Sample Category Title

November Flashlight for the FOMC Blackout Period

Summary

- The FOMC started its nascent easing cycle with a bang, opting to reduce the fed funds target range by 50 bps to 4.75%-5.00% at its last meeting on September 18. But further policy easing seems set to proceed at a slower pace. We look for the FOMC to reduce the fed funds rate by 25 bps at its upcoming meeting on November 7.

- Since the Committee last met, U.S. economic activity has generally surprised to the upside and suggested ongoing resilience. Concerns about rapid softening in the labor market were allayed by the September jobs report showing a much stronger pace of hiring the past three months and the unemployment rate falling to a four-month low. Solid retail sales and upward revisions to income suggest consumer spending remains on a firm footing. Consumer price inflation also came in a bit stronger than expected in September.

- The FOMC's September dot plot, the recent string of stronger-than-expected data and policymakers' comments give no reason to expect another 50 bps cut at the Committee's upcoming meeting. We expect the FOMC will continue to reduce its policy rate with a smaller 25 bps cut as the real fed funds rate remains elevated relative to the past expansion and Committee members' estimates of "neutral." Therefore, there seems to remain scope to "recalibrate" policy further to avoid the labor market cooling beyond the point of comfort without rekindling inflation.

- Yet given the recent run of data along with some officials' prior reluctance to cut much further, if at all, this year, we would not be surprised to see another dissent at the November 7 meeting, and view the risks to our expectation for a 25 bps cut skewed toward the FOMC leaving rates unchanged rather than opting for another 50 bps cut.

- Recent signs of funding pressures lead us to expect the FOMC will discuss the current pace of quantitative tightening (QT) at its November meeting. The secured overnight financing rate (SOFR) traded above the top end of the fed funds target range at the end of Q3, suggesting bank liquidity has become less ample. While we do not anticipate any changes to QT at this meeting, the recent stress will likely lead to an in-depth discussion about the timeline for the cessation of balance sheet runoff. We currently expect QT to cease at the end of Q1-2025.

Easing to Proceed, But at a Slower Pace

The Federal Open Market Committee (FOMC) maintained its target range for the federal funds rate at 5.25%-5.50% for more than a year (July 2023 to September 2024). Although the Committee judged that further rate hikes after last July were not warranted, it opted not to ease policy during that period due to the "elevated" nature of consumer price inflation. However, the Committee decided to slash rates by 50 bps on September 18 because the risks to the Fed's dual mandate of "price stability" and "full employment" were "roughly in balance."

Specifically, the year-over-year rate of "core" PCE inflation, which most Fed officials consider to be the best measure of underlying consumer price inflation, had receded significantly from its peak of 5.6% in February 2022 to 2.6% in July, the last data point the FOMC had when it met on September 18. Moreover, the 3-month annualized rate of change of core prices had receded to only 1.9% in July (Figure 1). On the other side of its dual mandate, the labor market was showing signs of softening. Nonfarm payrolls rose less than expected in August and the prior two months' gains were revised down by a combined 86K jobs, reducing the three-month average pace of hiring to 116K from 177K at the time of the July FOMC meeting. The unemployment rate, which had been 3.4% in April 2023, had trended up to 4.2% in August (Figure 2). As Chair Jerome Powell said in his Jackson Hole speech in late August, the FOMC did not "seek or welcome further cooling in labor market conditions."

Fast forward six weeks. Incoming data show that the U.S. economy remains remarkably resilient. Nonfarm payrolls rose by an eye-popping 254K in September, employment gains during the previous two months were revised up by a combined 72K and the jobless rate edged down to 4.1%. The core Consumer Price Index, which is a different measure of consumer price inflation than core PCE inflation but which is highly correlated with it, rose a bit more than expected in September relative to the prior month with a 0.3% gain. Retail spending in September was significantly stronger than most analysts had expected. Upward revisions to income growth over the past year also suggest the U.S. consumer is on sturdier footing, having saved a higher share of income over the past year than previously reported. We estimate that real GDP grew at an annualized rate in excess of 3.0% in Q3-2024 on a sequential basis. In short, the U.S. economy is hardly falling apart at present.

The string of data suggesting that the economy continues to expand at a robust pace and that the labor market is not unraveling have raised questions about whether the FOMC needs to cut again at its upcoming meeting. At its prior meeting in September, nearly half of FOMC participants were already of the view that it would be appropriate to reduce the Fed funds rate by only 25 bps, if at all, through the remainder of this year (Figure 3). While some FOMC members may not be on board with a further rate reduction at the November 7 meeting in light of the recent strength in activity, we believe the bulk of the Committee will want to ease policy further. That said, there seems to be little appetite among FOMC members to follow the 50 bps rate cut on September 18 with a similar-sized reduction in the target range for the federal funds rate at the upcoming policy meeting. Therefore, we look for a 25 bps rate cut on November 7.

We would not be surprised to see another dissent, however, in the form of a voter or two preferring a slower approach to policy easing. Therefore, the risks to our expectation for a 25 bps cut appear titled toward the Committee deciding to keep the target range unchanged, rather than opting for another super-sized move. Financial markets look to be in agreement. As of this writing, pricing in the bond market implies a 95% probability of a 25 bps cut rate cut on November 7.

Why cut rates at all at the upcoming meeting? With the fed funds rate currently trading at 4.83% and with core PCE inflation running at a year-over-year rate of 2.7%, the "real" fed funds rate is roughly 2.1% at present. In contrast, the real fed funds rate never exceeded 1% during the economic expansion of 2010-2019 (Figure 4). In other words, the stance of monetary policy remains restrictive, despite the 50 bps rate cut on September 18. In our view, the FOMC needs to cut rates further, albeit at a gradual pace, to return the stance of monetary policy to a more neutral setting. While the September jobs report allayed concerns of the jobs market deteriorating in a non-linear way, FOMC members such as Chair Powell and Governor Waller have indicated that the jobs market has become balanced, while San Francisco Fed President Mary Daly, a voter this year, has reiterated she does not want to see it moderate further. If the Committee wants to avoid the labor market cooling beyond the point of comfort, there appears further room to reduce the fed funds rate without rekindling inflation. Although the Committee will receive one more employment report during the blackout period, distortions caused by the impacts of Hurricanes Helene and Milton and a large strike at Boeing lead us to expect the Committee to put much less weight than usual on the report, and focus on the broader trend of the jobs market having cooled substantially over the past year.

Topic for Discussion at the FOMC Meeting: When Should Quantitative Tightening End?

The end-game to quantitative tightening (QT) is a topic that the Committee likely will discuss at the upcoming FOMC meeting. The Federal Reserve has been engaging in QT for more than two years by allowing maturing Treasury securities and mortgage-backed securities (MBS) to roll off its balance sheet up to specified caps each month. The Fed's balance sheet has contracted from roughly $9 trillion in Q2-2022 to about $7 trillion at present (Figure 5). The central bank's holdings of Treasury bills, notes and bonds have dropped by $1.4 trillion while its stock of MBS is down by approximately $450 billion. The Federal Reserve undertook quantitative easing (QE) in the aftermath of the financial crisis and again during the pandemic in an effort to ease monetary policy by more than simply cutting the fed funds rate to roughly 0%. QT is the inverse of QE. That is, QT is meant to remove monetary policy accommodation from the financial system.

The counterpart to the shrinkage on the asset side of the central bank's balance sheet is the equivalent reduction in its liabilities. The Fed's four main liabilities are Federal Reserve notes (i.e., currency in circulation), reverse repo agreements, the U.S. Treasury's "checking account," and the reserves that the nation's commercial banks hold at the central bank. As shown in Figure 6, the reserves of the commercial banking system have fallen by over $1 trillion on balance since late 2021.

Reserves held at the Federal Reserve are an important source of liquidity for the banking system. Maintaining an "ample" amount of reserves is important to the well-functioning of the financial system and critical to ensuring banks have enough ultra-safe, overnight, highly liquid assets to meet their needs. But, at what level should reserves be considered adequately "ample" rather than excessive? The Federal Reserve tracks a wide variety of indicators to assess the degree of scarcity for bank reserves. One key indicator is conditions in the market for Treasury repurchase agreements, also known as the Treasury repo market. Treasury repo transactions form the basis for the secured overnight financing rate (SOFR), a benchmark lending rate in the United States.

Because SOFR is an overnight financing rate, as the federal funds rate is, it generally fluctuates in the FOMC's target range for the federal funds rate, which is currently 4.75%-5.00%. Indeed, SOFR generally has traded near the bottom of the fed funds target range in recent years in a sign that reserves have been more than adequate to keep money market rates stable from day-to-day (Figure 7). However, SOFR briefly traded above the top end of the target range at the end of Q3-2024 amid some quarter-end balance sheet pressures on commercial banks. This recent jump in SOFR at quarter-end suggests that bank liquidity is not as ample as it was when the amount of bank reserves at the Fed was higher.

Although SOFR recently traded a bit above the top end of the target range for the fed funds rate, it subsequently has receded back toward the lower end of the target range for the federal funds rate. Furthermore, the quarter-end overshoot was significantly less than in September 2019 when SOFR spiked by 300 bps. As shown in Figure 6, the level of bank reserves is considerably higher today than in September 2019. However, the assets of the commercial banking system are 34% higher today than they were in September 2019. In other words, the banking system needs more reserves today than it did five years ago.

We do not expect the FOMC to announce an end to QT on November 7. We believe that the Committee will maintain the current monthly pace of balance sheet runoff, currently a maximum of $25 billion of Treasury securities and $35 billion of MBS, for a few months longer, probably until sometime in Q1-2025. But the scramble for liquidity in September 2019 led to dislocations in short-term funding markets that Fed officials seem eager to avoid. Therefore, we believe the Committee will have an in-depth discussion at the upcoming policy meeting about the timeline for the cessation of balance sheet runoff. We will learn more about the discussion, should it indeed take place, when the minutes of the November 6-7 FOMC meeting are published on November 26.

Sunset Market Commentary

Markets

Taking aside corporate news (Volkswagen, Boeing), this morning’s headlines still feature on news terminals. Brent crude fell from $76/b to $72/b after Israel shunned Iranian crude facilities with this weekend’s retaliatory strikes. JPY managed to erase part of the losses following snap parliamentary election results which terminated 15-years of LDP dominance as voters cut them short of a new absolute (coalition) majority. The most likely outcome is a weaker minority government as PM Ishiba gave no signs of stepping down. USD/JPY yoyoed from 152.50 to 154 and back. The fact that we’re still digesting such news is testament to the wait-and-see approach in the build-up to this week’s big events. German Bunds outperform US Treasuries in the run-up to the start of the Treasury’s end-of-month refinancing operation. They kick-off tonight with $69bn 2-yr sale and a $70bn 5-yr auction. Via a $44bn 7-yr Note auction tomorrow, supply focus goes to the Treasury’s quarterly refunding announcement on Wednesday. US yields trade 1-2 bps higher across the curve compared with losses for 2 to 3 bps for German yields. Relative yield dynamics don’t help the dollar with EUR/USD failing to return below 1.08. Later this week, the US publishes the first estimate of third-quarter GDP growth as well as quarterly PCE inflation numbers (Wednesday). Key US labour market data include JOLTS job numbers on Tuesday and (hurricane-affected) October payrolls on Friday. Spotlights are also on Europe with GDP growth released on Wednesday. The economy may have fared better than the dire Q3 PMI readings suggested (0.2% vs flat). Hard data lately often deviated from soft indicators. October inflation most likely picked up again in the EMU. Base effects will make it clear that the current 2% undershoot is temporary.

The Slovak Republic announced a new 7-yr syndication deal, to be launched it the near future (likely tomorrow). Its their second and final syndication of the year following a €3bn 10-yr deal in March. Via multiple regular and a special auction in February, Ardal also raised €7.2bn year-to-date. Add a small FX-deal (CHF; €0.65bn) and they’ll be close to hitting their original €13bn long-term funding target from the start of the year after tomorrow’s deal. That consisted out of €5bn redemptions and an expected budget deficit of €7.6bn. The latter could eventually be nearer to €5.8bn implying that the proceeds of the new 7-yr bond could be partly seen as prefunding for next year. The 2025 funding target will be €12-13bn stemming from €6.5bn bond redemptions and a forecasted deficit of €6.4bn. Ardal targets to raise €6bn via regular monthly auctions and €6bn via syndications.

News & Views

The Confederation of British Industry (CBI) said British retailers reported a fall in sales in October. After reporting only the third positive reading in September (+4), the headline index fell back to -6. Expectations were for an even bigger drop to -10. The CBI’s Principal Economist said that some firms highlighted increasing consumer caution ahead of this week’s Labour Budget as a key factor for the lower sales. The CBI’s wholesale index fell as well, from -8 to -14. The survey’s one-month forward looking gauge shows retailers expecting a flat performance for November. The drop in sales comes after other consumer confidence indicators, including GfK’s on Friday, showed sentiment deteriorating in recent weeks, often tied to uncertainty about the upcoming Budget reveal.

Central-European currencies remain under pressure these days. The Czech koruna underperforms the HUF and PLN but is trading in holiday-thinned circumstances but that doesn’t change the fact that EUR/CZK continues to trade near the recent highs (CZK lows) near but below 25.5. EUR/HUF came close of the 405 mark for the first time since end 2022. Due to the weak forint, bets for further easing by the central bank this year are evaporating. The Polish zloty is set for the lowest close against the euro since mid-2024 (EUR/PLN 4.351). Domestic factors play an important role with a bag of mixed data over the past weeks (eg. awful retail sales last week) fueling expectations for a first rate cut by the central bank perhaps sooner than the majority of the board currently floats (March 2025 instead of Q2?). That said, there’s a common factor pressuring CE currencies lately: Trump’s comeback since mid-September in the polls. Markets increasingly position for a second term, with the expected fiscal largesse pushing US yields higher in the so-called Trump trade. Trump’s foreign policy and the tariff threats in particular would be another hit for these smaller open economies. Lastly, a Trump presidency as well as a changed composition of Congress contains an element of geopolitical uncertainty as to how a Republican-led America will address the Russian conflict.

EUR/USD Edges Higher, German Consumer Confidence Next

The euro has started the new trading week with slight gains. In the North American session, EUR/USD is trading at 1.0817 at the time of writing, up 0.22% on the day. The euro has reeled off four consecutive losing weeks, declining 2.6% during that period.

There are no economic releases out of the eurozone or the US on Monday, which means we can expect an uneventful day for the euro. Germany releases the GfK consumer climate index on Tuesday, which has been in negative territory for three years. The index is expected to improve to -20.2 heading into November, compared to -21.2 for October. German consumers remain concerned due to high inflation and rising unemployment.

ECB eyeing eurozone inflation

Germany releases September CPI on Wednesday and the markets expect inflation to remain below the 2% target. August CPI fell from 1.9% to 1.6%, the lowest since Feb. 2021. Inflation has been falling but the battle is not over as the core inflation rate is at 2.7% and services inflation at 3.8%, well above the 2% target.

The European Central Bank cut rates earlier this month for a third time this year, bringing the key deposit rate to 3.25%. Will the ECB continue trimming at this year’s final meeting in December?

ECB policymakers are split on whether the central bank needs to respond quickly to headline inflation falling below 2%. ECB Governing Council member Pierre Wunsch sounded hawkish on Monday, saying that a soft landing is likely and “there is no urgency” to accelerate rate cuts. Other members want to discuss a 50-basis point move, although the markets have currently priced in a 35-basis point cut as the most likely scenario at the December meeting.

EUR/USD Technical

- EUR/USD tested support at 1.0809 earlier. Below, there is support at 1.0780

- 1.0826 and 1.0855 are the next resistance lines

Australian Dollar at 10-Week Low, RBA Remains Hawkish

The Australian dollar is showing limited movement on Monday. In the European session, AUD/USD is trading at 0.6609, up 0.13%. It has been a bumpy ride for the Aussie, which is coming off a fourth straight losing week and is down a massive 4.4% in October.

RBA’s Bullock says inflation will remain high

The Reserve Bank of Australia meets next week and is widely expected to maintain the cash rate at 4.35%. The RBA has become an outlier among the major central banks, most of which have embarked on a rate-cutting cycle in response to falling inflation. The RBA, however, has been hawkish about rate policy and has discussed the possibility of rate hikes at recent policy meetings.

The RBA’s annual report, published Friday, reiterated that inflation remained high and that inflation would not be sustainable within the 2%-3% target for ‘another year or two’. This signals that the central bank plans to continue its restrictive policy for some time and a rate cut isn’t likely before 2025.

Australia releases third-quarter inflation on Thursday. Headline CPI is expected to fall from 3.8% to 2.9% but core CPI, which is considered more important, and is expected to remain closer to 4%. The cautious RBA is unlikely to consider a rate cut before the core rate is closer to 3%. The RBA peak rate of 4.35% is significantly lower than the peak rate of the Fed, the BoE and the ECB, which means that the RBA won’t have to cut as much its counterparts when its joins the rate-cutting club.

AUD/USD Technical

- AUD/USD tested support at 0.6588 earlier. Close by, there is support at 0.6571

- There is resistance at 0.6617 and 0.6634

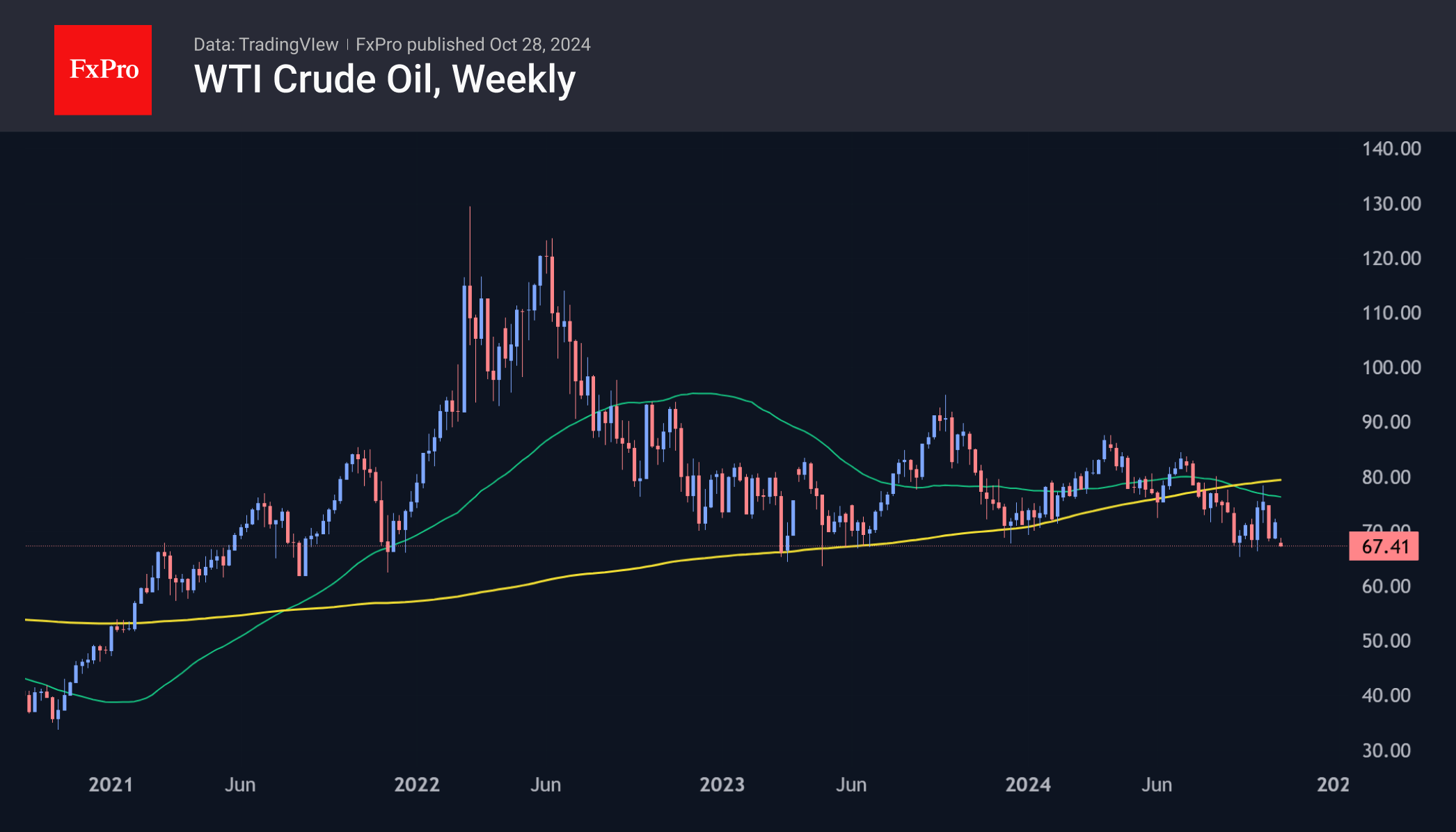

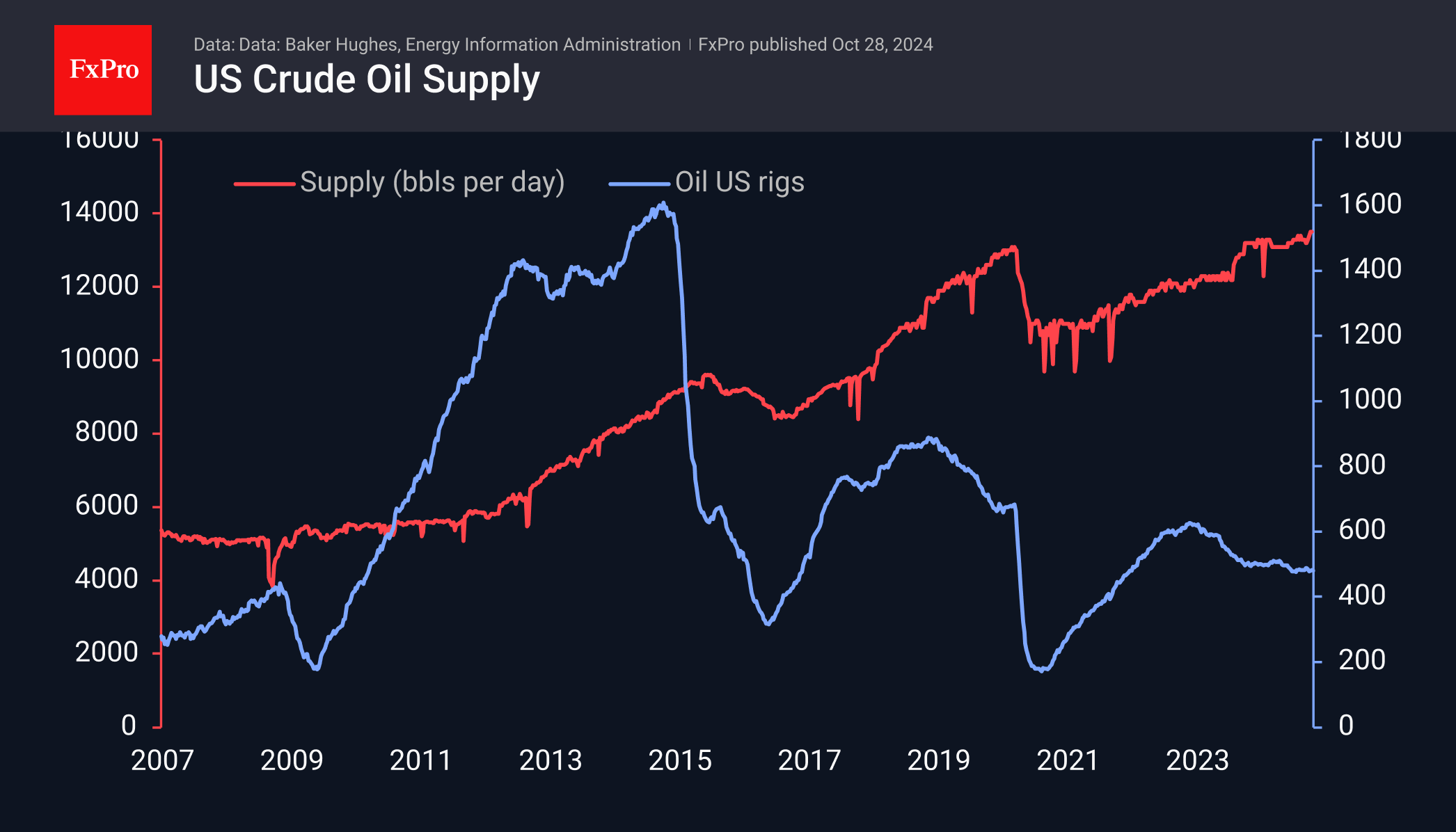

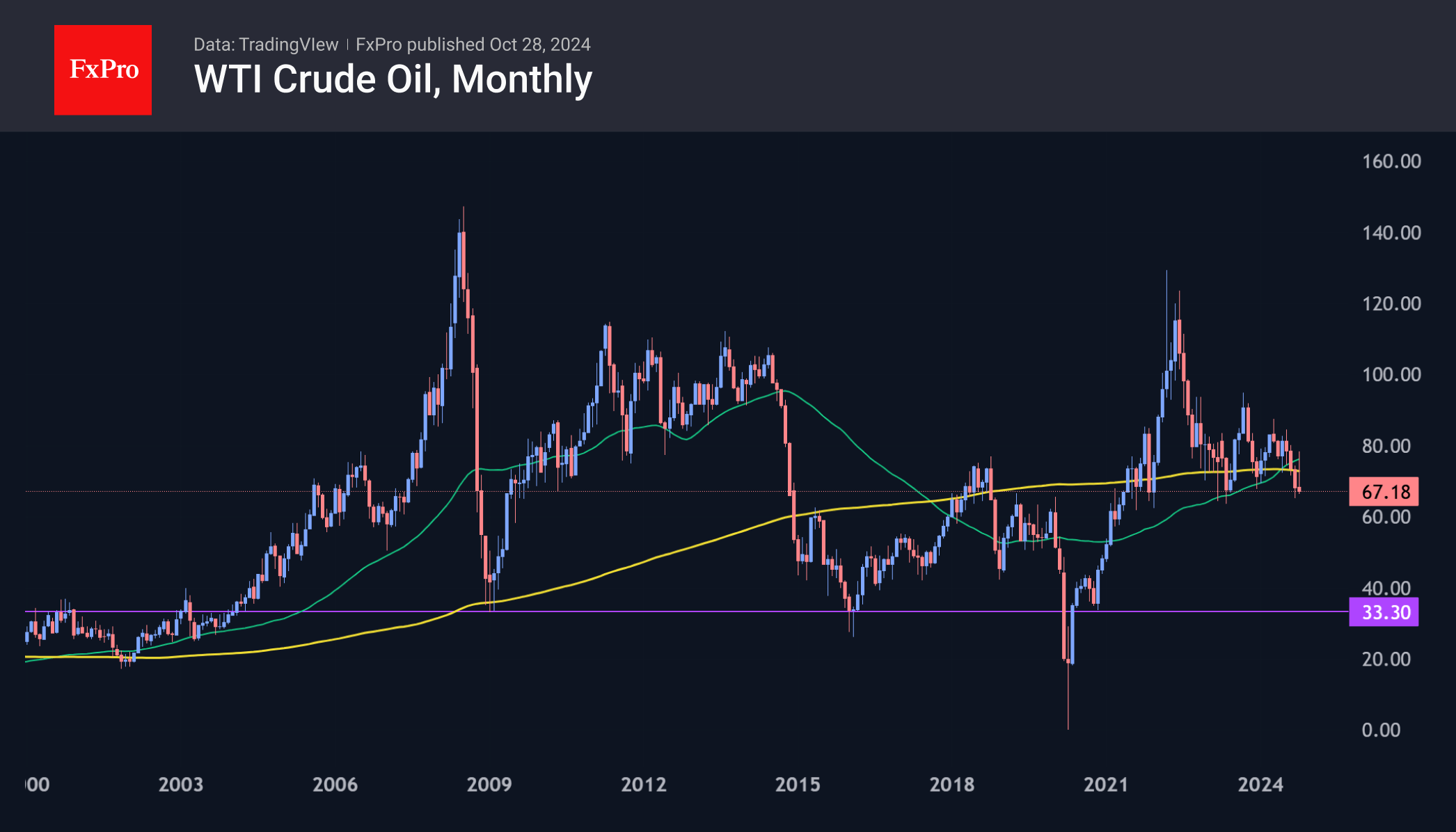

Oil Nears to September Lows; May Crash to $30

The price of crude oil fell by 6% on Monday to $67 a barrel for WTI and $71 for Brent. This return to the lows of the last two months is due to Israel’s attack on Iran’s oil capacity. The aftermath and retaliatory rhetoric from politicians in both countries have fuelled speculation that both sides are trying to avoid escalation for now. As a result, the geopolitical risk premium has fallen sharply. The price has returned to levels seen before the latest escalation in the Middle East.

In September, the price was near the lower end of its 40-month range, reflecting the slowdown in the global economy. Chinese stimulus has so far been disappointing in its slowness and limited nature. It will take months for the G10 monetary easing measures to reach the markets and reverse the economic trends in the major developed economies.

The US continues to produce strongly. Last week was the second consecutive week of record supply from the states, at 13.5 million bpd. At the same time, the number of oil rigs has been falling for almost two years and now stands at 480. The latter indicator is highly correlated with price but has temporarily lost its link with production levels. This is somewhat curious, as it suggests that companies want to squeeze the maximum out of today’s production but limit investment in future production.

The decline in drilling activity with relatively low inventories might be good news if it were not for the increasing contribution of alternative energy sources to the global energy equation. On the oil chart, the recent fall in prices has tipped the balance in favour of the bears. In October, they managed to keep the price above the 50-month moving average (roughly the same as the 200-week moving average), which had been a key support line since the beginning of the year and was broken in August.

As the new week begins, the price is testing the horizontal support of the last two years. A close below $65 in October would be a major bearish signal that could accelerate oil’s decline. There is a risk of a dam bursting, with the next downside target being the $50 area, a psychologically important intermediate level. The history of the 2008-2009, 2014-2015, and 2020 collapses suggests that the final ‘bottom’ may not come until the $30-35 area.

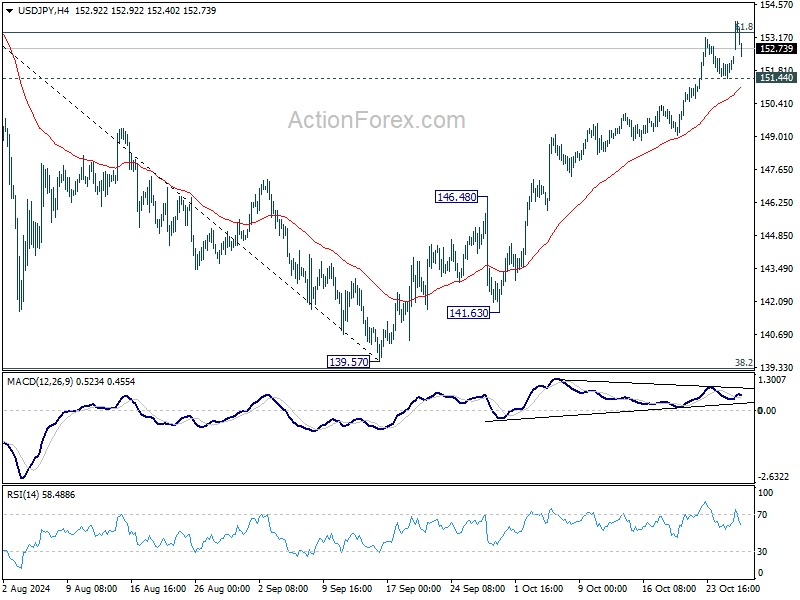

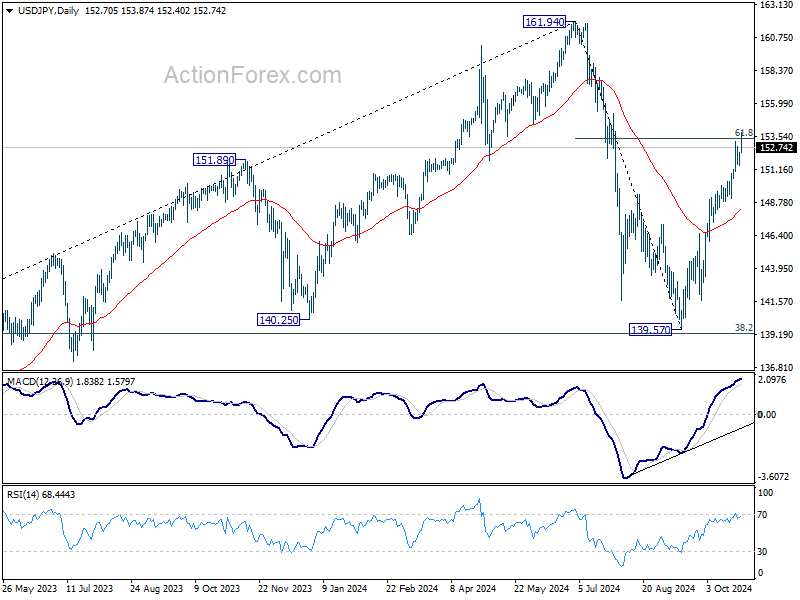

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.68; (P) 152.03; (R1) 152.62; More...

Intraday bias in USD/JPY stays on the upside with 151.44 minor support intact. Sustained trading above 61.8% retracement of 161.94 to 139.57 at 153.39 will pave the way to retest 161.94 high. On the downside, below 151.44 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

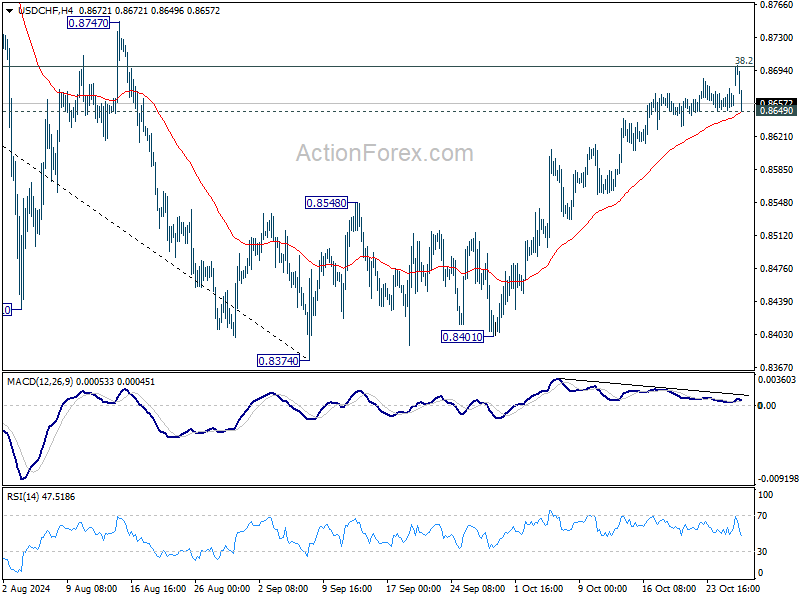

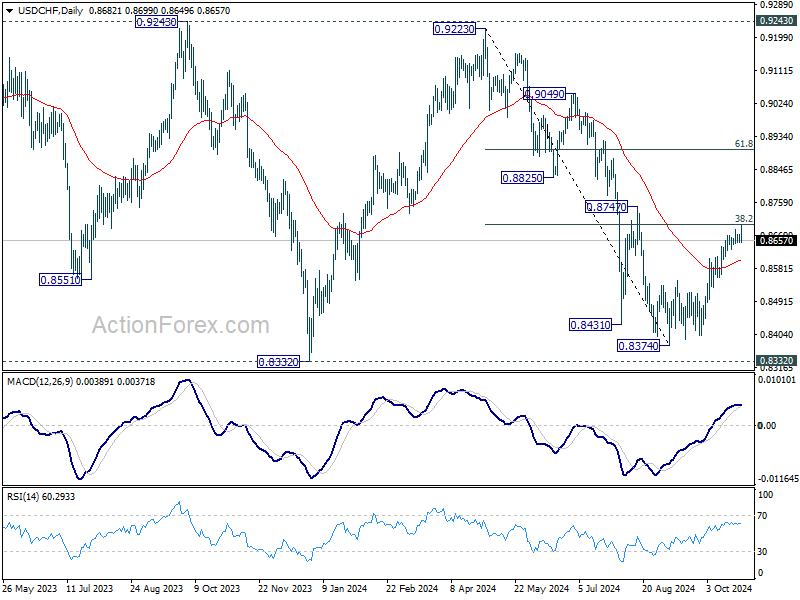

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8652; (P) 0.8664; (R1) 0.8679; More…

Intraday bias in USD/CHF stays mildly on the upside with 0.8469 minor support intact. Decisive break of 38.2% retracement of 0.9223 to 0.8374 at 0.8698 will argue that fall from 0.9223 has completed after defending 0.8332 low. Further rally should then be seen to 61.8% retracement at 0.8899 next. On the downside, below 0.8649 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

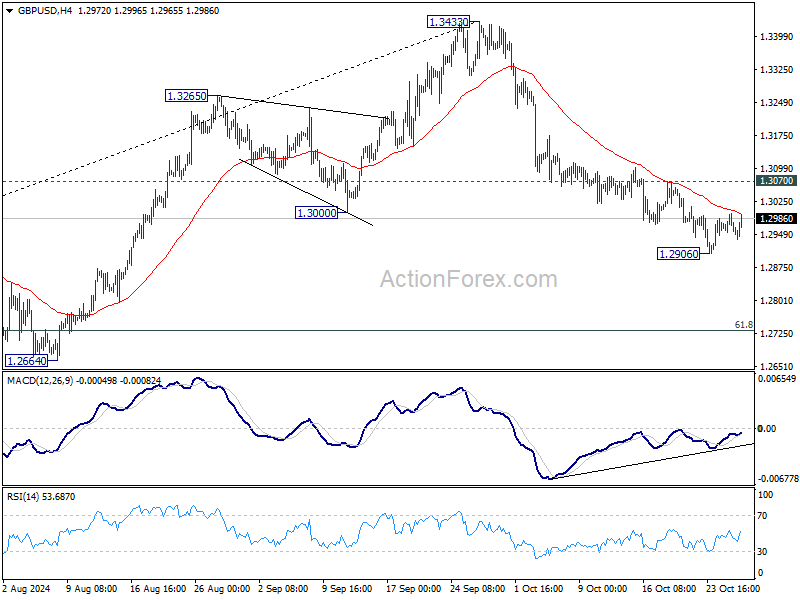

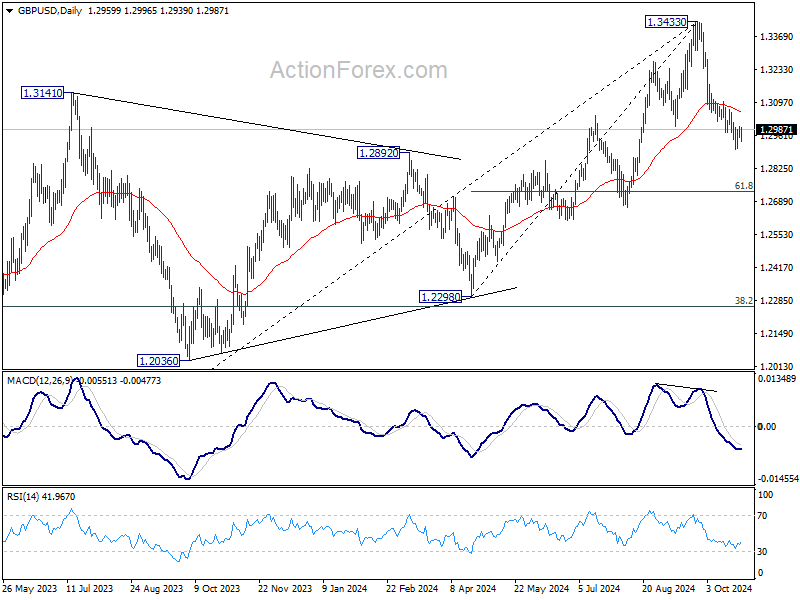

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2946; (P) 1.2972; (R1) 1.2989; More...

GBP/USD is staying in consolidation above 1.2906 and intraday bias remains neutral for the moment. Further decline is expected as long as 1.3070 minor resistance holds. Below 1.2906 will target 61.8% retracement of 1.2298 to 1.3433 at 1.2732. However, considering bearish divergence condition in 4H MACD, firm break 1.3070 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

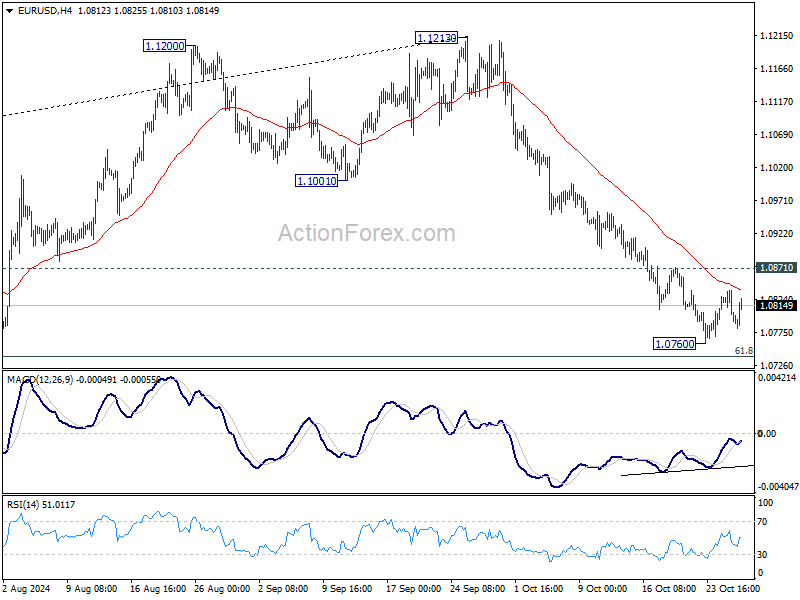

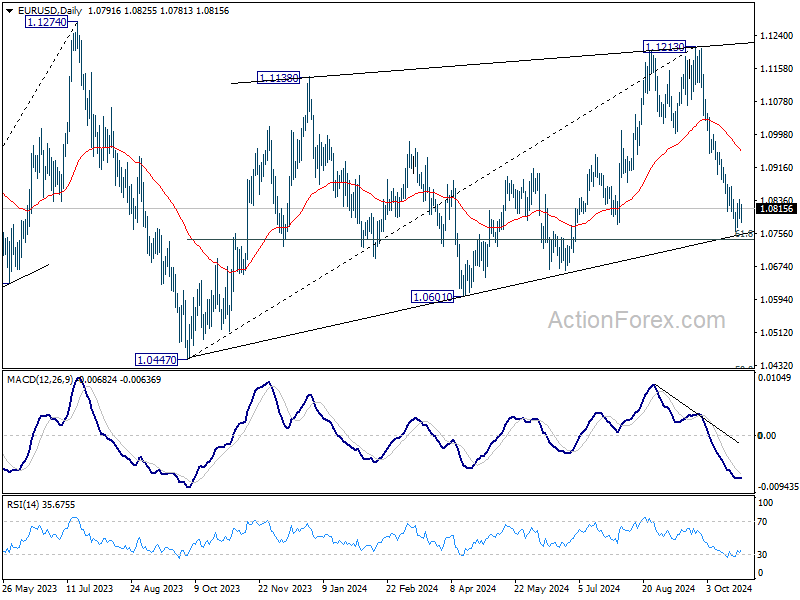

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0780; (P) 1.0809; (R1) 1.0826; More...

EUR/USD is extending consolidations above 1.0760 and intraday bias stays neutral. Further decline is expected as long as 1.0871 resistance holds. Below 1.0760 will target 61.8% retracement of 1.0447 to 1.1213 at 1.0740. Firm break there will target 1.0601 support next. However, considering bullish convergence condition in 4H MACD, break of 1.0871 will indicate short term bottoming, and turn bias back to the upside for 55 D EMA (now at 1.0956).

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

Yen Stabilizes Amid Political Speculation as Wage Growth Hits Record Levels

While Yen remains the weakest performer today, it has managed to recover part of its initial losses following the weekend’s inconclusive election. Investor sentiment stabilized somewhat on hopes that Japan's Liberal Democratic Party could still secure a majority in the lower house through a coalition with Komeito and smaller parties. Reports suggest that the government and ruling coalition are preparing to convene a special Diet session on November 11, leaving room for further political developments in the coming weeks.

Adding to Japan’s economic backdrop, average monthly wages in Japanese businesses reached a record 11,961 Yen this year, surpassing the 10,000-Yen mark for the first time. The 4.1% increase, the highest since 1999, reflects successful spring wage negotiations between management and labor unions, signaling a shift in Japan’s traditionally conservative pay culture. This sustained wage growth suggests that Japanese companies are responding to rising inflation, marking a third consecutive year of increases.

In the broader currency markets, Canadian Dollar follows Yen as the day’s second weakest currency, while Dollar ranks third after giving up early gains. Meanwhile, Euro is leading as the strongest, trailed by British Pound and New Zealand Dollar, with Swiss franc and Australian Dollar positioned in the middle.

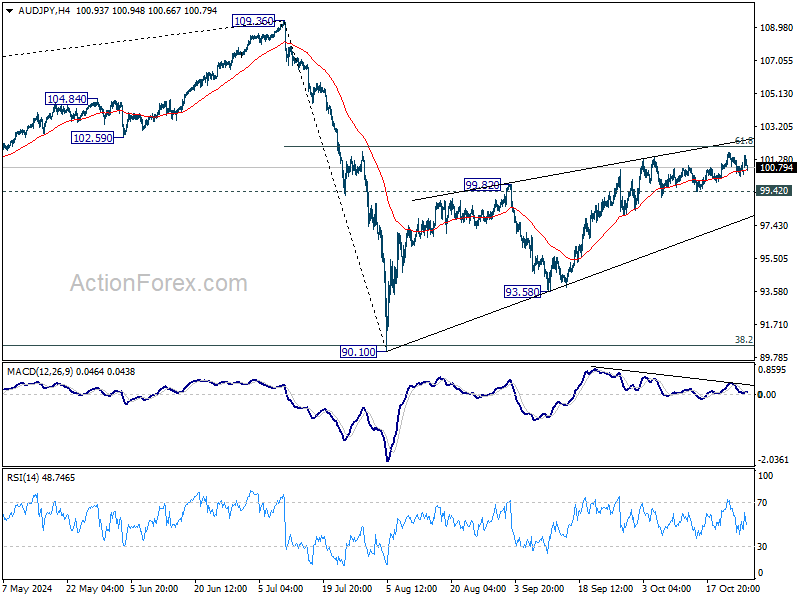

Technically, AUD/JPY has been a laggard in the rallies in Yen crosses today. Bearish divergence condition indicates continuous loss of upside momentum. While another rise cannot be ruled out, strong resistance could emerge at 61.8% retracement of 109.36 to 90.10 at 102.00 to limit upside. Break of 99.42 support should indicate short term topping, and bring deeper fall back towards 93.58 support.

In Europe, at the time of writing, FTSE is down -0.47%. DAX is down -0.25%. CAC is up 0.05%. UK 10-year yield is down -0.0243 at 4.215. Germany 10-year yield is down -0.0029 at 2.266. Earlier in Asia, Nikkei rose 1.92%. Hong Kong HSI rose 0.04%. China Shanghai SSE rose 0.68%. Singapore Strait Times fell -0.26%. Japan 10-year JGB yield rose 0.0227 at 0.975.

ECB’s Wunsch: Soft landing likely, no immediate need to accelerate rate cuts

In an interview with Reuters, Belgian ECB Governing Council member Pierre Wunsch emphasized the importance of patience regarding monetary policy adjustments, pointing to strong employment figures and rising real wages as signals of economic resilience.

Wunsch remarked that with the economy likely headed for a "soft landing," there is “no urgency in further accelerating the easing of monetary policy.”

Wunsch downplayed temporary inflation undershooting, and warned against "overdramatize such an event". He added, "Being a bit below 2% is not a big event if the medium term continues to point to 2%," especially if driven by a favorable terms of trade shock.

Wunsch further cautioned against making premature decisions ahead of December’s ECB meeting, noting that several high-stakes developments are expected in the coming weeks.

"We’ll have so much information until then, including two more inflation readings and new staff projections," he said. "There will be a U.S. election, and we also need to see how the conflict in the Middle East develops, so discussing precise levels is premature."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0780; (P) 1.0809; (R1) 1.0826; More...

EUR/USD is extending consolidations above 1.0760 and intraday bias stays neutral. Further decline is expected as long as 1.0871 resistance holds. Below 1.0760 will target 61.8% retracement of 1.0447 to 1.1213 at 1.0740. Firm break there will target 1.0601 support next. However, considering bullish convergence condition in 4H MACD, break of 1.0871 will indicate short term bottoming, and turn bias back to the upside for 55 D EMA (now at 1.0956).

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.