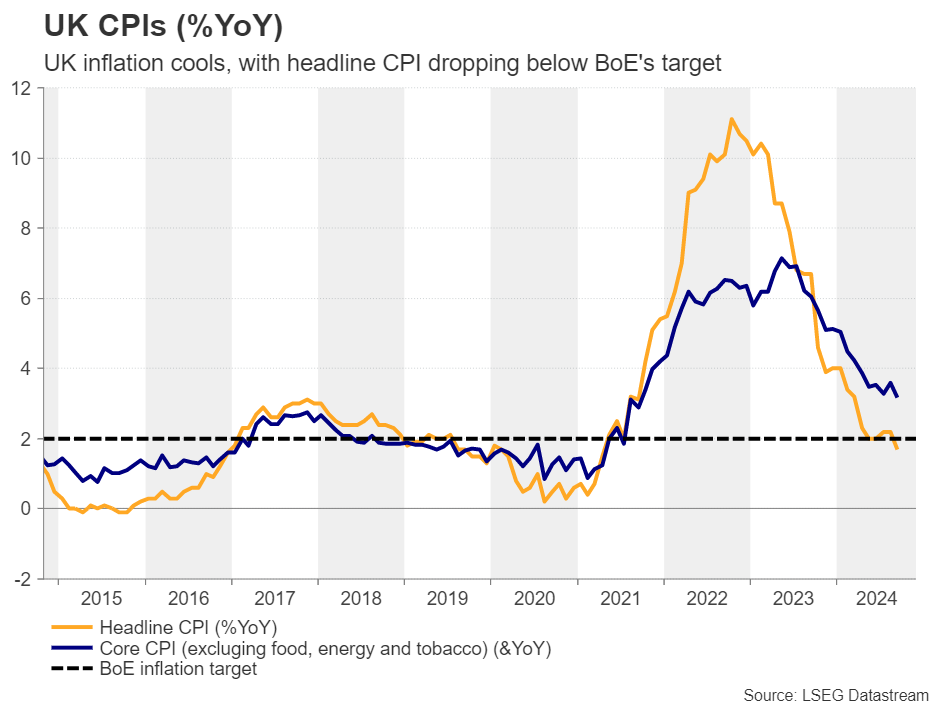

A BoE rate cut seems increasingly likely

Passing the ball to the BoE, at their September meeting, policymakers of this Bank decided to keep interest rates unchanged at 5.0%, noting that they will be careful about future rate cuts.

Nonetheless, a few weeks after the decision, BoE Governor Bailey said that they may need to be more active with rate cuts if the data continued to suggest progress in inflation, and indeed, the September numbers revealed that the headline CPI slipped to 1.7% y/y from 2.2%, while the core rate dropped to 3.2% y/y from 3.6%.

This prompted market participants to assign a strong 80% probability for a 25bps reduction at next week’s gathering, but the chances of this Bank following with another quarter-point reduction in December rest at around 30%.

Therefore, a rate cut on its own is unlikely to shake the pound much. The spotlight may fall on the voting and policymakers’ communication. If the votes reveal that the decision was a close call and the statement points again to no rush in further reductions, the pound could gain ground. The opposite may be true if it is agreed that more rate cuts are needed in the months to come.

New Zealand and Canadian jobs data

Elsewhere, the New Zealand and Canadian employment reports are due to be released on Tuesday and Friday respectively. The RBNZ is expected to proceed with a back-to-back 50bps reduction on November 27, with investors assigning a decent 15% chance for a bigger 75bps cut. The BoC also cut rates by 50bps last week, but it is now seen slowing back to quarter-point reductions, with a 35% chance pointing to another double cut.

Having that in mind, weak jobs data from these nations could convince more market participants to bet on the bolder action for each of those two central banks.

Fed Preview: Navigating Uncertain Waters

- We expect the Federal Reserve to cut rates by 25bp at the November meeting, which is nearly fully priced in by the markets at the time of writing.

- US October Jobs Report and Election Date pose significant risks to both sides of current rates outlook. We think the Fed is more likely to change its forward guidance than its rate decision next week in case of data / political surprises.

- Markets are pricing around 30% probability of a pause in December, but we still think 25bp cuts will continue in every meeting until June. More expansionary fiscal policy stance post-election could warrant an earlier end to the cutting cycle but is unlikely to affect rate decisions over the coming few months.

It is unlikely to be exaggeration to say that the six days in between publishing this report and the FOMC's rate decision come with historical levels of uncertainty. First, October Jobs Report will provide markets with the latest sense of resilience in US labour markets, and we look for a clear slowdown in nonfarm payrolls growth (+130k, Sep +254k). Any surprises should be interpreted with caution, though, given the long list of potential distortions related to weather, strikes and seasonality (read our preview from RtM USD - EUR/USD faces downside risk ahead of key events, 29 October).

But all eyes are naturally already on the US elections on 5 November. Donald Trump approaches the election as the slim favourite at least according to the prediction markets, but swing state polls remain extremely close. Pennsylvania and Wisconsin do not allow early counting of mail-in ballots which means they will likely be among the last states where results will be called. In 2020, Michigan was also called only around midnight European time between 6 and 7 November, and as Trump needs to win at least one of the three states, the results might only get confirmed within 24 hours of the rate decision.

In the past, the Fed has occasionally provided 'unofficial' guidance via select news outlets if data releases surprised sharply during the blackout. We think the bar for altering the outlook for the well telegraphed (and nearly fully priced in) 25bp move next week remains high due to the election. If the Jobs report (or change in expected fiscal policy stance) would warrant a shift in monetary policy, we expect the Fed to still move ahead with the 25bp cut and communicate any changes to the outlook in the form of more dovish/hawkish forward guidance during the meeting. The Fed will not publish new economic or rate forecasts so markets full focus will be on Powell on Thursday night.

At the time of writing, markets are pricing around 30% probability of the Fed pausing its easing cycle in December. If Republican sweep allows for more expansionary fiscal policies going forward, we would be inclined to call for a shorter easing cycle (e. g. removing cuts from the end of the forecast) but still call continuing cuts in the near-term. Rising odds of a Republican sweep have lifted the level of term premium priced into the USD curve, which together with stronger USD FX has contributed to a net tightening in financial conditions. Current level of policy rate remains well above FOMC's range of estimates for the neutral rate, and with inflation expectations broadly close to target, we do not see strong reasons for delaying the cuts for longer.

Weekly Focus – All Eyes on US Election and Central Banks

This week's data showed continued growth in the US and euro area in Q3, with the US GDP rising 2.8% q/q SAAR and euro area GDP increasing 0.4% q/q, surpassing expectations. Growth in the euro area was influenced by the Olympics in France and a revision of Germany's Q2 GDP. Without these factors, growth in these economies was flat, while Spain showed robust growth. In China, the October composite PMI rose to 50.8, signalling a recovery from the summer slump, driven by gains in both manufacturing and non-manufacturing sectors.

Tensions in the Middle East remain elevated after Israel retaliated against Iranian military sites following an attack on 1 October. However, the targeted response, which avoided energy infrastructure, was seen as less provocative, leading to a drop in oil prices. In Japan, the ruling coalition lost its Lower House majority, creating political uncertainty as it now requires support from other parties, which have criticized recent Bank of Japan (BoJ) rate hikes. Despite this, we expect the BoJ to continue rate hikes in December, as indicated at this week's meeting, even though rates were left unchanged. In the UK, the Labour government's first budget revealed a significant increase in borrowing over the next five years, pushing 10-year Gilt yields 20bp higher and reducing expectations for a back-to-back rate cut by Bank of England in December.

Euro area inflation increased to 2.0% y/y in October (cons: 1.9%, prior: 1.7%) driven by energy and food inflation, while core inflation was unchanged at 2.7%. Core inflation rose 0.20% m/m s.a. driven by still elevated service price increases of 0.30% m/m s.a. while goods prices remained unchanged at 0.0% m/m s.a. The October data thus showed that the very soft services inflation registered in September was a "blip" and inflation dynamics remain the same as we saw in the first months of Q3, namely with momentum in underlying inflation heading slowly in the right direction. Services inflation remains sticky on the back of elevated wage growth, which is supported by the strong labour market as also indicated by the unemployment rate, which dropped to an all-time low of 6.3% in September.

Next week, all eyes are on the US election. The first state results are expected a couple of hours past midnight on Wednesday European time, and by morning, around 70% of states had been called in the previous 2020-election. Donald Trump is the favourite to win the presidential election according to prediction markets, Republicans are expected to win majority in the Senate elections and House elections remain highly uncertain. The final swing state polls pointed towards a very close race for the White House and results from Pennsylvania, Michigan and Wisconsin, where results are likely to be known only late Wednesday, will likely play a key role in the outcome. We host two webinars on the morning Wednesday 6 November, which you can sign up for here and here.

On Thursday, focus turns to central banks as both Fed, BoE, Norges Bank, and the Riksbank have meetings. We expect both Fed and BoE to cut rates by 25bp in line with analyst consensus and market pricing. In both places, focus will be on forward-looking guidance especially in the UK after the recent jitters caused by the government's budget. For details, see Fed preview: Navigating uncertain waters, 1 November. On Friday, we should finally get the actual numbers on China's fiscal stimulus, which Reuters sources this week said could be 10 trillion yuan in extra debt the coming years.

US ISM manufacturing falls to 46.5, prices surge

US ISM Manufacturing PMI declined from 47.2 to 46.5 in October, falling short of the expected 47.6 and marking its lowest level since July 2023. This contraction is the index’s 23rd in the past 24 months.

Key components showed mixed results: new orders ticked up slightly from 46.1 to 47.1, but production dropped sharply from 49.8 to 46.2. Employment remained subdued, inching up only marginally from 43.9 to 44.4, while the prices index saw a notable increase from 48.3 to 54.8, suggesting upward cost pressures.

According to ISM, “demand remains subdued,” as firms remain hesitant to invest in capital and inventory, largely due to uncertainties surrounding Fed's monetary policy and concerns about inflation resurgence driven by fiscal policies from both major parties. October’s reading aligns with a modest 1.1% annualized growth in real GDP.

US: Payrolls Disappoint in October, But Unemployment Rate Holds Steady at 4.1%

Non-farm employment rose a meager 12k in October, well below the consensus forecast calling for a gain of 100k. Job gains over the two prior months were revised lower by 112k.

- The Bureau of Labor Statistics noted that Hurricane's Helene and Milton "likely" affected estimates in some industries, though did not provide any point estimates.

- Over the past three months, payroll gains averaged 104k, well below the 194k averaged over the prior twelve-month period.

Private payrolls were lower by 28k in October, with the largest declines seen in professional & business services (-47k) – all related to a pullback in temporary help (-48.5k) - and manufacturing (-46k), though this was largely due to the ongoing Boeing strike. Meanwhile, education & healthcare (+57k) and government (+40k) recorded solid gains last month. Job creation across most other industries was relatively flat.

In the household survey, a sharp decline in civilian employment (368k) largely offset a pullback in the labor force (-220k), keeping the unemployment rate steady at 4.1%. The labor force participation rate fell 0.1 percentage points to 62.6%.

Average hourly earnings (AHE) rose 0.4% month-on-month (m/m), a modest acceleration from September's downwardly revised reading of 0.3% m/m. On a twelve-month basis, AHE were up 4.0% (from 3.9% in September).

Key Implications

Between the ongoing Boeing strike and the devastating impacts of Hurricane's Helene and Milton, we knew this was going to be messy employment report. While the Bureau of Labor Statistics didn't provide any point estimates of hurricane impacts, they did note that the storms "likely" had some impact on last month's figures. Putting that aside, revisions to prior months were meaningfully lower, which on top of October's disappointing reading pulled the three-month moving average down to 104k, well below what's required to meet current growth in the labor force. However, given the various factors impacting last month's numbers, it's too early to draw any meaningful conclusions from today's report.

Other data out this week continued to point to a labor market that is decelerating but not necessarily deteriorating. Job openings continued to trend lower in September while hire and quit rates are now at or below pre-pandemic levels. This has helped to pressure compensation growth lower, with the Employment Cost Index slowing to 3.9% on a year-ago basis in the third quarter. Amid the ongoing pickup in productivity, this suggests the Fed's preferred wage metric is now growing at a pace broadly consistent with 2% inflation. This should give policymakers all the confidence they need to gradually reduce the policy rate by quarter-point increments at each of its upcoming meetings.

Dollar Falls on Weak NFP Job Growth, But Losses Remain Limited

Dollar saw broad-based weakness in early US session following a much weaker-than-expected non-farm payroll report. Headline job growth came in well below forecasts, though market reaction remains tempered, as the data is widely believed to be heavily skewed by recent hurricanes and strikes. With unemployment rate holding steady and wage growth surpassing expectations, the underlying labor market still appears resilient. While this report slightly adjusted market expectations, there remains a near 95% probability of a 25 bps rate cut by Fed next week.

In terms of weekly currency performance so far, Euro remains firmly in the lead. Yen has climbed to second place, benefiting from a post-NFP decline in US Treasury yields. Swiss franc ranks third, though its performance was dampened by weaker-than-expected inflation data, solidifying the chance of another SNB rate cut in December. Aussie remains at the bottom of the chart, followed closely by the Loonie. Sterling, despite a sharp drop on the UK budget news, managed to regain some ground and now ranks as the third weakest. Dollar and Kiwi are positioned mid-range.

In Europe, at the time of writing, FTSE is up 0.90%. DAX is up 0.65%. CAC is up 0.76%. UK 10-year yield is down -0.033 at 4.401. Germany 10-year yield is down -0.017 at 2.373. Earlier in Asia, Nikkei fell -2.63%. Hong Kong HSI rose 0.93%. China Shanghai SSE fell -0.24%. Singapore Strait Times fell -0.10%. Japan 10-year JGB yield rose 0.004 to 0.945.

US NFP grows only 12k in Oct, unemployment rate steady at 4.1%

US non-farm payroll employment grew only 12k in October, well below expectation of 106k. That compares to average monthly gain of 194k over the prior 12 months.

Nevertheless, unemployment rate was unchanged at 4.1%, matched expectations. number of unemployed people was little changed at 7.0m. Participation rate ticked down from 62.7% to 62.6%.

Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Annual growth of average hourly earnings ticked up from 3.9% yoy to 4.0% yoy.

UK PMI manufacturing finalized at 49.9, wait-and-see ahead of budget

UK’s PMI Manufacturing was finalized at 49.9 for October, down from September's 51.5, marking the first contraction since April.

Rob Dobson, Director at S&P Global Market Intelligence, noted that the sector has entered Q4 on an "uncertain footing," as businesses adopt a wait-and-see approach amid policy speculation leading up to the recent Budget. This cautious stance has weighed on investment and spending, with business optimism hovering just above September’s nine-month low.

However, there was positive news on inflation. Input costs dropped to a 10-month low, with inflation easing significantly—one of the largest declines in the survey’s 33-year history. Selling price inflation also moderated, giving BoE additional flexibility to support growth should demand weaken further.

Looking forward, Dobson noted that November’s PMI release will be closely watched for signs of how the Budget impacts business conditions and confidence level.

Swiss CPI down further to 0.6% yoy in Oct

Switzerland’s CPI decreased by -0.1% mom in October, missing expectations of flat growth. Core CPI, which excludes fresh and seasonal products, energy, and fuel, edged up by 0.1% mom. Prices for both domestic and imported products each declined by -0.1% month-over-month.

On an annual basis, headline CPI dropped to 0.6% yoy from 0.8% yoy, falling short of the anticipated 0.8% yoy increase. Core CPI similarly softened, slipping from 1.0% yoy to 0.8% yoy. Domestic product prices grew at a slower pace, declining from 2.0% yoy to 1.8% yoy, while imported product prices saw a deeper contraction, from -2.7% yoy to -3.1% yoy.

Japan's PMI manufacturing finalized at 49.2, weak domestic and global demand

Japan’s PMI Manufacturing was finalized at 49.2 in October, a decline from September's 49.7, signaling continued contraction in the sector.

Usamah Bhatti at S&P Global Market Intelligence noted that while output fell only slightly, it was at the sharpest rate since April, with new orders contracting at their fastest pace in three months. Companies cited “weakness in domestic and global demand” as weighing heavily on sales and output, particularly in the semiconductor and auto industries.

Bhatti added that “near-term outlook is clouded” as firms worked through backlogs, suggesting that incoming orders are insufficient to support ongoing production. Business confidence also remained subdued, hovering near a two-year low, with firms expressing concerns about the timeline for recovery from the current “economic malaise.”

China’s Caixin PMI manufacturing rises to 50.3, domestic demand recovery amid weak exports

China’s Caixin Manufacturing PMI improved to 50.3 in October, up from 49.3 and surpassing expectations of 49.5.

According to Wang Zhe, Senior Economist at Caixin Insight Group, October brought a mix of positive developments, including “growth in manufacturing supply and demand, increases in prices, proactive inventory replenishment by companies, and logistics delays.”

However, challenges persist as external demand remains soft; new export orders contracted for the third consecutive month. Wang added that declining employment levels and weak foreign demand continue to weigh on the sector.

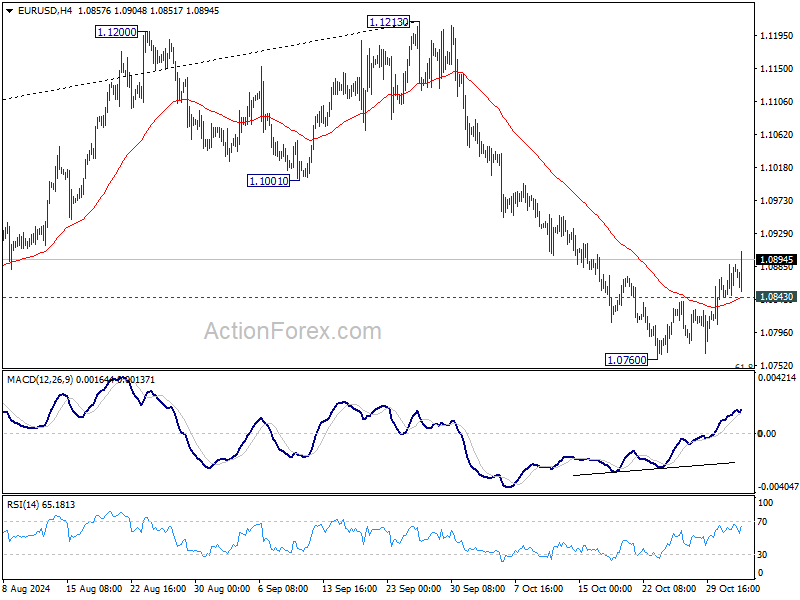

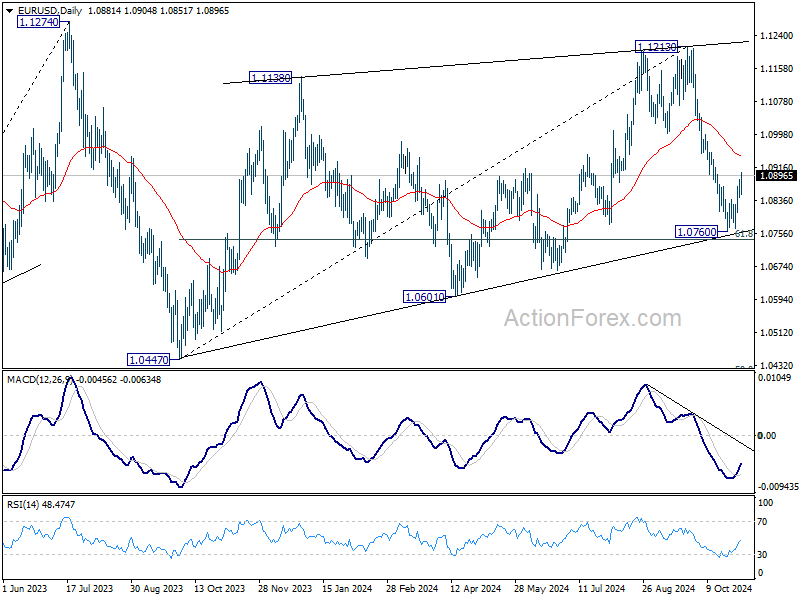

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0856; (P) 1.0872; (R1) 1.0900; More...

EUR/USD's rebound from 1.0760 short term bottom continues today and intraday bias stays on the upside for 55 D EMA (now at 1.0945). Strong resistance should be seen there to limit upside. On the downside, below 1.0843 minor support will turn intraday bias back to the downside. Sustained break of 61.8% retracement of 1.0447 to 1.1213 at 1.0740 will extend the fall from 1.1213 to 1.0601 support next.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

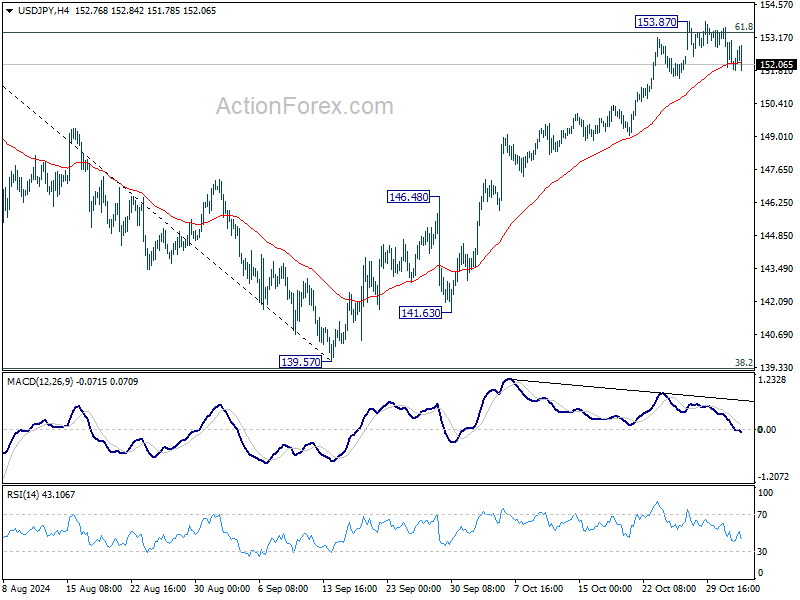

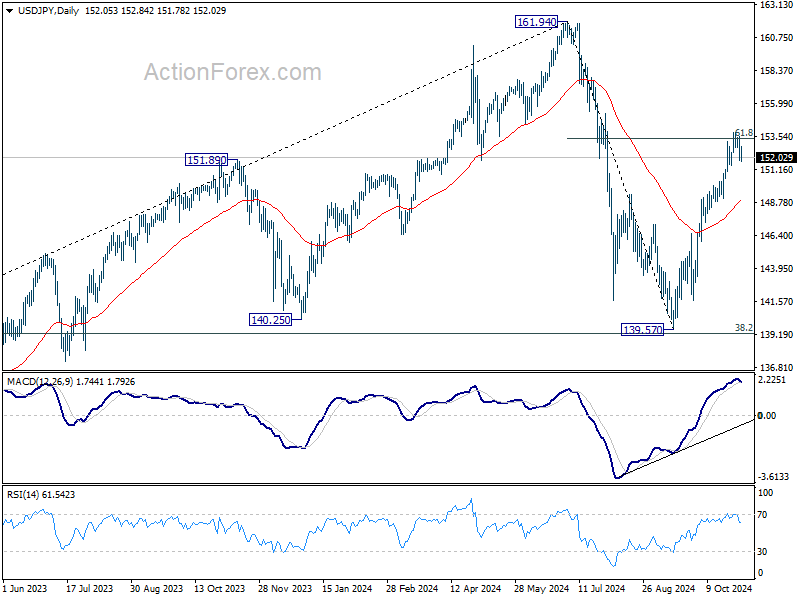

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.39; (P) 152.49; (R1) 153.14; More...

USD/JPY is still extending the consolidation pattern from 153.87 and intraday bias remains neutral. Deeper retreat cannot be ruled out but further rally is expected as long as 55 D EMA (now at 148.95) holds. Sustained trading above 61.8% retracement of 161.94 to 139.57 at 153.39 will pave the way to retest 161.94 high.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

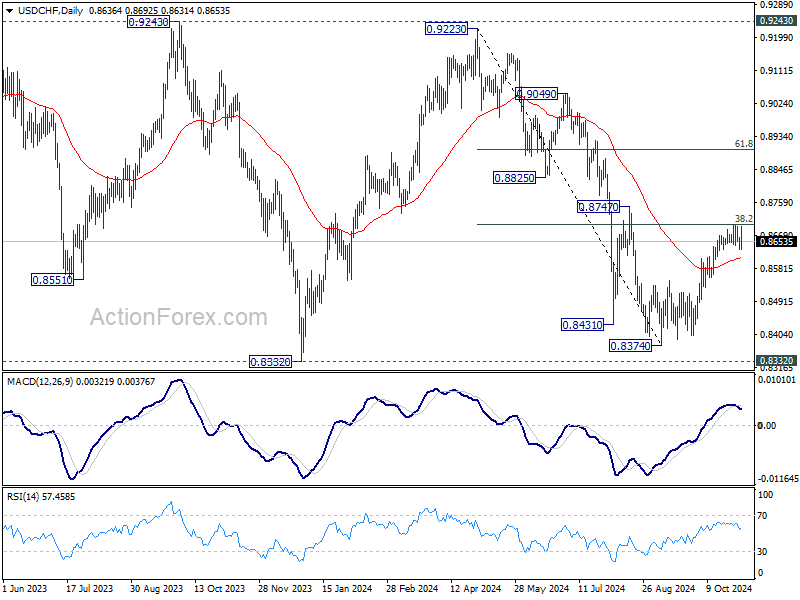

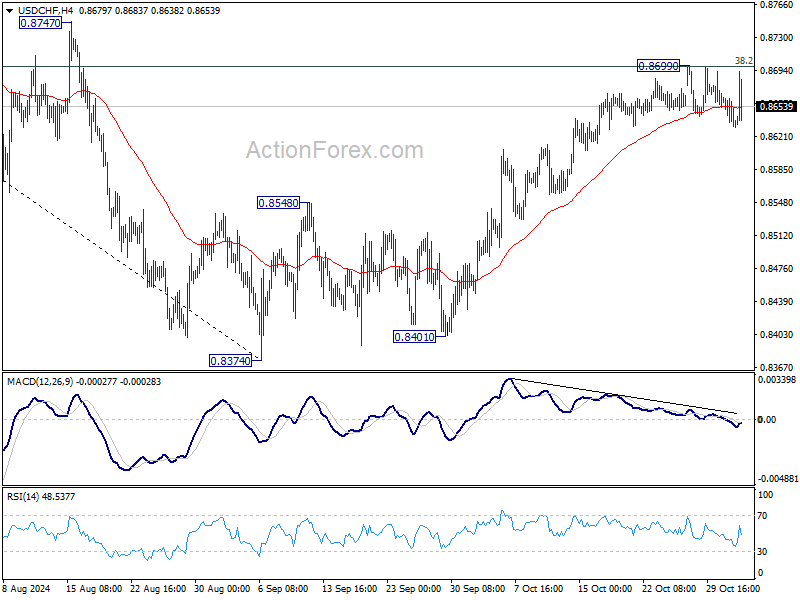

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8622; (P) 0.8646; (R1) 0.8659; More…

USD/CHF is still extending consolidation from 0.8699 and intraday bias remains neutral. Further rally remains in favor as long as 55 D EMA (now at 0.8609) holds. On the upside, decisive break of 38.2% retracement of 0.9223 to 0.8374 at 0.8698 will argue that fall from 0.9223 has completed after defending 0.8332 low. Further rally should then be seen to 61.8% retracement at 0.8899 next.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).