Sample Category Title

Count Down to the US Election

Last week was packed with earnings and data. Five of the Magnificent 7 stocks announced magnificent earnings. Some, like Google and Amazon, kept their investors on their sides, whereas others, like Microsoft and Meta failed to impress as their investors couldn’t get over the weaker forecast and further AI spending that they announced. Big Oil came up with lower profit but share buybacks and higher dividends at some of them helped weathering the bad news Then, the US GDP growth came in slightly lower than expected by analysts, at 2.8% for the Q3, but the consumer spending remained robust. And finally, on Friday, the US announced the official jobs data. The US economy ended up adding a meagre 12K jobs last month, the manufacturing and private nonfarm payrolls printed negative numbers. But the bright spot was that unemployment remained steady at 4.1% - suggesting that the NFP number probably took a one-off hit, and the wages continued to grow by 4% on a yearly basis – high compared to where the Federal Reserve (Fed) would like to see it, but well aligned with the market expectations. The market is now convinced that the Fed will announce another 25bp cut when it meets this week. That announcement is due Thursday, as before that we have the US election – on Tuesday.

Anyway, Friday’s NFP figure didn’t necessarily bring a relevant information on the table. The S&P500, Nasdaq and Dow Jones were better bid on Friday, but all three closed the week on a negative note. The US 2-year yield consolidated around 4.20% and the 10-year around 4.30% after the release. This morning, both are pushing higher, especially the 10-year yield – which spiked to 4.38% in Asia, as investors are closing their US treasury positions before the US election.

US election

The clock is ticking, and soon the suspense will break over who will be the next US president. Even though the prediction markets have been in favour of a Trump victory, the CNN poll this morning prints a 48% chance for a Harris win, versus 47% assessed to a Trump victory. The worst possible outcome for the market would be a too close race and a contested outcome.

In the short run, a Harris victory could bring relief to treasury and international markets, while a Trump victory could resonate louder – and not necessarily in a good way – for the euro and the European markets, due to the tariff threat. The Stoxx 600 index rebounded on Friday, but the index could bear the brunt of a potential Trump victory later this week.

In China, the Chinese equities start the week on a bullish note as the National People’s Congress began its five-day meeting, where policymakers are expected to provide more details on debt and fiscal initiatives to revive growth. There are media reports suggesting that China may announce a stimulus package exceeding 10 trillion yuan to boost economy. I can’t tell what amount of stimulus China will announce, if they put any number on it at all. But a Trump presidency could increase the size of the package and provide a safety net to Chinese investors in case of a Trump win.

USD offered ahead of US election

The US dollar kicks off the week on a bearish note. The USD index slid below the 200-DMA in Asia, the EURUSD is testing the 1.09 level at the time of writing, and Cable, which has been pressured by last week’s budget has jumped to flirt with the 1.30 psychological resistance. One of the safest harbours is gold, bid this morning near an ATH. The Swiss franc and the Swiss equity index are also seen as interesting defensive names in preparation of a contested US election outcome and heightened short-term volatility. The USDCHF has been testing an important Fibonacci resistance – the major 38.2% retracement on May to September selloff and which should determine whether the pair should remain in the bearish trend or step into a medium term bullish consolidation zone. Last week’s softer-than-expected Swiss inflation and sales data came to reinforce the dovish Swiss National Bank (SNB) expectations, weakened the franc bears’ hands, but the crucial Fibonacci resistance hasn’t been pulled out, and the USDCHF bulls may have to wait until the US election dust settles to continue betting in favour of a weaker franc. For the equities, the Swiss market is heavy in healthcare, pharmaceuticals, consumer staples and financials. Therefore, Swiss equities should weather increased market volatility.

Elsewhere, oil kicked off the week better bid on weekend news that OPEC could delay the planned December increase to oil production by a month – or more – on the back of a persistent selloff in oil prices due to the unfavourable combination of weaker demand and strong output prospects. The Middle East rumours also hint at a possible revival of tensions between Iran and Israel – a factor that could help bring tactical long positions back to the market this week. But price rallies are considered as interesting top selling opportunities as long as the gap between demand and supply widens.

US NFP Surprise to the Downside as Election Looms

In focus this week

Today, in the euro area, we receive the Sentix investor confidence indicator, providing the first assessment of sentiment in November. Focus is also on the final manufacturing PMI data for October.

On Tuesday, the US election takes place and is the major highlight of the week. Donald Trump is the small favourite to win the presidential election according to prediction markets, Republicans are expected to win majority in the Senate elections and House elections remain highly uncertain.

On Wednesday morning, when we - hopefully - know the results of the US election, we will be hosting two conference calls where we present our instant view on the results and implications for markets and the economy: Conference call on the implications of the US election for Global and Scandi markets at 8:40 - 9:10 CET and US elections morning call - Macro need-to-knows at 9:15 - 9:30 CET.

Economic and market news

What happened overnight

In oil markets, oil prices gained more than 1 USD following the announcement made by OPEC+ to delay December output increases until January next year. Recently, the price of oil has been pressured by decreasing demand in China, rising external supply and the outlook of the conflict in the Middle East improving.

What happened over the weekend

In the US, nonfarm payrolls growth practically halted according to October Jobs Report released Friday morning. NFP grew by only 12k (cons: 113k, prior: 254k). US government bond yields and EUR/USD shifted higher, but rather modestly compared to the seemingly large negative surprise. Most other labour market indicators for October have still painted a rather positive picture, so perhaps it is a good idea to not give this single (potentially distorted) reading too much weight.

On the wage side, average hourly earnings increased by a solid 0.4% m/m SA, which means that wage sum growth continued despite the weak employment reading. The household measure of employment showed an outright decline in employment (-368k) but as the labour force also shrunk by 220k, unemployment rate remained steady at 4.1%.

Finally, the ISM manufacturing index painted a mixed picture, with weaker business activity of 46.5 (cons: 47.6%, prior: 47.2%), but stronger new orders, employment and prices paid.

In Sweden, PMI for the manufacturing sector surprised to the upside with 53.1 (prior: 51.3). The surprise contradicts the weak NIER survey of last week and is off the table as an argument for the Riksbank to make a 50bp cut on Thursday.

In Norway, the NSA unemployment rate for October dropped to 1.9% (cons: 2.1%, prior: 2.0%) beating market expectations and tightening an already tight labour market. Additionally, the number of new vacancies dropped following relatively weak growth for more than a year.

In Switzerland, inflation for October surprised sharply to the downside with headline at 0.6% y/y (cons: 0.8%, prior: 0.8%) and core at 0.8% y/y (cons: 1.0%, prior: 1.0%). Prior to the release markets were pricing a 37bp cut for the meeting on 12 December. On release, EUR/CHF jumped, driven by energy prices, hotels and the volatile component of international package holidays. While our base case is a 25bp cut in December and March, this increases the likelihood of a 50bp cut in December quite significantly.

Equities. Global equities were higher on Friday, yet still lower over the past week. As mentioned several times last week, numerous factors are currently at play, making it challenging to distinguish the true drivers from mere noise. Nonetheless, last week and particularly Friday presented some very interesting results. Bond yields dropped sharply right after the low Non-Farm Payroll (NFP) print on Friday, only to grind higher throughout the session and closed the day higher. In the short term, the risk of a red sweep in the upcoming election seems more important for bond market than macroeconomic factors.

Last week's best-performing style was small-cap, despite higher yields. A red sweep would likely mean reduced regulation, or more precisely, diminished regulatory fears, which typically benefits small caps. Additionally, this season's earnings from small caps have not been impressive. Again, in the short term, it appears that elections have a more significant impact on small caps than yields.

Banks performed very well last, which makes sense given the strong earnings and higher yields. However, for us, banks are one of the biggest beneficiaries of a red sweep. More fiscal spending, increased lending activity, higher yields, and less regulation are all advantages. Policies on immigration and trade will have very little effect on banks. Therefore, based on both fundamentals and politics, it is logical to see banks performing exceptionally well recently.

US main equity indices on Friday were as follows: Dow +0.7%, S&P 500 +0.4%, Nasdaq +0.8%, Russell 2000 +0.6%. Asian markets were mostly higher this morning, with Japan closed.

FI: A sharp rally in global yields was recorded following the weaker-than-anticipated NFP on Friday with just 12k new jobs in October. However, as markets digested the timing of the poll coinciding with hurricanes as well as strong prices paid figure of the US ISM, markets quickly repriced higher in yields. 10y UST ended 10bp higher at 4.38%, in a bearish steepening move. German yields were broadly unchanged on the day. German ASW spread continued its tightening and now stands at just 5.8bp.

FX: EUR/USD rallied above 1.0900 after the NFP release. The distorted data did not have a lasting impact though and the cross closed Friday's session at day lows. Monday morning, one day before the US election, the cross is back at 1.09. Similarly, USD/JPY dropped briefly after the NFP, closed the week at day highs and is back below 152 this morning. Weak Swiss inflation numbers weighed on the CHF. The Scandies remain under pressure. EUR/NOK challenges two-months highs at 12.00 and EUR/SEK three-month highs at 11.65. Both crosses are sensitive to the US election outcome and the latter to the Riksbank decision on Thursday as well.

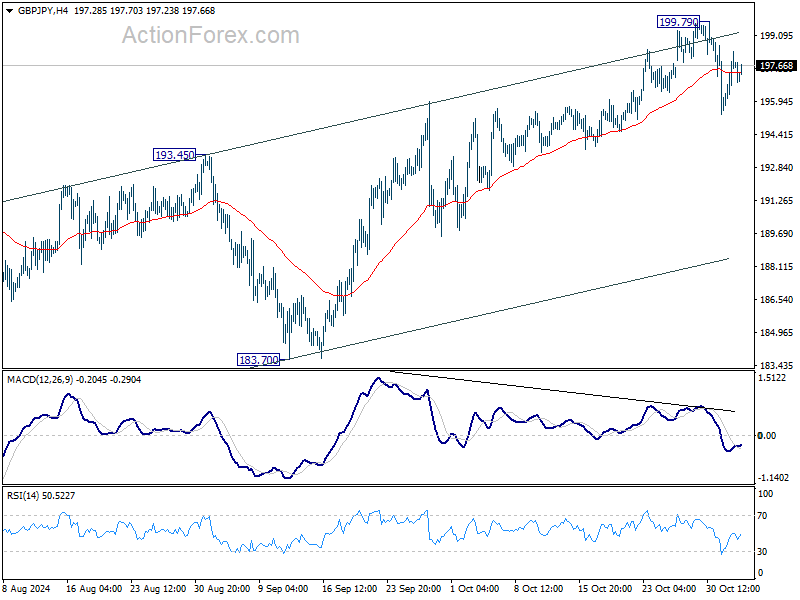

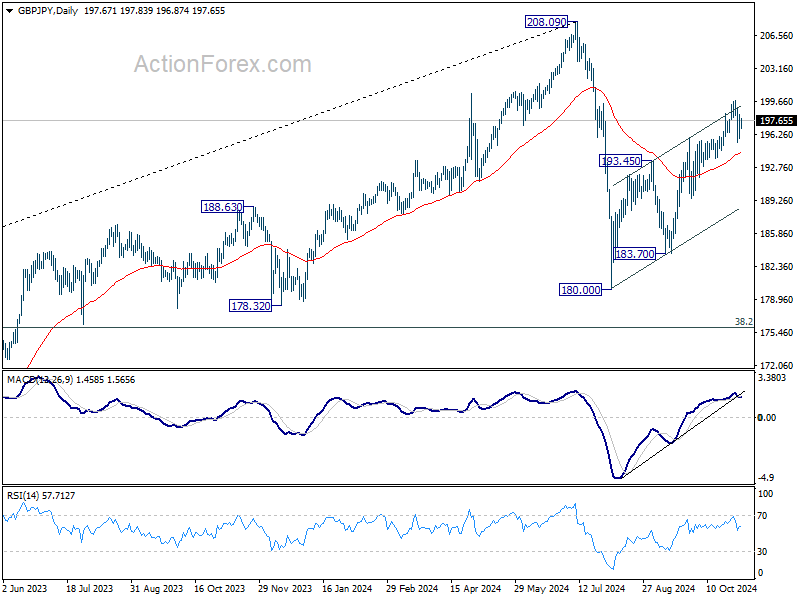

GBP/JPY Daily Outlook

Daily Pivots: (S1) 196.10; (P) 197.24; (R1) 198.69; More...

Intraday bias in GBP/JPY remains neutral for consolidations below 199.79. Further rally is expected as long as 55 D EMA (now at 194.26) holds. Above 199.79 will resume the rebound from 180.00 to retest 208.09 high. However, sustained break of 55 D EMA will argue that the corrective rise has completed already, and turn near term outlook bearish for 180.00/183.70 support zone.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

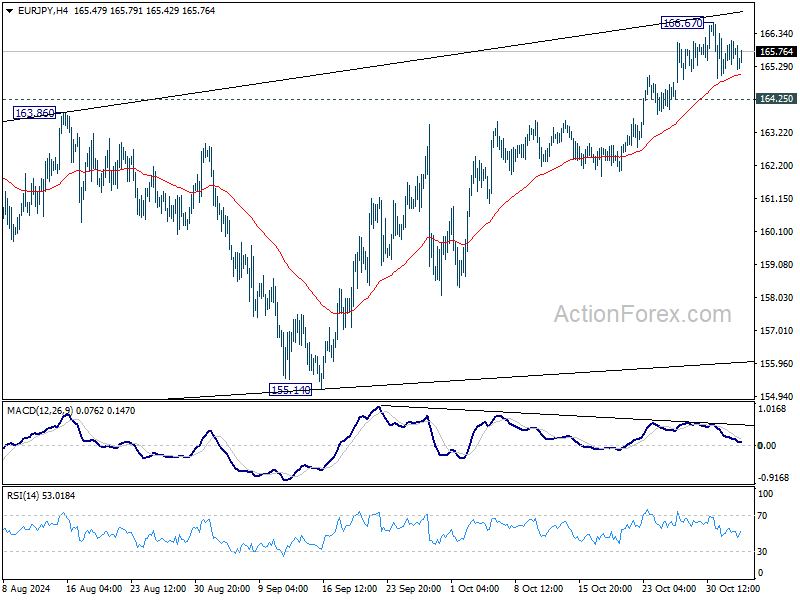

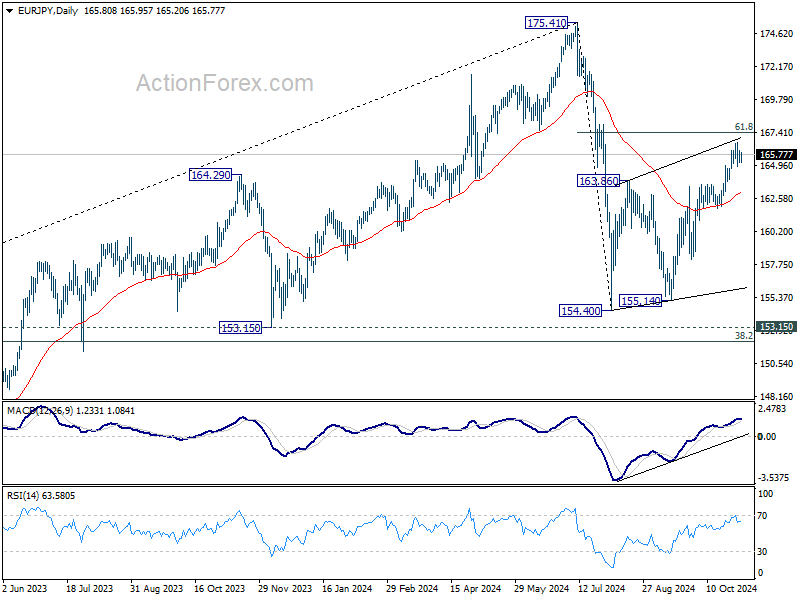

EUR/JPY Daily Outlook

Daily Pivots: (S1) 165.25; (P) 165.69; (R1) 166.14; More....

Intraday bias in EUR/JPY remains neutral for consolidation below 166.67. Further rally is expected as long as 164.25 minor support holds. Sustained break of 61.8% retracement of 175.41 to 154.40 at 167.38 will pave the way to retest 175.41 high. However, considering bearish divergence condition in 4H MACD, firm break of 164.25 will indicate short term topping, and turn bias to the downside for 55 D EMA (now at 163.06).

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

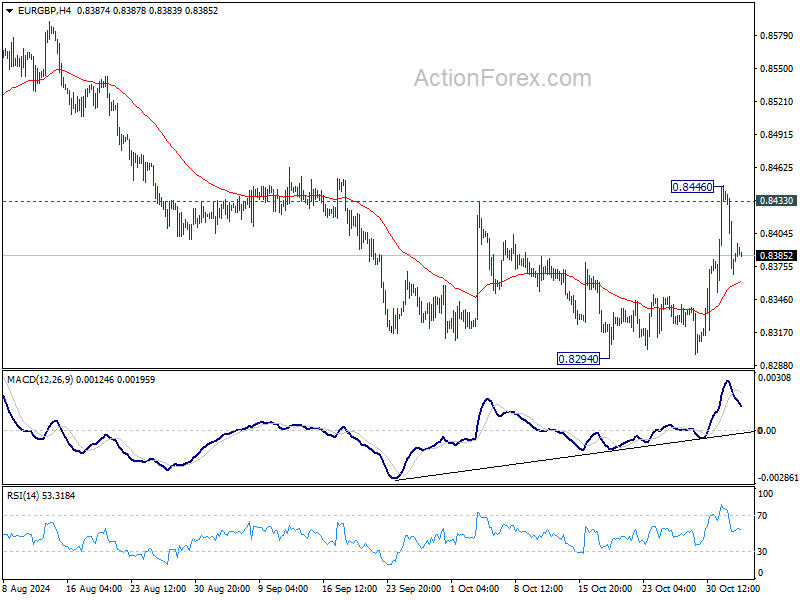

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8355; (P) 0.8399; (R1) 0.8429; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the downside, break of 0.8294 low will resume larger down trend to 0.8201 key support next. On the upside, break of 0.8446 will resume the rebound fro 0.8294 short term bottom towards 0.8624 resistance instead.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

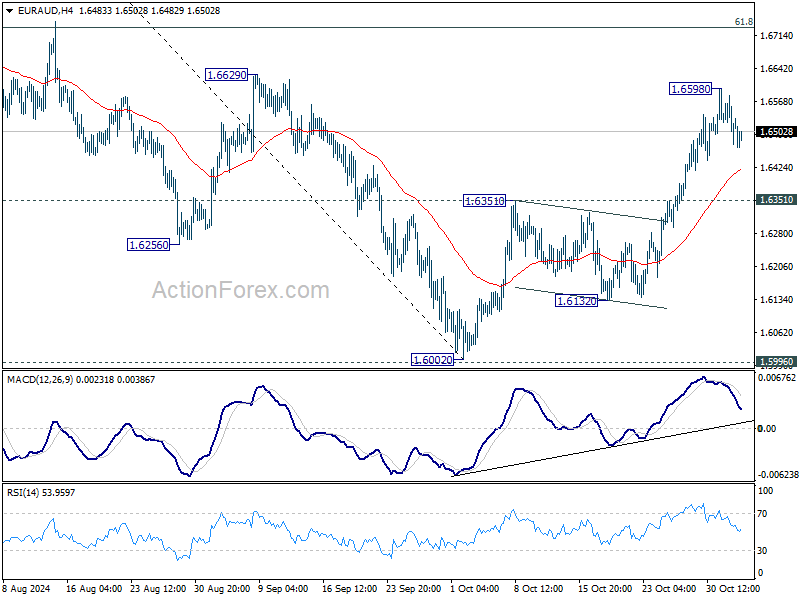

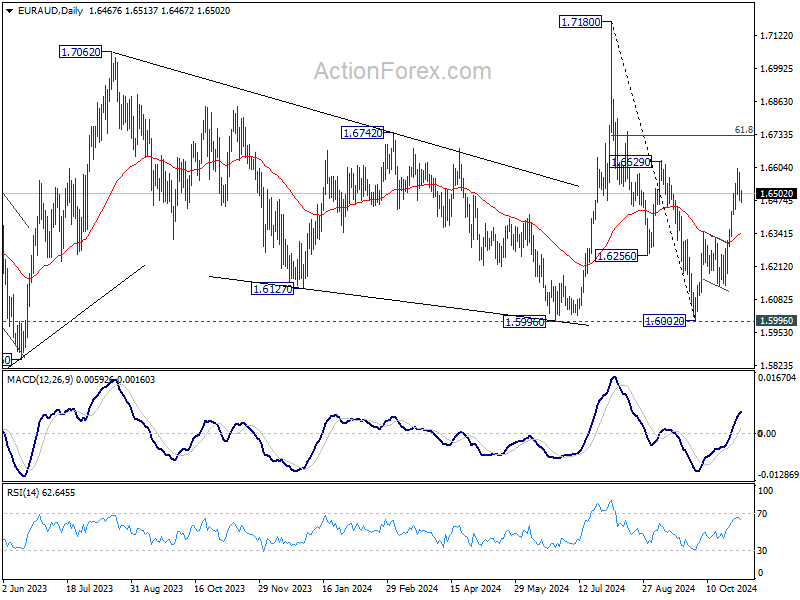

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6467; (P) 1.6526; (R1) 1.6576; More...

Intraday bias in EUR/AUD remains neutral for the moment/ Further rally is expected as long as 1.6351 resistance turned support holds. On the upside, above 1.6598 will resume the rise from 1.6002 short term bottom to 61.8% retracement of 1.7180 to 1.6002 at 1.6730 next. Sustained trading above there will pave the way to retest 1.7180 high.

In the bigger picture, as long as 1.5996 cluster support holds (38.2% retracement of 1.4281 to 1.7062 (2023 high) at 1.6000), up trend from 1.4281 (2022 low) is still expected to resume at a later stage. However, decisive break of 1.5996 will argue that the medium term trend has reversed and turn outlook bearish.

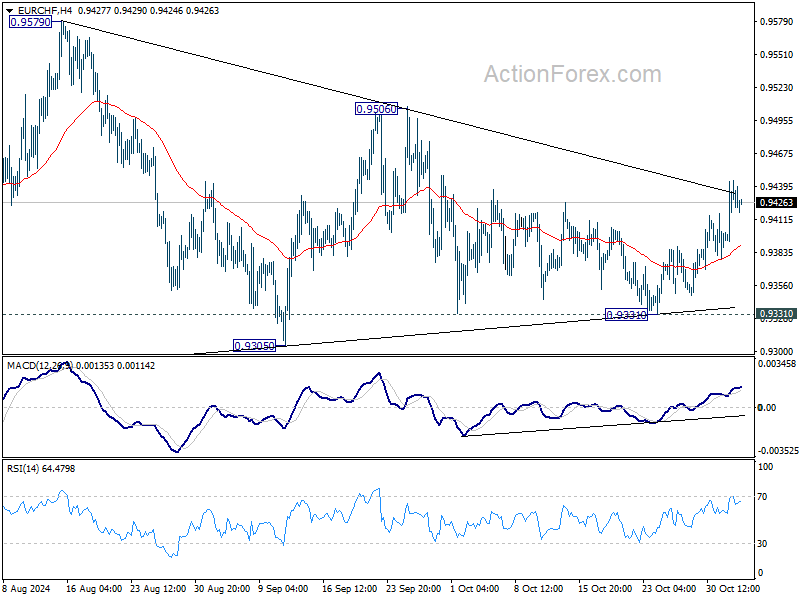

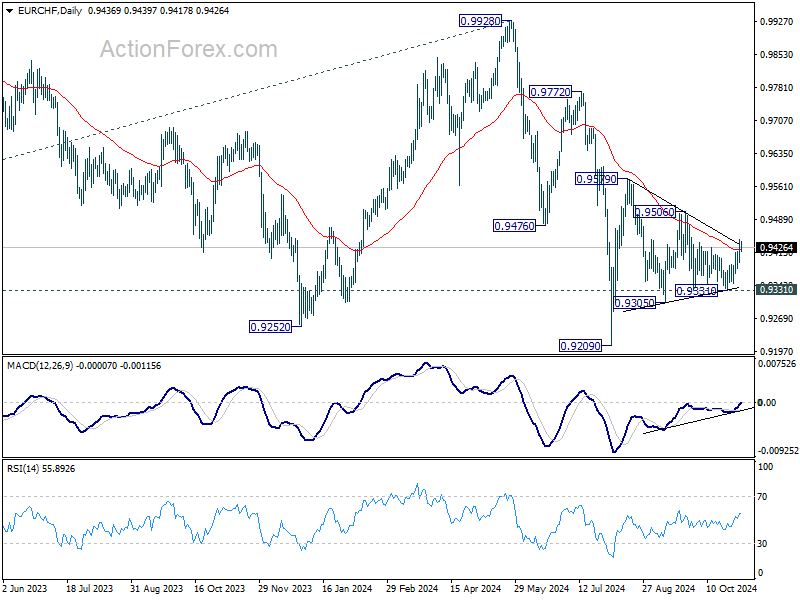

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9391; (P) 0.9419; (R1) 0.9450; More....

Intraday bias in EUR/CHF remains neutral and outlook is unchanged. On the downside, break of 0.9331 will resume the fall from 0.9579 towards 0.9209 low. On the upside, break of 0.9506 will turn intraday bias to the upside for 0.9579 resistance and above.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9421) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming at 0.9209 and bring stronger rebound back towards 0.9928 key resistance.

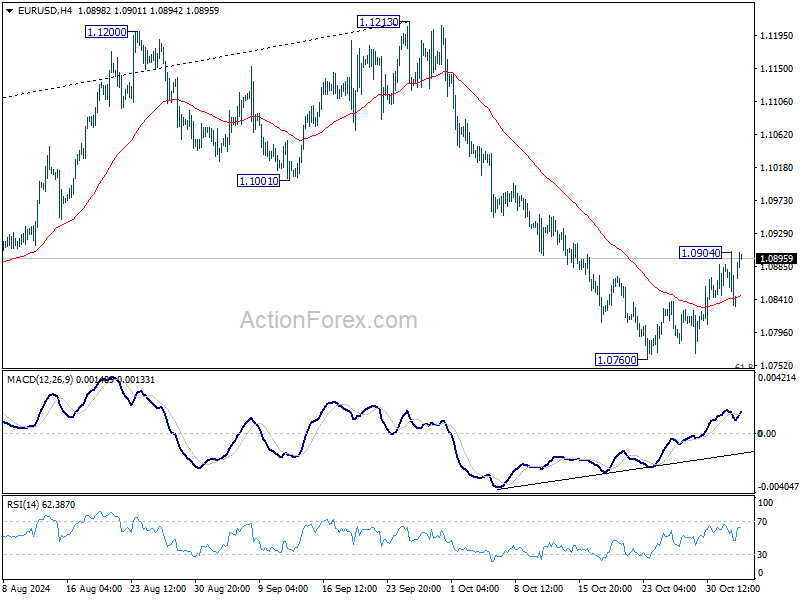

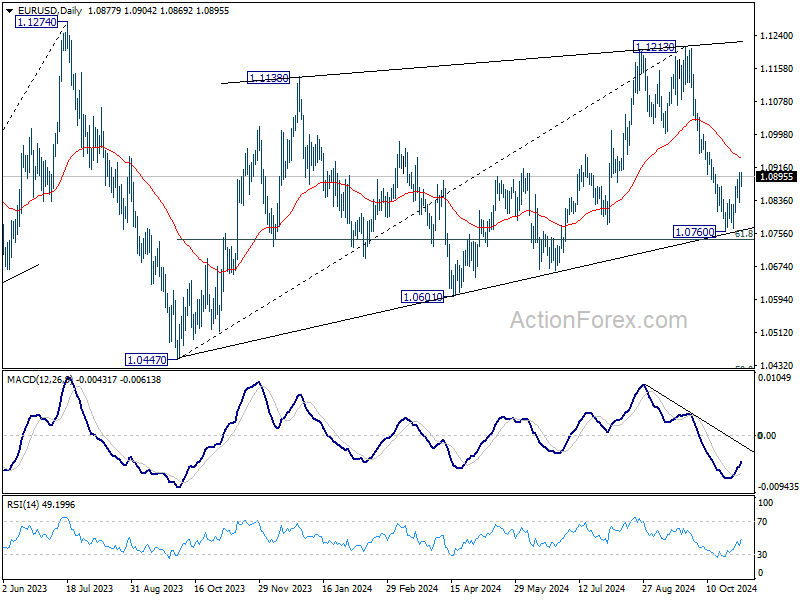

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0809; (P) 1.0857; (R1) 1.0883; More...

EUR/USD stays below 1.0904 temporary top despite today's rebound, intraday bias remains neutral first. On the upside, break of 1.0904 will resume the rebound from 1.0760 short term bottom to 55 D EMA (now at 1.0941). On the downside, sustained break of 61.8% retracement of 1.0447 to 1.1213 at 1.0740 will extend the fall from 1.1213 to 1.0601 support next.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

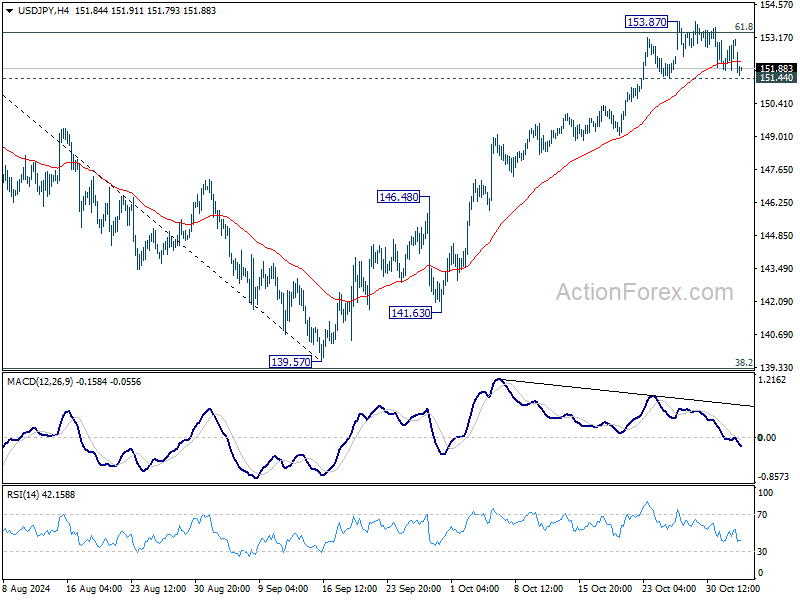

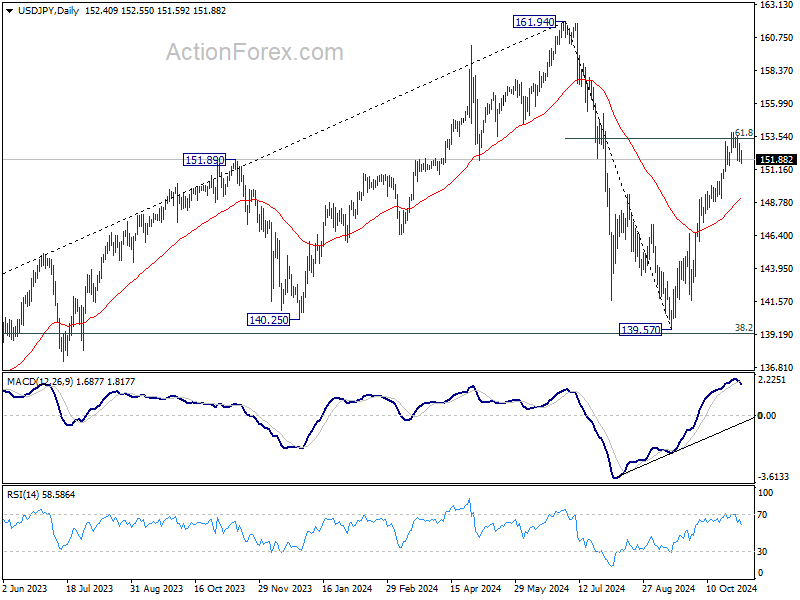

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.12; (P) 152.61; (R1) 153.42; More...

Intraday bias in USD/JPY remains neutral at this point, and more consolidations would be see. Another rise is expected with 151.44 support intact. Sustained trading above of 61.8% retracement of 161.94 to 139.57 at 153.39 will pave the way to retest 161.94 high. However, considering bearish divergence condition in 4H MACD, firm break of 151.44 will indicate short term topping, and turn bias back to the downside for 55 D EMA (now at 149.07).

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

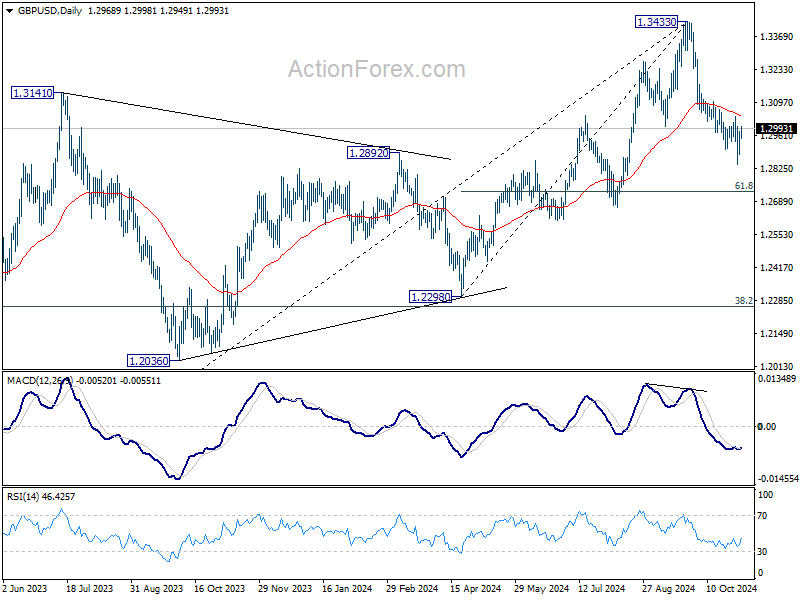

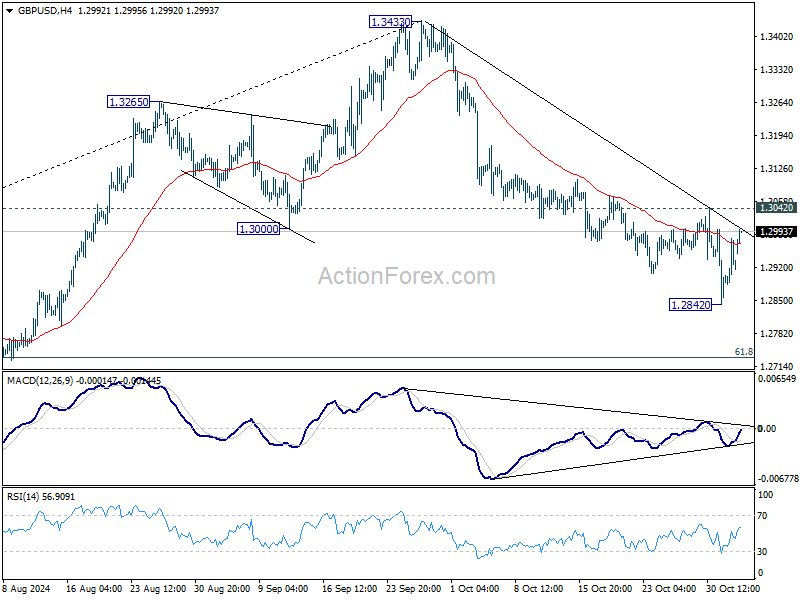

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2875; (P) 1.2927; (R1) 1.2970; More...

Intraday bias in GBP/USD remains neutral for the moment and more consolidations could be seen below 1.3042 resistance. Further decline is expected as long as 1.3042 resistance holds. Below 1.2842 will resume the fall from 1.3433 to 61.8% retracement of 1.2298 to 1.3433 at 1.2732. However, considering bullish convergence condition in 4H MACD, firm break of 1.3042 will indicate short term bottoming, and turn bias back to the upside.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.