Sample Category Title

US NFP grows only 12k in Oct, unemployment rate steady at 4.1%

US non-farm payroll employment grew only 12k in October, well below expectation of 106k. That compares to average monthly gain of 194k over the prior 12 months.

Nevertheless, unemployment rate was unchanged at 4.1%, matched expectations. number of unemployed people was little changed at 7.0m. Participation rate ticked down from 62.7% to 62.6%.

Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Annual growth of average hourly earnings ticked up from 3.9% yoy to 4.0% yoy.

GBP/USD Technical: Trendline Break Sets the Stage for Further Downside

- GBP/USD has broken below a long-term ascending trendline, signaling potential further downside.

- UK budget concerns and a drop in manufacturing PMI have contributed to the Pound’s struggle.

- UK budget concerns and a drop in manufacturing PMI have contributed to the Pound’s struggle.

Cable has struggled this week following the UK budget. Pound Sterling should have appreciated against the greenback considering the paring back of rate cut expectations from the Bank of England (BoE).

Following the UK budget expectations for the Bank of England to lower interest rates have dropped. This change came after the UK Chancellor announced the biggest tax increase since 1993, worth 40 billion pounds, along with plans to increase government spending and investment by raising the fiscal deficit. Additionally, the Office for Business Responsibility predicted higher inflation rates of 2.5% in 2024 and 2.6% in 2025, leading traders to reduce their bets on rate cuts by the Bank.

There are some other concerns around the UK budget which was raised by Moodys as well and could explain the British Pounds struggle. There are concerns that the added borrowing will impact the UKs ability to bring their finances in order. Moodys also stated that the UK budget creates challenges and cautioned that we could see muted growth from the UK moving forward.

The continued selloff in the US Dollar was not enough to arrest the slide in GBP/USD before a bounce occurred this morning. The release of the S&P Global Flash UK Manufacturing PMI dropped to 49.9 in October 2024, down from 51.5 the previous month. This was lower than expected and shows the first drop in factory activity since April. New orders decreased as clients waited for the UK budget.

Orders from abroad also fell for the 33rd month, with fewer orders from Europe, China, and the US. Production increased slightly as factories worked through their backlog of orders. Manufacturing jobs grew for the third time in four months, but more slowly because of fewer new orders. Costs for materials dropped to their lowest in ten months, and selling prices went up the least since February. Business optimism improved a little from a nine-month low in September. The data however appeared to have little impact on GBP/USD ahead of the US session

Source: FinancialJuice (click to enlarge)

A batch of US data awaits later in the day with the US jobs report chief among them. Markets are anticipating a strong number following labor data seen earlier in the week and should this come to pass, it will be interesting to gauge if cable can shrug off the US data and continue its move higher today.

GBP/USD Technical Analysis

GBP/USD is now at an interesting place as it has broken below the long-term ascending trendline which began back in April.

This trendline break opens up a host of scenarios and potential opportunities in cable moving forward. I could see a retest of the trendline developing before a continuation of the move lower with a deeper pullback to the 1.300 handle also a possibility.

Any such pullback may be preferred for any would-be-shorts looking to get involved. A break and daily candle close above the 1.30150 handle would invalidate the bearish setup.

Looking at the downside, support rests at the 200-day MA around 1.2800 before the 1.2750 and 1.2681 handles come into focus.

GBP/USD Daily Chart, November 1, 2024

Source: TradingView.com (click to enlarge)

Support

- 1.2845

- 1.2800

- 1.2750

Resistance

- 1.2942

- 1.3000

- 1.3033

SPX 500: Second Sign of Downside Volatility Emerges, Odds of Medium-Term Corrective Decline Increase

- Bearish reversal detected below 5,930 key medium-term resistance of the SPX 500.

- Market breadth indicator (% of component stocks above 20-day and 50-day moving averages) has deteriorated.

- The odds have increased for a medium-term corrective decline on the SPX 500 as the key US presidential election risk event looms on 5 November.

Since our last publication, the S&P 500 has reversed down by 3% from its current all-time high of 5,878 printed on 17 October, and right below the 5,930 key medium-term resistance highlighted earlier. It also ended October with a monthly loss of almost 1% dragged down by lackluster revenue guidance from three mega-cap technology stocks: Microsoft, Meta Platforms, and Apple.

Market breadth has turned weak

Fig 1: % of S&P 500 & Nasdaq 100 component stocks trading above 20-day & 50-day moving averages of 31 Oct 2024 (Source: TradingView)

One of the market breadth measurements on the S&P 500 has turned weak where the percentage of its component stocks trading above their respective 20-day and 50-day moving averages have turned southward bound.

The percentage of S&P 500 component stocks trading above their 20-day moving averages has declined sharply from 72% to 32% within two weeks.

A similar observation can also be seen in the percentage of S&P 500 component stocks trading above 50-day moving averages as it dropped from 77% to 47% over the same period (see Fig 1).

The rapid deterioration seen in these market breadth indicators of the S&P 500 to breach below their respective 50% levels has suggested that the medium-term uptrend phase of the S&P 500 has been damaged ahead of next week’s key US presidential election polling day on 5 November.

Bearish breakdown of “Ascending Wedge”

Fig 2: Medium-term & major trends of the US S&P 500 CFD Index as of 1 Nov 2024 (Source: TradingView)

Thursday, 31 October price actions seen on the US S&P 500 CFD Index (a proxy of the S&P 500 E-mini futures) have staged a bearish breakdown below the bearish reversal “Ascending Wedge” support from 5 August 2024 swing low now turns an intermediate pull-back resistance at 5,811.

In addition, the MACD trend indicator traced out a prior bearish divergence condition earlier on 23 October after a similar bearish divergence flashed out on the leading MACD Histogram a week earlier on 14 October.

These observations suggest that the US S&P 500 CFD Index may have formed a medium-term top and is in the process of shaping a potential medium-term (multi-week) corrective decline sequence.

Watch the 5,930 key medium-term pivotal resistance, and a breakdown with a daily close below 5,675 (close to the 50-day moving average) sees the next medium-term supports coming in at 5,390 (also the 200-day moving average) and 5,100.

On the other hand, a clearance with a daily close above 5,930 invalidates the bearish tone to expose the next medium-term resistances at 6,110/130 and 6,390 (also the upper boundary of the major ascending channel from March 2020 low).

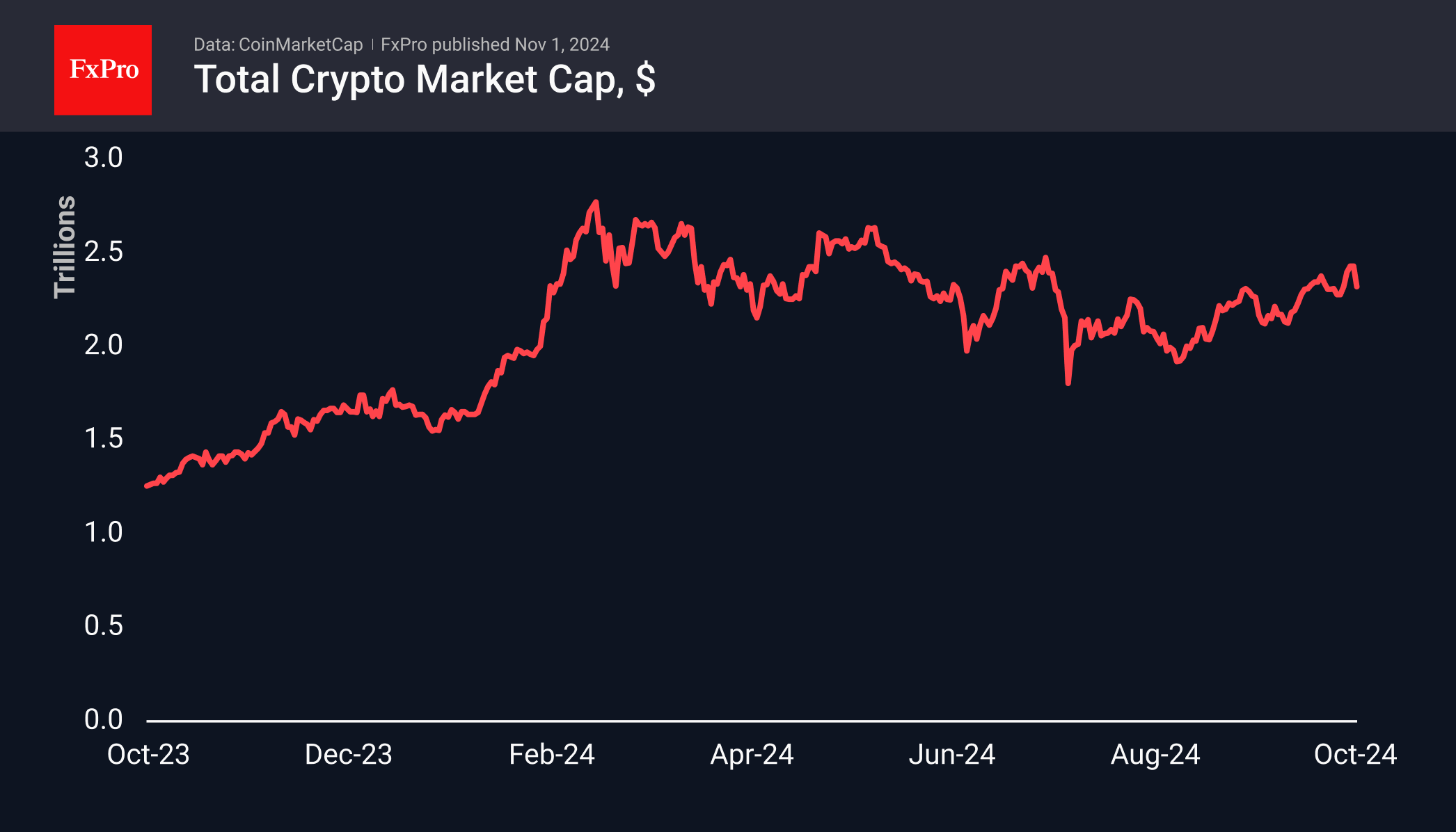

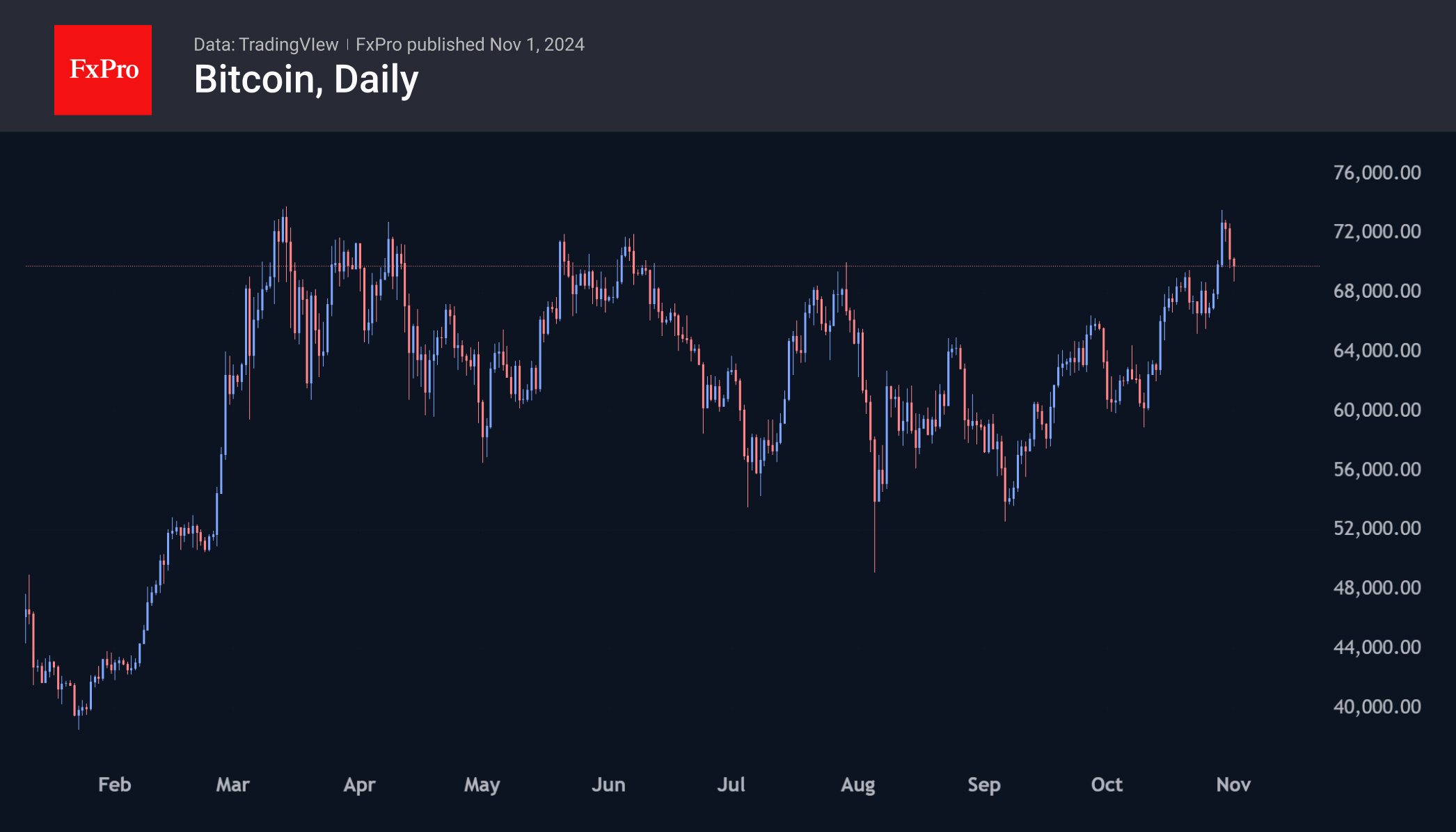

Crypto Takes a Step Back, Ready for Volatility

Market Picture

The crypto market stumbled on the last day of October, losing over 5.5% in 24 hours as investors turned to profit-taking. The drop coincided with the stock market entering a period of high uncertainty ahead of a mix of influential events: the NFP on Friday, the US election results on Wednesday and the Fed meeting on Thursday.

The total crypto cap rolled back to $2.33 trillion, where the market consolidated in the 10 days to 25 October. While painfully sharp, it fits well with the upward trend that has been building since early September.

Bitcoin has fallen back just below the $70K area, temporarily turning support into former resistance. After an impressive and rather unexpected attack on all-time highs, Bitcoin is now in news-waiting mode, ready to move either way from current levels. There will be no shortage of volatility and sharp reversals.

At the end of October, bitcoin was up 9.7% at $70K. In terms of seasonality, November is considered a successful month for BTC. Over the past 13 years, bitcoin has ended the month with a gain 8 times, with an average rise of 22% and an average fall of 17%.

News background

Crypto investment firm Canary Capital has filed an S-1 with the SEC to register a spot ETF based on Solana. Solana’s advanced DeFi ecosystem ensures sustained on-chain activity, as evidenced by the number of daily transactions and active and new addresses, while keeping user fees low, the company said in a statement.

In its Q3 report, MicroStrategy unveiled a plan to raise $42 billion to continue its bitcoin acquisition strategy. Since August 2020, the company has spent $6.9 billion to buy 252,220 BTC.

According to its quarterly report, social network Reddit sold nearly $6.9m of its BTC and Ethereum reserves in the third quarter. The company noted that fluctuations in crypto-asset exchange rates have negatively impacted its financial performance, as has the lack of a clear tax regime for cryptocurrencies.

The growth of the stablecoin market has led to increased demand for short-term Treasury securities, the US Treasury Department said in a report. The department estimates that stablecoin issuers have invested $120 billion in US debt.

31 October marked the 16th anniversary of the Bitcoin White Paper. The technical document described the working principles of the peer-to-peer payment system that went on to revolutionise the world of financial technology. Donald Trump congratulated the crypto community on the occasion.

Bitcoin Price Falls Short of Record High, Drops Below $70k

The BTC/USD chart shows the following:

→ Bitcoin’s all-time high is around $73,750 per coin, set on March 14, 2024, amid peak investor interest after the SEC approved a Bitcoin ETF on January 11.

→ This autumn, Bitcoin’s price is exhibiting positive momentum, partly fueled by the potential for Donald Trump to win the U.S. presidential election (with results expected on November 6). At a July cryptocurrency conference in Nashville, Trump promised support for the industry, raising hopes among crypto investors that his victory could drive Bitcoin prices to $100,000 or higher. Standard Chartered’s analyst has predicted that BTC/USD could reach $125,000 if Trump wins.

→ This week, Bitcoin’s price approached its all-time high but turned downward (as indicated by the arrow) just shy of reaching it, and has since fallen below the psychological level of $70,000 per coin.

What’s next?

Today’s technical analysis of the BTC/USD chart suggests:

→ Bitcoin’s autumn price fluctuations are forming an upward channel (shown in blue), constructed using linear regression. Currently, BTC’s price is positioned in the channel’s lower half.

→ The $69k level, which previously acted as resistance, now serves as support, though it may be breached, in which case the price may move toward the channel’s lower boundary.

The Crypto Fear and Greed Index currently stands at 75, indicating a “Greed” sentiment. Given this high level of emotional volatility, it’s possible that:

→ The recent drop represents a short-term correction after the RSI indicator flagged the market as overbought in the lead-up to the election and the approach of the all-time high.

→ The overall uptrend may persist, potentially pushing Bitcoin toward a new record high.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*At FXOpen UK and FXOpen AU, Cryptocurrency CFDs are only available for trading by those clients categorised as Professional clients under FCA Rules and Professional clients under AFSL 412871 – ABN 61 143 678 719 respectively. They are not available for trading by Retail clients.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

AUDUSD Holds Near August Lows: US Dollar Pressure Remains Strong

The AUD/USD pair fell to 0.6566 on Friday, marking its lowest since early August. The US dollar continued to strengthen last night, bolstered by signs of resilience in the US economy. Additionally, investors hold significant expectations for Donald Trump’s success in the upcoming presidential election next week.

Meanwhile, an unexpected improvement in Chinese manufacturing activity provided noticeable support for the Aussie. Given that China is Australia’s key trade and economic partner, the Australian dollar is highly responsive to developments in China.

Annual inflation in Australia eased to 3.5% in Q3 but remains above the Reserve Bank of Australia’s target range of 2.0-3.0%. Producer prices rose more than expected in the third quarter, while retail sales declined in September. These mixed signals are keeping the Aussie under pressure.

Baseline expectations suggest the Reserve Bank of Australia will leave the interest rate unchanged at 4.35% at its meeting next week.

Technical analysis of AUD/USD

On the H4 chart, the AUD/USD market completed a wave of decline to 0.6536. Today, the market is forming a consolidation range above this level. An upward breakout would signal the development of a growth wave towards 0.6656, viewed as a correction to the previous downtrend. Once this correction is completed, we may see a new decline towards 0.6492. Technically, this scenario is supported by the MACD indicator, with its signal line below zero near the lows and preparing to turn upwards.

On the H1 chart, the AUD/USD market has formed a consolidation range around 0.6561, with a potential extension towards 0.6530. After this, we may see the beginning of an upward wave targeting 0.6655 as the first objective. This growth structure is expected to be part of a broader correction. Technically, this scenario is also confirmed by the Stochastic oscillator, with its signal line below the 20 mark and preparing to rise towards 80.

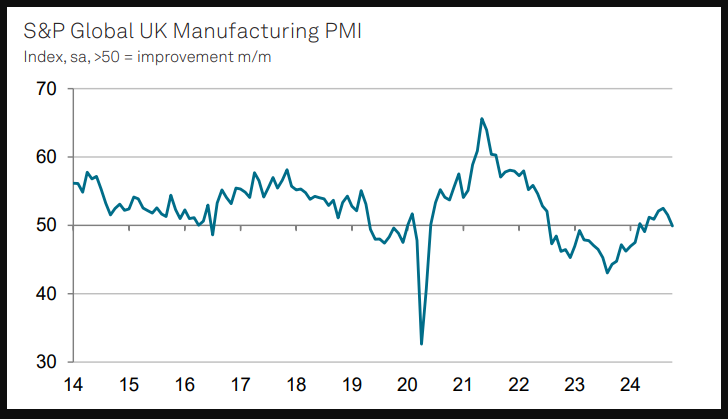

UK PMI manufacturing finalized at 49.9, wait-and-see ahead of budget

UK’s PMI Manufacturing was finalized at 49.9 for October, down from September's 51.5, marking the first contraction since April.

Rob Dobson, Director at S&P Global Market Intelligence, noted that the sector has entered Q4 on an "uncertain footing," as businesses adopt a wait-and-see approach amid policy speculation leading up to the recent Budget. This cautious stance has weighed on investment and spending, with business optimism hovering just above September’s nine-month low.

However, there was positive news on inflation. Input costs dropped to a 10-month low, with inflation easing significantly—one of the largest declines in the survey’s 33-year history. Selling price inflation also moderated, giving BoE additional flexibility to support growth should demand weaken further.

Looking forward, Dobson noted that November’s PMI release will be closely watched for signs of how the Budget impacts business conditions and confidence level.

WTI Crude Oil Recoups Bearish Gap

- WTI crude oil runs to 71.00 critical level near downtrend line

- Momentum oscillators reflect positive bias

WTI crude oil prices recovered the bearish gap that was created in the preceding week and is currently testing the medium-term downtrend line near 71.00.

The price has added more than 6% over the last couple of days with the technical oscillators mirroring the latest upward wave. The MACD oscillator jumped above its trigger line beneath the zero area, while the stochastic is heading north after the bullish crossover within its %K and %D lines above the 20 zone.

An extension to the upside and above the 71.00 key level could meet the area between the 20- and the 50-day simple moving averages (SMAs) at 71.80. Further up, resistance could run towards the 72.95 bar, which is taken from the latest high. Steeper increases could also reach the 76.65 hurdle ahead of the significant flat 200-day SMA at 77.60.

On the other hand, if the commodity weakens, the 67.00 round number could provide immediate support ahead of the 17-month low of 65.70. Even lower, the April 2023 trough at 63.60 could attract a greater attention as any leg lower could worsen market’s bearish outlook.

Regarding the medium-term picture, given that bearish sentiment deteriorated after the downfall toward 65.70 only a move above 78.75 could now help the market return to neutrality.

Euro Retreats from Recent Lows, Pound Plummets After Budget Data Release

In recent trading sessions, European currencies have shown mixed performance. The EUR/USD pair found support just below the 1.0800 level, while GBP/USD plunged below the critical 1.2900 support. Today, investors and market participants are awaiting U.S. labour market data, while next week’s U.S. election adds to the anticipation. This could lead to sharp increases in volatility for both pairs, with current trends potentially either intensifying or shifting dramatically.

EUR/USD

Recent macroeconomic data from the Eurozone has been relatively positive this week. For instance, Germany’s GDP for Q3, released on Wednesday, posted a 0.2% growth, beating the forecasted -0.1%. Similarly, the Eurozone’s GDP and the October Consumer Price Index (CPI) both showed positive trends.

Technical analysis of EUR/USD suggests the possibility of an upward movement, provided the price remains above 1.0800. If the U.S. Nonfarm Payrolls data proves positive, the pair could retest recent lows around the 1.0780-1.0760 range.

Key events for EUR/USD today:

- 15:30 (GMT +3:00) – U.S. ADP Non-Farm Employment Change;

- 15:30 (GMT +3:00) – U.S. Average Earnings data;

- 16:45 (GMT +3:00) – U.S. Manufacturing PMI for October.

GBP/USD

At the start of the current trading week, GBP/USD managed to strengthen to 1.3000. However, following the release of the UK’s Autumn Budget on Wednesday, the price saw a sharp decline, breaking through the crucial support level of 1.2900. Currently, the pair is testing this level as a resistance. A rejection at this point could push the downward trend towards 1.2800-1.2700. Conversely, a hold above 1.2900 could see the pair retest the 1.3000 level.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Swiss CPI down further to 0.6% yoy in Oct

Switzerland’s CPI decreased by -0.1% mom in October, missing expectations of flat growth. Core CPI, which excludes fresh and seasonal products, energy, and fuel, edged up by 0.1% mom. Prices for both domestic and imported products each declined by -0.1% month-over-month.

On an annual basis, headline CPI dropped to 0.6% yoy from 0.8% yoy, falling short of the anticipated 0.8% yoy increase. Core CPI similarly softened, slipping from 1.0% yoy to 0.8% yoy. Domestic product prices grew at a slower pace, declining from 2.0% yoy to 1.8% yoy, while imported product prices saw a deeper contraction, from -2.7% yoy to -3.1% yoy.