Sample Category Title

USD/CAD Weekly Outlook

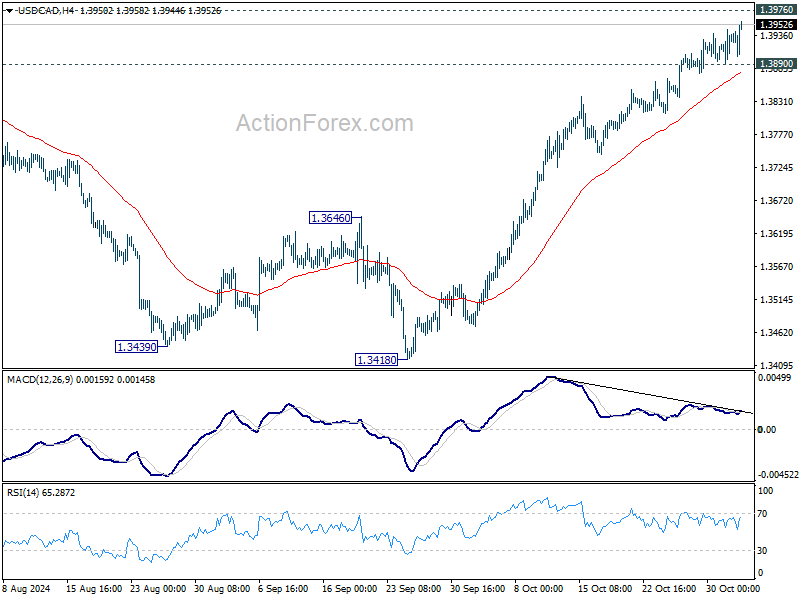

USD/CAD's rally from 1.3418 continued last week and there is no clear sign of topping yet. Initial bias remains on the upside for 1.3976 resistance. Decisive break there will resume larger up trend. Nevertheless, considering bearish divergence condition in 4H MACD, break of 1.3890 minor support will indicate short term topping, and turn bias back to the downside for deeper pullback.

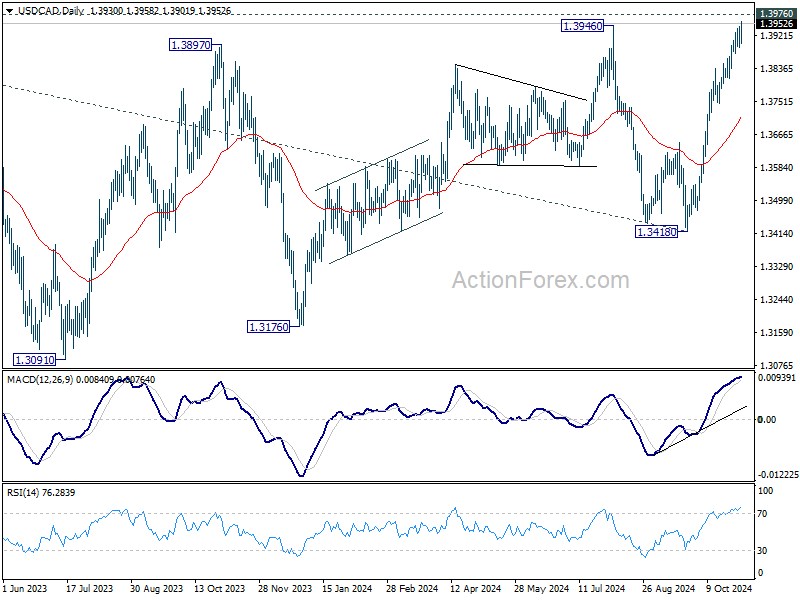

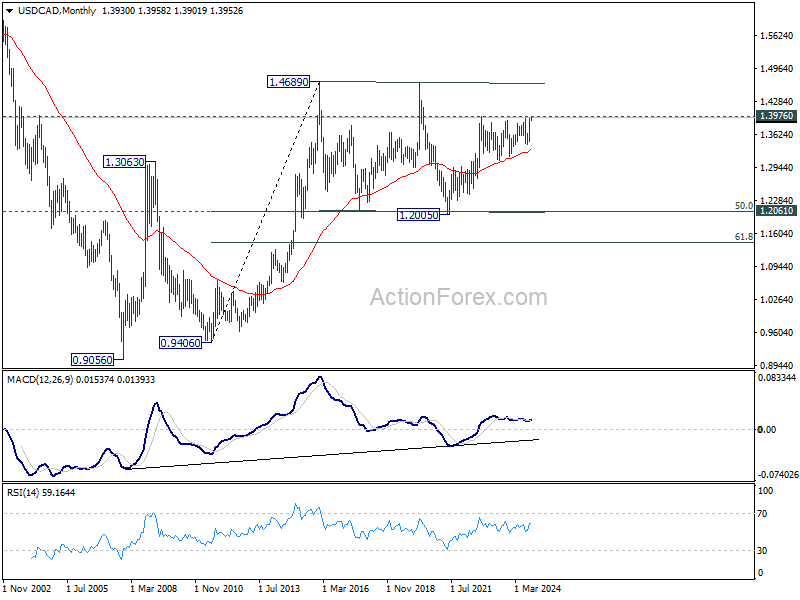

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage. Decisive break of 1.3976 will target 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391.

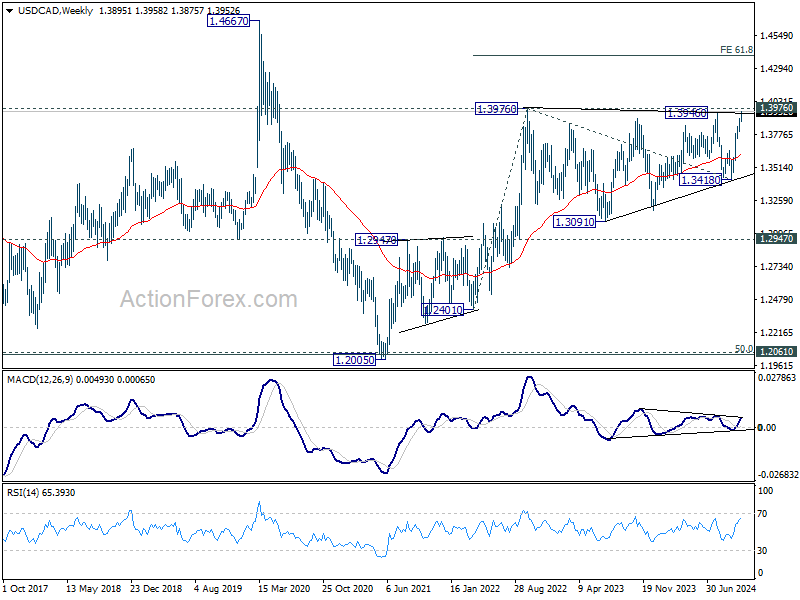

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.2947 resistance turned support holds.

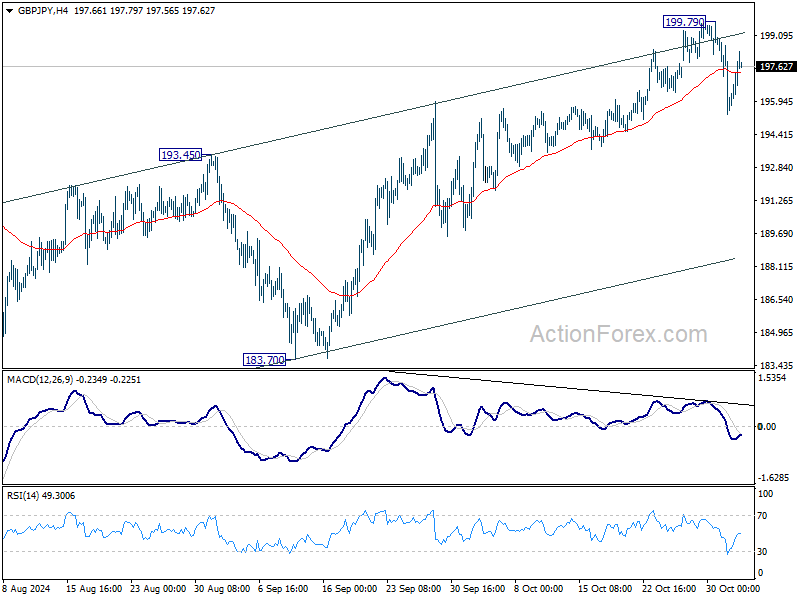

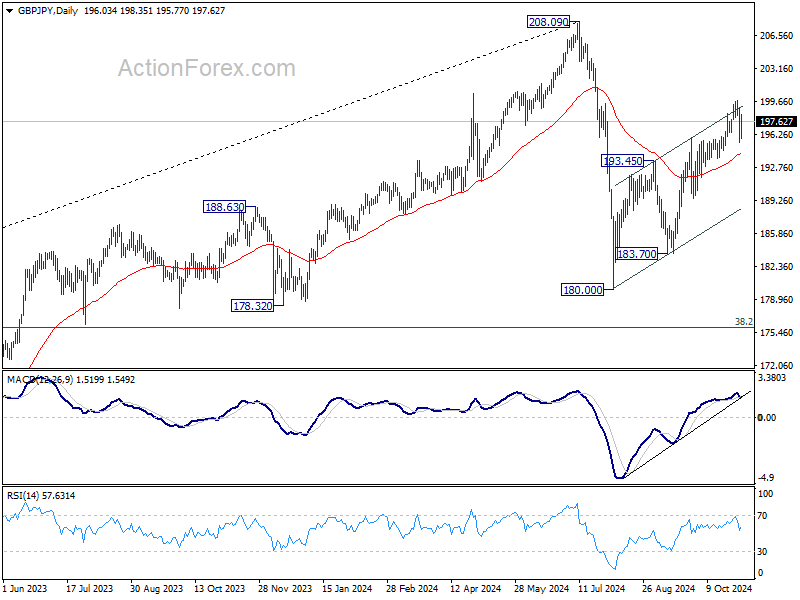

GBP/JPY Weekly Outlook

GBP/JPY edged higher to 199.79 last week but retreat again. Initial bias stays neutral this week first for more consolations. Further rally is expected as long as 55 D EMA (now at 194.26) holds. Above 199.79 will resume the rebound from 180.00 to retest 208.09 high. However, sustained break of 55 D EMA will argue that the corrective rise has completed already, and turn near term outlook bearish for 180.00/183.70 support zone.

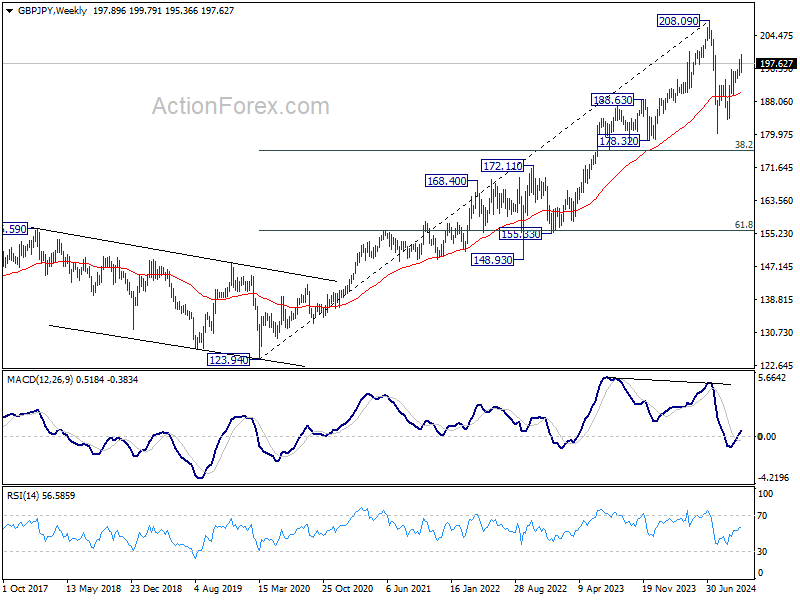

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

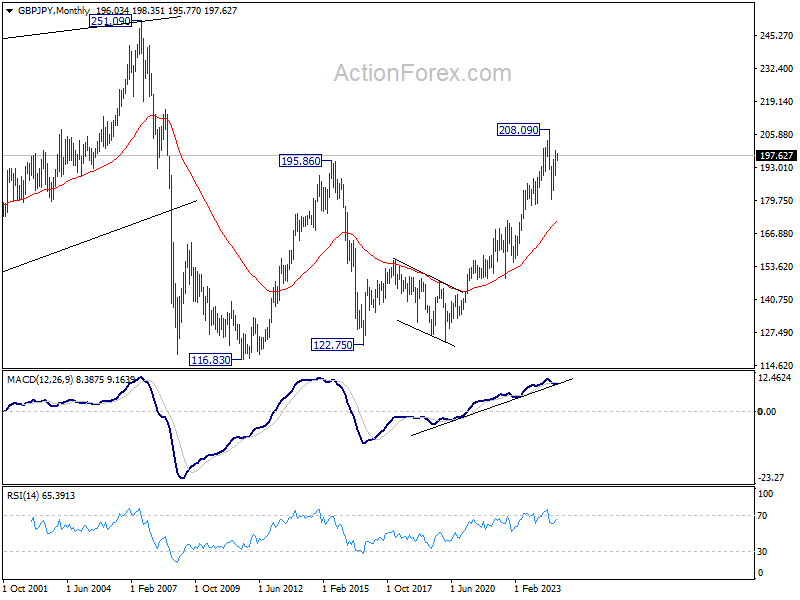

In the longer term picture, considering bearish divergence condition in W MACD, 208.09 is at least a medium term top. It's still early to conclude that the up trend from 122.75 (2016 low) has completed. But it's at least in a medium term corrective phase, with risk of correction to 55 M EMA (now at 172.07).

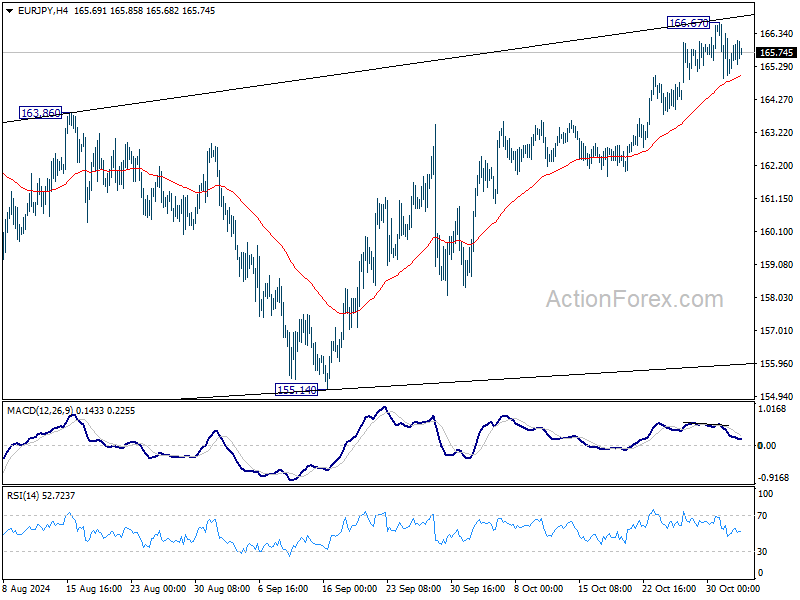

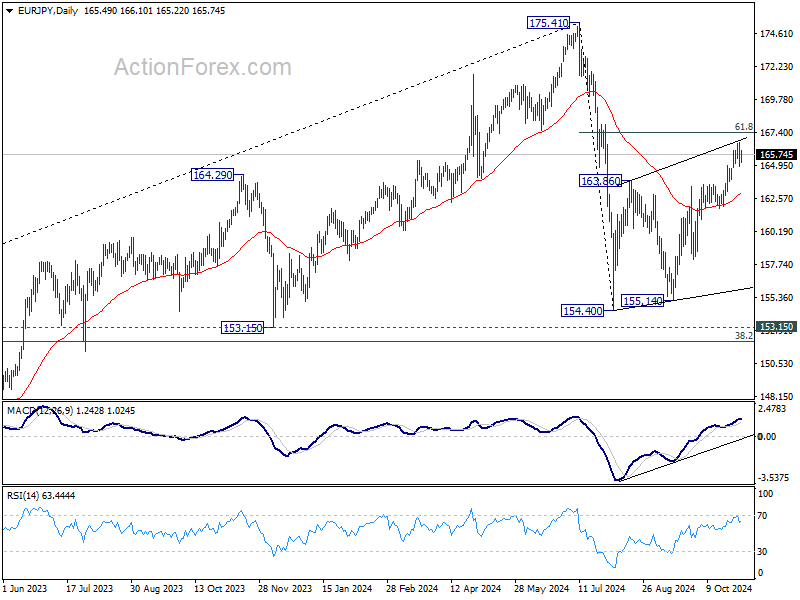

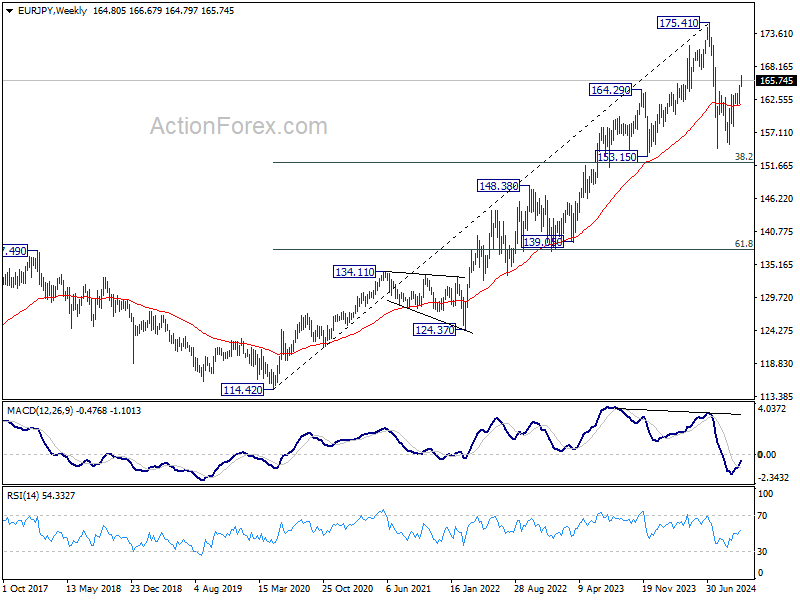

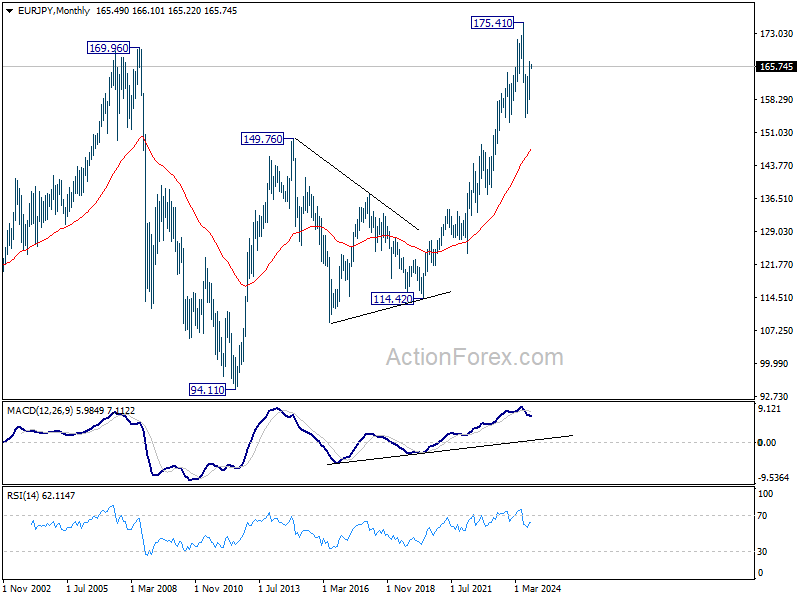

EUR/JPY Weekly Outlook

EUR/JPY's rally extended to 166.67 last week but turned sideway since then. Initial bias remains neutral this week for consolidations first. Further rally is in favor as long as 55 D EMA (now at 162.96) holds. Sustained break of 61.8% retracement of 175.41 to 154.40 at 167.38 will pave the way to retest 175.41 high. However, firm break of 55 D EMA will argue that corrective rise from 154.40 has completed, and turn outlook bearish for this support again.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

In the long term picture, considering bearish divergence condition in W MACD, 175.41 is at least a medium term top. It's still early to conclude that up trend from 94.11 (2012 low) has completed. But a medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 147.40).

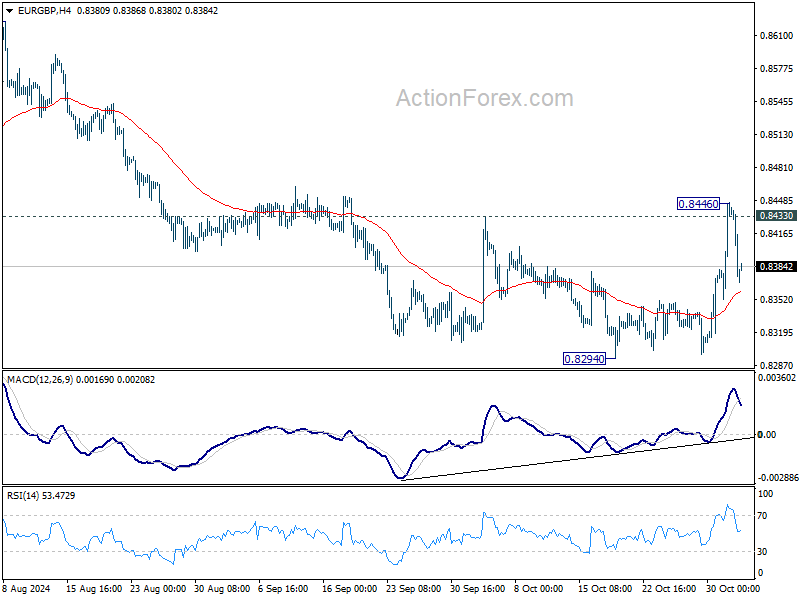

EUR/GBP Weekly Outlook

EUR/GBP rebounded strongly to 0.8446 last week, but failed to sustain above 0.8433 resistance and retreated sharply. Initial bias is turned neutral this week first. On the downside, break of 0.8294 low will resume larger down trend to 0.8201 key support next. On the upside, break of 0.8446 will resume the rebound towards 0.8624 resistance.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

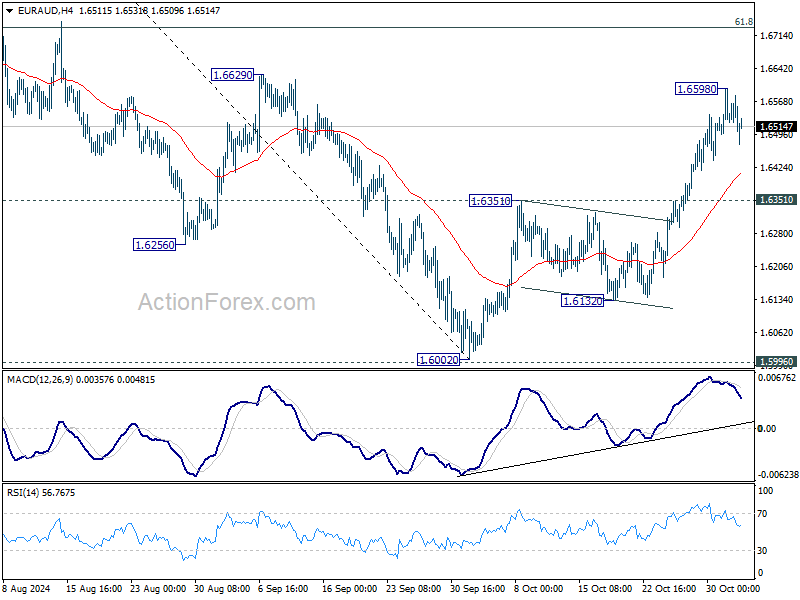

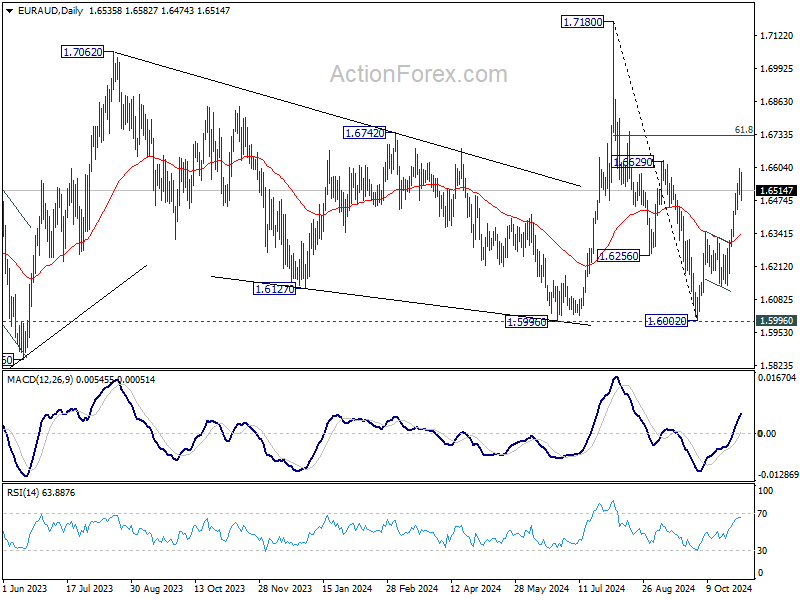

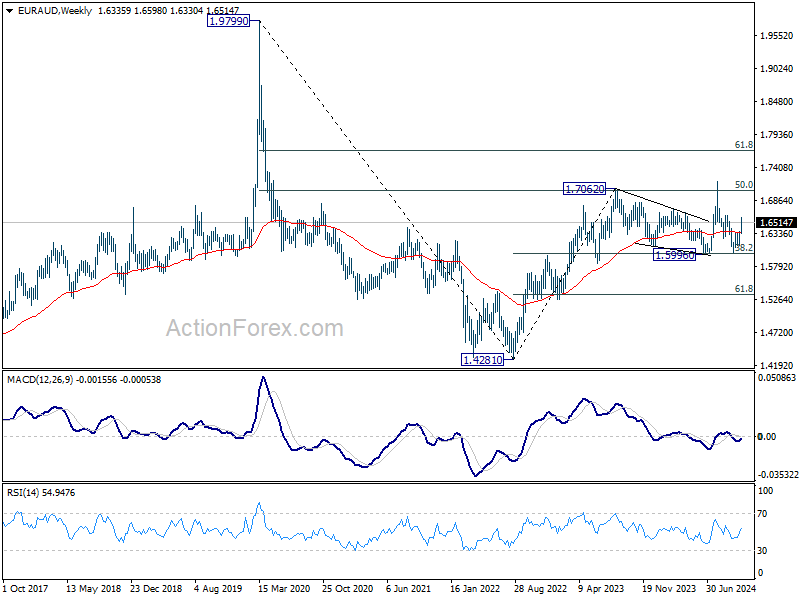

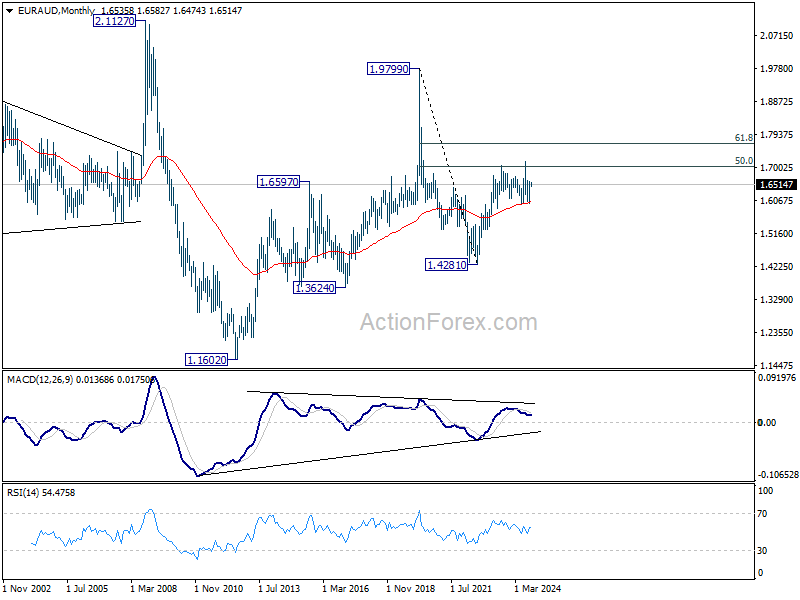

EUR/AUD Weekly Outlook

EUR/AUD's extended rebound last week suggests that corrective fall from 1.7180 has completed with three waves down to 1.6002, after drawing support from 1.5996. But as a temporary top was formed after hitting 1.6598, initial bias is turned neutral this week first. Downside of retreat should be contained by 1.6351 resistance turned support. Above 1.6598 will resume the rise from 1.6002 to 61.8% retracement of 1.7180 to 1.6002 at 1.6730 next. Sustained trading above there will pave the way to retest 1.7180 high.

In the bigger picture, as long as 1.5996 cluster support holds (38.2% retracement of 1.4281 to 1.7062 (2023 high) at 1.6000), up trend from 1.4281 (2022 low) is still expected to resume at a later stage. However, decisive break of 1.5996 will argue that the medium term trend has reversed and turn outlook bearish.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6022) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

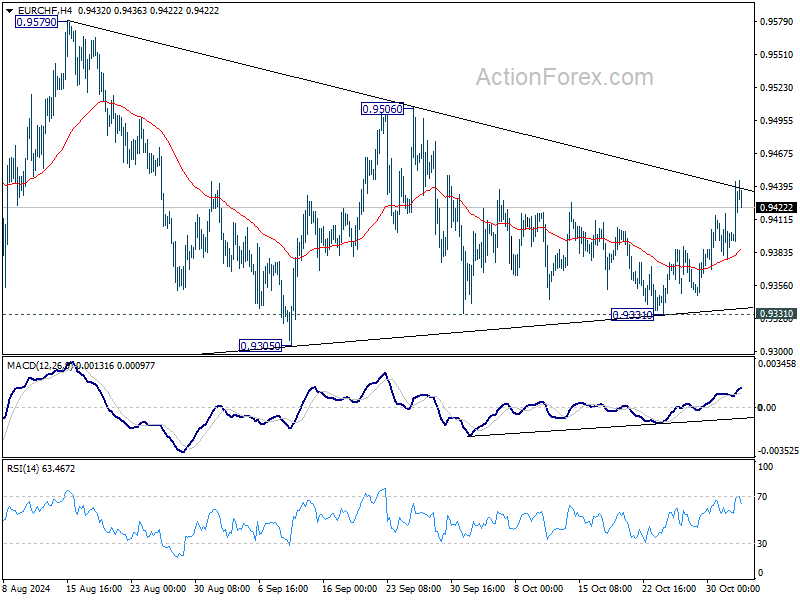

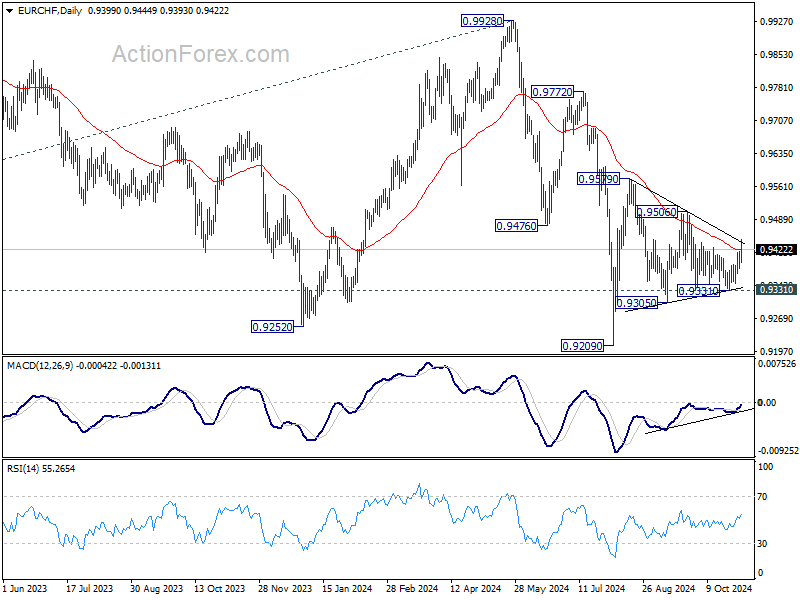

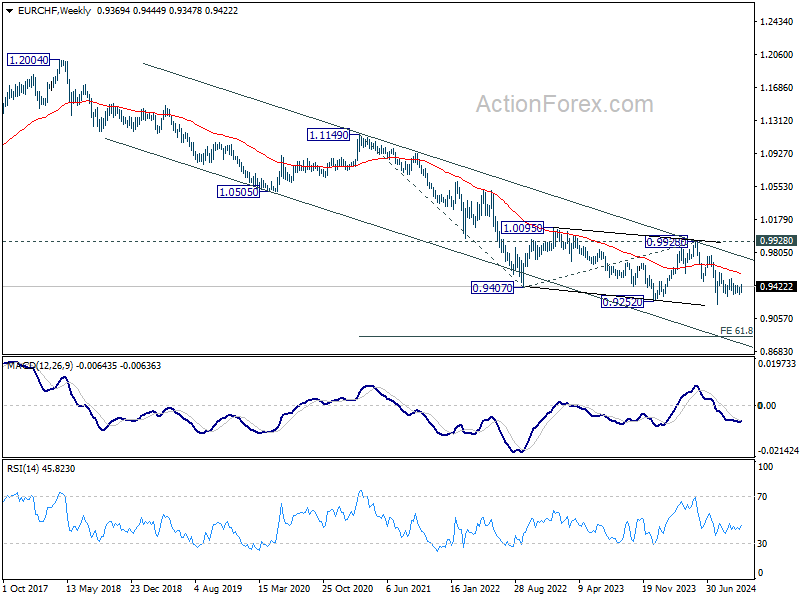

EUR/CHF Weekly Outlook

EUR/CHF rebounded last week but stayed inside near term converging range. Initial bias remains neutral this week first. On the downside, break of 0.9331 will resume the fall from 0.9579 towards 0.9209 low. On the upside, break of 0.9506 will turn intraday bias to the upside for 0.9579 resistance and above.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9421) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming at 0.9209 and bring stronger rebound back towards 0.9928 key resistance.

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption to 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Summary 11/4 – 11/8

Monday, Nov 4, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | TD-MI Inflation Gauge M/M Oct | 0.10% | |

| 08:50 | EUR | FranceManufacturing PMI Oct | 44.5 | 44.5 |

| 08:55 | EUR | Germany Manufacturing PMI Oct | 42.6 | 42.6 |

| 09:00 | EUR | Eurozone Manufacturing PMI Oct | 45.9 | 45.9 |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Nov | -12.7 | -13.8 |

| 15:00 | USD | Factory Orders M/M Sep | -0.40% | -0.20% |

| 23:50 | JPY | Monetary Base Y/Y Oct | 0.30% | -0.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | TD-MI Inflation Gauge M/M Oct | |

| Forecast: | Previous: 0.10% | ||

| 08:50 | EUR | FranceManufacturing PMI Oct | |

| Forecast: 44.5 | Previous: 44.5 | ||

| 08:55 | EUR | Germany Manufacturing PMI Oct | |

| Forecast: 42.6 | Previous: 42.6 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Oct | |

| Forecast: 45.9 | Previous: 45.9 | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Nov | |

| Forecast: -12.7 | Previous: -13.8 | ||

| 15:00 | USD | Factory Orders M/M Sep | |

| Forecast: -0.40% | Previous: -0.20% | ||

| 23:50 | JPY | Monetary Base Y/Y Oct | |

| Forecast: 0.30% | Previous: -0.10% | ||

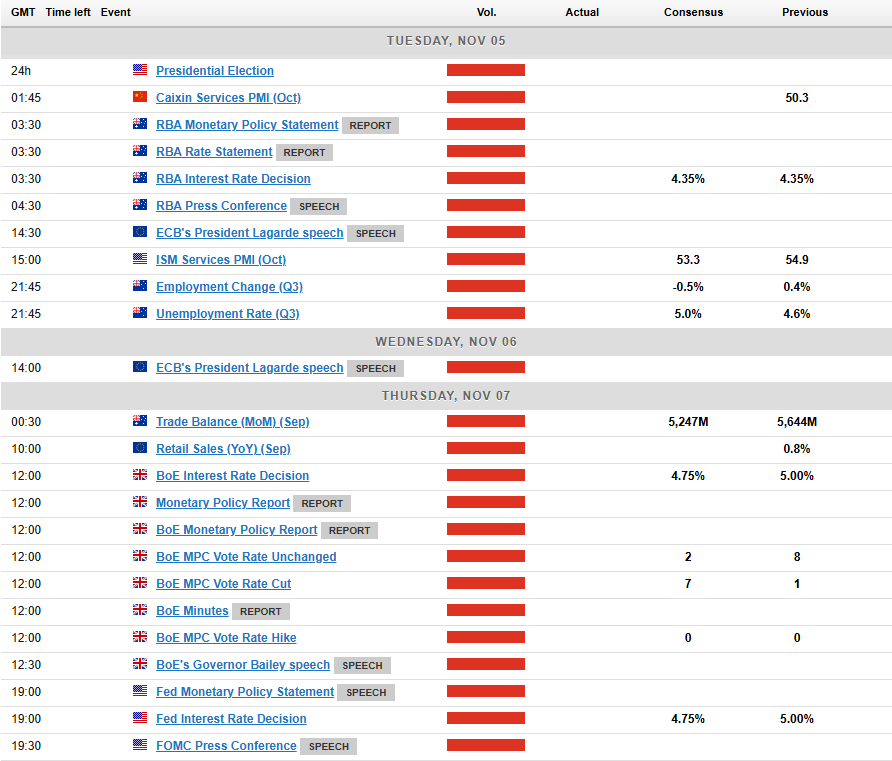

Tuesday, Nov 5, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:45 | CNY | Caixin Services PMI Oct | 50.5 | 50.3 |

| 03:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% |

| 04:30 | AUD | RBA Press Conference | ||

| 06:45 | CHF | Unemployment Rate Oct | 2.60% | 2.60% |

| 07:45 | EUR | France Industrial Output M/M Sep | -0.70% | 1.40% |

| 09:30 | GBP | Services PMI Oct F | 51.8 | 51.8 |

| 13:30 | CAD | Trade Balance (CAD) Sep | -1.6B | -1.1B |

| 13:30 | USD | Trade Balance (USD) Sep | -75.3B | -70.4B |

| 13:45 | USD | Services PMI Oct F | 55.3 | 55.3 |

| 15:00 | USD | ISM Services PMI Oct | 53.3 | 54.9 |

| 18:30 | CAD | BoC Summary of Deliberations | ||

| 21:45 | NZD | Employment Change Q3 | -0.50% | 0.40% |

| 21:45 | NZD | Unemployment Rate Q3 | 5.00% | 4.60% |

| 21:45 | NZD | Labour Cost Index Q/Q Q3 | 0.70% | 0.90% |

| 23:50 | JPY | BoJ Minutes |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:45 | CNY | Caixin Services PMI Oct | |

| Forecast: 50.5 | Previous: 50.3 | ||

| 03:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 4.35% | Previous: 4.35% | ||

| 04:30 | AUD | RBA Press Conference | |

| Forecast: | Previous: | ||

| 06:45 | CHF | Unemployment Rate Oct | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 07:45 | EUR | France Industrial Output M/M Sep | |

| Forecast: -0.70% | Previous: 1.40% | ||

| 09:30 | GBP | Services PMI Oct F | |

| Forecast: 51.8 | Previous: 51.8 | ||

| 13:30 | CAD | Trade Balance (CAD) Sep | |

| Forecast: -1.6B | Previous: -1.1B | ||

| 13:30 | USD | Trade Balance (USD) Sep | |

| Forecast: -75.3B | Previous: -70.4B | ||

| 13:45 | USD | Services PMI Oct F | |

| Forecast: 55.3 | Previous: 55.3 | ||

| 15:00 | USD | ISM Services PMI Oct | |

| Forecast: 53.3 | Previous: 54.9 | ||

| 18:30 | CAD | BoC Summary of Deliberations | |

| Forecast: | Previous: | ||

| 21:45 | NZD | Employment Change Q3 | |

| Forecast: -0.50% | Previous: 0.40% | ||

| 21:45 | NZD | Unemployment Rate Q3 | |

| Forecast: 5.00% | Previous: 4.60% | ||

| 21:45 | NZD | Labour Cost Index Q/Q Q3 | |

| Forecast: 0.70% | Previous: 0.90% | ||

| 23:50 | JPY | BoJ Minutes | |

| Forecast: | Previous: | ||

Wednesday, Nov 6 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Services PMI Oct F | 49.3 | 49.3 |

| 07:00 | EUR | Germany Factory Orders M/M Sep | 1.80% | -5.80% |

| 08:50 | EUR | France Services PMI Oct F | 48.3 | 48.3 |

| 08:55 | EUR | Germany Services PMI Oct F | 51.4 | 51.4 |

| 09:00 | EUR | Eurozone Services PMI Oct F | 51.2 | 51.2 |

| 09:30 | GBP | Construction PMI Oct | 55.3 | 57.2 |

| 10:00 | EUR | Eurozone PPI M/M Sep | -0.50% | 0.60% |

| 10:00 | EUR | Eurozone PPI Y/Y Sep | -3.50% | -2.30% |

| 15:00 | CAD | Ivey PMI Oct | 54.2 | 53.1 |

| 15:30 | USD | Crude Oil Inventories | -0.5M | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Sep | 3.00% | 2.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Services PMI Oct F | |

| Forecast: 49.3 | Previous: 49.3 | ||

| 07:00 | EUR | Germany Factory Orders M/M Sep | |

| Forecast: 1.80% | Previous: -5.80% | ||

| 08:50 | EUR | France Services PMI Oct F | |

| Forecast: 48.3 | Previous: 48.3 | ||

| 08:55 | EUR | Germany Services PMI Oct F | |

| Forecast: 51.4 | Previous: 51.4 | ||

| 09:00 | EUR | Eurozone Services PMI Oct F | |

| Forecast: 51.2 | Previous: 51.2 | ||

| 09:30 | GBP | Construction PMI Oct | |

| Forecast: 55.3 | Previous: 57.2 | ||

| 10:00 | EUR | Eurozone PPI M/M Sep | |

| Forecast: -0.50% | Previous: 0.60% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Sep | |

| Forecast: -3.50% | Previous: -2.30% | ||

| 15:00 | CAD | Ivey PMI Oct | |

| Forecast: 54.2 | Previous: 53.1 | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -0.5M | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Sep | |

| Forecast: 3.00% | Previous: 2.80% | ||

Thursday, Nov 7, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Sep | 5.28B | 5.64B |

| 03:00 | CNY | Trade Balance (USD) Oct | 73.5B | 81.7B |

| 07:00 | EUR | Germany Industrial Production M/M Sep | -1.00% | 2.90% |

| 07:00 | EUR | Germany Trade Balance (EUR) Sep | 24.3B | 22.5B |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Oct | 716B | |

| 10:00 | EUR | Eurozone Retail Sales M/M Sep | 0.40% | 0.20% |

| 12:00 | GBP | BoE Interest Rate Decision | 4.75% | 5.00% |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0--8--1 | 0--1--8 |

| 13:30 | USD | Initial Jobless Claims (Nov 1) | 220K | 216K |

| 13:30 | USD | Nonfarm Productivity Q3 P | 2.30% | 2.50% |

| 13:30 | USD | Unit Labor Costs Q3 P | 0.50% | 0.40% |

| 15:00 | USD | Wholesale Inventories Sep F | -0.10% | -0.10% |

| 15:30 | USD | Natural Gas Storage | 78B | |

| 19:00 | USD | Fed Interest Rate Decision | 4.75% | 5.00% |

| 19:30 | USD | FOMC Press Conference | ||

| 23:30 | JPY | Household Spending Y/Y Sep | -1.80% | -1.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Sep | |

| Forecast: 5.28B | Previous: 5.64B | ||

| 03:00 | CNY | Trade Balance (USD) Oct | |

| Forecast: 73.5B | Previous: 81.7B | ||

| 07:00 | EUR | Germany Industrial Production M/M Sep | |

| Forecast: -1.00% | Previous: 2.90% | ||

| 07:00 | EUR | Germany Trade Balance (EUR) Sep | |

| Forecast: 24.3B | Previous: 22.5B | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Oct | |

| Forecast: | Previous: 716B | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Sep | |

| Forecast: 0.40% | Previous: 0.20% | ||

| 12:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 4.75% | Previous: 5.00% | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 0--8--1 | Previous: 0--1--8 | ||

| 13:30 | USD | Initial Jobless Claims (Nov 1) | |

| Forecast: 220K | Previous: 216K | ||

| 13:30 | USD | Nonfarm Productivity Q3 P | |

| Forecast: 2.30% | Previous: 2.50% | ||

| 13:30 | USD | Unit Labor Costs Q3 P | |

| Forecast: 0.50% | Previous: 0.40% | ||

| 15:00 | USD | Wholesale Inventories Sep F | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 78B | ||

| 19:00 | USD | Fed Interest Rate Decision | |

| Forecast: 4.75% | Previous: 5.00% | ||

| 19:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

| 23:30 | JPY | Household Spending Y/Y Sep | |

| Forecast: -1.80% | Previous: -1.90% | ||

Friday, Nov 8, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Sep P | 108.9 | 106.9 |

| 07:45 | EUR | France Trade Balance (EUR) Sep | -7.0B | -7.4B |

| 08:00 | CHF | SECO Consumer Climate Q4 | -33 | -34 |

| 13:30 | CAD | Net Change in Employment Oct | 33.2K | 46.7K |

| 13:30 | CAD | Unemployment Rate Oct | 6.60% | 6.50% |

| 15:00 | USD | Michigan Consumer Sentiment Index Nov P | 70 | 70.5 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Sep P | |

| Forecast: 108.9 | Previous: 106.9 | ||

| 07:45 | EUR | France Trade Balance (EUR) Sep | |

| Forecast: -7.0B | Previous: -7.4B | ||

| 08:00 | CHF | SECO Consumer Climate Q4 | |

| Forecast: -33 | Previous: -34 | ||

| 13:30 | CAD | Net Change in Employment Oct | |

| Forecast: 33.2K | Previous: 46.7K | ||

| 13:30 | CAD | Unemployment Rate Oct | |

| Forecast: 6.60% | Previous: 6.50% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Nov P | |

| Forecast: 70 | Previous: 70.5 | ||

Markets Weekly Outlook – US Elections and Central Banks Lead the Way

- Global markets experienced a mixed week, influenced by geopolitical risks and US jobs data revisions.

- The week ahead focuses on China’s Standing Committee meeting, the US election and Central Bank Meetings.

- Wall Street indexes struggled, potentially due to high valuations and AI capital spend.

Week in Review: US Jobs Revised Downward After Positive GDP

A mixed week comes to a close as markets deal with renewed geopolitical risks and another downgrade to jobs numbers by the US Bureau Labor of statistics. US Earnings was another area that both surprised and disappointed as Wall Street fret about growing AI capital expenditure.

Six of the ‘Magnificent 7’ companies have already reported with revenue and profit beats but rising capital expenditure around AI continues to weigh on the minds of market participants. Amazon however soared on Friday as it shook off the blues of the Q2 earnings report and on course to post its best day since February, up around 6.5%. This helped Wall Street Indexes rise on Friday after the US open. Apple disappointed markets but the stock price held firm with the technology company down 0.5% on the day.

The NFP report did not paint a pretty picture as markets digested another significant downward revision to the previous two months data. The last two job reports were revised lower by a combined 112k jobs with the August report revised down by 81k and the September number by 31000. This has given the Fed more room on the rate cut front just as market participants were eyeing the possibility of less rate cuts moving forward.

Source: LSEG (click to enlarge)

When it comes to performance, the US Dollar Index saw four days of declines this week before a resurgence on Friday. This came as a surprise as market participants were pricing in more aggressive rate cuts which in theory should have led to further USD weakness. Are we seeing the US Dollars safe haven appeal returning?

Commodities saw Oil trickle higher for the majority of the week but finding hurdles consistently. Brent has been unable to close the gap it left over the weekend, but is still up around 2.5% for the week. Gold reached fresh highs before suffering a $60 drop on Thursday before steadying slightly on a Friday. Given the rising risks and geopolitics at play, it would take a brave person to hold onto gold shorts at present.

Wall Street Indexes have all struggled this week and are on course to finish in the red. The sky high company and index valuations may also be off putting to market participants. Will US Indexes be able to stage a recovery in US Election and FOMC week?

The Week Ahead: China’s Standing Committee Meeting, US Election and Central Bank Meetings

Asia Pacific Markets

The week ahead in Asia will see focus pivot back to China, while rising tensions with North Korea need to be monitored as well.

In China, next week will be the meeting of China’s Standing Committee of the National People’s Congress, which will take place between 4-8 November. Markets are paying close attention to see if there will be changes to budget targets or details about new bonds. This would help understand the size of future financial plans. The slow start of this financial boost has lessened some of the initial excitement after monetary policy changes in September, but a big new financial package could bring back that enthusiasm.

Next week is relatively quiet for data releases. Trade data is expected on Thursday, where we anticipate export growth to slightly increase to about 5% year-on-year. However, we expect import growth to drop to -5.0% year-on-year after staying close to zero in the previous months.

Japan has just come off a busy week with next week expected to be much more subdued. Labor cash earnings will be a key release to watch as wage growth has been a key for the BoJ in its policy normalization efforts. Therefore a significant uptick here could add some strength to the struggling JPY.

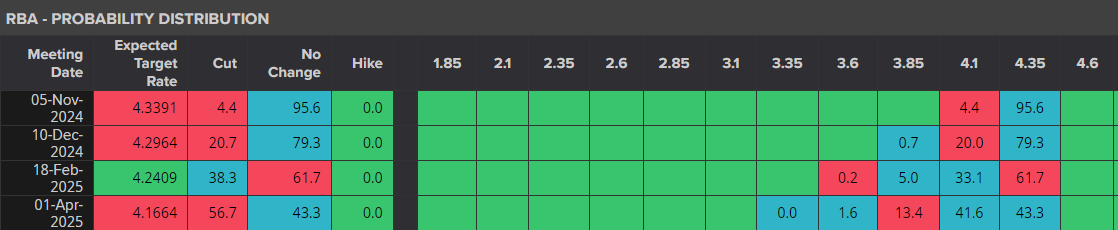

The RBA are holding their interest rate meeting next week and this follows on from the inflation data this week. Inflation came in much better than expected, now at its lowest level since Q1 2021 with a print of 2.8%.

Markets appear convinced that despite the drop in inflation the RBA will keep rates on hold. Markets are pricing in around a 95.6% chance that the RBA keep rate on hold. Will we get a surprise?

Source: LSEG (click to enlarge)

Europe + UK + US

In developed markets, the European Union is enjoying a slight respite with the major data release being retail sales. There are also two speeches from ECB President Christine Lagarde, which after the recent bout of data may provide some insight into ECB policy moving forward.

The UK is set for another busy week after the Autumn Budget was released this week. A mixed bag and reaction to the budget heading into the BoE meeting leaves the British Pound in an intriguing position against many of its counterparts.

According to LSEG data, markets are pricing in around an 84% probability of a 25 bps cut next week which could send the British Pound lower.

The biggest events next week however are from the United States. The US Election is on Tuesday with the FOMC meeting following the very next day. The jobs data downgrades on Friday have really cemented rate cuts from the Fed at both the November and most likely December meetings.

The US Election is the one with the most uncertainty as polling has thrown up extremely mixed numbers. Betting websites have Donald Trump as the front runner, while a Reuters/Ipsos poll and a few others have Kamala Harris in the lead. The question is who prevails and what will the impact be? A trump win could help benefit Gold prices as market participants may use it as a hedge against the pending uncertainties.

Besides Gold we could see some wild swing in US Dollar pairs, Wall Street Indexes and potentially a knock on effect for markets as a whole as risk sentiment sways back and forth.

Chart of the Week

This week’s focus is back to Gold, following fresh highs and a significant pullback in what was a very choppy week.

There are of course factors supporting further increases in the Gold prices as global uncertainties continue to rack up.

Having made its run toward $2800 an ounce and falling short, this may see gold bulls make one final attempt at a test or breach of the $2800 handle.

A move higher from here will bring 2750 back on the table for the 2775 price level becomes an area of focus.

Conversely a move lower from here needs to break the 2724 handle before the 2714 and 2700 come into focus.

The RSI on the daily has finally left overbought territory which could be a sign of a shift in momentum. However, at present i would say, keep a close eye on geopolitical developments as this could have a major impact on markets over the weekend.

Gold (XAU/USD) Daily Chart – November 1, 2024

Source: TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 2724

- 2714

- 2700

Resistance

- 2775

- 2790

- 2800

The Weekly Bottom Line: Canada’s interest rate conundrum; Too much of a good thing

Canadian Highlights

- A call for a jumbo cut to head off mortgage reset rates must be assessed carefully. Surprisingly, roughly a quarter of mortgages will reset at a LOWER interest rate next year.

- For those renewing into higher rates, the shock might be milder than expected, given a 30% increase in home prices and wages. Years of debt repayments have also built equity room, which homeowners, including those with variable-rate-fixed-payments mortgages, can use to lower payments if needed.

- While rapid rate cuts can relieve mortgage pressures, they also stoke risks. Restoking housing demand, pulling forward consumer spending, weakening purchasing power and dampening investment through a softer loonie. Indeed, there is such a thing as too much of a good thing.

U.S. Highlights

- The U.S. economy expanded by a robust 2.8% quarter-on-quarter (annualized) in the third quarter, only a touch slower than the 3% pace seen in Q2.

- Growth in both income and consumer spending picked up in September while core PCE inflation held steady at 2.7% y/y.

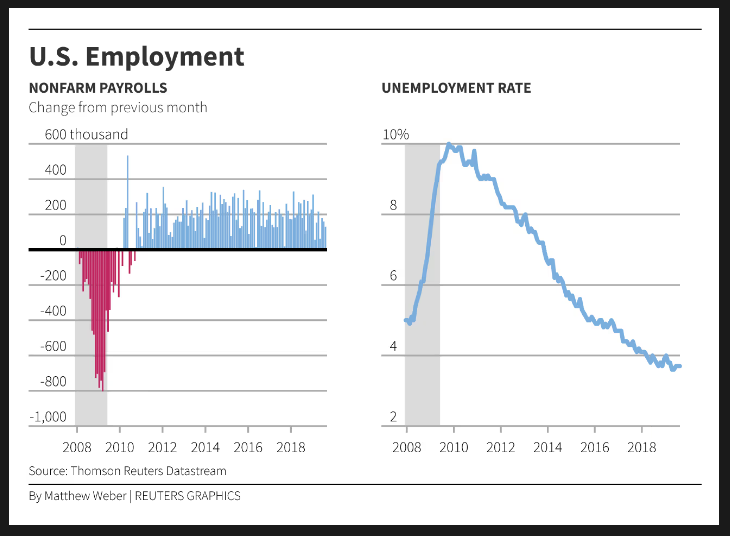

- Employment was essentially flat in October, with the economy adding a meager 12k jobs – well below the already-low 100k consensus estimate. The ongoing Boeing strike and disruptions related to Hurricanes Helene and Milton both weighed on the headline.

Canada – Canada’s interest rate conundrum: Too much of a good thing

Last week, we published on the Bank of Canada’s decision to deliver an outsized 50-basis-point interest rate cut. Some clients have commented that a faster descent is necessary to head off mortgage renewal risks. The concern is embedded in the lingering effects of the pandemic. In 2020, home sales shot up 40% in just twelve months as the Bank of Canada slashed the policy rate to near-zero. Homebuyers responded to a once-in-a-generation deal on mortgage rates. Now as 2025 approaches, those renewing a 5-year mortgage – the preferred term in Canada – could face sticker shock.

Chart 1 offers some comfort with three key messages:

First, it will likely surprise many that roughly a quarter of mortgages will reset at a LOWER interest rate. Many homeowners in the past two years selected shorter mortgage terms in the hopes that the Bank of Canada would be cutting rates as renewals hit. Good call! The savings will be tremendous. Depending on the institution, the current 5-year mortgage rate is between 4.0% and 4.7% compared to the prior average transaction rates of 5.8% to 6.9% for those folks. That’s a huge step down that will free up disposable income.

Second, the majority of mortgages coming up for renewal next year and in 2026 sit at an average rate of 2.5%. There will be upward pressure on monthly payments for these folks. However, not as much as you might think. Since 2020, Canadian home prices and wages have both risen by over 30%. And five years of debt paydown has created equity room that could be taken back up if homeowners want to mitigate the increase in monthly mortgage payments by extending their amortization.

The benefits of lower rates and higher equity hold true for variable rate mortgage holders too. Those with variable payments have already experienced some rate relief due to 125 basis points in interest rate cuts so far. For a $500,000 mortgage, this translates to a $370 reduction in the monthly payment. For borrowers whose payments do not adjust with rate changes, these reductions will bring benefits at renewal in the form of either lower monthly payments or a shorter amortization period. Moreover, it appears that this group is faring better than initially anticipated when analysts looked at the data a year ago. Many borrowers have proactively increased their payments, effectively reducing their average amortization period by a full year (Chart 2).

Lastly, financial risks are further lowered than many Canadians presume due to past macroprudential rules. Canada’s mortgage stress test requires mortgage applicants to qualify not at their contract rate, but at an interest rate that is two percentage points higher, or a floor rate of 5.25%, whichever is higher. With the 5-year mortgage rate floating at around the 4% mark, homeowners who secured rates in the 2% range in 2020 remain within the scope of that stress test. If they qualified then for a mortgage, they should be sitting in a better spot today with the benefit of time and wage gains, presuming there hasn’t been a change in the household income status. Given the lack of job losses in the job market, this assumption holds true for most.

Bottom line, when rates were rising rapidly, mortgage renewals were on everyone’s mind as a key risk that required flagging by the Bank of Canada. But it no longer presents itself as that lurking monster of 2025. By extension, it’s not the smoking gun for ongoing 50 basis point rate cuts. It’s important to balance the two-sided nature of risks. The other side is inadvertently restoking the housing market, leading to a new cycle of restrained affordability and debt accumulation. The Bank must also be mindful of underestimating the spending impulse. A more rapid rate-cut cycle will pull forward or front load consumer spending relative to a gradual cycle. Because data is lagged, by the time it’s readily observed, the momentum impulse could be stronger than anticipated and require course correction. And finally, caution is warranted in creating too wide an interest rate spread to the U.S.. The loonie has already broken below a technical threshold by dipping below 72 cents. Chronic weakness reduces Canada’s purchasing power abroad, which can become counterproductive to investment because firms source a significant amount of machinery and equipment from other countries.

We must remember, there is such a thing as too much of a good thing.

U.S. – The U.S. GDP data delivers treats, but the payrolls report plays tricks

Next week all eyes will be on the U.S. elections and the Federal Reserve meeting. However, this week the focus has been on the health of the U.S. economy – an important reference point for both presidential candidates and the Fed.

Wednesday’s advanced GDP report showed that the U.S. economy is alive and well. Coming on the heels of the solid 3% gain in Q2, the economy expanded by 2.8% (quarter-over-quarter annualized) in Q3. Consumers were the belle of the ball, with spending accelerating to 3.7%, or the fastest pace since Q1 2023 (Chart 1).

This ongoing resilience was further echoed in September’s personal income and spending report. It showed that spending increased by 0.5% m/m in September, outpacing income and indicating that consumers kept their purse strings open as Q3 wrapped up. Lower prices at the pump in recent weeks may have boosted confidence, giving consumers some reprieve from the ever-rising prices elsewhere. On that front, core PCE deflator – which excludes food and energy – rose 0.3% m/m in September. This held the twelve-month change steady at 2.7% for the third consecutive month, but this was largely due to “base effects”. Importantly, the 3-and-6-month annualized rates of change sit just above the Fed’s 2% inflation target, suggesting we’re likely to see more downward pressure on the year-ago measure in the months ahead.

As we noted in a recent report, there are several reasons consumers may have more momentum than previously anticipated, such as a notable upgrade to personal income in first half of 2024 and a larger buffer of savings. However, the savings cushion is quickly dwindling, with the personal saving rate having now declined for three consecutive months. This suggests we’re likely to see some moderation in consumer spending to something more consistent with a trend-like pace of around 2% in the months ahead.

On that note, October’s payroll report was expected to be a weak one, but still surprised to the downside. The economy added just 12k jobs in October, well below the expectation for a 100k gain, while. Adding to the disappointment, downward revisions shaved 112k from the two prior months’ gains. The ongoing Boeing strike helped to cut over 40k from the headline number in October, while Hurricanes Helene and Milton also likely had a heavy hand weighing down the payrolls figure.

As a result, the Fed will likely look through October’s noisy employment data, and instead focus more on the broader trends showing that the labor market is decelerating but not necessarily deteriorating. Moreover, with the Fed’s preferred wage metric – the Employment Cost Index – showing wage pressures now growing at a pace roughly consistent with 2% inflation, the FOMC should have all the confidence they need to continue to gradually reduce the policy rate. We expect the Fed to cut by 25 basis-points at next week’s meeting. While this decision seems almost certain, the U.S. elections remain a wild card, promising to keep everyone on edge until the final votes are tallied.

Weekly Economic & Financial Commentary: What Goes Up, Must Come Down

Summary

United States: It’s Halloween. Everyone’s Entitled to One Good Scare.

- Nonfarm payrolls rose a much weaker-than-expected 12K in October. Worker strikes and hurricanes played a major role in the headline miss. The unemployment rate, which is derived from the household survey and counts those not working due to a strike or severe weather as employed, held steady at 4.1%. A 25 bps rate cut at next week's FOMC meeting remains highly likely.

- Next week: ISM Services (Tue.), Nonfarm Productivity (Thu.), Consumer Sentiment (Fri.)

International: Bank of Japan Holds Policy Steady Amid Political Uncertainty

- It was a remarkable week in Japanese politics as the Liberal Democratic Party (LDP) suffered its first major loss in the country's lower house in more than a decade. As a result, we see political uncertainty persisting in the coming weeks. It is against this backdrop that the Bank of Japan held monetary policy steady this week. Looking ahead, we remain comfortable with our forecast for the next 25 bps rate hikes to come at the January 2025 and April 2025 meetings.

- Next week: Brazil Selic Rate (Wed.), Riksbank Policy Rate (Thu.), Bank of England Policy Rate (Thu.)

Interest Rate Watch: What Goes Up, Must Come Down

- We expect the FOMC to elect to reduce the federal funds rate 25 bps at next week's monetary policy meeting. Economic growth has generally remained solid since the Committee last met in September, but the restrictive stance of policy today supports a further reduction.

Credit Market Insights: Refinancing Activity Slows Down Amid Pickup in Mortgage Rates

- Mortgage rates have risen sharply over the past weeks despite expectations the start of the Fed's rate cutting cycle would help ease pressure on financing costs for home buyers. As a result, refinancing activity that had once picked up has since tumbled back down to this summer's lows.

Topic of the Week: The Election Is Near; Is Consumer Confidence Poised for a Rebound?

- The U.S. presidential election, a major source of uncertainty for consumers, is less than one week away. It is instructive to explore how consumer confidence levels have rebounded following November elections in previous cycles and how this cycle compares.