Sample Category Title

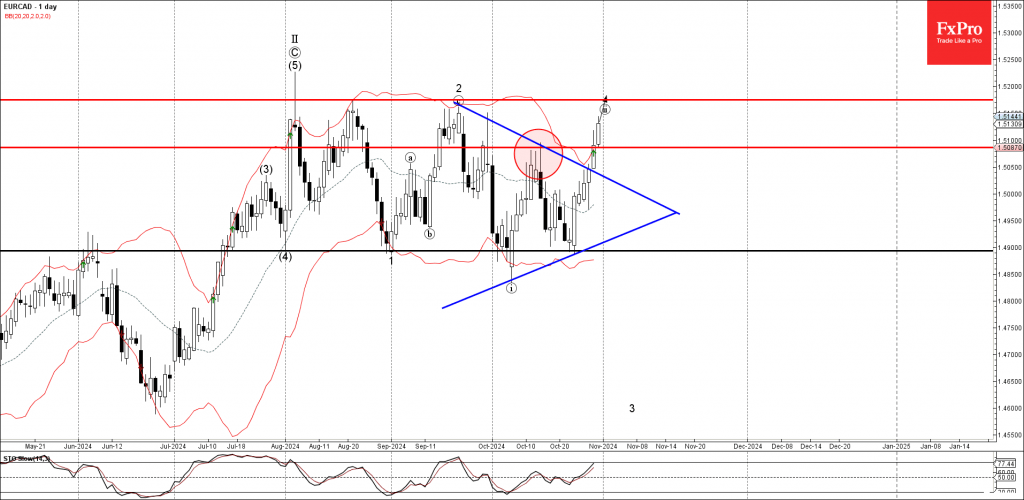

EURCAD Wave Analysis

- EURCAD broke resistance level 1.5085

- Likely to rise to resistance level 1.5175

EURCAD currency pair recently broke the resistance level 1.5085 (which reversed the price in the middle of October).

The breakout of the resistance level 1.5085 was preceded by the breakout of the daily Triangle from September – which accelerated the active wave ii.

Given the continuation of the bearish Canadian dollar sentiment, EURCAD currency pair can be expected to rise to the next resistance level 1.5175 (the former monthly high from September and the target for the completion of the active wave ii).

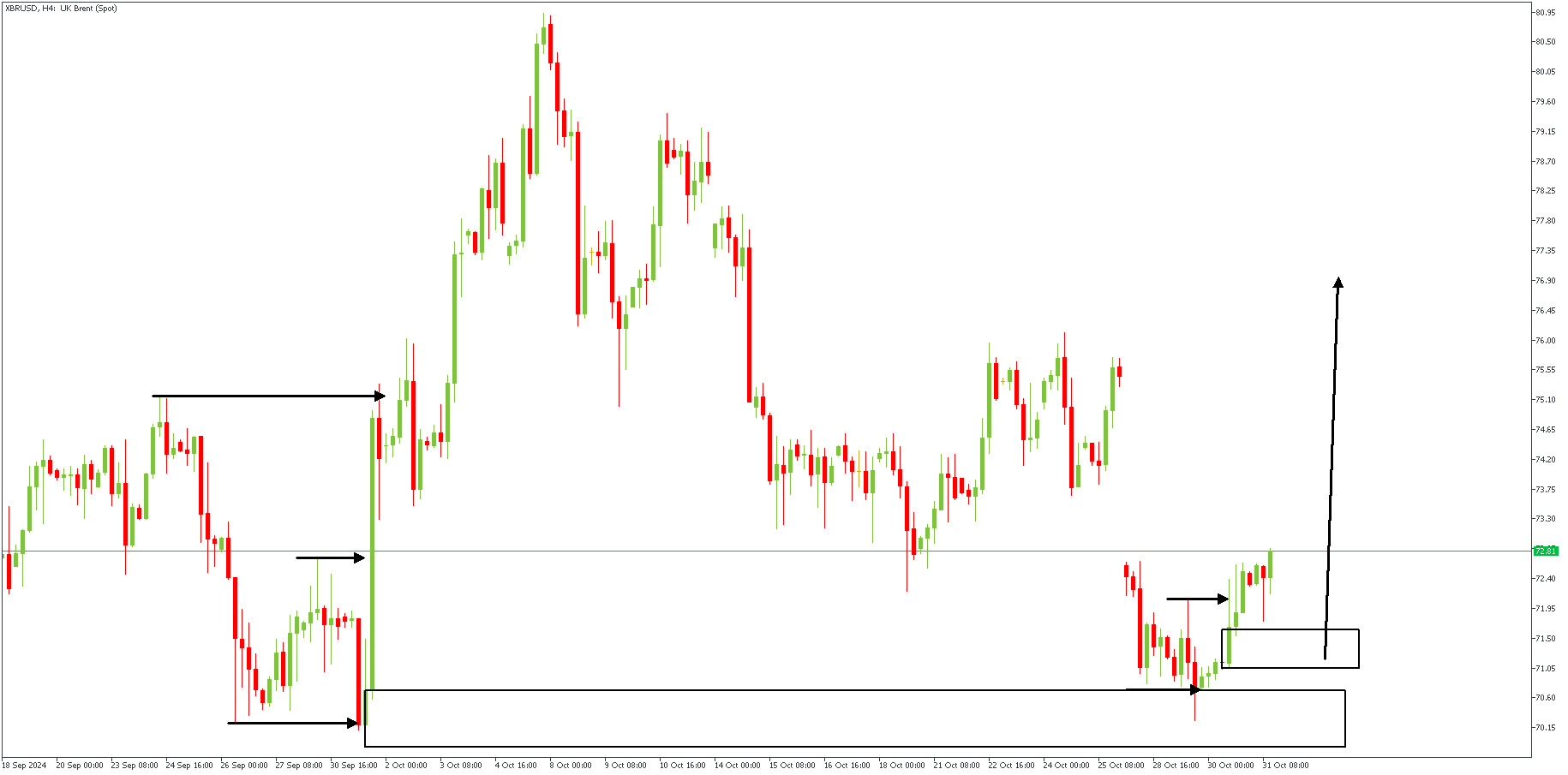

Oil: Bullish Impulse Expected

Yesterday, West Texas Intermediate (WTI) crude oil was trading at $68.17 per barrel, up by 0.37% over the last 24 hours. So far this year, WTI prices have fallen by 7.18%. Similarly, Brent crude oil was priced at $71.87 per barrel, marking a 0.35% increase in the past day, but it's still down 9.09% year-to-date.

WTI oil hit a 52-week low of $64.78 on September 10, 2024, while Brent reached its low of $68.33 on September 11, 2024. This year's highest prices for WTI and Brent were $87.85 and $92.58, respectively, back in April, which is about 22% higher than where prices currently stand. Historically, Brent crude reached an all-time high of $147.50 per barrel in 2008, whereas WTI prices once dropped as low as negative $40 during the COVID-19 pandemic due to storage issues in the U.S.

XBRUSD – H4 Timeframe

The 4-hour timeframe chart of XBRUSD shows prices reacting to the demand zone at the base of the previous low. After the price broke above the previous high at the highlighted arrowed lines, it slipped back down to retest the demand zone in preparation for a bullish impulse. It is expected that the price will reach the previous high as its initial target.

Analyst's Expectations:

- Direction: Bullish

- Target:77.34

- Invalidation:69.53

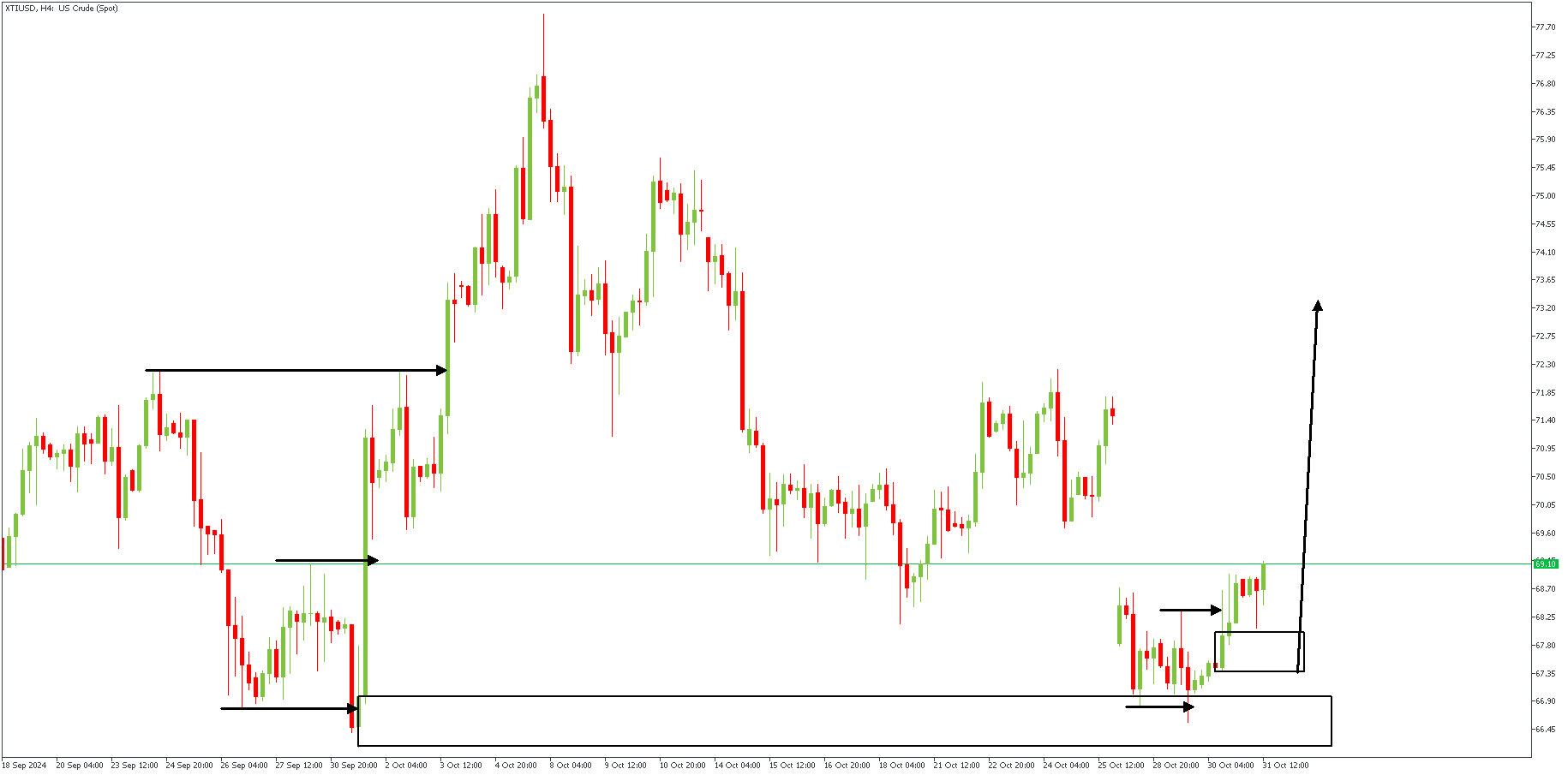

XTIUSD – H4 Timeframe

The price action on West Texas Oil's (WTI) 4-hour timeframe perfectly mirrors all the details from our analysis of Brent. As the price reacted initially from the demand zone, the price is expected to continue on its bullish trajectory until it reaches the previous high.

Analyst's Expectations:

- Direction: Bullish

- Target:73.49

- Invalidation:65.05

Gold & Dollar: Safe-Haven Retreats

Dollar

The dollar index corrected after four consecutive weeks of gains. This is typical when national currencies and bond markets come under pressure ahead of important elections. The U.S. is facing this right now, although the dollar is often seen as a safe haven in times of market turmoil. In this case, gold and cryptocurrencies are temporarily trying out that role. However, we would advise against getting carried away with the idea of a dollar crash or a catastrophic U.S. debt default. This idea seems to have damaged most of today’s investors.

It is more reasonable to see the DXY decline as a pullback after a month of growth. The tactical targets for this correction are 103.8 and 102.8. The former is 76.4% of the initial advance and the 50-week moving average. The latter represents a pullback to 61.8% of the advance, which could fully recharge buyers.

Gold

Gold is in its fourth consecutive week of gains, the last three of which have been in the mode of regularly updating all-time highs. In futures, the price rose above $2800 per troy ounce, while the spot price stalled slightly as it approached this level. The current rally began in October last year with the first signs of a monetary policy shift. In less than thirteen months, the price has risen by 50%.

On a weekly basis, the RSI index has breached the 80 mark. This is only the sixth time in the last fifteen years. Corrections have always followed, with the lowest being a 5% correction in April this year. On other occasions, pullbacks have been between 8% and 20%. But there is an important caveat to this tactic. A signal for a correction begins when the asset returns from overbought territory; before this point, going against the trend is challenging, as price changes can be highly volatile due to waves of short-position margin calls.

Sunset Market Commentary

Markets

The fall-out of Reeves’ “one of the largest fiscal loosenings of any fiscal event in recent decades” on UK bond markets went into a second day. Gilt yields sprint another 10.1 (30-yr) to 19 (2-yr) bps higher with new YtD highs for all maturities >5 years. The front-end is heavily influenced by central bank expectations. Markets trim their Bank of England easing bets at a lightning pace, with currently only expecting an amount of 83 bps over the next 12 months. This compared to (an already meagre) 100 bps yesterday and 114 bps the day before. Just month ago, the counter stood at +/- 150 bps. Despite this lofty front-end support, sterling loses out both against the dollar and the euro. That suggests a lot of risk premia is behind the rise at the long end, which isn’t per se a good thing for GBP(or any other currency). EUR/GBP is advancing towards the 0.84 big figure. Breaking higher ahead of the weekend would turn the technical picture more neutral for the pair. In other core markets, Bunds heavily underperform US Treasuries. Yesterday’s stronger-than-expected Q3 GDP numbers and reaccelerating inflation (headline back at 2%, core stable at 2.7%, services at 3.9%) challenges markets (perhaps too) pessimistic view on the euro area economy. German yields add another 1.2 (30-yr) to 8.9 bps (2-yr). Germany’s 10-yr (+3.5 bps) spread vs swap (+0.1 bps) is <2 bps away from turning positive again for the first time in the history of the euro. With Germany’s 10-yr used as the key benchmark to measure risk premia against, this is more than symbolically important. Treasury yields add between 0.7 and 3.7 bps across the curve. US eco data included a slightly lower-than-expected Employment Cost Index of 0.8% vs 0.9% consensus for Q3. That was offset by an unexpected drop in jobless claims from 228k to 216k – the lowest since May of this year. PCE deflators for September could be derived from yesterday’s Q3 outcome so they came in broadly in line with expectations. The Japanese yen outperforms global peers in currency markets though moves are contained. USD/JPY eases to 153.04 in the wake of the BoJ’s policy meeting this morning. Governor Ueda confirmed hikes will continue if the inflation outlook materializes. EUR/USD stands pat at 1.085, awaiting its next potential mover: tomorrow’s October payrolls report.

News & Views

Polish inflation accelerated from 0.1% M/M in September to 0.3% in October (vs 0.4% consensus). The annual figure ticked higher, from 4.9% Y/Y to 5% Y/Y in which is the highest since December of last year. The increase was driven by food prices (4.7% Y/Y to 4.9% Y/Y) and energy prices (11.5% Y/Y from 11.4% Y/Y; low base effect in October 2023). Core inflation will only be published mid-November but likely remained stuck above 4% Y/Y. Elevated price pressure is the key reason why the National Bank of Poland didn’t restart its cutting cycle yet, pointing to the March 2025 inflation report as potential kick-off point. Markets recently started erring to the side of a quicker start on the back of some disappointing eco numbers. The Polish zloty remains in the defensive, caught by international moves and changes on NBP thinking, with EUR/PLN (4.35) gradually returning to the YTD highs around 4.40.

The Norges bank announced that it will purchase FX on behalf of the government equivalent to NOK 150mn per day in November. That’s down from 400mn/day in October and the lowest level of FX buying since March 2022. The Norges Bank carries out FX transactions related to petroleum revenue spending over the central government budget and saving in the government pension fund. The lower volume is linked to a revision to this year’s fiscal spending in the latest budget plan. There is some speculation that the Norges Bank could morph into a net seller of FX from next year on linked to a shift in the government’s liquidity management policy. A possible announcement is due in December or January and could help the ailing Norwegian currency which is amongst this year’s weakest performing currencies losing over 6% against the euro. EUR/NOK is closing in on the 2023 & 2024 highs around 12.

Canada’s Economy Flatlined in August, With a Pickup Expected in September

Canadian economic growth stalled in August after modest GDP growth in July. This print landed in line of Statistics Canada's advanced guidance and consensus expectations. Early estimates from Statistics Canada point to decent growth in September (0.3% m/m).

August's reading was broad-based, with output expanding in 12 of 20 industries. A 0.1% m/m gain in the services sector offset the drag in goods-producing industries (-0.4% m/m).

On a weighted basis, the manufacturing sector posed the biggest headwind for August activity, falling 1.2% m/m with most subcomponents also seeing declines. Elsewhere on the goods side, mining/quarrying/oil & gas (+0.6% m/m) and construction activity (0.3% m/m) rebounded from their declines in July.

On the services side, August's rail strike led to a 7.7% m/m drop in rail transportation activity, extending losses from July's wildfire-induced slide in rail activity. The public administration sector was up for a fourth consecutive month (0.5% m/m), while finance and insurance (0.5% m/m) and retail trade (0.6% m/m) also helped push the overall services sector into positive territory.

Behind the advanced reading of a pickup in growth in September is an increase in the finance and insurance sector as well as construction and retail trade. Weaker expected activity in the mining/oil & gas sector offset some of the growth.

Key Implications

Today's GDP data confirm economic momentum is cooling after somewhat decent growth in the second quarter. Even with current guidance pointing to a strong bounce back in September, downward data revisions to prior months has third quarter growth tracking around 1.0% quarter-on-quarter (q/q) annualized. This poses downside risk to the Bank of Canada's recently revised Q3 forecasts of 1.5% (down from a hefty 2.8% previously).

The BoC's next rate decision isn't until mid-December and there is still a lot of data to digest between now and then. We don't think this will ring any alarm bells for the Bank but it puts more emphasis on their fears around a weakening economy. That said, we think the cumulative 125 bps of cuts delivered to date will do it's part in reigniting economic activity into the end of they year. Looking ahead, more cuts are on the way, with the focus now shifting to upcoming labour market and inflation data.

U.S. Personal Income and Spending Growth Picks Up in September

Personal income grew 0.3% month-on-month (m/m) in September, up slightly from July's 0.2% gain and bang on market expectations.

Accounting for inflation and taxes, real personal disposable income grew a modest 0.1% for a fourth consecutive month.

Consumer spending was robust in September. Personal consumption expenditures grew by 0.5% m/m, above the market expectations for 0.4% growth. This was also a marked acceleration relative to the 0.3% pace in August.

Stripping out inflation, spending rose 0.4% m/m in real terms – an improvement relative to the 0.2% gain recorded in August. A gain in spending volumes was supported by much higher outlays on goods, which rose by 0.7% m/m, while services increased by 0.2% m/m.

The Fed's preferred inflation metric, the core PCE price deflator, rose 0.3% m/m – ahead of the market expectations for 0.2% increase. Year-over-year, core PCE inflation came in at 2.7%, unchanged for the third consecutive month.

Consumers set aside less for the rainy day. The personal savings rate declined to 4.6% in September (down from 4.8% in August and 4.9% in July).

Key Implications

Today's monthly income and spending data showed that consumers have ended Q3 on a strong note. Indeed, consumer spending has been remarkably resilient in the last two quarters. As we noted in our recent report, there are several reasons consumers may have more momentum than previously anticipated, such as a notable upgrade to personal income in H1-2024 and a larger cushion of savings.

Looking ahead to the fourth quarter, monthly spending data is expected to be distorted by the impacts of Hurricanes Helene and Milton, with clean-up and rebuilding efforts likely to boost spending in the short term. However, as these effects subside, we expect spending to moderate closer to a 2% pace throughout 2025, as the economy remains on track for a soft landing. With inflationary pressures easing and the labor market gradually softening, we expect the Fed to cut the fed funds rate by 25 basis points next week.

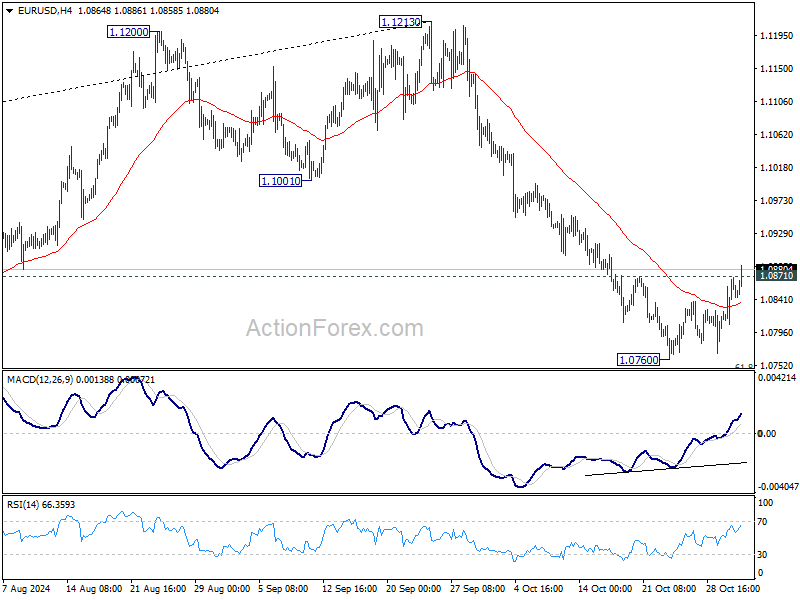

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0814; (P) 1.0842; (R1) 1.0885; More...

EUR/USD's break of 1.0871 resistance confirms short term bottoming at 1.0760, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for 55 D EMA (now at 1.0945). Strong resistance should be seen there to limit upside. On the downside, sustained break of 61.8% retracement of 1.0447 to 1.1213 at 1.0740 will extend the fall from 1.1213 to 1.0601 support next.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

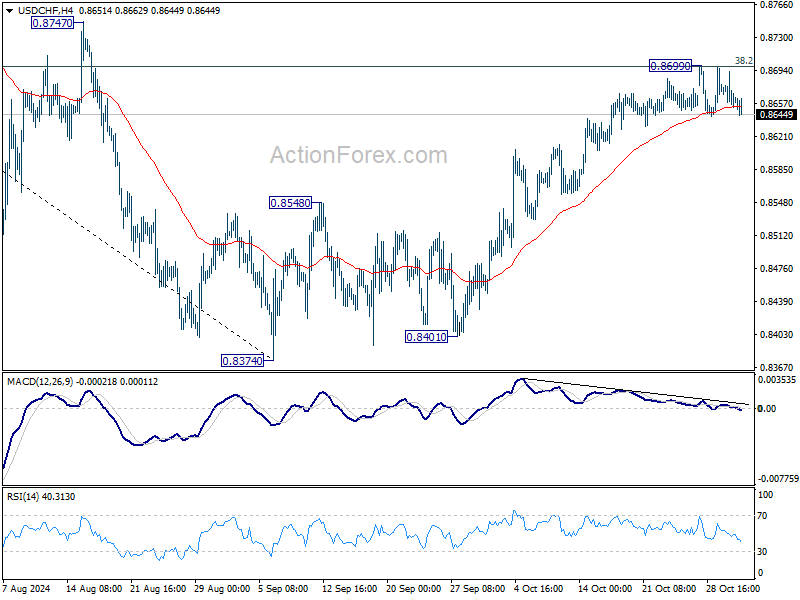

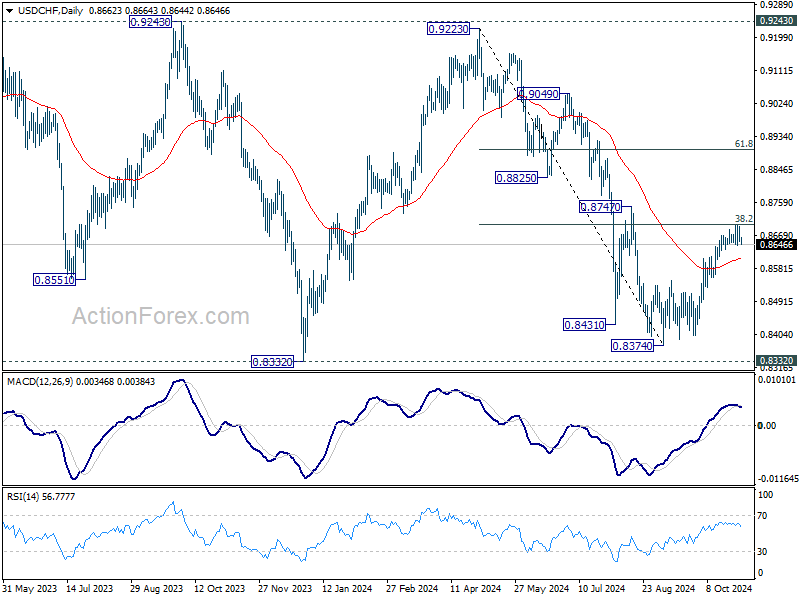

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8646; (P) 0.8672; (R1) 0.8700; More…

USD/CHF is staying in consolidation below 0.8699 temporary top and intraday bias remains neutral. Further rally remains in favor as long as 55 D EMA (now at 0.8609) holds. On the upside, decisive break of 38.2% retracement of 0.9223 to 0.8374 at 0.8698 will argue that fall from 0.9223 has completed after defending 0.8332 low. Further rally should then be seen to 61.8% retracement at 0.8899 next.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

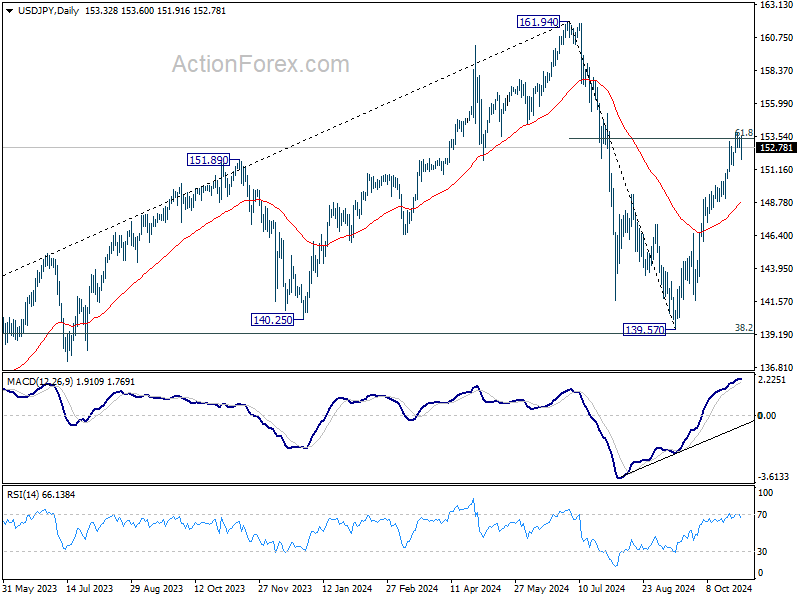

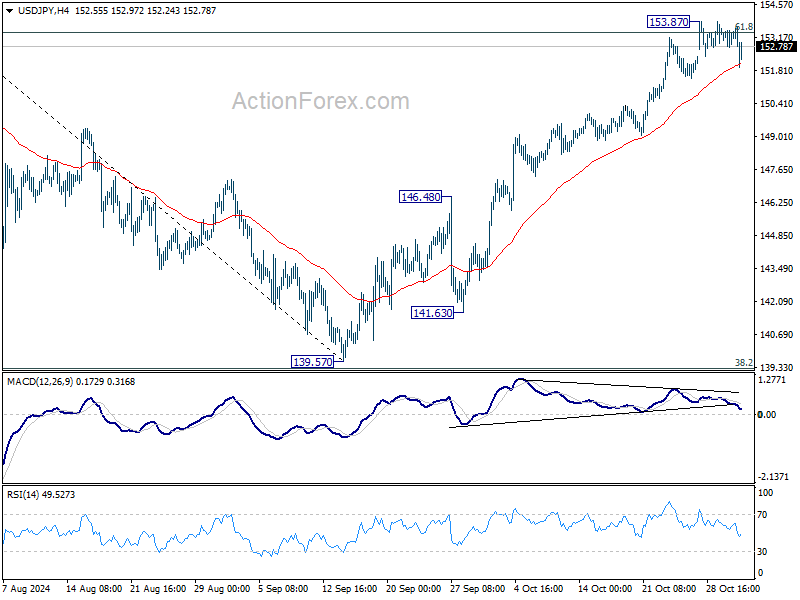

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.80; (P) 153.33; (R1) 153.92; More...

USD/JPY is extending consolidation below 153.87 temporary low and intraday bias stays neutral. Deeper retreat cannot be ruled out but further rally is expected as long as 55 D EMA (now at 148.84) holds. Sustained trading above 61.8% retracement of 161.94 to 139.57 at 153.39 will pave the way to retest 161.94 high.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.